NEU - NewMarket Is A Cash Cow

2023-04-10 23:41:57 ET

Summary

- Net sales recovered in 2021 from the coronavirus pandemic crisis and continued increasing in 2022.

- Both gross profit and EBITDA margins increased during the past quarter boosted by cost control initiatives along with price increases.

- The company's debt load doesn't represent a significant risk as inventories are highly inflated and cash from operations remains high.

- Aggressive share buybacks are perpetually increasing the position of shareholders holding the company's shares.

- The recent share price decline represents a good opportunity to acquire shares and hold them for the long term.

Investment thesis

NewMarket Corporation ( NEU ) is a company that can be bought and held for decades as it is a leading player in the petroleum additives industry and has very healthy profit margins, which allows for high returns to shareholders in the form of dividends and regular share buybacks. Still, current high inflation rates are having a significant impact on the company's operations as operating costs have increased significantly, but the company has adopted a strategy of cost reduction and product price increases that have boosted margins, which stabilized at very healthy levels during the past quarter.

Despite all this, the inflationary environment continues to impact operations and could continue to reduce profit margins in the coming quarters, and a potential recession as a consequence of interest rate hikes to offset high inflation rates could stress the company's operations even further as a reduction in volumes due to lower demand could further impact profit margins in the foreseeable future. In this regard, current headwinds and a potential recession have caused pessimism and lower expectations for NewMarket Corporation among investors, which has pushed the share price lower, accumulating a total decline of 27.05% from all-time highs of $505.16 in November 2019.

Even so, current cash from operations is enough to widely cover both dividend and interest expenses thanks to high profit margins along with record-high net sales in 2022. This fact, together with inventories of more than half of the company's total long-term debt, makes me consider the recent share price decline as an opportunity for those dividend growth investors with a long-term time horizon.

A brief overview of the company

NewMarket Corporation manufactures and sells petroleum additives, including highly formulated lubricant and fuel additive packages, and antiknock compounds, and also offers contracted manufacturing and related services. Still, petroleum, lubricant, and fuel additives generated 99.60% of the company's total net sales in 2022, so it is the segment in which virtually all of the company's operations take place. The company operates in North America, Europe, Asia, and South America and was founded in 1887. Its market cap currently stands at $3.51 billion, and insiders own a whopping 22.54% of the company's shares outstanding, which means that the management is the main beneficiary of the good performance of the share price.

NewMarket Corporation logo (Newmarket.com)

The company's stated goal is to deliver a 10% compounding return to shareholders per year over a five-year period (earnings per share growth plus dividends). Currently, the company pays a quarterly dividend of $2.10, which represents a 2.28% dividend yield on cost at current share prices, and also performs aggressive share buybacks. These two ways of distributing profits among shareholders are what make NewMarket Corporation a shareholder-friendly company, and those are the same reasons why I believe that holding NEU stock is a good way to build wealth over the years.

Currently, shares are trading at $368.51, which represents a 27.05% decline from all-time highs of $505.16 on November 15, 2019. Certainly, this is a significant decline, especially considering that the company is one of the largest lubricant and fuel additives companies in the world. That is why I believe that NewMarket Corporation deserves to be considered as a potential opportunity for long-term dividend growth investors at current share prices. But before jumping in, it is important to look in depth at the recent evolution of the company, as well as the current headwinds and potential risks.

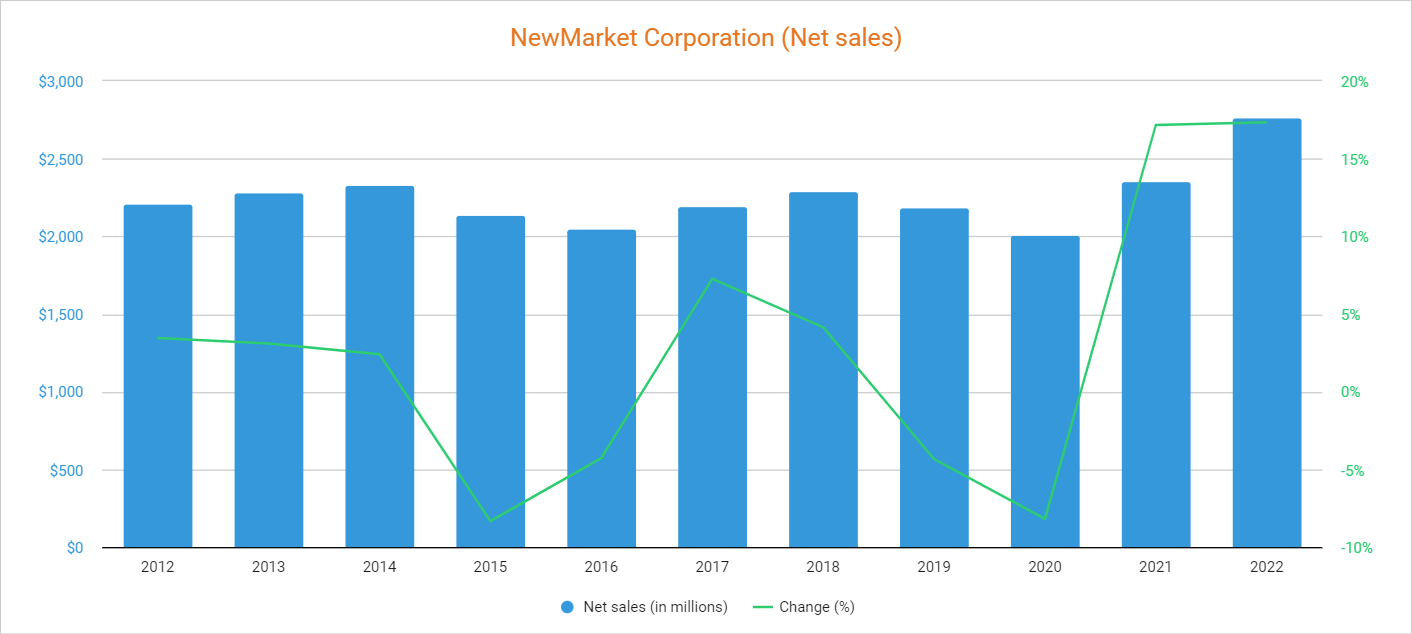

Net sales are at record highs as the company has recently increased the price of its products

The company's net sales have remained stagnant for many years and declined by 4.34% in 2019, and by 8.19% in 2020 as a result of restrictions during the worst period of the coronavirus pandemic crisis. Nevertheless, net sales recovered in 2021 as they increased by 17.17%, and reached all-time highs in 2022 as they increased again by a further 17.35% (despite a 2.9% decline in shipments as a consequence of the Russia-Ukraine war) due to product price increases carried out to transfer the increase in the cost of production to customers. In this regard, net sales in the Petroleum additives segment in 2022 were 26% higher than those of 2019, before the coronavirus pandemic crisis, and shipments were also 5% higher compared to 2019.

NewMarket Corporation net sales (10-K filings)

{kind=link}

On a quarterly basis, net sales increased by 16.93% year over year during the first quarter of 2022, 22.50% during the second quarter, 11.87% in the third quarter, and 18.38% in the fourth quarter, so nothing points to a slowdown in sales. Still, concerns of a potential recession are increasing over time as central banks raised interest rates to combat high inflation rates. Using 2022 as a reference, 35.26% of net sales are generated within the United States, whereas 29.21% take place in Europe, the Middle East, Africa, and India, 15.76% in Asia Pacific, 6.56% in China, and 13.20% in the rest of the world.

The recent share price decline along with increasing net sales have caused a drastic drop in the P/S ratio, which currently stands at 1.338. This means the company generates net sales of $0.75 for each dollar held in shares by investors, annually, which I consider to be quite high considering the company's strong ability to convert sales into actual cash.

This ratio is 34.47% lower than the average of 2.042 during the past decade and represents a 50.52% decline from decade-highs of 2.704. This means that investors are placing less value on the company's sales due, firstly, to a higher debt load as a result of strong share buybacks carried out in recent years, and secondly, due to the recent margin contraction as a result of inflationary tensions on the verge of a potential recession that could push these margins to even lower levels than current ones. Still, margins are starting to show signs of improvement thanks to product price increases, which is translating into strong cash from operations.

Margins are recovering after a slump caused by inflationary pressures

The company's margins have been significatively impacted by the coronavirus pandemic crisis in 2020, worldwide supply chain disruptions in 2021, and high inflation rates and the war between Russia and Ukraine in 2022. Nevertheless, the headwinds from 2022 are still present and are expected to remain a challenge for the whole of 2023. And now, a potential recession is a scenario that is increasingly seen as a possible reality in the short to medium term. But returning to the company's profitability, operating profit increased in 2022 mainly due to increased selling prices, but higher raw material and operating costs continue to have a significant impact on profit margins. In this regard, the company's gross profit margin was 23.17% in 2022, and the EBITDA margin was 16.83% as the company reported a net income of $280 million for the full year.

Still, margins started to show strong signs of improvement during the past quarter as the company reported a net income of $91 million thanks to a gross profit margin increase to 26.31% and an EBITDA margin improvement to 20.33%, boosted by strong pricing action and cost control initiatives. In this regard, margins are under control, so the next aspect to take into account to determine the resources that the company has to navigate current headwinds and a potential recession is its debt position, which is, in my opinion, widely manageable.

The company's debt is highly manageable

Dividend payouts and especially aggressive share buybacks have caused a significant increase in the company's long-term debt, which has tripled in the past 10 years to $1 billion. Still, the company's debt position doesn't represent a significant risk despite low cash and equivalents of $68.7 million as it closed 2022 with a net debt to EBITDA at 2 times.

In addition, the company has expanded its inventories since 2021 to $631 million, which is more than half of the company's total long-term debt. This greatly reduces the risk that debt entails for the company as these inventories can be easily converted into cash.

Despite this, there is no guarantee that the management will use the company's inventories to reduce their outstanding debt as they have a tradition of distributing more cash than generated through dividends and aggressive share buybacks. The good point is that the outstanding shares withdrawn from the market could be reissued in the future (albeit at a price possibly lower than the current one) if cash from operations decreases and cannot cover dividend and interest expenses. Still, both expenses are being covered quite easily at present, so things would have to get much worse before operations would struggle to continue covering them.

The dividend is safe as it represents a slow portion of the company's cash from operations

The company has more than doubled its dividend payout in the past 10 years and the latest raise was announced in October 2021 when it announced a quarterly dividend of $2.10 per share, which represented a 10.53% rise compared to the previous dividend payout.

Thanks to these raises and the recent share price decline, the dividend yield currently stands at 2.28%, which is very generous considering the low cash payout ratio over the years. In the following table, I have calculated the dividend cash payout ratio by calculating what percentage of the cash from operations has been used over the years to cover the dividend and interest expenses. In this way, we can determine the sustainability of the dividend through actual operations, and then I'll take a deeper look at the company's ability to cover both expenses during the last quarter of 2022 and the full year.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $235.0 |

| $268.0 |

| $353.4 |

| $242.8 |

| $197.9 |

| $337.2 |

| $284.20 |

| $165.3 |

| $108.6 |

| Dividends paid (in millions) |

| $59.4 |

| $70.8 |

| $75.8 |

| $82.9 |

| $80.4 |

| $81.7 |

| $83.4 |

| $85.9 |

| $84.3 |

| Interest expense (in millions) |

| $23.7 |

| $17.7 |

| $21.8 |

| $21.9 |

| $26.7 |

| $29.2 |

| $26.3 |

| $34.2 |

| $35.2 |

| Cash payout ratio |

| 35.36% |

| 33.02% |

| 27.62% |

| 43.16% |

| 54.11% |

| 32.89% |

| 38.60% |

| 72.66% |

| 110.04% |

As we can see, the company typically covers the dividend and interest expenses with less than 50% of the cash from operations, although said ratio exceeded 70% during 2022 as a result of abnormally low cash from operations of $108.6 million. Nevertheless, inventories increased by $132.9 million year over year, and accounts receivable by $67.9 million while accounts payable only increased by $27.2 million, which means the company can cover the $119.5 million dividend expense and interest expenses with plenty of room through its operations.

As for the past quarter, cash from operations was $92.7 million (which represents a 357% increase year over year) and inventories increased by $39.2 million quarter over quarter, but accounts receivable declined by $91.5 million while accounts payable declined by only $12.2 million. In this regard, the cash from operations and the increase in inventories, as well as the reduction in accounts payable despite a reduction in accounts receivables, mean that the company could cover its dividend and interest expenses with approximately half of the cash generated annually through its operations ( using the last quarter as a reference), so the dividend is pretty safe so far, and excess cash is allowing for continuous share buybacks, which are significantly reducing the total number of shares outstanding.

Share buybacks represent a way of returning cash to shareholders

The company regularly conducts share buybacks in order to distribute returns among investors. This serves to reduce the number of outstanding shares and thus improve per-share metrics since thanks to share buybacks each share represents a growing portion of the company over time. In fact, the total number of shares outstanding declined by 27.24% during the past 10 years. Such a significant decrease is possible thanks to the fact that the company invests more cash in buybacks than in dividends as it delivered $84 million to shareholders in the form of dividends and $208 million through share repurchases in 2022. During the announcement of the latest dividend raise in October 2021, the company's board of directors approved a $500 million share buyback program through December 2024, so share buybacks are expected to go on for a long time.

This means that investors can expect to see their company's stake increase over time, which will not only improve per-share metrics but also the company's ability to continue increasing dividends by distributing them among fewer shares.

Risks worth mentioning

Although it is true that the company has a risk profile that I consider as quite low, there are some risks that I would like to highlight related to the short to medium term.

- Despite a recent improvement, profit margins could contract again if inflationary tensions continue to impact the global economy, and more specifically the company's operations.

- A potential recession as a consequence of the recent interest rate hikes could negatively affect the company's volumes, which would lead not only to a reduction in net sales but also in profit margins. This could lead to a further decline in the share price as well as a higher dividend cash payout ratio.

- The speed at which the company performs share repurchases could slow down in the coming quarters and years as a result of a higher debt load (and thus higher interest expenses) if cash from operations is negatively impacted by further inflationary pressures or a recession materializes.

Conclusion

NewMarket Corporation's operations are very profitable and the balance sheet is very robust despite recent inflationary headwinds, with which I consider that the recent share price decline represents a good opportunity to acquire shares for any dividend growth portfolio as the company is very shareholder-friendly thanks to dividend payouts and aggressive share buybacks. Furthermore, inventories of $631 million are resources that the company could convert into cash if inflationary headwinds intensify in the short to medium term or if a recession finally takes place.

The increase in product prices has allowed the company to stabilize profit margins at healthy levels and achieve record net sales despite a slight decline in shipments due to the war between Russia and Ukraine, which will also help to dilute part of the debt contracted in recent years used to make aggressive share buybacks. That is why I believe that holding shares of NewMarket Corporation continues to be a good way to build wealth over the years.

For further details see:

NewMarket Is A Cash Cow