NEM - Newmont: An Opportunity To Buy At The Deepest Discount In Years

2023-10-26 06:52:54 ET

Summary

- Newmont stock has dropped 56% from its 2022 high, creating a rare buying opportunity.

- Weak operational and financial results, as well as the pending merger with Newcrest, have contributed to the stock's recent decline.

- The second half of 2023 is expected to see improved performance and the company has a strong 5-year outlook.

- Newmont is superior to Barrick, yet trades at a similar market cap and EV. There is 30-40% upside in NEM in order to get in line with the valuation of GOLD.

I'm going to put it bluntly: An opportunity like this in Newmont ( NEM ) doesn't come around often. Think once or twice a decade.

I'm no stalwart NEM bull. I wasn't constructive on the stock over the last several years because it was trading at a high relative value compared to its peers, such as Barrick Gold ( GOLD ).

However, NEM is down 56% from its 2022 high of $80+ per share and has significantly underperformed the sector. For a small or mid-cap gold producer, a decline of that magnitude isn't unusual, but for the largest gold company in the world, it's rare to see such a dramatic loss, especially over a relatively short period.

Over the last year, NEM has notably lagged behind the sector and its peers, as the shares are off by 11%, while the HUI, Agnico Eagle ( AEM ), and Barrick are up 16%, 18%, and 11%, respectively. Over the last week, NEM is down over 6% and has lost considerable ground, especially compared to its closest rival (i.e., GOLD), which is up over 5%. That's a 12% spread.

So what's going on with the stock, why has it dropped to such a degree, and why is this such an opportunity? I will now address all of these questions.

What Goes Up, Must Come Down

From the 2011 peak in the sector up until the spring of 2022, NEM was up almost 50%. Not only did it completely recover from the depths of the bear market lows, but it tacked on substantial gains. This was all occurring as the rest of the sector was still sitting on 40-50% losses. NEM became overly stretched starting from 2020 onward, as it had just closed the Goldcorp acquisition, was generating all-time high operating and free cash flow, and the price of gold spiked to $2,000. As the largest gold miner in the world, NEM is usually the first gold stock that investors/institutions buy if they want to gain exposure to the sector and rising gold prices. Most aren't familiar with the other names in the sector, which makes NEM a go-to stock. Considering the company was also outperforming operationally, it led to a surge in buying.

Newmont's valuation simply became overextended by a significant degree a year and a half ago, at least on a relative basis. And what goes up must come down. The outperformance and lofty stock price weren't sustainable unless gold broke out to new all-time highs, which it didn't.

The entire sector came under pressure as Newmont's stock price peaked, and NEM plunged with the rest of the group, underperforming on the way down.

Explaining The Recent Weakness

While the sector has been in recovery mode over the last year, NEM has continued to lose more ground, and there are two reasons for the recent share price weakness:

1. The Pending Merger With Newcrest

Newmont made a ~US$17 billion bid for Newcrest Mining ( NCMGF ) in February of this year, which Newcrest's Board rejected.

Over the following three months, the two companies continued discussions and completed further due diligence on one another. NEM upped its offer to ~US$19 billion in May, which Newcrest accepted.

Rarely does the acquirer in this sector see its stock price increase in value during a pending merger, especially if there is uncertainty surrounding the price that will ultimately be paid for the acquiree.

Newcrest also reported disappointing Q3 results last week (mostly due to scheduled maintenance at many of its mines), but the company paid a special dividend as well. There are currently a few moving parts and increased volatility in Newcrest's shares, and there's been a notable increase in volume and selling in NEM. Either some arbitrage players and/or institutional selling is probably negatively impacting NEM.

The pending merger with NCMGF has most certainly weighed on Newmont over the last eight months.

2. Weak Operational And Financial Results

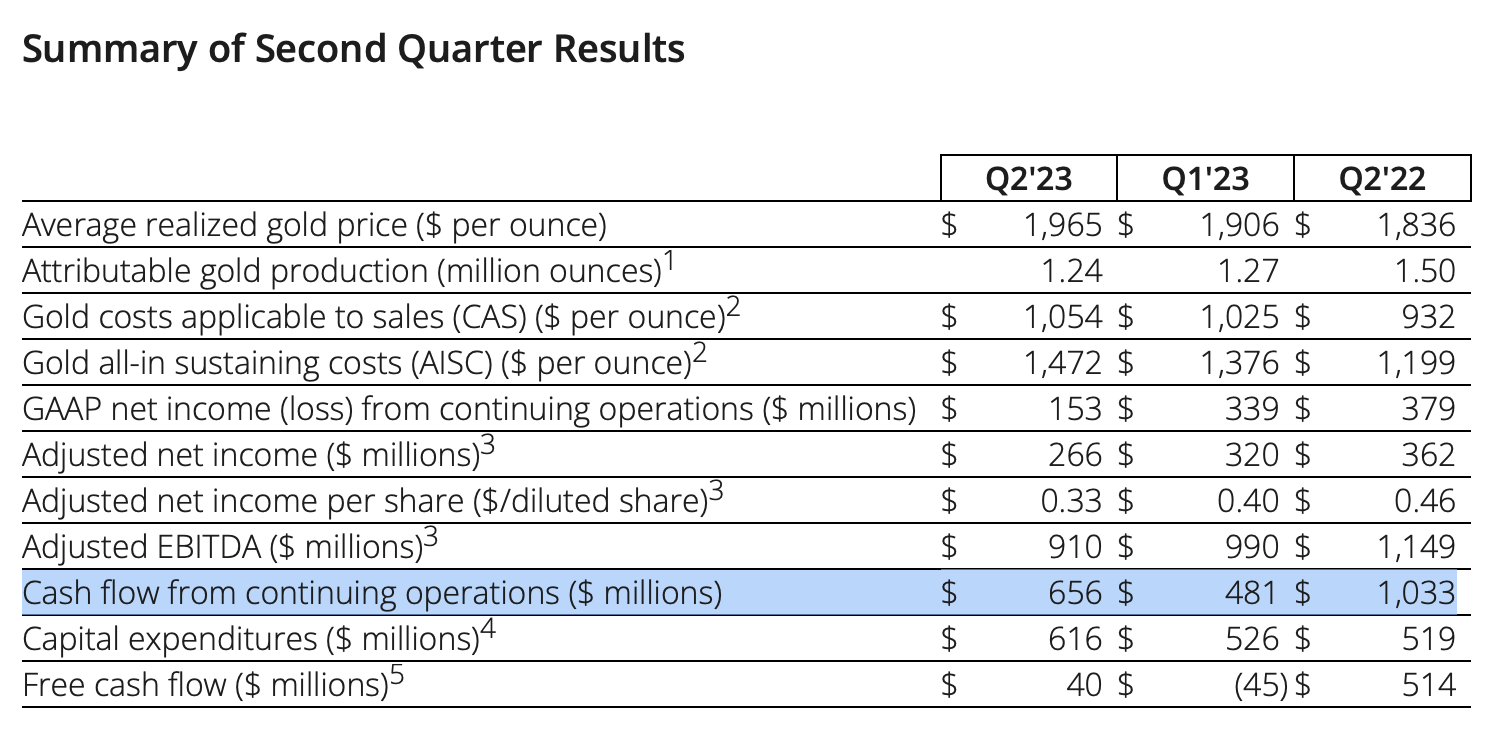

NEM declined 5% the day the company reported discouraging Q2 2023 financial results, which included still significantly high AISC. The company sold gold at $1,965 in the second quarter, or more than $100 per ounce higher than the prior-year quarter, but AISC was $1,472, or an almost $300 increase compared to Q2 2022. Operating cash flow increased QoQ, but it was well below last year when gold prices were lower. Free cash flow was also a paltry US$40 million as the company continues to spend heavily on CapEx.

{kind=link}

Production was expected to be weighted to the second half of the year, but Q2 2023 was also impacted by several other events, including the strike at Peñasquito, the temporary halt of production at Éléonore due to the wildfires in Canada, the pausing of mining for two weeks at Cerro Negro for safety inspections and to reinforce "the Newmont way" to the workforce (i.e., proper safety), and the decision to process lower grade stockpiles at Akyem in Q2 (originally planned for Q4) in order to optimize the mine plan.

Peñasquito also remained shut down during Q3 as the strike continued, which has also likely negatively impacted the stock as it's the company's largest operation on a gold equivalent basis.

Why It's Now Time To Buy NEM

1. A Much Improved Second Half of 2023 And Strong 5-Year Outlook

The second half of this year will look dramatically different than the first half. Ahafo will see higher grade and tonnes mined from the Subika open-pit and underground operations, Cerro Negro is expected to be mining higher grade stopes, Tanami will see more tonnes mined and processed with the highest grades coming in Q4, higher grades are expected at Akyem, and the Nevada joint venture and Pueblo Viejo are both expected to be weighted "strongly toward the second half of the year."

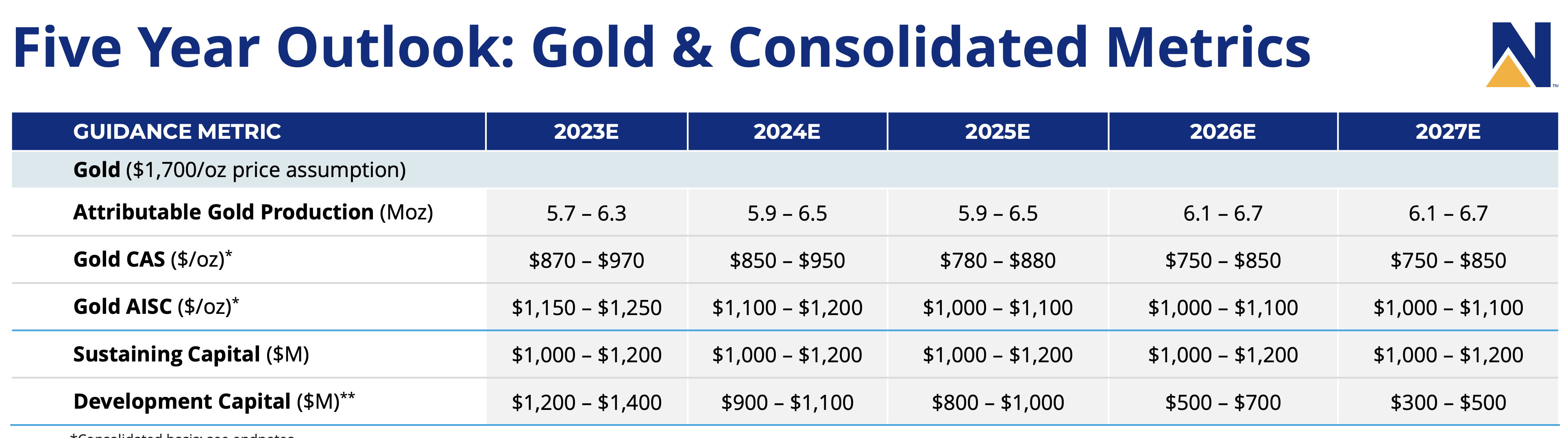

Newmont reiterated its guidance for the year of between 5.7 and 6.3 million ounces of attributable gold production and AISC between $1,150 and $1,250 per ounce. Through Q2 2023, the company produced 2.5 million ounces of gold at an AISC of $1,424 per ounce, indicating that second-half production should be 3.2-3.8 million ounces of gold and sharply lower AISC.

As we are in Q4, these improvements are happening now. So we have bullish catalysts hitting, just not yet reported.

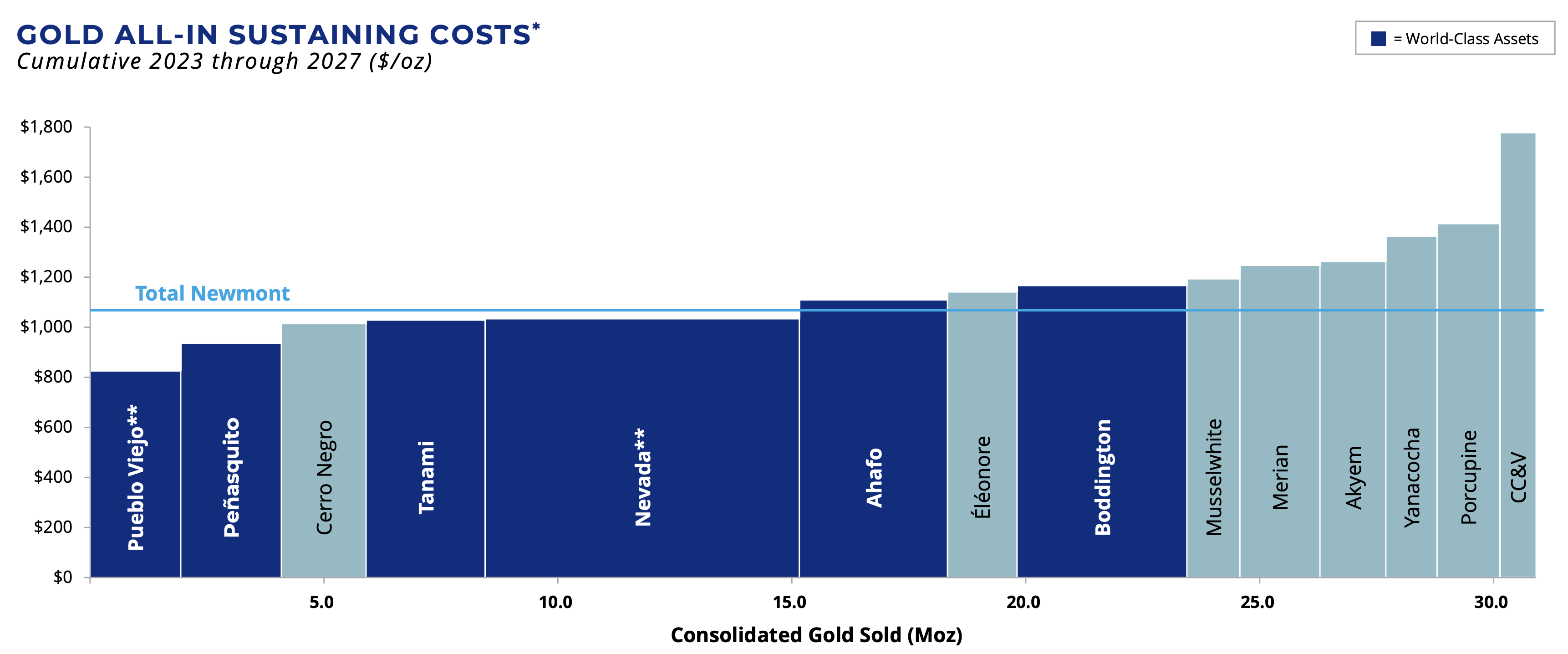

Investors are selling NEM because of a short-sighted view, as they believe the high AISC and low cash flow will continue. But Newmont's portfolio of assets is exceptional, and most of its mines are lower cost, as evidenced by the expected AISC from 2023-2027 for each individual operation. H1 2023 isn't indicative of the future.

{kind=link}

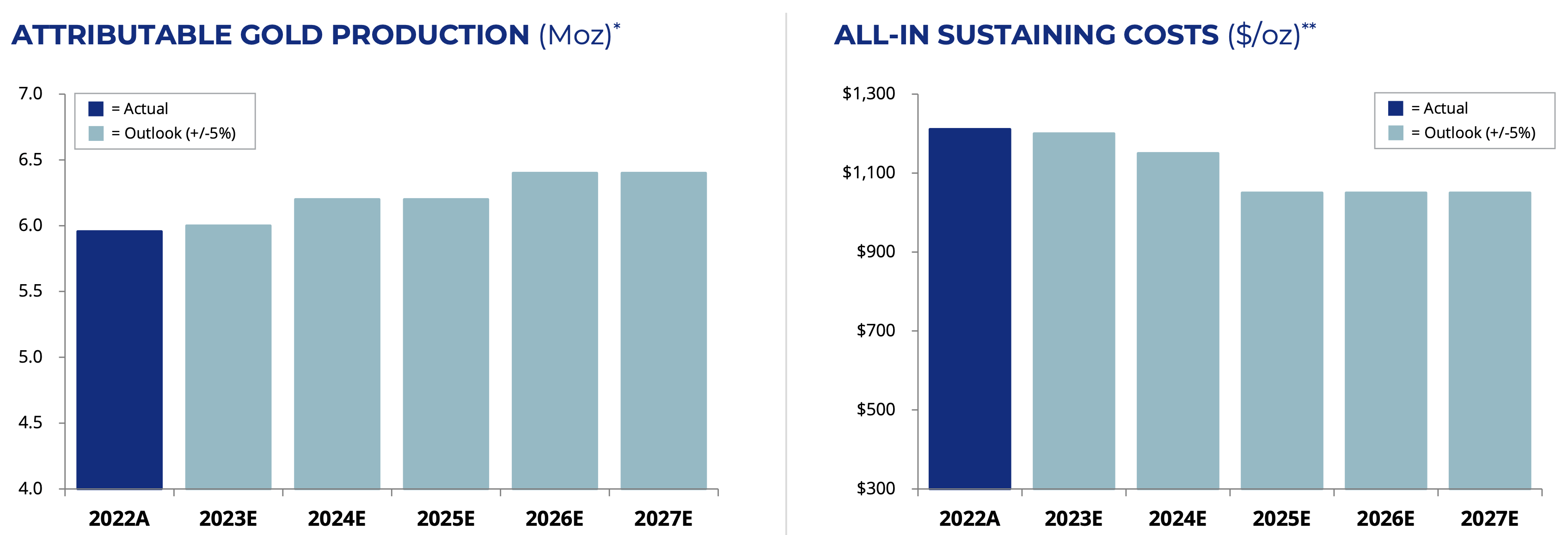

Newmont is also spending heavily to solidify its current portfolio, which will begin to pay dividends in two years. The Tanami Expansion 2 and Ahafo North project will result in an increase in production and lower costs. The company is spending over $2.5 billion on growth projects, and output is expected to potentially reach 6.7 million ounces by 2026. The five-year outlook shows progressive increases in production and decreases in AISC, with AISC dropping to as low as $1,000 per ounce by 2025. Even if continued inflationary pressures prevent Newmont from achieving its cost targets, this outlook gives it a $150-$250 per ounce buffer to maintain its current AISC. In other words, if the industry sees a ~$200 per ounce increase in costs over the next 3-5 years, Newmont's AISC would remain flat, giving it a tremendous competitive advantage.

{kind=link}

{kind=link}

Last week, NEM also announced it had reached an agreement with the union at Penasquito, and the strike has ended, which gives even greater confidence for the short and long-term outlooks.

2. The Acquisition Of Newcrest Will Make NEM By Far The Largest And Best Gold Miner On The Planet

The production and AISC outlook above doesn't include the pending Newcrest acquisition, which will result in an additional ~2 million ounces of annual gold production and a substantial increase in copper output.

Newcrest also has lower AISC than Newmont, and the former expects AISC to decline well below $1,000 per ounce over the next several years, so Newmont's margins will also improve because of this merger.

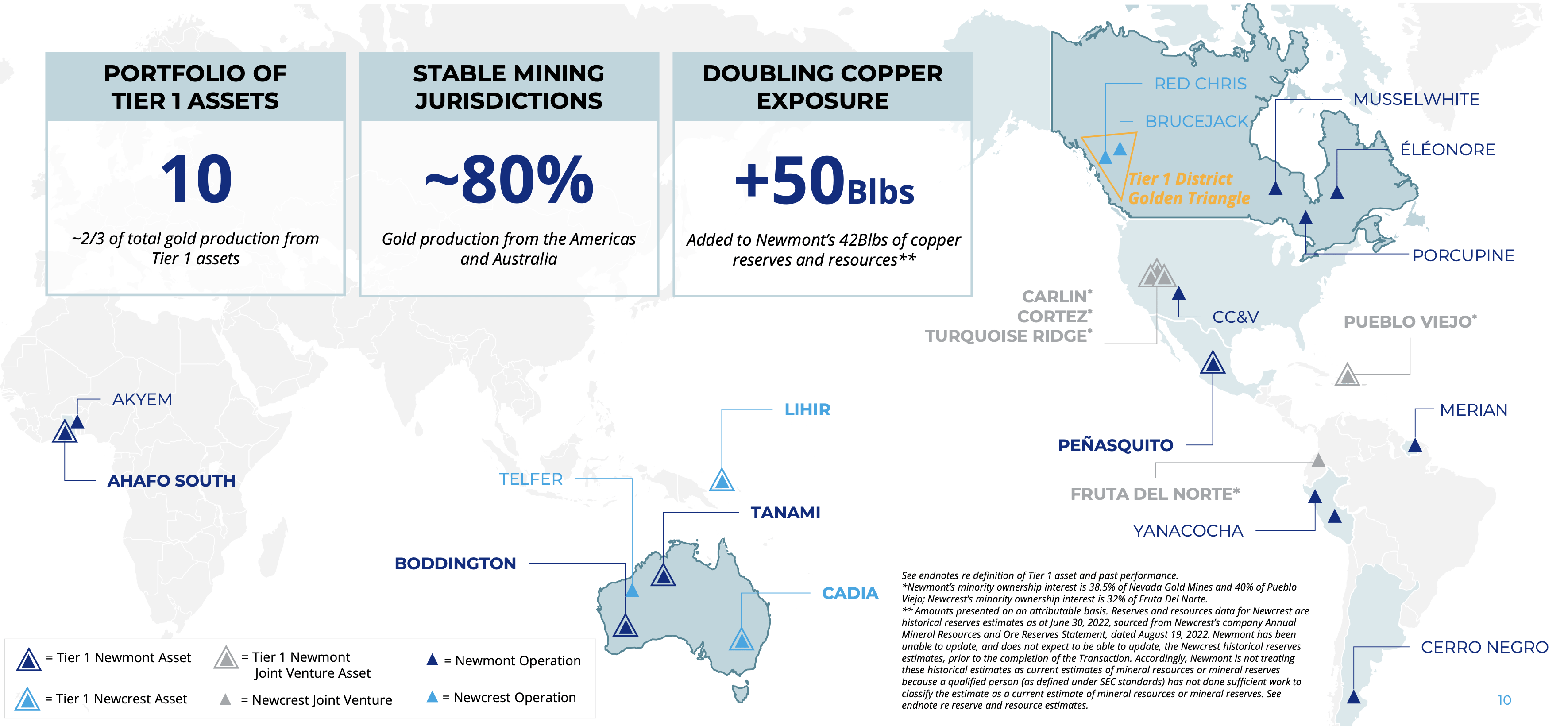

Once the deal closes, which is expected to occur in the next week or two, it will make NEM by far the largest and best gold miner on the planet, with a portfolio containing a whopping 10 Tier 1 assets with 80% of production from the Americas and Australia.

It's an incredible portfolio, one that is tremendously well-diversified.

Let's start in Canada, head south, then take a trip east around the rest of the world. You have the high-grade, low-cost Brucejack mine in Canada, along with the Musselwhite, Éléonore, and Porcupine mines in the country. The latter three (which aren't Tier 1 assets) have struggled with costs, and Éléonore never turned out to be the mine that was originally anticipated, but they are still producing ~800,000 ounces of gold per year combined and generating solid cash flow at current gold prices. Red Chris, located in the Golden Triangle, is a small-scale operation, but it contains considerable gold and copper and could be a multi-decade Tier 1 Au/Cu mine if fully developed. The NGM (Nevada Gold Mines) JV with Barrick contains a host of Tier 1 assets (Carlin, Cortez, and Turquoise Ridge) that produce over 3 million ounces per year on a 100% basis (Newmont owns a 38.5% stake in the JV). These are truly world-class assets. Pueblo Viejo in the Dominican Republic is also a JV with Barrick, and with the plant expansion complete, Pueblo Viejo could ramp up to 1 million ounces of gold production per year on a 100% basis. Peñasquito is another world-class mine; a polymetallic orebody that produces over 300,000 ounces of gold and 30 million ounces of silver annually and is the second-largest silver mine on the planet. Newmont will gain exposure to the high-grade, low-cost Fruta del Norte mine via Newcrest's 32% equity interest in Lundin Gold, the owner of the operation. Merian is a solid asset producing over 300,000 ounces of gold per year. Newmont is currently expanding the high-grade Cerro Negro mine in Argentina, which will increase annual output from this low-cost operation to more than 350,000 ounces and extend the mine life through 2034. Jumping the Atlantic Ocean, Ahafo is another Tier 1 mine, with the currently-in-development Ahafo North project expected to add 300,000 ounces of gold production annually for the first five years of its mine life, with combined production from both Ahafo North and Ahafo South of over 700,000 ounces at an AISC of likely ~$1,000 or below. Then, a hop over the Indian Ocean to Australia and PNG, and there are a handful of just monster gold deposits with substantial copper production. Bringing Newmont's Boddington and Tanami operations and Newcrest's Telfer, Cadia, and Lihir mines under one umbrella will make NEM the largest regional gold play, as they are some of the most sizable gold mines in the world. I didn't mention every mine in production or all of the projects (such as Wafi-Golpu), but the point is the portfolio is extensive and high-quality. It's the best of the best. Nobody comes close.

{kind=link}

{kind=link}

Just as important, if one of these mines goes down, it won't be detrimental to Newmont. The breadth and quality of the assets cannot be understated.

3. Substantial Synergies And Asset Sales Will Further Bolster The Balance Sheet

Once the Newcrest acquisition is complete, Newmont expects to realize US$500 million in annual synergies from G&A consolidation, supply chain savings, and operational improvements. So there are additional margin expansion opportunities over the next 1-2 years.

Newmont also expects to realize ~$2 billion of cash from portfolio optimization (i.e., asset sales) over the next two years. Mature (e.g., Telfer) and non-core (e.g., Havieron) operations will be monetized, although it's not exactly clear which mines Newmont is looking to sell, and Telfer and Havieron are only two potential candidates.

Newmont had a US$3.2 billion war chest at the end of Q2 2023 and only ~US$2.3 billion of net debt. Newcrest will bring about ~US$2 billion of net debt to the table (accounting for the special dividend paid), which non-core asset sales will fully cover. The $5+ billion of annual operating cash flow from the combined entity and the free cash flow generation potential will likely result in NEM having zero net debt within a year or two at current gold and copper prices.

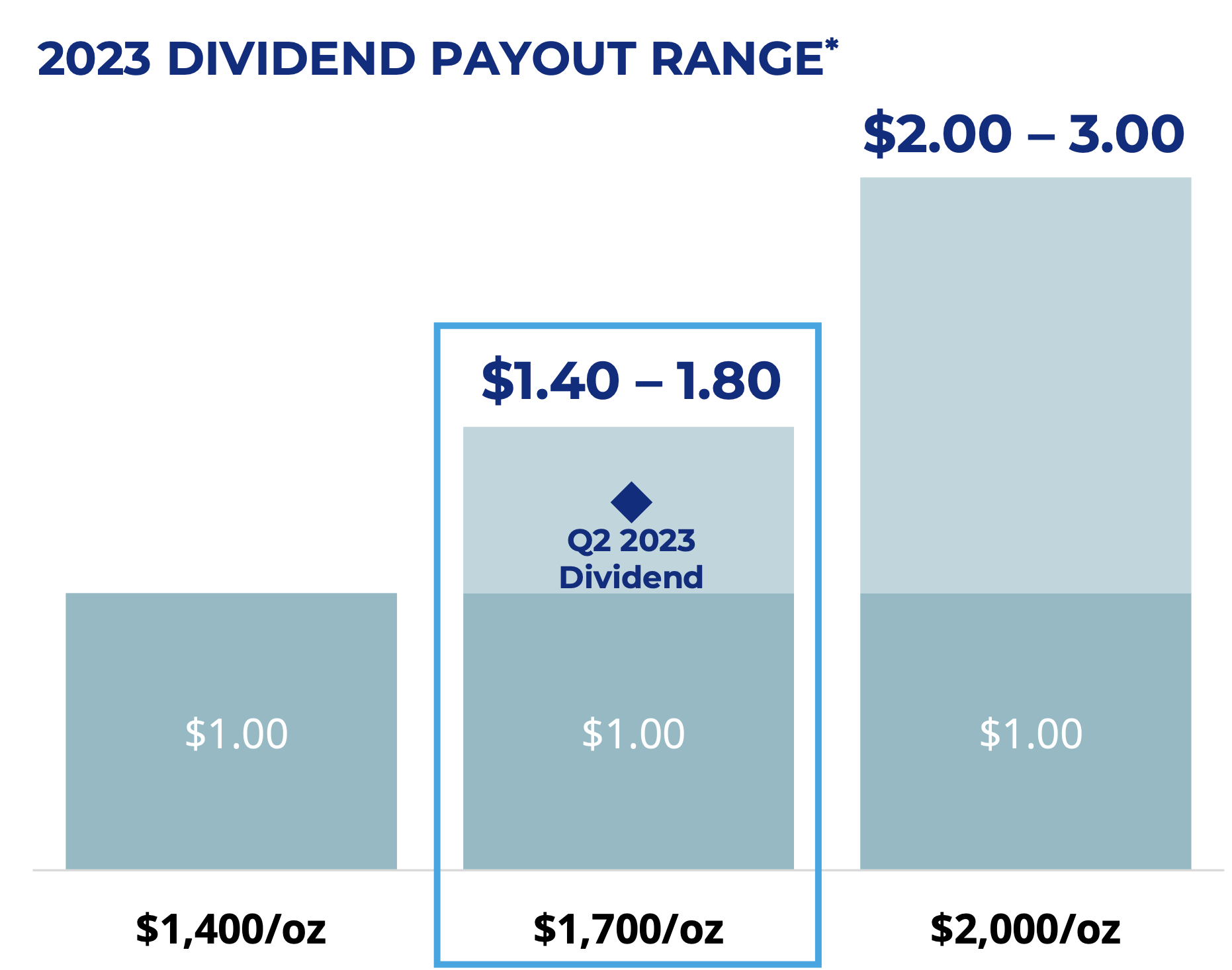

4. A 4%+ Dividend That Will Only Increase

Newmont continues to maintain a $1.00 per share base dividend with a variable component based on incremental free cash flow and the prevailing gold price.

The Q2 2023 dividend equates to a yield of just over 4%, and at the current gold price and assuming cash flow rebounds in H2 2023, the yield will be moving higher.

{kind=link}

There are many non-gold stocks (REITs, old Dow components, etc.) being touted because they have a strong 5-7% dividend, but many of these companies are saddled with debt and facing short-term headwinds that could result in a dividend cut. You don't have that risk with Newmont, given its healthy balance sheet, expected OCF and FCF, and gold knocking on the door of $2,000 again.

With NEM, investors get a hearty dividend and likely dividend increases if gold remains at current levels. Even if you aren't a traditional gold stock investor, one could see the appeal of buying NEM at these prices and in the current environment, as it's an income-generating investment that also offers inflation protection.

5. Valuation, Valuation, Valuation

In real estate, it's "location, location, location." When scouring for opportunities in the stock market, it's "valuation, valuation, valuation."

This is the lowest relative value that I've seen in Newmont in years. The following chart sums it up. Newmont's market cap has contracted from US$70 billion down to just under US$30 billion, which is the same valuation as Barrick. Adjusting for enterprise values, NEM trades at only a ~$3 billion higher value than GOLD. At the peak in 2022, Newmont's market cap was ~$25 billion higher than Barrick's.

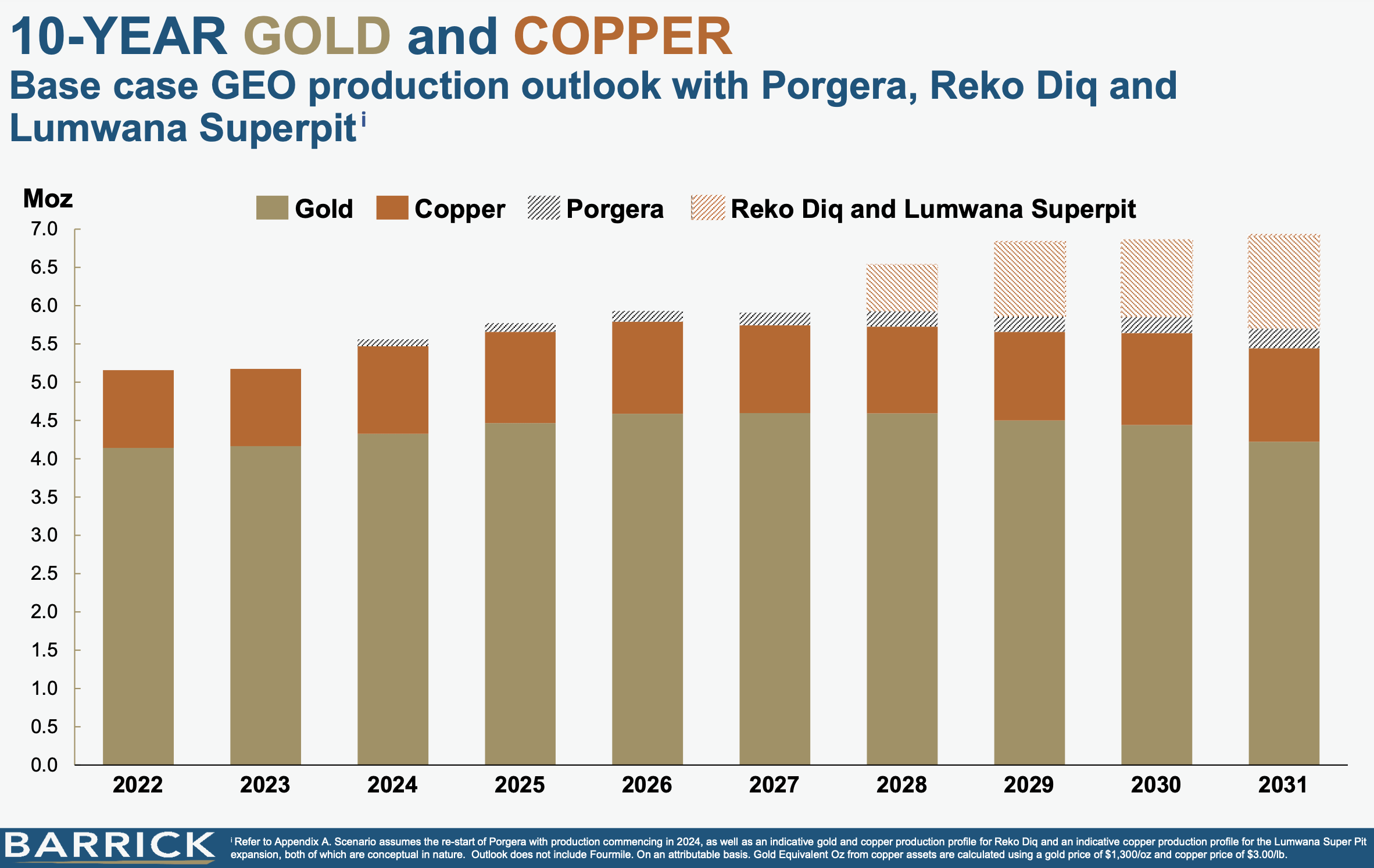

Barrick expects gold production to remain at around 4.0-4.5 million ounces per year over the next 5 years. On a gold equivalent basis, production is expected to average 5.0-5.5 million ounces. The 10-year outlook is similar, as I'm not including Reko Diq or the Lumwana Super Pit, both of which will require billions and billions of dollars of CapEx, carry heavy risks, are still 5+ years out, and are primarily copper assets. I don't believe these shouldn't be priced in yet.

{kind=link}

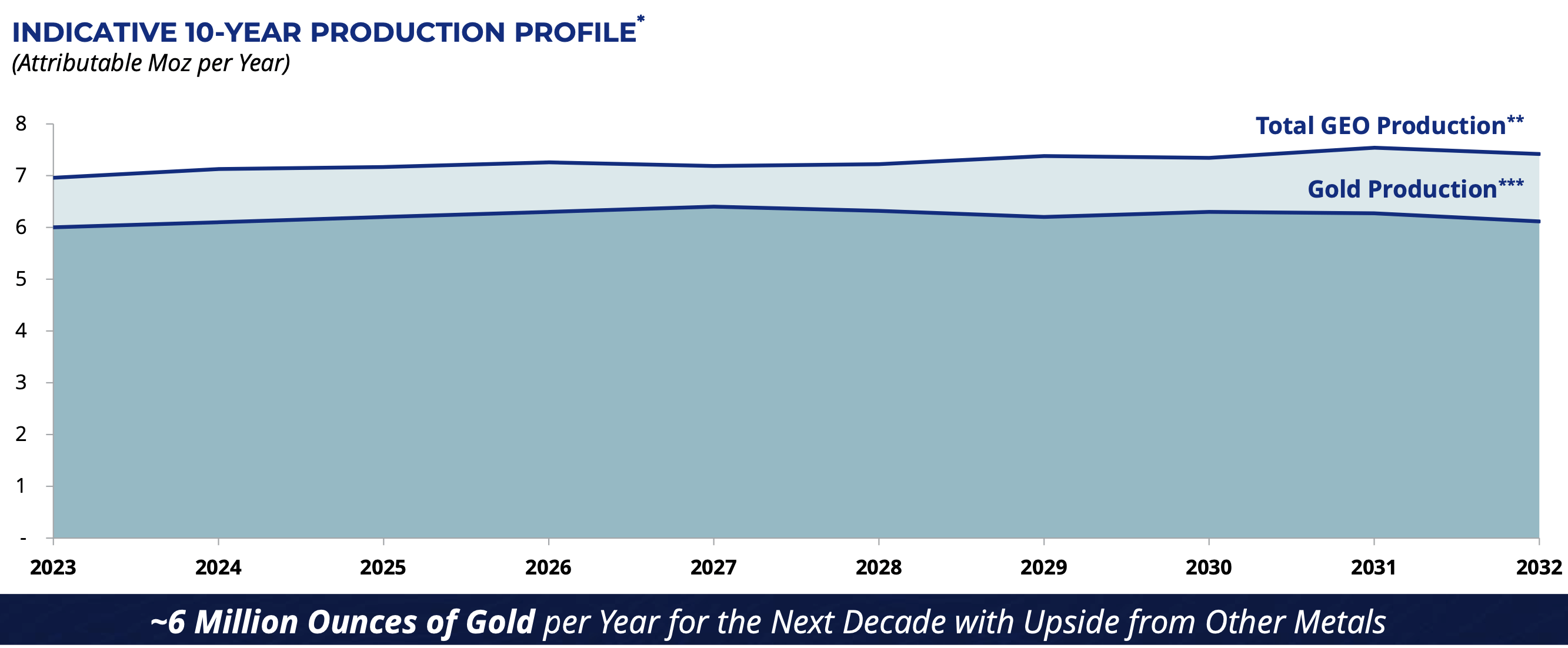

Newmont expects to produce over 6 million ounces of gold on average over the next 5 years, and over 7 million GEOs. There is also slight uptrend in GEO production over the next decade. That's ~35% more gold and ~30% more gold equivalent compared to Barrick, and using the top end of the production range for Barrick as well. This doesn't include any production from Newcrest, which I will get to in a minute.

{kind=link}

If Barrick had a substantial cost advantage, lower jurisdictional risks, or premium assets compared to Newmont, then one could potentially justify the current similar valuation to NEM. However, the two companies share many of the same assets (e.g., the Nevada JV and Pueblo Viejo JV), Newmont owns more Tier 1 mines and has a lower overall jurisdictional risk, and lastly, NEM expects lower AISC than Barrick.

The pro-forma market cap of Newmont and Newcrest is ~US$43 billion and the EV is around US$47 billion. Newmont expects 8 million ounces of total combined annual gold production once the transaction closes and combined annual copper production of approximately 350 million pounds (from Canada and Australia). On a gold and gold equivalent basis, that's almost double the production of Barrick.

On an apples-to-apples basis, if Barrick is trading at a $29 billion EV, then the pro-forma EV of Newmont/Newcrest should be $60-$65 billion, especially when you account for lower jurisdictional risk, lower AISC, and potential non-core asset sales that will bring in several billion dollars. That's 30-40% upside in NEM in order to get in line with the valuation of Barrick.

I'm not suggesting that Barrick is overvalued, either. Both companies are trading at a discount to fair value; Newmont is just considerably more undervalued.

Let's now quickly compare Newmont to the third largest gold producer in the world: Agnico Eagle.

At the start of this year, I discussed that on a P/CF basis, Agnico Eagle was a much better value compared to NEM. But the tables have turned, given the multiple contraction in the latter this year and factoring in the benefits of the Newcrest merger. AEM has a market cap of $24 billion and a margin + jurisdiction advantage over Newmont, but Agnico produces about 1/3 of the gold equivalent and is trading at around ~10x cash flow vs. ~8x for Newmont on a pro-forma basis. We have to adjust for the premium that AEM usually commands, but on a historical relative valuation basis, NEM is trading at a deep discount by comparison.

One of the keys to outperforming in this sector is to spot the divergences and the react according. There is no reason to own Barrick over Newmont at current valuations.

I expect that even if the price of gold remains flat, NEM will be re-rated over the next year as the integration of Newcrest, higher production and lower costs, higher cash flow, asset sales, and increases in the dividend will bring the valuation of NEM more in line with its peers.

While NEM might not offer the same upside potential as a small or mid-cap producer, it's one of the lowest risks gold miners one can buy at this stage and the best value amongst its peers. I see limited downside at current gold prices.

Risks = Not Many At These Prices

With a healthy balance sheet, an incredibly diversified asset base, strong margins and dependable cash flow even at much lower gold prices, and the majority of production coming from favorable jurisdictions in the Americas and Australia, there aren't heightened risks when it comes to NEM.

The main potential issue over the short-term is whether the Newcrest assets that Newmont is acquiring actually live up to the expectations and conclusions drawn from the due diligence conducted.

Sometimes, there are negative surprises that only come to light once you take control of assets and start mining them. I don't see an extremely elevated risk of that happening with Newcrest's assets — as they've been in production for many years — but until NEM has been running them for at least 12-24 months, we can't assume that all will perform as expected. My greatest concern would be on the cost side and whether these mines can truly hit the multi-year AISC guidance that Newcrest has put out.

One could argue that considerable risks are already priced into NEM. So even if one or two of the Newcrest assets don't hit targets, or there's another strike at Peñasquito, or one of the NGM assets severely underperforms, a degree of operational disappointment is baked into the cake.

In Summary

This is the best risk/reward opportunity in NEM that I've seen in years. The company is so well diversified and has such a plethora of quality assets, that even if one goes down, it won't have a dramatic impact. When you factor in the 50%+ decline in NEM since its 2022 peak, the turnaround expected in production and free cash flow starting last quarter (which will soon be reported), the strong dividend, and the bullish 5+ year outlook with higher production and lower AISC expected, I don't see any reasons to not own NEM, especially if one is constructive on the gold price over the next few years. Even if gold does nothing, I believe NEM could stage a healthy reversal once Newcrest is fully integrated and asset sales are complete.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Newmont: An Opportunity To Buy At The Deepest Discount In Years