GOLD - Newmont Should Be A Core Gold Holding: Triple In Price Next? (Rating Upgrade)

2023-11-28 03:24:19 ET

Summary

- Newmont is now the largest gold miner globally after its merger with Newcrest Mining, with a long list of Tier-1 mines.

- The company owns world-class gold reserves and resources, as well as extensive exposure to silver and copper.

- Newmont offers a bargain valuation vs. lesser peers and historical comparisons with a strong dividend yield backstop, making it an attractive investment opportunity.

- I am upgrading my rating to Strong Buy on recent share weakness.

Newmont ( NEM ) stands out as the top blue-chip choice in the gold mining space. It is now the largest gold miner on the planet (on sales and equity market capitalization) after the completed merger weeks ago with Australian-based Newcrest Mining .

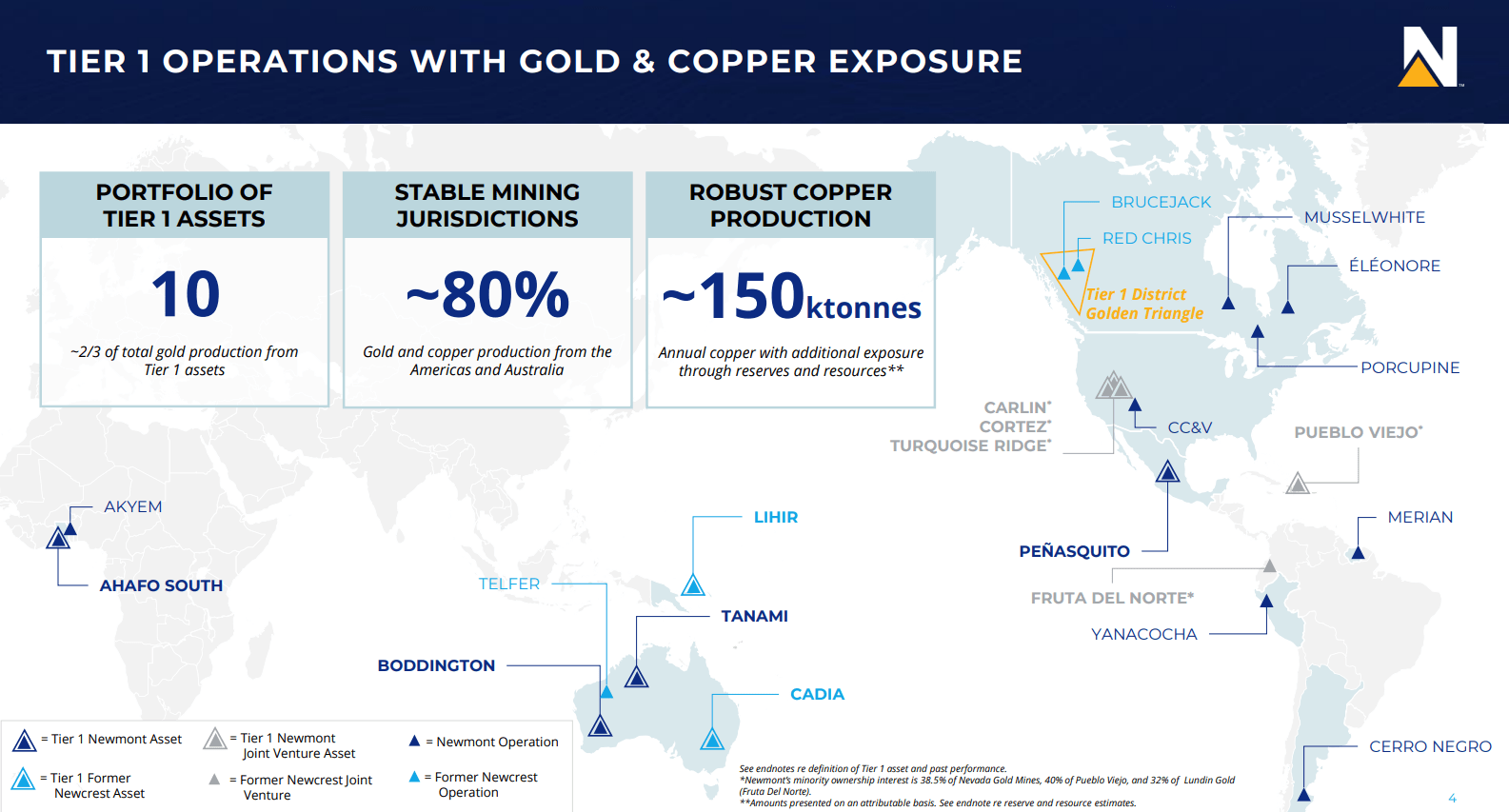

My last Newmont article in August here described a list ownership advantages coming in 2024 from the marriage, including asset rationalizations (management expectations of small mine sales to improve overall margins and reduce leverage), cost synergies (estimated at US$500 million pre-tax over 24 months), relatively low production costs (an estimated US$1350 per ounce for All-In Sustaining Costs) vs. peers, and the strongest diversification of Tier 1 mines in stable jurisdictions (10 of them) available to investors.

Newmont - November 2023 Investor Presentation Newmont - November 2023 Investor Presentation

{kind=link}

{kind=link}

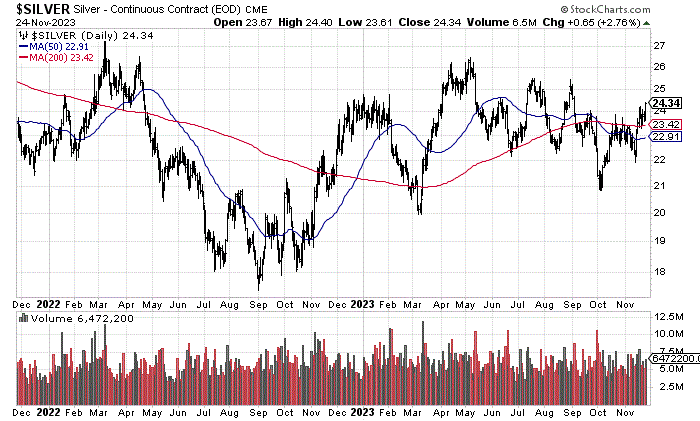

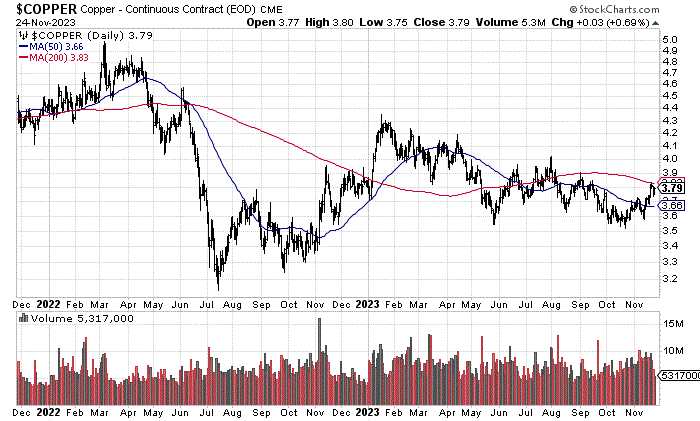

In addition to massive gold reserves and resources of 327 million ounces reported at the end of 2022, alongside 8 million ounces in annual gold production combined, the new and improved Newmont is also one of the largest silver (1.2 billion ounces in proven reserves and indicated resources) and copper (350 million pounds annually) producers in the world. Why is this important? Because I fully expect silver and copper prices to outperform my already super-bullish forecast for gold in the years ahead. Green energy supply growth requires enormous quantities of both silver and copper, for starters.

The truly bullish news is this whole business setup is available at one the lowest sector valuations, when it should be one of the highest to properly account for current and future developments in precious metals pricing.

For me, Newmont is a "must own" in nearly every portfolio, especially those with decent weightings in precious metals. The 4% dividend yield is likely to jump substantially over the next 2-3 years on rising metal values for income investors. Given US$3000 gold plus $50 silver an ounce, and $6 copper per pound as upside targets in 2024-25, projecting Newmont's $37 quote today will rise above $100 is not rocket science. Even assuming more muted $2500 gold, $40 silver, and $5 copper levels, while swinging from a steep undervaluation to just a normalized zone on fundamental financial ratios, I am projecting a share price closer to the $85 quote high of 2022.

YCharts - Newmont, Price Changes, 10 Years

As a consequence of gold and silver prices perking up in November, I am raising my Newmont rating from Buy to Strong Buy . Let me explain the valuation story and my buy logic.

Bargain Valuation

Because of its concentration in top-quality U.S. assets, minimal use of debt/leverage over the years, low production costs historically, and large diverse asset sizing, Newmont had typically commanded a "premium" valuation vs. gold mining peers before 2023.

However, with Wall Street playing a wait-and-see game regarding how Newcrest's assets fit into the old Newmont business model, valuation multiples have come down considerably for the combined organization (mainly on the lower share quote).

Instead of the premium enterprise valuation on EBITDA in years past, the combined Newmont/Newcrest entity is now going for a relatively normal ratio vs. the major gold miners of 7.8x projected 2024 results.

My peer sort group includes Barrick Gold ( GOLD ), Agnico Eagle ( AEM ), AngloGold Ashanti ( AU ), Gold Fields ( GFI ), Kinross Gold ( KGC ), Pan American Silver ( PAAS ), Freeport-McMoRan ( FCX ), and BHP Group ( BHP ).

YCharts - Newmont vs. Major Gold Mining Peers, EV to Forward EBITDA Estimates, 1 Year

When we look at combined earnings moving in the right direction after a rough 2023 at several Newmont mines, the valuation on income generation is also becoming quite compelling.

Seeking Alpha Table - Newmont, Analyst Estimates for 2023-25, Made November 25th, 2023

{kind=link}

A stripped-down forward P/E of 17.2x is quite inexpensive (sitting at 20+ years of proven reserves) vs. mining peers (10 to 15-years of proven reserves) or the stock market in general. Considering Newmont has usually sold at a 50% premium P/E to the S&P 500 index over many decades, today's 10% to 15% discount to the equivalent 2024 projected multiple of 20x for U.S. blue chips generally is a head scratcher. And, Newmont's actual P/E could be dramatically lower than current estimates if gold/silver/copper prices rise next year like I am projecting.

YCharts - Newmont vs. Major Gold Mining Peers, EV to Forward 1-Year Earnings Estimates, 12 Months

For sure, the stock price to trailing sales ratio estimate is very attractive given industry-leading asset quality and diversification, at a minimal premium to peers. Note: the pre-merger Newmont number of 3.5x a year ago has declined to 2.7x in November, about the same as projected for the post-merger amalgamation by the end of 2024 (not pictured). For comparison, the 35-year average P/S number is around 4.0x for Newmont.

YCharts - Newmont vs. Major Gold Mining Peers, Price to Trailing Sales, 12 Months YCharts - Newmont, Price to Trailing Sales, Since 1988

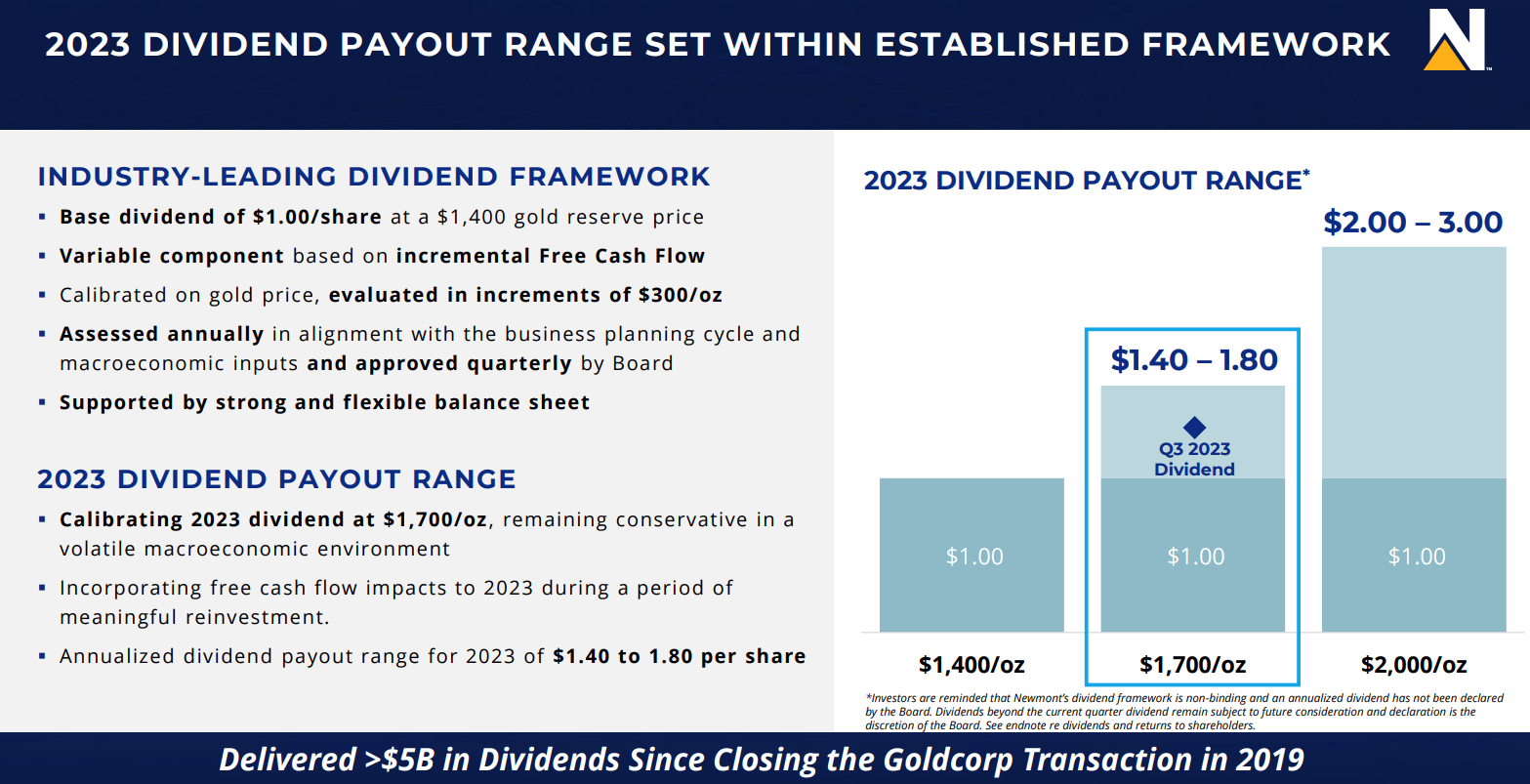

Another super-bullish excuse to look at Newmont shares today is the dividend yield proposition. Management has suggested most free cash flow in the future will be paid out as cash dividends to shareholders. Already, the 4.8% trailing yield (4% forward estimate) is a much better deal than you can find in the gold mining sector or from U.S. businesses in general. If you want a money-printing hedge that is promising to pay out huge dividend increases if precious metals climb in value appreciably soon, Newmont is a unique and interesting income idea.

YCharts - Newmont vs. Major Gold Mining Peers, Trailing Dividend Yields, 1 Year YCharts - Newmont vs. U.S. Equity Market Indexes, Trailing Dividend Yields, Since 2007 Newmont - November 2023 Investor Presentation

{kind=link}

Unparalleled Investment Logic

Having traded gold miners for 35 years, there are four main reasons to buy a gold producer. The first is as a generic portfolio hedge against aggressive Federal Reserve (central bank) money printing and geopolitical turmoil in the world. Assuming we are entering recession soon, Newmont should be considered right now as the Fed starts easing bank credit policy in 2024. Gold miners often experience strong "outperformance" of the S&P 500 during recessions and bear markets, with some of the biggest upmoves in price coming near the end of recessions (as money printing ramps higher).

The second reason to own any gold miner is valuations are lower than normal. In terms of arbitrage trading between stocks in the mining sector, and other industries generally, a great time to buy comes when valuations are beaten now. Newmont checks off this box with flying colors, as it is undervalued vs. both the gold mining industry and usual relative pricing to the S&P 500.

A third reason to consider buying Newmont is you are bullish on precious metals and gold in particular. This is common sense, but a recap is higher selling prices for produced gold/silver/copper means greater income and cash flows. Gold miners can rise and fall by 2x to 3x the percentage changes in mined metals pricing (owning decades of mining reserves and future operating income creates the leverage). Mining share quotes almost always follow metals pricing, outside of stock market crash spans like 1929 and 1987. Since I am personally very bullish on precious metals, Newmont is now a screaming buy idea.

My last reason to look at owning a gold miner revolves around resource finds and discoveries. When major new deposits are uncovered, especially at smaller outfits, stock prices can soar. In Newmont/Newcrest's case, its large size will not allow for massive share gains on new discoveries. However, its outlook for adding ounces combined with 20+ years of existing proven & probable reserves (at current production rates) fully supports acquiring a position in your portfolio. Newmont pre-merger did add about 5% to economic reserves during 2022. Most other blue-chip gold mining companies as alternatives have fewer economic reserves as a function of production or assets situated in less-safe political jurisdictions.

My point is: if there was ever a time to consider Newmont for immediate-term and long-term ownership, November 2023 ranks as a terrific moment to get serious about purchasing a stake.

Final Thoughts

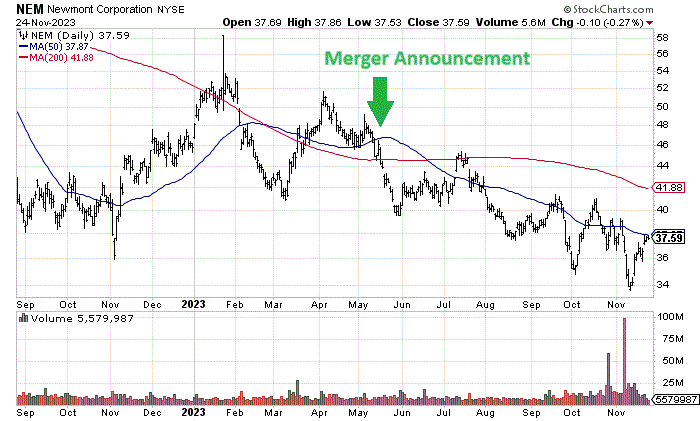

I will say upfront, I have had a bullish rating on Newmont all of 2023 and do own a sizable position again. It has been a disappointing journey, before, during, and after the May takeover announcement for Newcrest Mining. The good news is gold/silver are performing better in recent weeks, and previous Newcrest owners not wanting to hold the merged company have hopefully sold out their holdings after November's deal completion. So, many of the overhangs keeping pressure on NEM's quote may have now run their course.

Remember, without the misplaced confusion and pessimism by investors over the slightly dilutive Newmont/Newcrest transaction for production levels at the beginning, the upside potential would not be as positive. A share move from $37 to $100 (my target price in 2-3 years) would generate +170% in price appreciation vs. the same destination bought at $50 for +100% gains.

StockCharts.com - Newmont, 15 Months of Daily Price & Volume Changes, Author Reference Point

{kind=link}

Wall Street can now focus on the undervaluation story, rising precious metal quotes, a Fed soon to pivot to credit easing policy in a recession, and the potential for commodity inflation (on greater demand for silver and copper) during the next economic upturn.

What are the investment risks going forward? Two stand out to me. As operations are well diversified and the production profile is one of the strongest/conservative in the sector, I worry more about macroeconomic changes.

A huge bear market or crash in pricing on Wall Street generally would almost surely keep a lid on Newmont as well, at least initially. The silver lining (I mean gold) is such a scenario may lead to record levels of money printing to prevent another depression similar to the 1930s. In fact, had you bought gold miners after 1929's September to November -50% crash span, gold assets proved the smartest sector to own during the next 3 years.

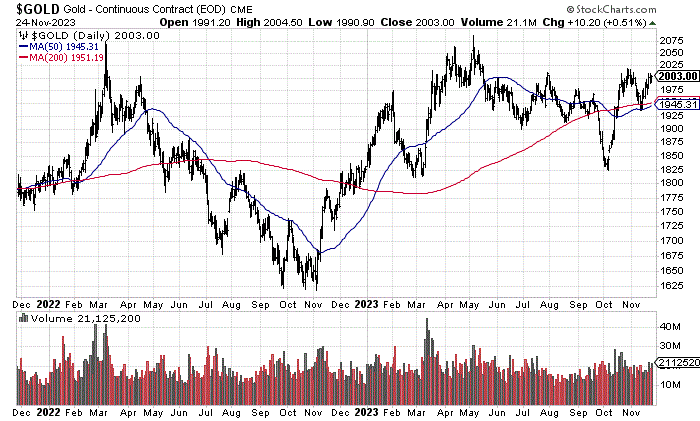

Another risk, which is obvious to all, would come if gold/silver/copper prices do not rebound robustly, like I am projecting. I have written a number of bullish articles on gold and silver in particular during 2023. As an example of my thinking, you can read my October effort here on gold's bullish lease rate picture, and a November article here on silver's undervaluation characteristics. Yet, if precious metals remain stagnate for price, Newmont's upside will be limited in 2024.

StockCharts.com - Nearby Gold Futures, 2 Years of Daily Price & Volume Changes StockCharts.com - Nearby Silver Futures, 2 Years of Daily Price & Volume Changes StockCharts.com - Nearby Copper Futures, 2 Years of Daily Price & Volume Changes

{kind=link}

{kind=link}

{kind=link}

For patient investors, when we (1) start to look at ramping production at acquired Newcrest mines, (2) the constructive effects of expected asset sales on margins and the balance sheet, plus (3) the cost synergies of eliminating overlapping work positions while instituting mining and management techniques mastered by Newmont, the outlook for improving margins and profits is worth the current share price of admission, in my opinion.

Again, I am upgrading my rating for Newmont to Strong Buy . There are just too many sound reasons to own it. I suggest for your wealth's future, please don't ignore it. Using a projected P/E of 20x earnings, on a leaner, higher-margin business in 2-3 years, works out to $100 a share on $5 EPS created by $3000 gold, $50 silver and $6 copper (assuming minor operating cost increases of 7% annually). A move from $37 to $100+ a share over the next 24-36 months will likely run circles around S&P 500 and Big Tech NASDAQ 100 total returns, paying dividend rates far lower than Newmont's current yield.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Newmont Should Be A Core Gold Holding: Triple In Price Next? (Rating Upgrade)