NEM - Newmont: Sitting At Trough Multiple Ahead Of Margin Recovery

2023-09-12 07:14:56 ET

Summary

- Newmont had a tough Q2 with lower output, lower margins and weaker free cash flow generation, but it was an abnormally bad quarter with several headwinds, one-time impacts.

- However, Newcrest had a solid quarter & posted strong FY2023 results, and these results were achieved in a softer year without any benefits from high-margin projects in the pipeline.

- In this update, we'll look at Newcrest's results, why this is transformative for Newmont, and whether the stock is finally attractive enough to start a position.

The Q2 Earnings Season wasn't nearly as strong as expected for the gold sector, and Newmont's (NEM) headline results were among the weakest sector-wide, with lower production, higher costs, and a significant decline in free cash flow. However, this is a trend that we've seen among several producers and is not company-specific, and while Newmont's free cash flow was pressured in the period, this was due to increased investments at key project, elevated sustaining capital and the impact of lower than planned production at several mines. However, Newmont is unique in that it will lap easy comparisons in H1 2024 (abnormally weak H1 2023), with growth capital beginning to taper off at its legacy assets and it will also benefit from multiple low-cost and large-scale assets gained in the Newcrest acquisition plus higher production at Pueblo Viejo (Expansion) and Tanami.

In this update, we'll look at Newcrest's annual results and why this deal will be transformative for Newmont, especially when combined with the improving free cash flow generation for its legacy business.

Brucejack Operations - Newcrest Presentation

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Newcrest Q2 Production & Sales

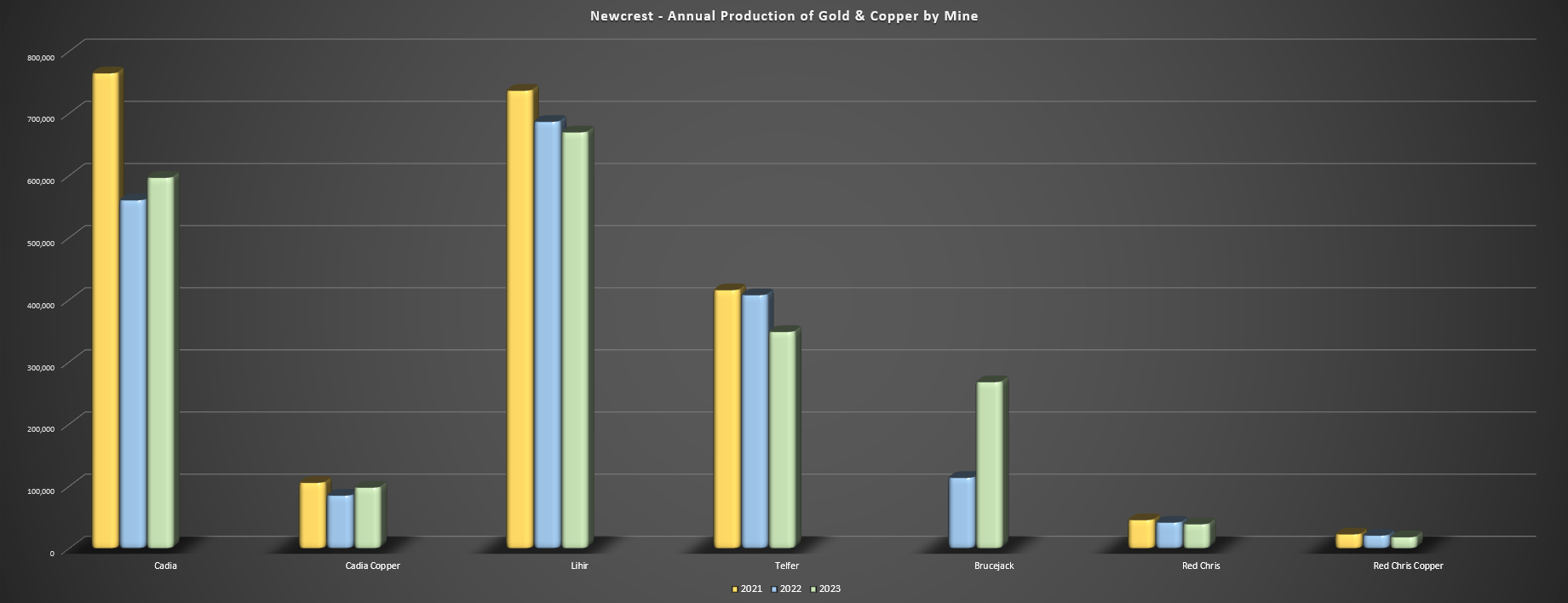

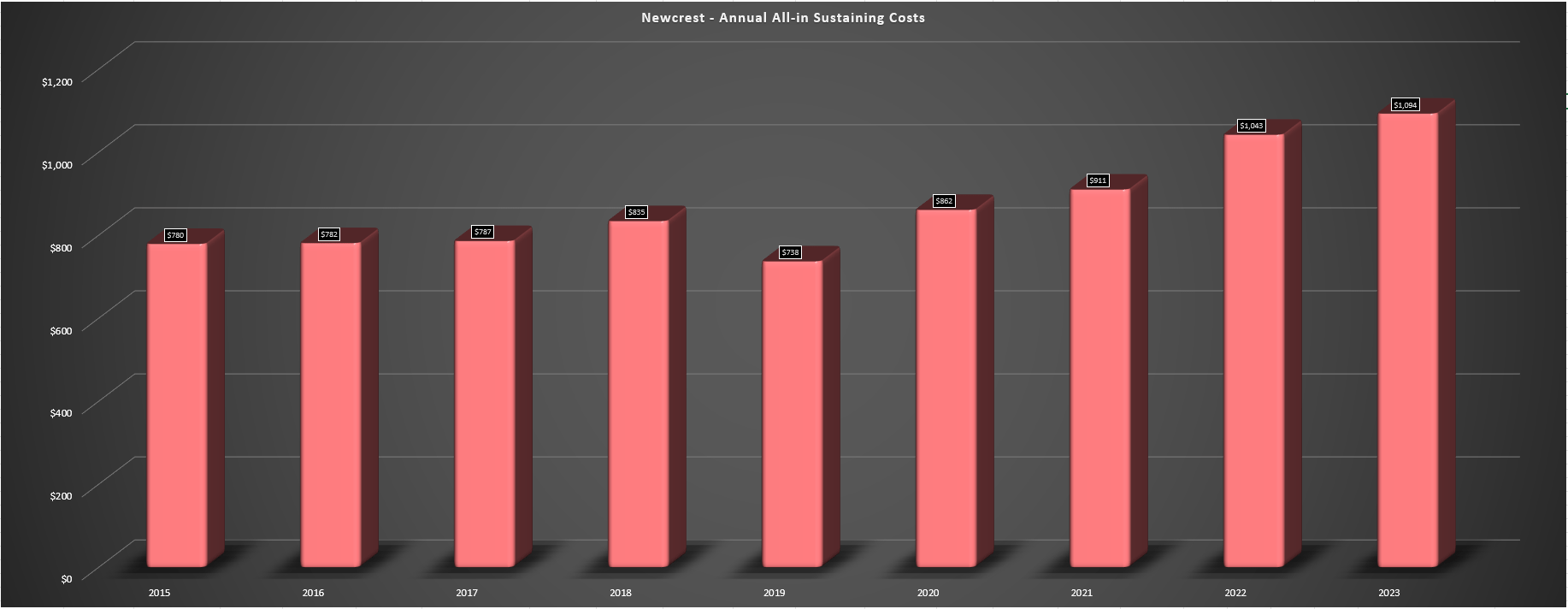

Newcrest released its FY2023 (June 2022 to June 2023) results last month, reporting annual production of ~2.11 million ounces of gold and ~133,100 tonnes of copper, an increase from ~1.96 million ounces of gold and ~120,700 tonnes of copper in the year-ago period. The higher production was related to a stronger year at Cadia and a full year of gold production from Brucejack, offset by lower production at Telfer, Lihir, and Red Chris. And despite minimal help from gold and copper prices (flat and down, respectively), Newcrest had a solid year financially, reporting revenue of ~$4.51 billion, operating cash flow of ~$1.61 billion and industry-leading all-in sustaining costs of $1,093/oz, up ~5% year-over-year, which was a much smaller rate of change than its peer group.

Newcrest - Annual Production of Gold & Copper by Mine - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, Cadia was the stand-out with ~596,900 ounces of gold produced at all-in sustaining costs [AISC] of $45/oz, making this one of the lowest-cost mines sector-wide next to Ernest Henry. This solid cost performance was despite higher sustaining capital in the period related to TSF construction, and it was despite a lower average realized copper price of $3.76/lb, resulting in lower by-product credits. Newcrest noted that the improved production was related to recovery improvements following the commissioning of the two-stage plant expansion project, and the company also approved the Cadia PC1-2 Feasibility Study, with first ore expected in FY2026. While costly at ~$1.2 billion, the project has a 23% IRR at $1,950/oz gold and extends the mine life well into the 2050s, making this one of the longest-life gold assets sector-wide.

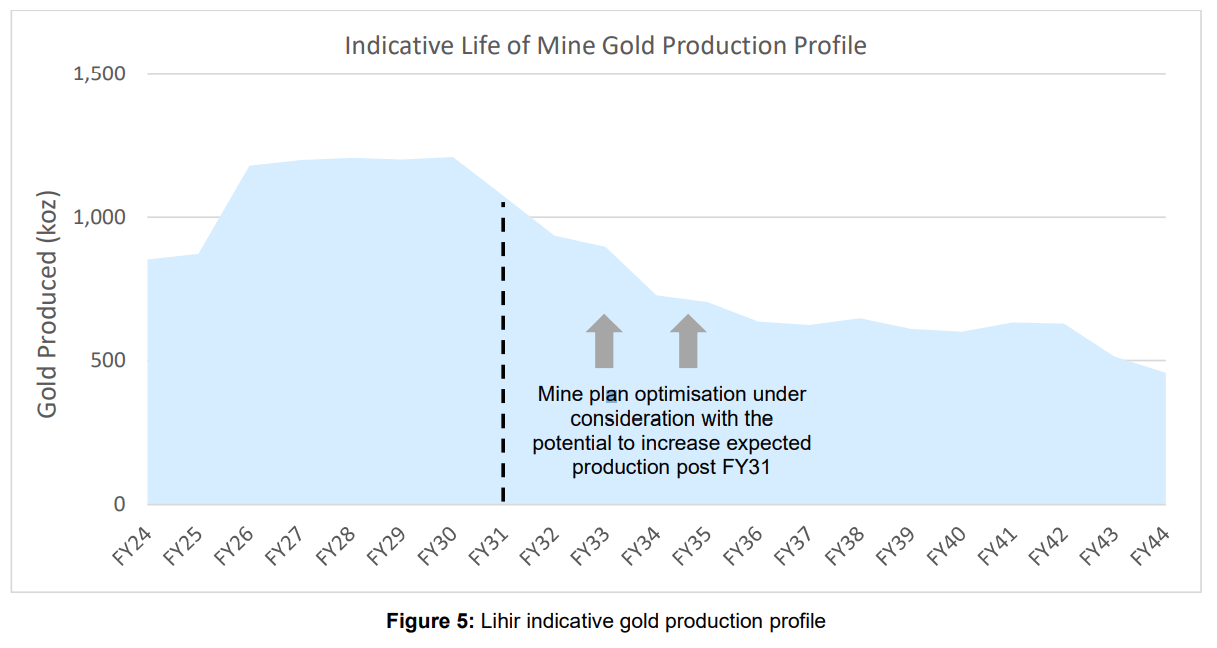

Unfortunately, the solid results at Cadia were overshadowed by a tough year the company's largest Lihir Mine in Papua New Guinea, which produced just ~670,000 ounces last year, down from ~687,000 ounces in FY2022. The lower production was related to lower feed grades, with a higher proportion of low-grade ex-pit material processed in H2 due to the impact of extreme rainfall which impeded pit access and affected material handling at the crushers. This softer H2 production was on top of an already tough H1 performance where mill throughput was impacted by drought conditions which limited water supply, in addition to lower mill availability due to unplanned downtime. Fortunately, 2024 will be a better year with high-grade ore from the recently approved Phase 14A cutback, and this will help to displace lower-grade stockpiles previously planned for feed during the transitional zone between the Lienits and Kapit Pit from FY2023 to FY2027.

Lihir Production Profile - Company Release

{kind=link}

The result is a more consistent production profile with higher output overall with a steady trend higher in gold production going forward until FY2030. And like Cadia, returns are robust, with a 64% IRR even at a conservative $1,800/oz gold price assumption.

Finally, in British Columbia, production was lower at the company's new Brucejack Mine, but costs still came in well below the industry average. Looking at the annual results, Brucejack produced ~286,000 ounces of gold at all-in sustaining costs of $1,157/oz despite a ~60% increase in sustaining capital in the period. Meanwhile, the mine generated ~$115 million in free cash flow despite lower production than planned. Unfortunately, Red Chris' results were weaker, with lower gold and copper production, a lower copper price and similar sustaining capital contributing to costs well above the industry average ($3,733/oz vs. $1,349/oz). Newcrest noted that recoveries were impacted by a shift to mining at the Main Zone (Phase 7) vs. East Zone which carries higher levels of pyrite. That said, the big picture at Red Chris has never been more bullish, with continued exploration success and a path to negative AISC later this decade with Red Chris Block Cave, and continued high-grade results from East Ridge and Far East Ridge.

Costs & Margins

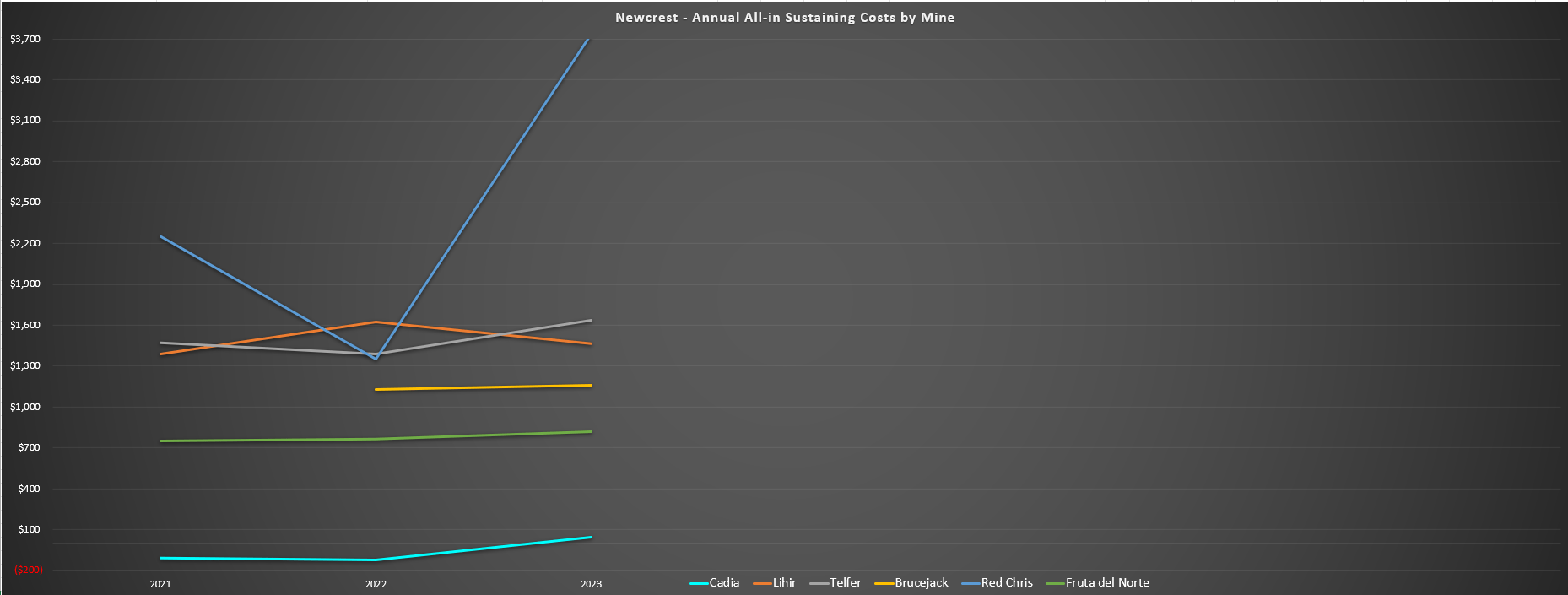

Moving over to costs and margins, Newcrest's assets performed well overall despite the headwind of lower by-product credits from a weaker copper price. This was helped by a weaker Canadian and Australian Dollar in the period, but also higher production at Cadia which had a massive year despite lower gold head grades. That said, Lihir's elevated costs (Newcrest's largest mine) pulled the company's consolidated costs higher to $1,093/oz (FY2022: $1,043/oz), resulting in AISC margins declining to $680/oz (FY2022: $732/oz). However, these margins still came in above the industry average for the period, and we should see better costs at Lihir next year (FY2023: $1,466/oz) assuming we don't see another year with multiple headwinds.

Newcrest Annual AISC by Mine - Company Filings Newcrest - Annual Operating Cash Flow & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

{kind=link}

Finally, from a financial standpoint, it may look like Newmont paid a lofty price for Newcrest considering that the company generated just ~$404 million in free cash flow year, given that Newmont is paying upwards of $18.0 billion for the company (45x trailing free cash flow). And while there's no disputing that it's paying a premium price, this is a portfolio that is not operating at anywhere near its full potential currently. This is because Lihir's production profile is well below life-of-mine production levels (~670,000 ounces vs. ~820,000 ounces) even ahead of potential upside from steep wall technologies and a simpler seepage barrier design, Red Chris is a money-losing asset currently, but it's a future ~300,000 ounce gold producer at negative ~$200/oz AISC from 2029-2035, and Havieron will also come online later this decade, a high-grade asset whose ore will be trucked to Telfer, with AISC expected to come in below $800/oz.

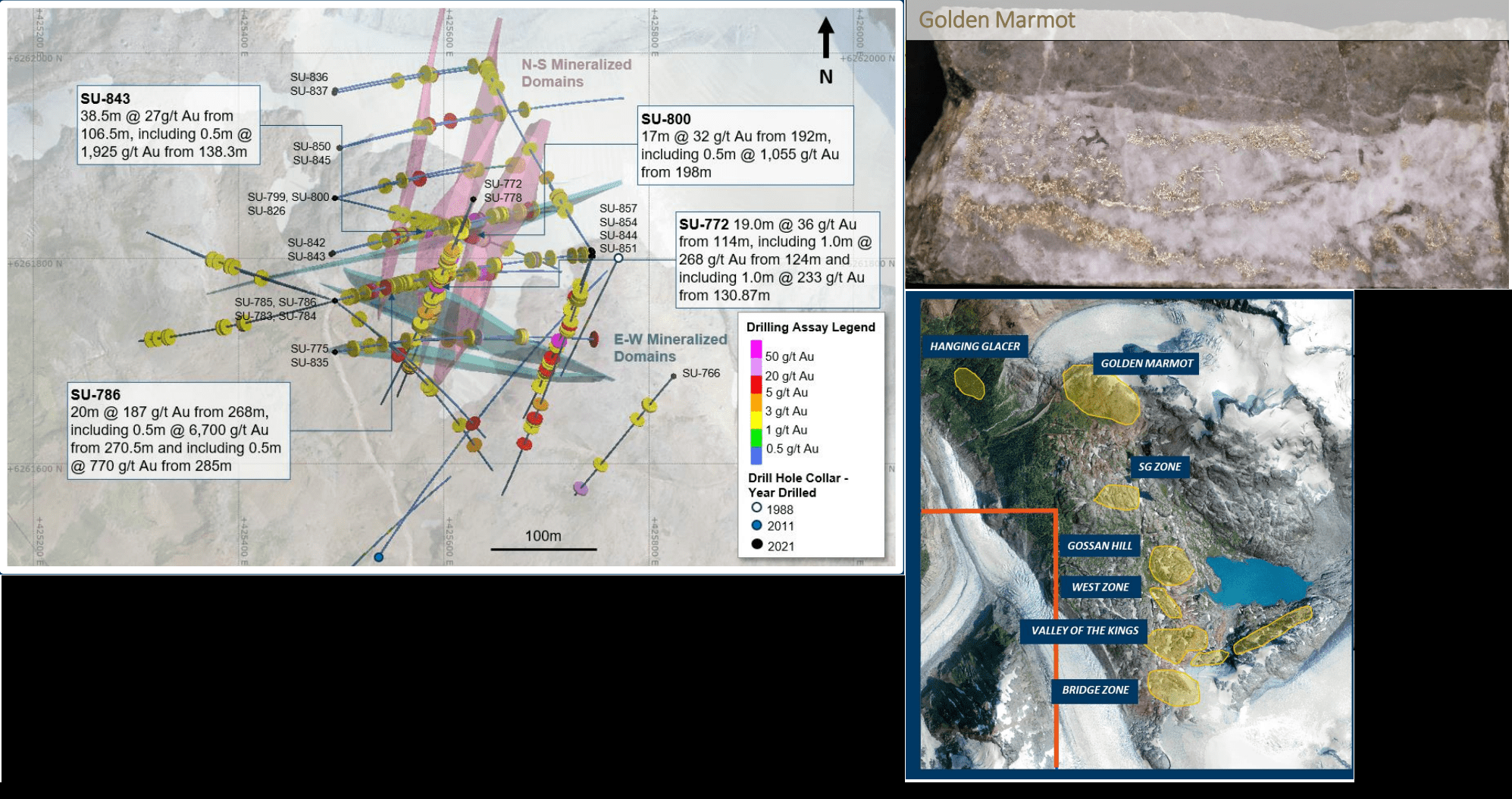

Hence, this will be a very different looking group of assets from a free cash flow standpoint later this decade when Havieron and Red Chris Block Cave are online, Brucejack is further optimized and Lihir's production profile is above 1.0 million ounces per annum. Plus, this doesn't even count upside from East Ridge, Far East Ridge, and Wafi-Golpu, with Newcrest having a 50% ownership in the latter asset which could also be a negative AISC producer. So, while the price paid may look steep, it's hard to put a price on multiple assets with what look to be at least 25 year mine lives (Cadia, Havieron, Red Chris, Wafi Golpu) with all-in sustaining costs coming in between [-] $100/oz and ~$800/oz, miles below the current industry average. And with the ultra high-grade Golden Marmot discovery + new high-grade near mine discoveries (North Block, 1080 HBx zones) Brucejack should also see its costs improve further, with the potential for sub $1,000/oz AISC when combined with a planned increase in throughput (4,500+ tonnes per day), the potential to use ore sorting technology and further synergies.

For those unfamiliar, highlight holes from North Block include 28.5 meters at 262 grams per tonne of gold (including 1.0 meter at 7,400 grams per tonne of gold), highlight holes at Golden Marmot include 20 meters at 187 grams per tonne of gold (including 0.50 meters at 6,700 grams per tonne of gold), and highlight holes at 1080 HBx include 18 meters at 306 grams per tonne of gold (including 1.0 meter at 5,370 grams per tonne of gold) and 38.5 meters at 49 grams per tonne of gold (including 1.0 meter at 1,735 grams per tonne of gold), and 10.5 meters at 918 grams per tonne of gold, among the highest-grade intercepts reported sector-wide from just one of Newcrest's many assets. Importantly, these are entirely separate from world-class intercepts coming from other assets in the portfolio like at Havieron (~150 meters at 3.7 grams per tonne of gold and 0.15% copper) and Red Chris (~248 meters at 1.6 grams per tonne of gold and 1.4% copper, or ~3.5 grams per tonne gold-equivalent).

Golden Marmot Mineralization, Drill Results & VOK + Regional/Near Mine Targets - Newcrest Presentation

{kind=link}

The New Newmont

Assuming the successful amalgamation of Newcrest and Newmont, the company will extend its lead over the sector's largest gold producers with ~8.0 million ounces of annual gold production, ~380 million pounds of copper production (excluding significant growth from projects that include Red Chris Block Cave and 50% of Wafi-Golpu) and it will have multiple Tier-1 assets in its portfolio, defined as those with 500,000 GEOs of production per annum (100% basis), a 10+ year mine life, and costs in the lower end of the cost curve. These assets include Tanami, Turquoise Ridge (38.5%), Carlin (38.5%), Cortez (38.5%), Pueblo Viejo (40%), Lihir, Cadia, Boddington, and Penasquito. Plus, from a cost standpoint, Newmont is confident it can achieve $500 million in pre-tax synergies within two years of the deal closing (20% G&A, 40% supply chain helped by economies of scale, 40% Full Potential Continuous Improvement Program).

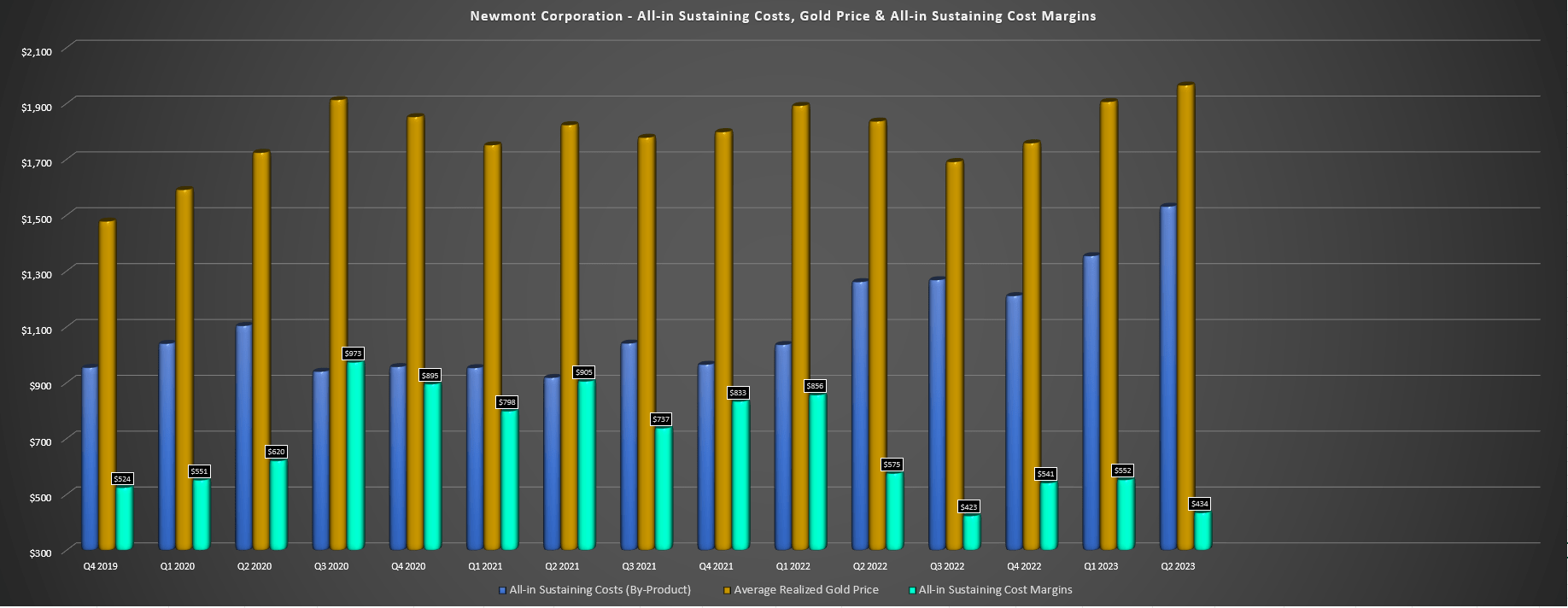

Despite this path to Newmont solidifying itself as a larger and more diversified producer, many investors have avoided the stock because while it may be the largest gold producer, its margins have taken a beating over the past two years, as has its free cash flow generation. Its AISC margins evidence this, plummeting to $493/oz in its most recent quarter (Q2 2021: $788/oz), and quarterly free cash flow dropping 93% to $40 million (Q2 2021: $578 million) on a two-year basis. These stats are even more disappointing given that Newmont enjoyed a record average realized gold price of $1,965/oz in Q2 2023. That said, outside of inflationary pressures, there were several key differences from Q2 2023 vs. Q1 2021.

Newmont - AISC (By-Product), Gold Price & AISC Margins - Company Filings, Author's Chart

{kind=link}

For starters, capital expenditures were ~50% higher at $616 million with sustaining capital spend and higher growth capital expenditures. Elevated sustaining capital was related to camp upgrades at Musselwhite and the addition of five new autonomous haul trucks at Boddington. The latter (growth capital) was due to increased spending at Tanami Expansion 2, Ahafo North, Pamour, and the Cerro Negro District Expansions. Finally, the company got little help from its lower-cost Penasquito Mine in the period with mining activities halted in early June related to a strike, and also saw production curtailed at Cerro Negro (safety inspections) and Eleonore (evacuation because of wildfires). And while Penasquito may not be much help in Q3 and it looks like Q4 could be affected as well at this rate, Newmont should see higher grades at Subika Underground, Cerro Negro, and Tanami, and stronger production from Turquoise Ridge, Cortez, and Carlin in the second half, helping to improve consolidated AISC in H2.

Plus, if we look further out to 2025, we should see a material decline in Newmont's all-in sustaining costs as the company benefits from:

- higher gold sales

- lower costs at Tanami 2 Expansion and Ahafo North once these projects are completed

In addition, while Newmont (stand-alone basis) looks to be seeing trough margins with a steady trend higher beginning next year, Newcrest's operations are much lower cost, and there's a path to even lower costs across its portfolio. In fact, as highlighted earlier, Newcrest's AISC came in well below the industry average at $1,093/oz despite a tough year at its largest asset (Lihir), little help from copper prices which affected its by-product credits, underperformance from Brucejack because of a brief shutdown following a tragic fatality, and a very high cost year at Red Chris. However, if approved, Red Chris Block Cave could produce ~300,000 ounces of gold and ~80,000 tonnes per annum of copper from 2029 to 2034, with all-in sustaining costs expected to be deeply in negative territory even at sub $4.00/lb copper prices.

Red Chris Block Cave - 2021 Study - Newcrest Release

{kind=link}

So, while we will see lower costs immediately for Newmont if the Newcrest deal is approved, the medium-term and long-term benefits are also significant, with low-cost projects like Havieron (70%) and Red Chris Block Cave (70%) paving a path towards sub $1,000/oz AISC and the potential for even lower AISC if Wafi-Golpu (50%) is developed (another asset that's expected to have negative AISC). To summarize, with a larger production profile, more Tier-1 assets, greater diversification and the ability to optimize the portfolio by selling non-performing assets, I would expect Newmont to enjoy multiple expansion over the next two years and a much higher share price with a complete 180 in sentiment once investors get used to significantly higher free cash flow generation and a return to ~$750/oz AISC margins (~$1,200/oz AISC) vs. the much higher cost profile currently ($1,424/oz AISC year-to-date).

Summary

Newmont remains out of favor today with the Penasquito strike extending longer than some had hoped, a rough H1 2023, and what might seem like a never-ending trend in higher costs, all combined with a dearth in free cash flow generation for a ~$30 billion company. However, digging into the results, it's clear that much better days are ahead, with significant progress on lower-cost projects (Tanami 2, Ahafo North), a better H2 on deck, and a transformative acquisition that will help with a steady decline in AISC short-term, medium-term, and long-term, especially if key projects like Red Chris Block Cave are green-lighted and the company does a solid job optimizing its portfolio. Hence, with the stock in the penalty box and trading near multi-year lows, I see this as an even better buying opportunity than September 2022, with high-margin projects closer to completion, the dividend cut out of the way, and a more robust development pipeline if the deal goes through.

In summary, I see this pullback in NEM below US$39.00 as a buying opportunity.

For further details see:

Newmont: Sitting At Trough Multiple Ahead Of Margin Recovery