NR - Newpark Resources: A Splash Of Cash And A Potential Catalyst

Summary

- Changes are in store at Newpark, including a possible sale of the fluids business.

- The company is trading at an attractive valuation and should experience solid growth in 2023.

- Investors with a high amount of risk tolerance may find this plucky micro cap attractive at current prices.

Introduction

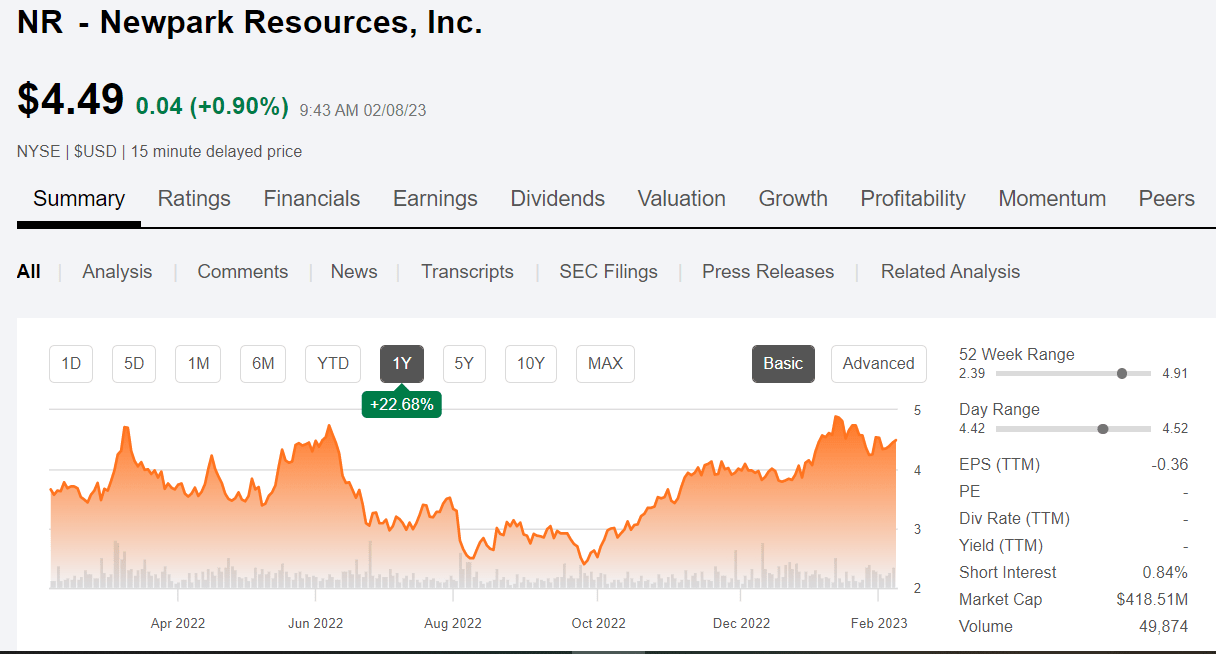

In my last article on Newpark Resources ( NR ) in October of last year, I rated them a hold at $2.85 a share. The very next day, seemingly, the company began a rally that took them all the way to $4.00, and once they closed the sale and sublease of their Port Fourchon blending plant, the stock rallied another 23% to $4.91 per share. Is there anything else going on?

{kind=link}

In this article we will review the company's Q-3 financials and revalidate the thesis for the company. Long-time readers know I'm a fan of the company. Newpark was poised to become a much larger company in 2015 and give larger rivals, Halliburton ( HAL ), Baker Hughes ( BKR ), and Schlumberger ( SLB ) an "elbow in the side." The offshore downturn that began then has finally taken its toll and the company has abandoned the goal of moving into the Big Leagues of mud.

What's left then are the regional markets of West Texas, the Middle East and North Africa, Brazil, and AsiaPac-Australia. All markets where they are not the leaders or runners up, but manage to make a living with innovative products and strong local representatives.

The question before us, is this enough to take Newpark through the $5.00 barrier for the first time since early 2020? It might, and there's another catalyst that could be in the offing. Read on.

The thesis for Newpark

The company is bifurcated into two business that have no obvious synergies, Fluids and Mats. Both have been in a growth mode over 2022, but are largely tied to the rig count which stalled out in Q-4.

Newpark fluids business attracts clients who want big company technology and more personalized service than the big three can provide. Its technology is top tier but heavily weighted toward the deepwater market from which it has just taken a big step back. It also has a boutique formation damag e and evaluation lab that supports its breaker business - CleanSorb, but is probably underutilized. The company has some new water-based entrants targeted primarily at the U.S. land market, but that's a crowded field. Crowded and low margin. Newpark reports margins of 5%+ in this business.

The problem Newpark has in fluids is that the big three use them as loss leaders in big tenders. They can bundle the full suite of their portfolio and offer multi-service discounts that are just not realistic for Newpark. While Newpark's technology is top tier, the big three can match it, leaving Newpark out in the cold a lot of the time.

Mats is a high margin mostly rental business (20%+) that generates about a third of the income that comes from fluids, but has no real moat. Interlocking mats provide a base for rig roads and location foundations that increase access and cleanliness. Something you battle constantly in remote work sites is filth. It accumulates on your hands and feet. It's in the air, pulverized by the tires of heavy equipment trucks, cranes, flatbeds, tanks, silos, etc. Mats help keep that to a minimum and are probably the easiest sell in the oilfield. Newpark also has made other industrial remote location inroads, but nothing there compares to the scale of rigs as they move from location to location.

Newpark also is a company looking for direction as we documented in our last article. An activist investor Bradley Radoff has gotten a turnaround specialist added to Newpark's board , so we can expect more changes in the quarters to come. I opined in the last article in regard to this quote from Mathew Lanigan, CEO of Newpark:

We're exploring a range of options to optimize our capital deployment in this market.

Me - As an investor, nothing sends me diving for cover faster than language like that. Whatever Lanigan is talking about... a straight sale (of the plant at Fourchon) is an unlikely prospect.

How right I was. So is that it? Newpark continues to struggle along bouncing off resistance at $5.00 per share? Maybe not.

A potential catalyst for Newpark

We have some potential resolution to one of the key problems I highlighted in the last article. That being, they have the top fluids exec- David Paterson , in the business in their fold, and passed him over last year to become CEO. That has gone from being a problem to a tell as I have refined my thinking. The Fluids business is being prepped to be sold . (I deserve a smack on the head for not figuring this out previously.)

The Fluids business is ripe for consolidation, and I can see one of the big players like No. 4, Weatherford ( WFRD ) or perhaps a company already in the business, like ADNOC Drilling , bringing this high technology company into their fold. As I've said, Newpark is disadvantaged in tenders with its pure-play drilling fluids offering. Now with the cash bonanza that will come from exiting the GoM Fourchon based deepwater and Minerals Grinding business (about $130 mm) combined, and having a strong team headed up by Patterson, Newpark could bring a premium price. This brings us to our Fun with Numbers segment.

If you take their last good year in fluids (2018), and before the Mats acquisition, Newpark generated $10.53 in revenue per share - RPS - and $110 mm in EBITDA. They're back to $8.31 in RPS, and EBITDA is distorted from the mark to market write down for the sold assets. Let's put an acquisition multiple on the $110 mm of 8X. That gets you to a sales price of ~$9.50 per share for the fluids business, minus the mostly fluids debt of about $1.20 per share, minus a couple of bucks a share for the Mats business. Call it $6.50 per share for fluids, so far. Are we done? Nope.

Newpark is getting ready to receive a boatload of cash, about $130 mm as noted above. Much of which nearly all of which should be apportioned to the fluids business. So, let's add back in that $1.20 per share, and settle on a sales price of about $7.50-$8.00 per share for this business. See, fun with numbers!

Q3 and guidance for Q4

Newpark experienced growth across its product lines, with recent revenues rising ~10% to $219 mm, with fluids contributing $169 mm and Mats-$51 mm. Sequential EBITDA was impacted by a $29 mm write down of multiple assets from the fluids segment. The company has $20 mm of cash on the books, and debt of $157 mm, much of which the company has targeted in the incoming cash influx toward. The company also took steps to reduce SG&A costs with a company wide consolidation to their Katy Technical center for office space, and addition of tenants. ( This place is a palace that was initiated at the peak of the expansionist chutzpah in 2014. )

CFO, Greg Piontek closed out the Q-3 call on a bullish note-

We are encouraged by the longer-term outlook within our core markets in North America land and throughout the EMEA region.

Well there you go!

Risks

First, let's agree that this potential catalyst - although I'm pretty confident based on my experience that something what I suggest is in the cards, is pure, unadulterated speculation on my part. It may not happen, and probably won't happen the way I've mapped out. A spin-off would accomplish some of the same objectives and if no one sees value in the fluids business, may be the way it goes.

Second, Newpark is captive to the rig count. If it rises, revenues increase, with the inverse also being true.

Your takeaway

Right now Newpark is trading at a reasonable 6.8X multiple to EV/EBITDA - if you back out the debt that supposed to go away. The business as a standalone will probably grow this year by at least 10%, thanks mostly to growth forecast in their EMEA market. That would take revenues toward $900 mm and EBITDA toward $90-$100 mm all rolled up. To maintain the current multiple the share price needs to advance to $7.40 per share, or a 60% premium to current prices.

Bottom line, I think growth in Newpark's shares is a reasonable expectation this regardless of what scenario plays out. Risk tolerant investors might want to consider if a risky microcap, like NR fits into their portfolio.

For further details see:

Newpark Resources: A Splash Of Cash And A Potential Catalyst