NR - Newpark Resources: Speculative Buy With Multiple Expansion Potential

2023-09-06 07:30:00 ET

Summary

- Newpark's stock has doubled since May and is drawing the attention of fund investors.

- The company's Fluids business may be divested, leading to a cash infusion and a shift in perception from an OFS company to a rental service company.

- Newpark's Industrial Solutions segment has shown strong growth and profitability, with record revenue and improved margins in the second quarter.

- Rating upgrade - Buy.

Introduction

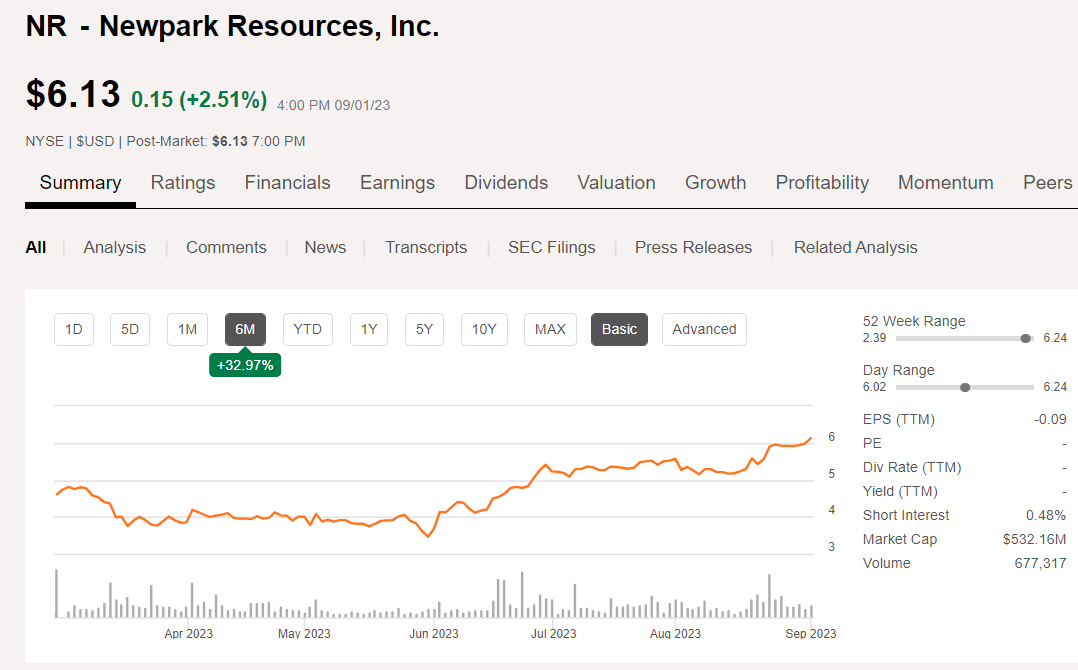

We have followed Newpark's ( NR ) rally for several months now . Since May 31st, the stock has doubled and seems to be drawing the attention of fund type investors with large trading days such as the 23rd of August, where 2.2 mm shares changed hands, well above its normal 2-300K daily trading volume. Clearly something is up with the stock that merits a fresh look.

{kind=link}

The technical pattern for NR is bullish with the stock trading above the 50 and 200 Day SMA and having broken... no "smashed" through resistance in the mid-$4's to reach the low $6's - a level it hasn't seen since late 2019.

The stock has moved so fast that the few analysts that do cover it have been asleep at the switch and missed this momentum entirely . A few seagulls may shift their perch as a result!

The question hanging out there, is there more to come? Or will gravity reassert its dominance and pull NR back down to Earth?

The changing thesis for NR

I documented this shift in the last article in June, where the company had just pushed through the $4.00 level, suggesting folks wait for a pull back to add to positions. That turned out to be the wrong call as the stock continued higher for the next couple of months, as noted above.

In the second quarter conference call, management was a little more specific about the future of its Fluids business than in past calls. (Perhaps suggesting a deal of some sorts may be in the works?) CEO Matthew Lanigan comments on the plans for the Fluids business:

We remain committed to exploring all viable options that are in the best interest of the Fluid Systems business and our shareholders. We are confident that in pursuing this course of action, we will enhance the competitive positioning of the Fluids business and unlock the inherent value in our two divisions for our shareholders, while also positioning our Industrial Solutions business for accelerated growth, transforming Newpark into a scaled, industrial rental and service company. Should we successfully divest the Fluids business, we believe this would create opportunity to further simplify our overhead structure and drive a meaningful SG&A reduction within the remaining organization.

The problems with drilling fluids are that they are totally rig-related - one rig, one mud system, and don't complement many other service lines. They are hideously working capital intensive - particularly for a deepwater project, and require a number of extremely skilled people, one might say almost " Fluidsdoc-ian ", to successfully deploy in the field. I could go on, but let's leave it that Fluids are the " Red-Headed, StepChildren " of the OFS universe.

That brings us to the Industrial segment that is the future of Newpark. I've made the industrial case for Newpark in past articles and I invite you to read some the older articles here for more color. What the market sees is the massive "face-lift" that America is getting in the way of replacing old, worn out infrastructure and installing new-solar/wind farms and the like. All of these activities require remote work site environments, where location access needs to be assured, and dirt and debris controlled in the field support sites. Matthew Lanigan, CEO comments on growth in the industrial segment:

Within our Industrial Solutions segment, our actions to drive sustained profitable growth have yielded encouraging results. On a trailing 12-month basis through the second quarter, Industrial Solutions segment revenue and adjusted EBITDA have increased by 20% and 41%, respectively, driven by our continued penetration of utility projects, improved pricing, along with raw material sourcing and operating cost efficiencies. Importantly, we continue to have a significant pipeline scheduled rental projects and product sales opportunities which positions the business well heading into the second half of the year. We believe our continued organic investment in fleet will equip us to drive sustained, double-digit, annualized revenue growth as we capitalize on accelerating demand in the utilities and critical infrastructure markets we serve.

So there you have it. The market sees two things coming down the road for Newpark. One is a substantial cash infusion from the sale of the Fluids business, and multiple expansion due to deleveraging, and selling inventory in the Fluids business along with the business itself. Finally, the Fluids business gone, Newpark will no longer be viewed as an OFS company - it won't be - and will get a multiple closer to other rental service companies like McGrath RentCorp ( MGRC ), trading at 17X EV/EBITDA.

Q-2, 2023 and Guidance

Newpark generated net income of $1.7 million, or $0.02 per diluted share, on total revenue of $183.3 million, compared to a net loss of $7.8 million, or ($0.08) per basic share, on total revenue of $194.1 million, in the prior year period. Newpark reported Adjusted EBITDA of $19.8 million in the second quarter 2023, or 10.8% of total revenue, compared to $13.3 million, or 6.8% of total revenue, in the second quarter 2022.

Industrial Solutions had another record revenue quarter. Revenues were $48 million in the second quarter, with rental and service revenues representing 83% of the segment revenue. Rental and service revenue was $40 million for the second quarter, a 32% year-over-year improvement. Growth in rental and service revenues reflects continued organic growth within their core utility infrastructure markets.

Industrial Solutions segment profitability remained strong in the second quarter as reflected by the segment adjusted EBITDA margin of 37.7%, a 660 basis point year-over-year improvement. Improved segment margin realization reflects growth in higher-margin rental volumes and continued price discipline, along with improved operating cost leverage, including strong manufacturing and fleet utilization.

The Fluids Systems segment generated revenue of $135 million in the second quarter, representing a decline of 7% versus the prior year period. Segment adjusted EBITDA margin improved 350 basis points to 6.5% in the second quarter. During the second quarter, NR reduced their net capital employed in the Fluid Systems business by $20 million or 8%, reflecting the ongoing monetization of receivables, inventories and excess PP&E as well as the effect of the asset impairments.

Debt stood at $76 mm, down from $88 mm in the prior quarter. They have $22 mm in cash and $80 availability on their ABL as of Q-2.

Guidance

Industrial Solutions revenue is expected to improve sequentially to a range of $52 million to $58 million primarily benefiting from the timing of product sales activity, including the effect of Q2 product orders that were delivered in early Q3.

Fluid Systems segment anticipates third quarter revenue to decline sequentially to a range of $120 million to $130 million, primarily reflecting a decline in the U.S. and a pullback from the record quarter in the Eastern Hemisphere, partially offset by a seasonal recovery in Canada. Expected EBITDA is in the range of $17 million to $22 million, and interest expense of $2 million, while the effective tax rate should be near the 30% level for the third quarter.

Borrowings under the ABL facility declined to $8 million in July. Free cash flow generation is expected in the range of $15 million to $25 million in the third quarter benefiting from solid EBITDA generation and reductions in net working capital primarily within the U.S. Fluids business.

Risks

Risks associated with NR are shifting more to general outlook for the economy and away from an OFS oriented tie to oil gas prices. I think most of the O&G softness is priced in at this point, and we could actually see a rebound as drilling activity responds to the price signal being sent by the oil market.

Your takeaway

Newpark is trading at ~7X EV/EBITDA on a TTM basis at current levels, a figure that could decline to ~3.5X if credit is given for the $200 mm of the Fluids Segment's working capital.

Newpark's Mats systems is in a double-digit growth phase, increasing its market share and seeing an expanding addressable market as discussed. The company is forecasting $80 mm of forward EBITDA for 2023 on an annualized basis in Mats. If we put that 7X multiple on that figure, shares move toward the $6.52 level on Mats financials alone. The sale of the Fluids business and monetization of the inventory should provide further lift, if and when that occurs. If multiple expansion is awarded by the market in the coming quarters, the stock could rally still further.

We have already been richly rewarded by NR since loading up below a buck a few years ago in 2020. I think the investment case for the stock remains strong and am putting a buy on the shares, for investors with a moderate risk profile.

For further details see:

Newpark Resources: Speculative Buy With Multiple Expansion Potential