NEWT - NewtekOne: Q2 2023 Updates Valuation Redo Reiterate Buy

2023-08-07 02:36:38 ET

Summary

- NewtekOne's deposit growth is exceeding forecasts - the bank could reach $1 billion in deposits by Q2 2024. However, its growth is currently bottlenecked by the rate of loan issuances.

- NewtekOne recently hired 3 executives, all of whom are from the former Iberiabank, who I believe form a natural leadership team for NewtekOne's expansion.

- The securitization business, which I ignored in my previous article, has a significant ~20% ROE and cannot be ignored - NewtekOne will continue to recycle loan capital.

- I redo my valuation of NewtekOne, this time including the securitization businesses, and arrive at a value of $736M. A significant margin of safety exists at current prices.

Q2 2023 Earnings Conference Call

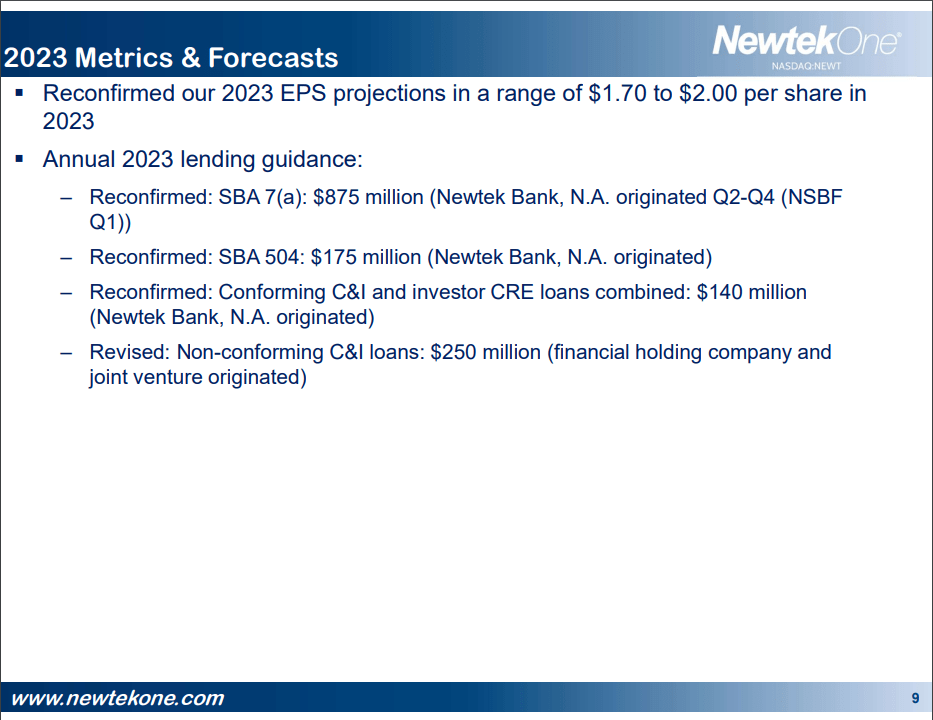

Earnings in Q2 2023 were 26 cents/share, on which 18c/share of dividends were paid back in July. Even though this quarter's earnings are lower than last quarter's earnings, the company guidance is still on $1.70-$2.00/share of earnings for 2023, largely expected to be driven by stronger numbers in the second half of the year.

The most important operational slides are shown below. Lending was strong, and Newtek Bank's net interest margin is beginning to and gradually converging to what it could be once it scales up more. However, there is much more going on underneath the hood. Listening and reading to conference call for this quarter, my biggest takeaways from this quarter were...

Financial Highlights

- Cash and cash equivalent levels were $256.3M, as compared with $197.1M at the end of Q1 2023. This is very much fueled by deposit growth.

- Loans held for investment rose from $699.6M in Q1 2023 to $730.7M in Q2 2023. For every $1 of SBA loans that Newtek Bank issues, it keeps $0.25 of those loans (the unguaranteed portions) on the balance sheet.

- Net interest margin rose from 2.70% to 2.95% to 3.61% as of Q4 2022, and Q1 and Q2 2023. This still has room to grow - NIM should approach 6% over the long run.

- Closed a total of $476.1M of loans in the first 6 months of 2023, which is a 11.2% increase from the first 6 months of 2022.

- Newtek Bank had ROTCE and ROAA of 32.1% and 4.9% for Q2 2023

- Newtek Bank had an efficiency ratio of 58.7% for Q2 2023. As time goes by and the bank scales up more, this efficiency ratio should decrease due to more operational and financial leverage.

- Newtek Bank had risk-based capital ratio of 29.4% and Tier-1 leverage ratio of 16.9%. The bank remains extremely liquid and well-funded.

On the whole, things are running smoothly, despite the many difficulties and headwinds that were overcome behind the scenes due to the bank conversion. However, there are some hiccups here and there. The most notable one is...

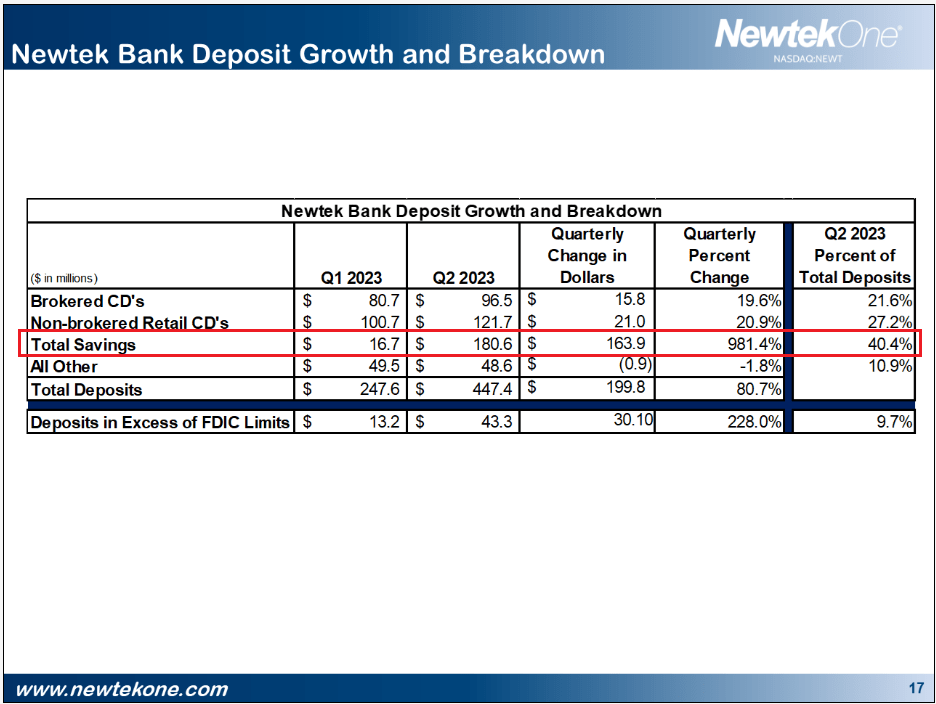

Newtek Bank Has A Glut Of Deposits

Below are the pro forma forecast figures of deposit growth from Q4 2022, presented side by side with the actual reported figures:

| As of |

| Pro Forma & Forecast |

| Actual Reported |

| Dec 31, 2022 |

| $140 million |

| Mar 31, 2023 |

| $227.6 million |

| $248 million |

| April 28, 2023 |

| $310 million |

| June 30, 2023 |

| $371.2 million |

| $447 million |

| Sept 30, 2023 |

| $472.0 million |

| Dec 31, 2023 |

| $590.9 million |

Deposit growth is well ahead of forecasts. Q1 2023 saw $107M in gathered deposits, and Q2 2023 saw $200M in gathered deposits. At this rate of deposit gathering, I'd estimate that NewtekOne (NEWT) will reach $1 billion in deposits somewhere around Q2 2024. The vast majority of the deposit growth has been in high yield personal savings:

Q2 2023 Earnings Conference Call

{kind=link}

However, deposit gathering is only half the story: the other half is putting the deposits to work. NewtekOne currently has over $250 million of cash invested with the Federal Reserve, as of this press release . NewtekOne pays its deposit customers a rate roughly equal to the Fed Funds rate as a way to keep deposits in its bank, which will be dry powder for the SBA lending business.

The strategy here is to give up any interest margins that could be earned on a Fed funds rate - deposit rate differential and hope for a bigger meal down the road: issuing more loans and selling the 75% guaranteed portions for a ~10% premium to the principal.

I have included in this article two "Extra" pieces at the end, that I've tucked away for the sake of continuity. They detail:

- Extra #1: Explains how NewtekOne has constructed pipelines for both gathering deposits and issuing loans. I call this a sort of operational vertical integration.

- Extra #2: A summary of how NewtekOne prices its deposit products and sets up its strategy for deposits.

For now there is some disconnect between the lending arm and deposit accepting arms of Newtek Bank - partly driven by the seasonality of SBA lending, partly driven by operational headwinds related to the recent FHC conversion. I would wait for Q4 2023 figures to look for progress in wanting lending to catch up with deposits - historically, the best quarter for Newtek has been Q4.

My conclusions: I would consider deposit gathering to be largely a solved problem. If NewtekOne wants more deposits, all it has to do is raise the deposit rate on its high yield personal savings accounts an extra fraction of a percent to become the market leader, and new deposits should pour in like a tsunami. I very much hope that the company management will put more of their attention in the near future on putting these deposits to work.

Nonconforming C&I Loans Business - Securitizations To Be Issued Down The Road

From the Q1 2023 conference call, NewtekOne expects to do a significant amount of business in nonconforming C&I loans:

Lending Guidance (Q1 2023 Conference Call)

{kind=link}

An expected $250M of such loans are expected to be made in 2023, however at the time of that call it was unclear to me what NewtekOne would be doing with those loans. Now, that has been clarified during this quarter's call:

Our non-conforming C&I loans are funded at the holding company and joint some of our balance sheet. We exit out via securitizations. This is also a 20% to 30% ROE business.

Instead of issuing and holding these loans to maturity, NewtekOne will instead sell these loans and recycle the capital. Judging from NewtekOne's history with securitizations, I think this is how things will play out.

I would assume that the nonconforming C&I loans would have an interest rate that is comparable with that of the SBA loans, namely prime + 3.00%, or roughly 11.50% in today's environment. The C&I loans would be pooled into a securitization trust, and class A and BBB notes with advance rate ~80% would be sold against that trust, yielding something around prime minus 0.25-1%.

NewtekOne would keep the equity portion of the securitization, and earn the interest rate difference between the underlying and the rates on the notes, about 4 - 5% in total. Since 80% of the capital can be recovered, it can be used to construct another C&I loan securitization, over and over.

The point is, the repeated recycling of capital like this can generate multiple securitization deals using the same capital, hence this is ultimately a 20-30% ROE business. However, since each securitization involves $100M of loans and the guidance is for $250M of C&I loans for 2023, we should expect that it will take several years for NewtekOne to fully build out this strand of business.

However, knowing the advance rate can tell us a lot: 100% minus the advance rate is the amount of equity that NewtekOne "owns" in its securitization business, which can be helpful in the future for valuing the securitization business.

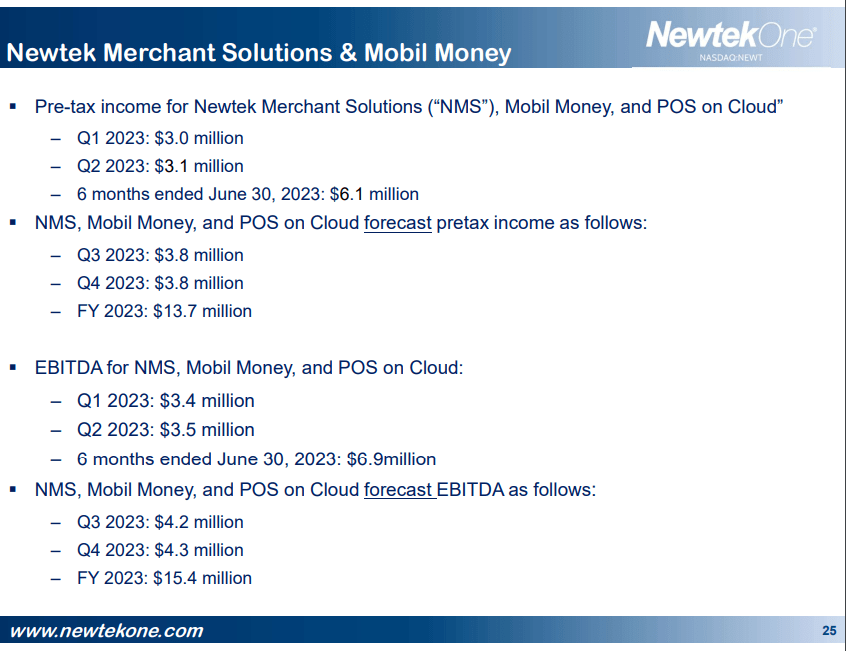

Newtek's Other Subsidiaries - Payment Processing & Tech Solutions

During the conference call, Barry Sloane also touched on the other subsidiaries briefly - enough information to very roughly estimate the value of the subsidiaries, and also some bits on the usefulness of having the payment processing business. Below is the 2023 guidance for combined Newtek Merchant Solutions and Mobil Money:

Newtek Merchant Solutions & Mobil Money Guidance (Q2 2023 Conference Call)

{kind=link}

Expected EBITDA for these subsidiaries for 2023 is $15.4M. Unfortunately, we don't know exactly how that translates into Net Income. Since these subsidiaries are very asset-light, I would personally estimate the net income contribution of NMS and Mobil Money to be about $10M/year, or 65% of EBITDA.

Additionally, NewtekOne will likely be spinning off Newtek Technology Services: it was mentioned that NTS would be spun off / sold, with proceeds going to shareholders within 18 months. This was part of the FHC conversion - business activities sufficiently unrelated to banking would be divested.

Newtek Technology Solutions is expected to deliver EBITDA of $3.7M in 2023. Doing some similar math, I would surmise that NTS contributes about $2M/year to NewtekOne's profits, and applying a 10-12x multiple on it, we can arrive at a value of $20-24M for NTS. Not an insignificant part of the share value.

Acquiring Human Capital - NewtekOne Has Hired Three Former IberiaBank Executives

NewtekOne has been on a hiring spree over the last two years, and the new names really flesh out the company's leadership team. One highly prominent feature of the new hires has been that of three former executives of IberiaBank, which was acquired by First Horizon in 2020. The hope here is that these three people have worked together in the past, and already know how to collaborate because they are known quantities to each other. Additionally, each hire's prior experience is exactly what NewtekOne needs for its scale-up operation. There are three names, each with extensive leadership experiences:

Burt Chandler: Hired in July 2023 as Director of Operations, effectively the COO of Newtek Bank. Last position was SVP / Director of central deposit operations at Bancorp South/Cadence Bank, including leading debit card initiatives. Before that he spent decade at IberiaBank as SVP and Director of Bank Operations. His task at Newtek Bank is to manage the deposit operations and lead Newtek Bank's planned debit card.

M. Scott Price: Hired in May 2023 as CFO of NewtekOne. He has over 17 years of experience in banking and accounting in financial services industries. He spent a decade at IberiaBank as Executive VP, CAO, and Corporate controller, leading a team of 100 employees in corporate accounting, corporate tax, and business unit financial support. He implemented efficiencies across financial processes and supported corporate growth of 3 times over 7 years and 7 acquisitions.

Nicholas Young: Hired in July 2021 as Chief Risk Officer of NewtekOne (while Newtek was still a BDC), as well as President and COO of Newtek Bank. He has over 20 years of experience in credit risk management and mergers & acquisitions and was the former Executive VP and Chief Credit Officer for IberiaBank. Part of the reason why he was hired was to leverage his experience, contacts, and relationships in the banking industry.

I suspect that M. Scott Price and Burt Chandler were hired via their connection to Nicholas Young. These three men are former executives of IberiaBank, which was at its time of acquisition, a regional bank with assets totaling ~$30 billion and a combined total of 325 locations in the Southeastern US. They have experience in running a regional bank, which is what in size Newtek Bank aspires to become.

I believe that these three executives who formerly worked together at the same bank are a ready-made leadership team for NewtekOne as it scales up its banking operations. After all, they willingly chose to work together again 3 years after they parted ways . I think this is a very good sign for NewtekOne shareholders.

Valuing NewtekOne

I would approach this by a sum-of-the-parts approach. There are three parts of NewtekOne that I will consider:

- Newtek's Non-Bank Subsidiaries

- Newtek Bank

- Newtek's Securitizations

I did do a valuation of NewtekOne in my previous article. However, I will repudiate that valuation for a number of errors I made on that valuation and start afresh. In particular, I omitted a valuation of the securitization business, which represents a considerable portion of NewtekOne's profits.

Newtek Non-Bank Subsidiaries

This one is easy for now - there is little information available about NMS and Mobil Money, so I will simply use my valuations from earlier in my article. Applying a 10-12x multiple to my estimates of the net income contributions of Newtek Merchant Services & Mobil Money ($10M) and Newtek Technology Services ($2M), I arrive at a present value of $120-144M .

If it turns out that these businesses have unusual growth potential, then it is worthwhile to revise that number upwards.

Newtek Bank

There are 4 items in my previously published DCF valuation model (link to previous version of model) for Newtek Bank that I think are worth updating:

- Rename "Unguaranteed portion of loans" to "Fraction of Loans Retained", and delete the line for "guaranteed portion of loans retained".

- Initial Quantity of Loans In Newtek Bank: $0M. In the last model I erroneously used $310M which was the quantity of deposits as of Q1 2023. I want the model to only track the SBA loans.

- Initial Year Loans Issued: The Mr. Sloane has issued guidance for 2023 that states that $875M of SBA 7a and $175M of SBA 504 loans should be issued. My old valuation neglected the SBA 504 loans. Hence, I will use $ 1,050M for this parameter.

- Remove the "Time Until Market Saturation" assumption: it seems unreasonable to think that the SBA market will ever stop growing alongside the US economy, and NewtekOne's market share is small enough that it's unlikely to encounter market saturation problems in the medium term.

Click here to see the updated valuation spreadsheet. The coloured boxes contain the other inputs and assumptions used in the valuation. The most important input is the discount rate for the model cash flows, which I have set equal to 10%.

However, the bank is set up to grow very quickly. According to my model, the net income contribution of the bank and the 10x multiple valuation of the Newtek Bank should work out to the following for each of these years:

- 2023: $37.62M net income, worth $376M today in market cap

- 2024: $48.45M net income,

- 2025: $59.36M net income,

- 2026: $70.92M net income,

- 2027: $83.24M net income...

NewtekOne's Securitizations

I have had some trouble in the past trying to value NewtekOne's securitization business. However, I have arrived at a back-of-the-envelope calculation. The advance rate on the securitizations determines the multiplier to the interest margin earned on the securitizations, that leads to a return on equity.

Since the advance rate is ~80%, that multiplier is 5. I reckon a ~4% interest margin to be earned on the securitization trusts, which arrives us at a ~20% ROE for that business. Since our discount rate is 10%, this means that we should value the securitizations at a 2x multiple to the amount of equity that NewtekOne owns in the equity portion of the securitizations (20%). This means that the net present value of the securitization business is worth about 40% the principal value of the loans in the securitization trusts.

Currently, NewtekOne has 5 securitizations outstanding:

- Series 2018-1, principal amount $109M

- Series 2019-1, principal amount $119M

- Series 2021-1, principal amount $103M

- Series 2022-1, principal amount $116M

- Series 2023-1, principal amount $104M

I would therefore estimate the securitization trusts business of NewtekOne to be worth about $220M .

Summing Up The Pieces

The sum of the 3 parts of NewtekOne is $716M . The current market capitalization of NewtekOne is about $460M, implying that there exists a significant margin of safety on the shares if bought at their current price.

This valuation does not differ much from the valuation I made in my previous article, though what it does differ in is acknowledging the present and continued contribution of the securitization business to company profits.

In the present, NewtekOne is operating with all engines running at full throttle, despite the operational difficulties due to the recent FHC conversion and I would not be surprised to see excellent operating results and associate share price gains in the short term and medium term.

Extra #1: NewtekOne Has Vertically Integrated Deposit Gathering And Loan Growth

NewtekOne has several intangible organizational relationship assets at play that help streamline the process of scaling up Newtek Bank. They are the Alliance Partnerships, NewTracker, and the Apiture Partnership. Let's see how they work together:

Alliance Partnerships and NewTracker Secure New Leads For Loans

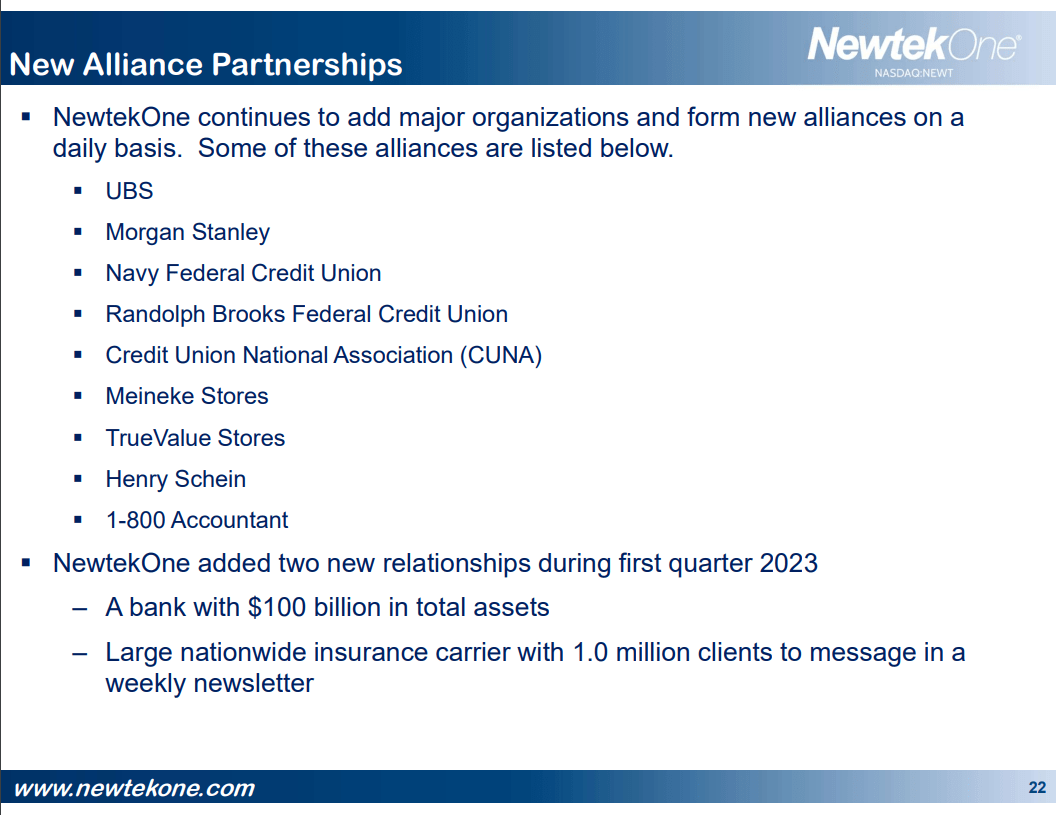

The first stage is the Alliance Partnership. These are agreements between NewtekOne and its alliance partner companies to refer business to NewtekOne in exchange for commissions and fees. As part of the deal, NewtekOne provides marketing support as well as a co-branded website.

Most importantly, entering into an alliance partnership is a win-win arrangement for both NewtekOne and the contracting party. The contracting party is able to retain more business and strengthen their own customer relationships because they have a new avenue (NewtekOne) to refer their clients to for business funding.

As always, NewtekOne is growing its list of Alliance Partnerships, sources of loan referrals in exchange for commissions. The following slide was presented on the Q1 2023 earnings conference call:

NewtekOne Alliance Partnerships (Q1 2023 Earnings Presentation)

{kind=link}

For more on Alliance Partnerships, see here .

The second stage is the NewTracker. Once the referral to Newtek is made, there is no more work left to do for the referrer. The alliance partner can track the progress of the referral on the NewTracker app, which provides full transparency on the referral's progress from submitting a loan application to the final outcome.

NewTracker is available to see on the app store .

Apiture Partnership & Competitive Deposit Rates Fuel Deposit Growth

However, simply getting loan referrals is not enough - where do the funds for issuing the loans come from? In a bank, they should mostly come from depositors, and this is how the Apiture partnership closes this loop. Apiture is a technology services provider to small banks that gives them digital banking capabilities.

NewtekOne's partnership with Apiture means that NewtekOne is now able to open new customer bank accounts online, without need for in person interactions at a physical branch. The idea is that digital banking platforms will not only be more cost effective than banking at physical locations, but also will be a source of funds for issuing new loans.

Find out more about Apiture here at their website .

The average rate that NewtekOne earns on SBA loans is prime + 3.0%, which right now works out to 11.25%. This allows NewtekOne to pay a premium rate for deposits, currently set at 5.00% for their online personal savings accounts, higher than the rates on most other online savings accounts. This allows NewtekOne to strongarm deposits towards the bank.

CEO Barry Sloane has often stated that NewtekOne is a technology enabled bank. NewTracker and Apiture are the two technologies that are central to the complete technological vertical integration of Newtek Bank.

Extra #2: Newtek Bank's Deposits Strategy

A cursory glance at Newtek Bank's offerings strongly suggests that NewtekOne is actively trying to funnel individuals towards its personal high yield savings accounts. Newtek Bank's online high yield personal savings account pays a handsome 5.00% in interest, while its CDs under or equal to 15 months pay 4.60%, under or equal to 24 months pay 4.00%, and over 24 months pay 2.00%.

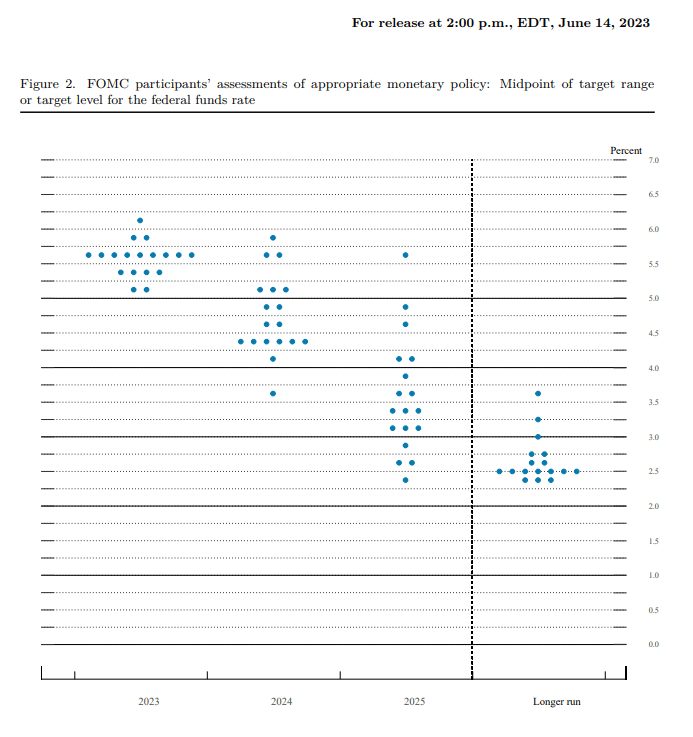

Additionally, the tapering of terms on the offered CD products shows that NewtekOne management is very well aware of interest rate expectations, and price their products in accordance with them. CD rates are strongly tied to Fed Funds rates, which can be forecasted using the Fed dot plots:

Fed Dot Plot, 14 June 2023 (Federal Reserve)

{kind=link}

Here in the most recent Fed dot plot, we can see that the Fed funds rate in 2023 is expected to peak at around 5.75 - 6.00%, and gradually falls to 4.00-5.00% in 2024, 3.50% - 4.50% in 2025, and 2.50 - 3.00% in the longer run. NewtekOne is building in interest rate expectations into its CD offerings today - smart!

Newtek Bank also offers business accounts: business checking at 1.00%, and business savings at 3.50%. I believe that these products are more geared towards the operational needs of businesses, and not maintaining long-term deposits. In fact, the personal savings account can be considered the bedrock of Newtek Bank.

Consider the primary use cases of a 5.00% high yield savings account. Individuals have emergency funds as a separate "bucket" of savings from investments, a pile of cash worth 6-24 months of salary to tide them over through tough times. Another use case is saving for a down payment on a house.

Since this money remains a pile of cash, it needs to be stashed away at the highest interest rate possible. By courting savers to place their emergency funds or down payment savings at a market leading interest rate, NewtekOne builds a deposit base that is less volatile than the deposit bases of other small banks, and reduces the incentives for customers to defect to other banks.

For further details see:

NewtekOne: Q2 2023 Updates, Valuation Redo, Reiterate Buy