NEXA - Nexa Resources: I Stand On The Sidelines

Summary

- NEXA's FY 2022 results reveal improved YoY revenues that failed to translate into bottom-line profitability.

- An improvement in cost performance is the key to ensuring long-term growth as zinc prices remain under pressure.

- With a 5% dividend yield, NEXA might suit the portfolio of some 'income' investors.

- Nonetheless, we believe the stock is a 'hold' keeping in view its limited near-term growth potential.

Thesis

Nexa Resources ( NEXA ) is a large-scale, Latin America-based integrated zinc producer having assets in Peru and Brazil. NEXA's recently published Q4 2022 results disappointed us in terms of non-GAAP EPS of -$0.04, despite a healthy 15% YoY increase in revenues (Q4 2022 revenue=$780 MM). The positive YoY revenues were primarily attributable to higher sales volumes that were met with lower average prices for zinc and related products.

This article will highlight particular aspects of NEXA's business model that have an element of risk. It will also discuss the company's financial and operational performance during FY 2022 together with the key challenges faced by the company. This should help us decide whether NEXA is an attractive investment from a growth perspective. Let's get into the details.

Business Model

NEXA has two operating segments; mining and smelting. The mining business comprises five fully operational underground mines and another underground mining project. Likewise, the smelting business comprises three zinc smelters. The table below highlights the key features of these business operations.

Mining and Smelting Operations - Factsheet (Author-Table 1)

NEXA's business model is robust regarding the diversification of assets and the nature of operations. The company also benefits from product diversification through the following categories:

- Metallic Zinc: Largely used in the galvanization of structures, NEXA's metallic zinc products are categorized into SHG (read: Special High Grade) zinc, CGG (read: Continuous Galvanizing Grade) alloys, and Special Alloys (made from further processing of SHG zinc). These products are produced by NEXA's smelting business segment.

- ZAMAC: ZAMAC (read: Zinc, Aluminium, Magnesium, and Copper) is a zinc alloy widely used in various industries including automotive, construction, furniture, jewelry, etc.

- Zinc Oxide: ZO (read: Zinc Oxide) is obtained through the volatilization of metallic zinc, and has diversified industrial usage in chemicals, tires, animal feeds, fertilizers, etc.

- Zincal: Zincal is an agricultural limestone powder that contributes to the growth of plants and crops. Zincal is obtained from the conversion of the tailings material (or waste material) at the Morro Agudo mine and can be termed a commercially viable by-product.

- Other By-Products: Apart from the above, NEXA's zinc mining operations produce some other commercially viable by-products including copper sulfate, copper cement, sulfuric acid, silver concentrate, cadmium, etc. Besides, metallic by-products (such as copper, lead, silver, and gold) obtained from zinc concentrates at NEXA's mining operations are used to offset the overall production costs of zinc production.

What are the risks in NEXA's business model?

- Unlike precious metals which are considered traditional safe-haven assets and turn-to investments in a time of economic contraction, zinc, and related products do well in a period of global economic expansion. As a zinc supplier, NEXA holds a leadership position in Latin America (approximately 80%+ market share) excluding Mexico and is a strategic supplier of zinc/related products in Africa (approximately 25%+ market share), and other continents (~3% market share in North America and Europe, and ~1% market share in Asia). That said, the risk of global economic contraction directly impacts the demand for NEXA's products. For reference, note that NEXA's annual revenues dropped sharply from $2.33 BB in 2019 to $1.95 BB in 2020 (or 16%), thanks to the global economic meltdown triggered by the COVID-19 pandemic. More importantly, the ongoing Russia-Ukraine war has impacted global industrial demand, and I believe NEXA's revenues may be impacted by this unfavorable macroeconomic development.

- Another related factor is the zinc demand from China. According to Wood Mackenzie, China accounted for approximately 50% and 52% of global zinc and copper demand respectively in 2021. The company states in its 2021 Annual Report (Form 20-F),

Any slowdown in China's economic growth that is not offset by increased demand or reduced supply from other regions could have an adverse effect on demand for our products or commodity prices and result in lower revenues, cash flow and profitability.

- NEXA sells a majority of its products through supply contracts with customers, which typically range between one year and four years. These contracts are renewed throughout different periods during the year and are affected by the prevailing zinc prices as well as their outlook. Only a small proportion of NEXA's zinc products are sold at spot rates. The company's Form 20-F for 2021 revealed that approximately 50% of its 2021 sales of metallic zinc were made to the top 10 customers. Likewise, ~60% of 2021 sales of zinc oxide were made to the top 10 customers, and approximately 90% of total concentrate sales were made to the top 3 customers. On the flip side, NEXA purchases raw materials for some of its products from third-party suppliers. For instance, in 2021, ~50% of the total zinc raw material consumed in NEXA's smelting operations was either purchased from third parties or obtained from secondary raw materials. It's pertinent to note that in March 2021, one of NEXA's third-party suppliers shut down its calcine (raw material for smelters) production facility. Consequently, the company anticipated a decline of ~7% in sales volumes in 2022 compared with 2021. In other words, the supply disruption was expected to reduce annual consolidated smelter production by ~30kT, even though NEXA partially managed to offset this supply reduction by sourcing raw materials from other third parties. In my view, operational difficulties on part of third-party vendors/customers may cause a dent in NEXA's supply chain (as highlighted above), and may also impact its future revenues.

Note that we have quoted certain instances from the 2021 Form 20-F to highlight those risks that are significant in the prevailing macroeconomic business environment, due to the unavailability of Form 20-F for 2022 (expected in March 2023).

Review of FY 2022 performance

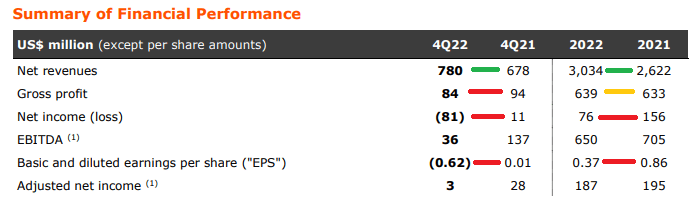

NEXA's FY 2022 revenues of $3,034 MM saw a healthy ~16% increase, YoY (FY 2021 revenues=$2,622 MM). Q4 2022 revenues clocked in at $780 MM (Q4 2021: $678 MM). The company's CEO stated regarding these results ,

The fourth quarter of 2022 marked my first full year as CEO of NEXA, where I focused on increasing efficiency across our organization. We deployed a set of initiatives and new ways of working, which streamlined our cost base ...

The table below shows that despite a notable upside in YoY revenues during Q4 and FY 2022, NEXA's gross profit, net income, and EPS witnessed a stark decline, on a YoY basis. These facts contradict the above statement of the company's CEO which otherwise implies an improvement in NEXA's cost performance during 2022. On that note, it's worth mentioning that NEXA's mining business recorded a whopping 34% YoY increase in consolidated cash cost net of by-products (from $0.21/lb in 2021 to $0.28/lb in 2022). Likewise, the smelting business saw an 18% YoY increase in consolidated cash cost (from $1.13/lb in 2021 to $1.34/lb in 2022). The higher YoY cost performance is attributable to inflationary pressures in 2022.

{kind=link}

The company's other key financial performance metrics including CAPEX of $381 MM (2021: $508 MM), total cash of $516 MM (2021: $763 MM), and net debt of $1,161 MM (2021: $962 MM) all showed a downtrend on a YoY basis. Besides, the company ended the year with negative free cash flows of ~$246 MM.

Things looked a bit better on the operational front though. The mining segment delivered impressive performance in terms of concentrate production. Look at the table below.

| Metal in Concentrate |

| Guidance Range - 2022 |

| Actual Production - 2022 |

| Comment |

| Zinc |

| 287-318 kT |

| 296 kT |

| Met guidance |

| Copper |

| 28-35 kT |

| 33 kT |

| Met guidance |

| Lead |

| 46-55 kT |

| 57 kT |

| Exceeded guidance |

| Silver |

| 8.6-10 Moz |

| 10 Moz |

| Met guidance |

Interestingly, NEXA was able to meet the consolidated production guidance despite failure to meet guidance for the Aripuana project. Moreover, the company's smelting business also surpassed expectations as noted below.

| Metal Sales |

| Guidance Range - 2022 |

| Actual Production - 2022 |

| Comment |

| Zinc metal |

| 528-551 kT |

| 578 kT |

| Exceeded guidance |

| Zinc oxide |

| 37-39 kT |

| 40 kT |

| Exceeded guidance |

Challenges

Apart from the risks highlighted in an earlier section, some other challenges could impact NEXA's operational and financial performance during 2023. We discuss these key challenges below.

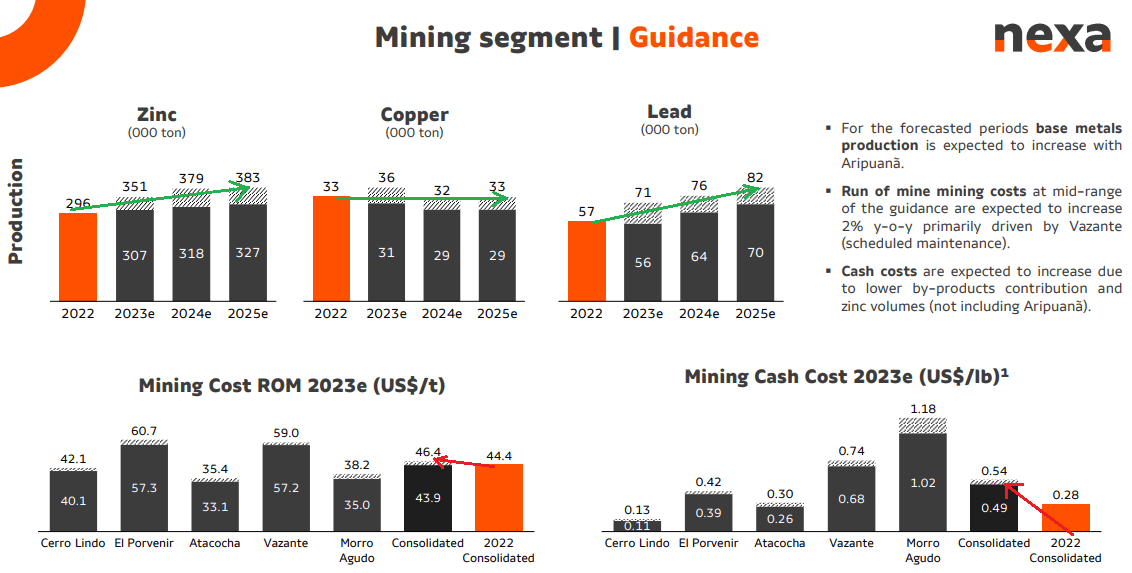

1) Outlook for 2023 and beyond: The thing that bothers me is that despite exceptional production numbers from both business segments together with improved YoY revenue performance, the company's cost and bottom-line profitability remained unimpressive during 2022. Interestingly, the company's 3-year production guidance (2023-2025) for the mining segment reveals an overall uptrend. Nonetheless, the problem of YoY higher production costs is expected to persist. Look at the charts below.

Mining Segment - Outlook for Production and Costs (2022 Results Presentation)

{kind=link}

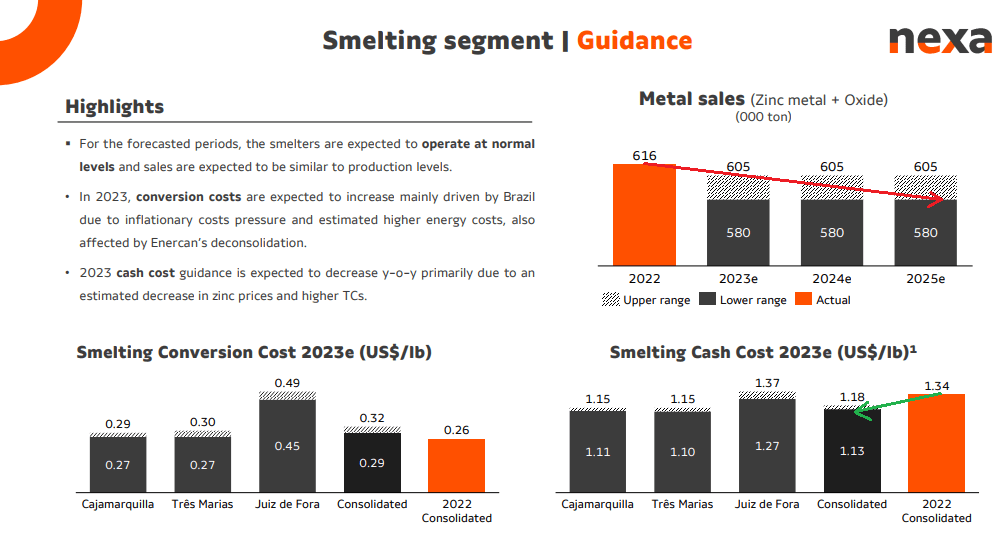

There are mixed expectations for the smelting segment . Metal sales volume is expected to witness a slight decline from their 2022 levels (but remain steady forthwith for the next 3 years). Meanwhile, smelting cash costs are likely to improve in 2023. Look at the charts below.

Smelting Segment - Outlook for Sales and costs (2022 Results Presentation)

{kind=link}

Based on the above discussion, I believe the key growth catalyst for the future is not 'increased production volume' from the mining business segment nor 'increased metal sales volume' from the smelting business segment. These factors do help to uplift the operational outlook but the company should focus on cost reduction if it were to improve its bottom-line profitability, going forward.

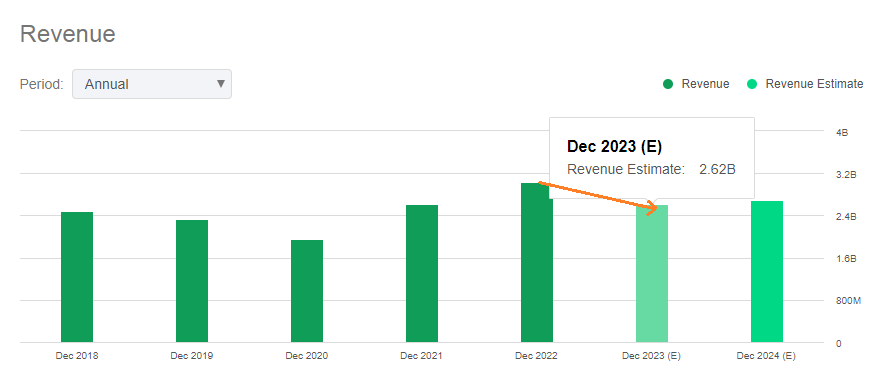

That said, I see that mining cash costs are expected to jump from $0.28/lb in 2022 to $0.49-0.54/lb in 2023 (guidance range), while smelting conversion costs are anticipated to increase from $0.26/lb in 2022 to $0.29-0.32/lb in 2023 (guidance range). Hence, I don't expect any significant improvement in the company's overall financial performance during 2023, on a YoY basis. These expectations are further echoed by the fact that the 2023 revenue forecast is lower than the 2022 actual revenues, as shown in the chart below.

{kind=link}

2) Operational challenges: During 2022, the company's mining operations at the Atacocha mine were suspended multiple times by protests from local communities. The hurdles were cleared typically within 7-10 days but they resulted in lost production.

- On March 17, 2022, the mine road access was illegally blocked by the Machcan community resulting in the suspension of mine production. Mining activities resumed on March 21, 2022, after a successful dialogue with the local community. The estimated loss in zinc production was 0.3kT.

- On May 12, 2022, the mine road access was again illegally blocked by the Joraoniyoc community resulting in the suspension of mine production. Mining activities resumed on May 23, 2022, resulting in an estimated loss of 0.3 kT of zinc production.

- On August 29, 2022, the mine road access was again illegally blocked by the San Juan de Milpo community resulting in the suspension of mine production. Mining activities resumed on September 12, 2022, resulting in an estimated loss of 0.4 kT of zinc production.

- On January 03, 2023, the mine road access was illegally blocked once again by the Machcan community resulting in the suspension of mine production. Mining activities resumed on January 09, 2023, after NEXA had engaged with the local community. The estimated production loss is between 0.2-0.3 kT.

Another potential problem is the weather conditions at the Brazilian assets. The Vazante project is located in the Minas Gerais State of Brazil which is one of the coldest regions in the country and receives the most rain during the November-March period . During Q1 2022, heavy rainfall resulted in partial flooding of the lower levels of the Vazante underground mine, thus limiting production to ~60% of its nameplate capacity. The Aripuana project is located in the State of Mato Grosso which receives the most rain during the October-April period. In 2022, heavy rainfall caused operational stoppages and power outages at the site of the Aripuana project. In my view, heavy rainfall during peak monsoon seasons could disrupt operations at NEXA's Brazilian assets which have relatively attractive mining dynamics compared with their Peruvian counterparts (more on this later).

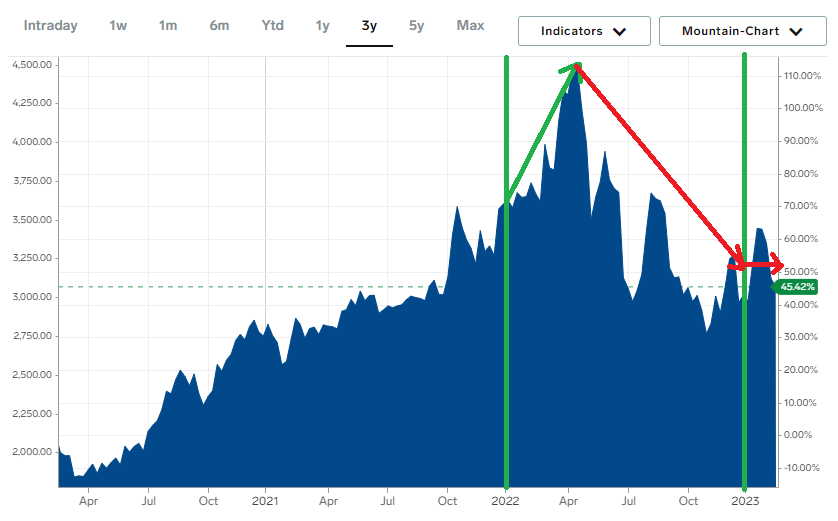

3) Depressed zinc prices: As noted earlier, only a small portion of NEXA's zinc sales are made at spot prices. Nonetheless, the prevailing zinc prices and the expectation of zinc's price outlook impact the price agreed upon in contracts with third-party customers. During 2022, zinc prices witnessed a multi-decade high of ~$4,500/ton before witnessing a reversal trend following global macroeconomic concerns stemming from the Russia-Ukraine conflict. At present, zinc prices are in the range of ~$3,000/ton. Higher average zinc prices supported the company's revenues during 2022. On the flip side, lower average zinc prices are likely to adversely impact NEXA's revenues during 2023, on a YoY basis.

{kind=link}

4) Division of Resources: Another potential problem that I see is the division of resources between NEXA's Peruvian and Brazilian assets. Based on the information in Table-1 above:

- The Peruvian assets classified under the mining segment have a total nameplate throughput capacity of ~31.8 ktpd, while the Brazilian assets for the same segment have a nameplate capacity of ~12.6 ktpd. The Peruvian assets have >2x the nameplate throughput capacity than the Brazilian assets. It's worth noting that the nameplate capacity for the Brazilian assets includes 4.6 ktpd attributable to Aripuana which is an asset under development. At the beginning of February 2023, ~60% of the nameplate throughput capacity was reached (approximately 2.76 ktpd) at Aripuana. Regarding the smelting business segment, the Peruvian smelter has a processing capacity of 344.4 ktpy which is more than the combined processing capacity of the two Brazilian smelters (96.9 ktpy + 192.2 ktpy= 289.1 ktpy).

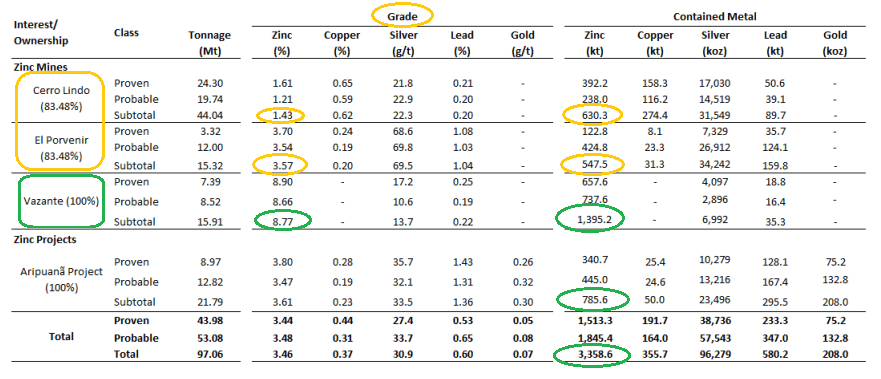

- In March 2022, NEXA published information regarding mineral reserves and resources at its mining assets latest as of December 31, 2021. I noted that Cerro Lindo (a Peruvian asset) had the lowest zinc grade at 1.43% compared with the other mining assets. The total P&P (read: Proven & Probable) zinc reserves of this Peruvian mine are only 630.3 kT which is less than 1/2 that of the Vazante mine (a Brazilian asset); at ~1,395 kT. Interestingly, the Vazante mine's reserves have an average zinc grade of 8.77% which far exceeds the grade of both Peruvian assets namely Cerro Lindo and El Porvenir (EP's zinc grade=3.57%, EP's zinc reserves=547.5 kT). If we add the 785 kT zinc reserves of the Aripuana project (another Brazilian asset), we conclude that out of the total P&P zinc reserves of 3,358 kT, ~2,180 kT (or 65%) reserves are attributable to NEXA's Brazilian assets. Finally, the Brazilian assets (Vazante and Aripuana) have a longer mine life (of ~11 years) compared with the Peruvian assets (Cerro Lindo=8 years, El Porvenir=7 years). Look at the following table for details.

{kind=link}

- The problem is, Peruvian assets have lower zinc grades, lower reserves, and greater processing capacity than their Brazilian counterparts. Since zinc prices and the macroeconomic factors that impact zinc's demand/supply dynamics are beyond NEXA's control, the only way to improve bottom-line profitability is to focus on cost reduction. At present, a greater proportion of the company's resources are tilted toward Peruvian assets instead of Brazilian assets. For reference, note that ~52% of the company's 2022 exploration program was allocated to the Peruvian assets, while only ~40% was allocated to the Brazilian assets (the remainder was allocated to other geographies). I believe this whole situation makes it difficult to improve NEXA's overall cost performance in the near term.

The Light At The End Of The Tunnel

NEXA is a top zinc producer in Latin America. Even though I expect the company's FY 2023 performance to be affected by multiple risks/challenges that we've discussed in detail above, I expect things to improve over the medium-to-long term due to the expected Aripuana ramp-up to nameplate capacity by H2 2023. In my view, greater resource production from promising Brazilian assets will benefit the company over the long term.

Additionally, the company has a ~$110 MM exploration program (for 2023) to increase the expected life of the mines, and to better define the underlying mineral resource at its mining assets. The company's liquidity position remains strong despite a total outstanding debt of ~$1,669 MM since structured debt repayments will begin at least 4 years from now. Look at the company's debt profile below.

NEXA's Long-Term Debt Profile

Finally, the company has maintained a dividend yield of ~5% during the last 12 months which is a moderate yield to appeal to an 'income' investor. A special dividend of $0.18/share was approved by NEXA's Board this month, and the company anticipates possible additional dividend payment during H2 2023. It's pertinent to mention here that NEXA has consistently paid dividends during the last 5 years.

Nonetheless, considering the risks in NEXA's business model, its operational and financial performance during 2022, production and cost guidance for 2023, as well as the metal price outlook (especially zinc prices), I conclude that NEXA's share price is unlikely to deliver any significant growth in the near term unless the company improves its cost performance, or there is a notable increase in zinc prices from the current levels. Otherwise, the share price is likely to oscillate within the range of $6-7.50. That said, I believe the NEXA stock is a 'hold' at least in the near term (next 12 months).

{kind=link}

For further details see:

Nexa Resources: I Stand On The Sidelines