NEXA - Nexa Resources: Things To Consider Before Jumping On The Bandwagon

2023-08-21 08:16:12 ET

Summary

- Depressed zinc prices have hurt NEXA's revenues during Q2 2023, and may continue to impact revenue growth in the near term.

- Cost optimization is the key to improve bottom-line profitability, and Aripuana's ramp-up to full scale can significantly help in this area.

- Forecasts for 2023 and 2024 reveal declining YoY revenues and EPS, implying limited room for near-term share price growth.

- NEXA has regularly paid dividends during the last 5 years, however, I believe the dividends may take a cut going forward.

- It may appear that NEXA is trading cheaply based on certain valuation metrics, however, I see this as an indicator of a low-growth stock at least in the near term.

Thesis

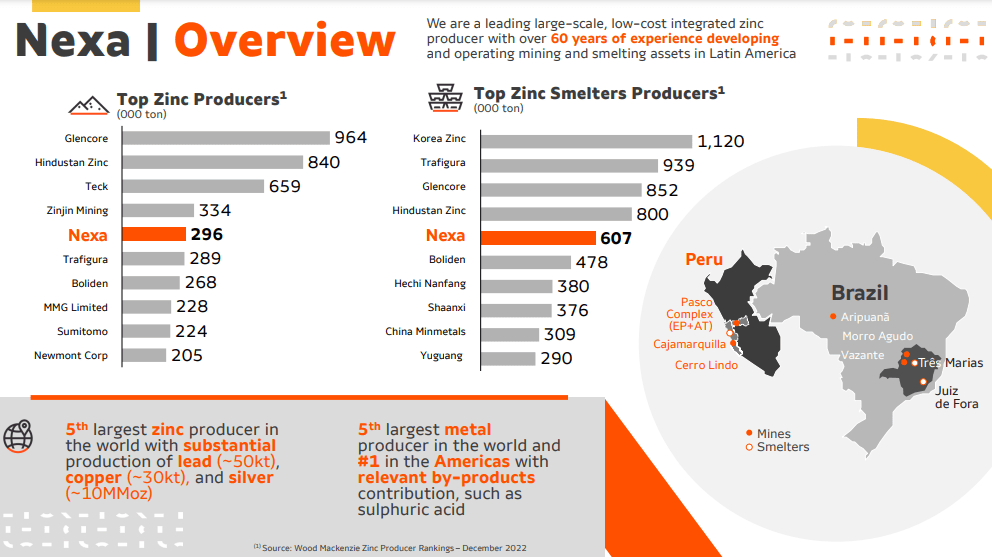

Nexa Resources S.A. ( NEXA ) is a Latin America-based integrated producer of zinc-related products with a portfolio of five underground mines and three smelters, in addition to an underground mining project. All its assets are strategically located in either Peru or Brazil. The company enjoys a top 10 slot in the global zinc producers/ metal producers list, according to Wood Mackenzie's December 2022 'Zinc Producer Rankings', and has been in business for over six decades.

{kind=link}

For a company of such repute, one would expect robust performance in terms of financial position, revenue growth, cost optimization, bottom-line profitability, dividends, and more importantly, stability in the share price. However, NEXA's performance on many of these metrics remains questionable. For instance, the share price recorded a whopping 30% decline during FY 2023 (from $7.47 in January 2023 to $5.10 at the time of writing), pushing the stock toward the lower end of its 52-week range (between $4.14-7.70).

Given NEXA's position as an industry leader in zinc-related products, one might be tempted to believe it's an attractive investment at the current price levels. However, as we will discuss in our analysis, one needs to carefully assess the headwinds that impact multiple aspects of NEXA's financial and operational performance thereby limiting the stock's near-term growth potential—time for the details.

Q2 2023 Review - Results and Expectations

NEXA's 2Q23 revenues clocked in at $627 MM (down ~25% YoY), with non-GAAP EPS of $0.04. To quote the company's CEO on this occasion (relevant extracts only, with emphasis added by the author),

In 2Q23, we experienced an increasingly volatile macroeconomic environment, driven by persistent U.S. inflation, and concerns about the Chinese economy. These factors put downward pressure on base metal prices, with zinc prices falling 19% and copper 5% compared to 1Q23.

Some of these headwinds are persisting and continue to weigh on metal prices and our business. Although we expect LME prices to remain under pressure , we remain committed to financial discipline, evidenced by a portfolio of initiatives focused on cost reduction , plus CAPEX and working capital optimization which are being implemented. These initiatives have allowed us to achieve positive cash generation in 2Q23. Despite this challenging environment, we are maintaining our production and cash cost guidance.

Let's analyze the key aspects of the above statement of NEXA's CEO:

1) Zinc Prices - Headwinds Are Likely To Persist: The first thing pointed out by the CEO (and rightly so) is pressure on zinc prices, which is typically the lifeline for a producer of zinc-related products. Also, from a sensitivity analysis perspective, the market price of underlying products is the most sensitive factor to a project's after-tax NPV. Put another way, a change in the price of the key product (zinc in the case of NEXA) significantly impacts the value proposition associated with a product/business segment, etc.

Trading Economics - Zinc's 5-year price chart

Zinc's 5-year price chart reveals a persistent uptrend from March 2020 onward which peaked in April 2022 (at ~$4,400/t) before reversing to the present-day levels between $2,400-2,500/t. Zinc prices have shrunk by more than $2,000/ton during the past 15 months.

For background, note that China's industrial production data for April 2023 showed a 5.6% YoY growth against the forecast of 11%. This lower-than-expected demand growth led to a decline in copper and zinc prices. However, recent hopes of demand recovery from China support base metal prices. Nonetheless, S&P Global expects the demand for global refined zinc to grow by ~1.4% due to tight monetary policies adopted by both the US and Europe. In contrast, the supply of global refined zinc is expected to grow by 1.9%.

In my view, this marginal imbalance between supply and demand for global refined zinc will keep a check on zinc prices, and prevent any significant near-term upside in zinc prices.

It's pertinent to mention that spot zinc prices do not directly impact NEXA's sales since only a tiny portion of the company's revenues are attributable to zinc sales at spot prices. Instead, the company enters into supply contracts whose term ranges between 1-4 years. Nonetheless, the prevailing zinc prices do impact NEXA's contract pricing with suppliers 'indirectly' in the following manner:

- Concentrate sales are made at LME reference price minus a discount based on treatment charges.

- Metallic zinc/ zinc oxide sales are made at the average LME quotation prices during a quotation period (which may include the month before/ after the shipment, etc.).

2) Cost Reduction - A Challenge: The second thing pointed out by the CEO was initiatives aimed at cost reduction. I find it challenging to agree with the CEO's statement on this. Given the declining trend in zinc prices during the past 2 years, cost optimization is the only way forward if NEXA is to retain its edge in this competitive industry. Unfortunately, the company is having a hard time managing its overall cost performance.

For reference, note that NEXA's "consolidated cash costs net of by-product credits" for its mining segment increased from $0.21/lb in 2021 to $0.28/lb in 2022, and further increased to $0.37/lb during Q2 2023 (latest reported quarter). The increase in cash costs was due to lower contributions from by-product credits, and higher treatment charges. Although Q2 cash costs for the mining segment were well within the 2023 guidance range between $0.49-0.54/lb, it doesn't help improve the overall picture, especially in a depressed zinc price environment.

On the flip side, the consolidated cash costs for the smelting segment increased from $1.13/lb in 2021 to $1.34/lb in 2022 but reduced to $1.12/lb during Q2 2023 (at the lower end of the 2023 guidance range between $1.13-1.18/lb). The sharp decline was mainly attributable to lower prices of zinc which is the primary raw material for the smelting segment.

Although the cost performance from the smelting segment may look impressive, I believe that due to the following three reasons, it'd be challenging for NEXA to improve its overall cost performance going forward:

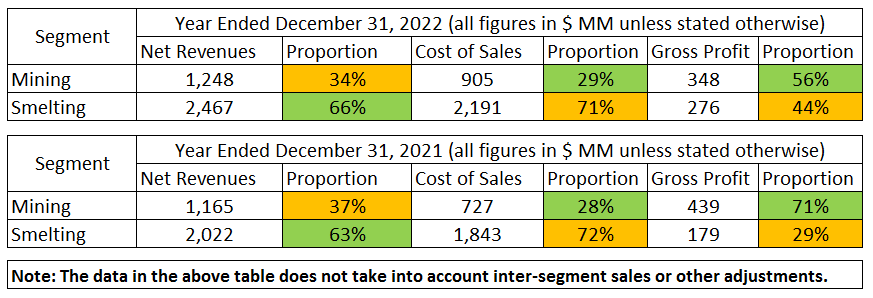

First, the smelting segment accounts for a lower proportion of NEXA's annual gross profit than the mining segment, despite having a higher share of revenues, and an even greater percentage of 'cost of sales'. Check Table-1 below.

Table-1: Segment-wise Proportion of Sales, Cost of Sales, and GP - Source: Author

{kind=link}

In my view, NEXA would need further improvement in the cost performance of the smelting segment to have a notable positive impact on its overall cost performance.

Second, although the proportionate share of the smelting segment's gross profit has increased from 29% in 2021 to 44% in 2022, NEXA lowered its 2023 production guidance from the smelting segment. On that note, the segment's 2022 production of 616kT is estimated to shrink to the range of 580-605 kT and remain within that range during the 2023-2025 period.

In my view, due to the frequent stoppages at one of the Peruvian mines (Atacocha, check Table-2 below), the risk of floods following heavy rainfalls at the Brazilian assets (resulting in production stoppages and/or lost production), and the fact that a sizable portion of the mining segment's production is used as the raw material for the smelting segment, one may expect the smelting segment's 2023 production to come out at the lower end of the guidance range. This could impact NEXA's overall cost performance during 2023.

Table-2: Suspension of Atacocha's Operations - Source: Author

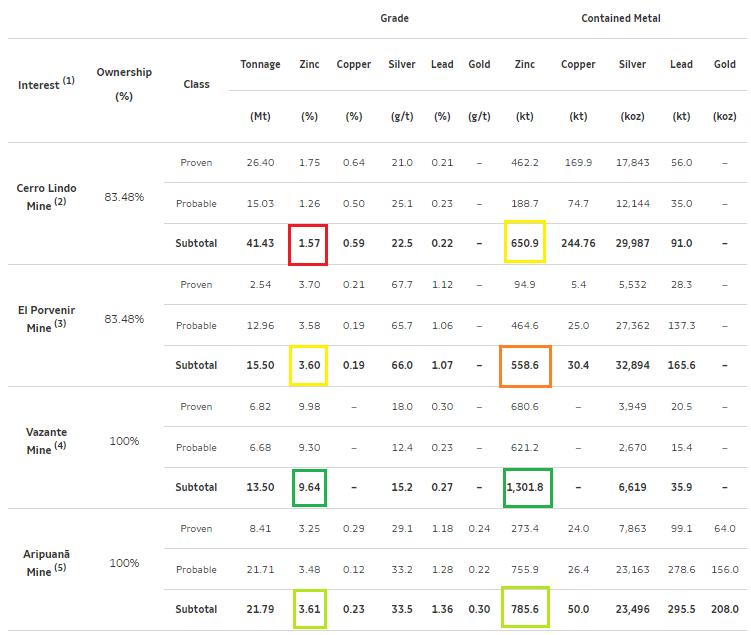

Third, the company has not improved its cost performance from the attractive Brazilian assets. Look at the following table highlighting the P&P (read: Proven & Probable) Reserves of NEXA's Brazilian (Vazante and Aripuana) and Peruvian (Cerro Lindo and El Porvenir) assets.

{kind=link}

The table clearly shows that the Vazante mine (or VZ) in Brazil is currently the best asset in NEXA's portfolio in terms of both zinc grade and metal contained. Its estimated metal reserves (of ~1,302 kT) are more than the combined reserves of the two Peruvian assets namely Cerro Lindo (or CL) and El Porvenir (or EP).

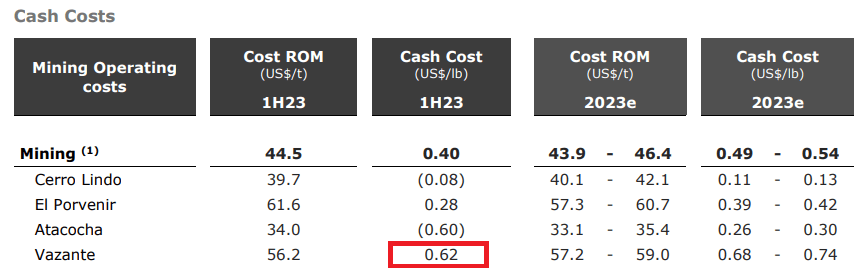

However, despite having the best zinc grades among all mining assets (which generally implies lower mining costs), the Vazante mine incurred higher cash costs than its Peruvian counterparts during H1 2023. Take a look at the table below.

Table-4: Mine-wise cost performance during H1 2023 - Source: NEXA

{kind=link}

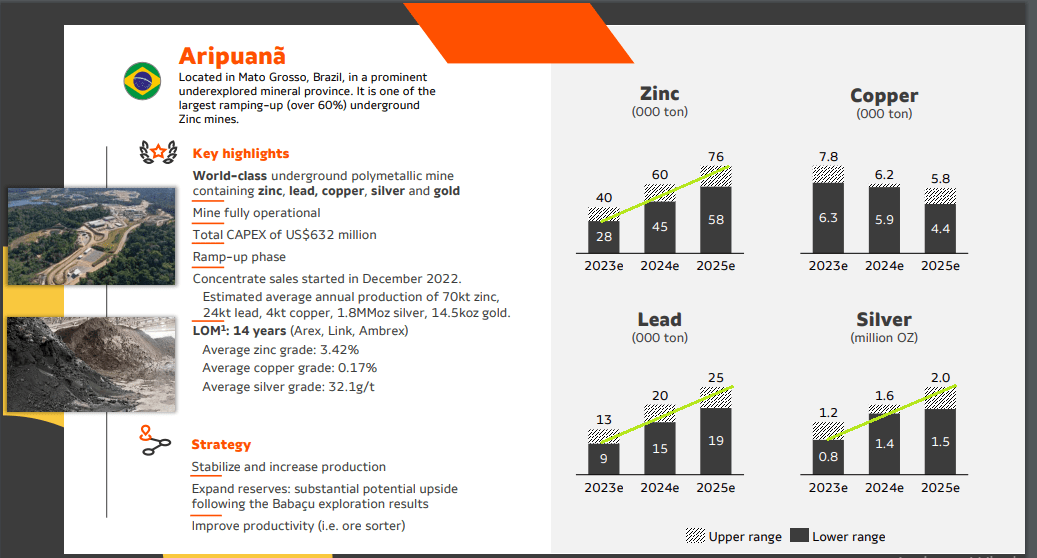

Aripuana - The Way Forward?

Perhaps one reason why Vazante's cash costs are higher than the others (check Table-4) despite having far better zinc grades than its Peruvian counterparts is lower by-product credits. As seen in Table-3, Vazante lacks any copper reserves (compared with 244.76 kT for CL, and 30.4 kT for EP), and has only ~6.62 Moz silver (compared with 29.98 Moz for CL, and 32.89 Moz for EP), and 35.9 kT lead (compared with 91 kT for CL, and ~166 kT for EP).

This is where the promising Aripuana project (or AP) comes in. A closer look at Table-3 also reveals that Aripuana has:

- average zinc grade of 3.61%, better than the average grades of CL and EP;

- zinc reserves of 785.6 kT, far better than both CL and EP;

- copper reserves of 50 kT, better than EP;

- silver reserves of 23.49 Moz, far better than VZ and nearly matching the reserves of CL and EP;

- 295.5 kT of lead, far better than any other mine; and

- 208 Koz of gold, making it the only asset in NEXA's portfolio with gold resources.

The above numbers indicate that Aripuana's ramp-up to full-scale production will not only support high-end zinc production, it will also help ensure low-end costs thanks to the availability of sufficient by-product credits from the production of both base metals (copper and lead) and precious metals (gold and silver). The company is progressing on Aripuana's development and expects to achieve the nameplate throughput capacity (of 6.1 ktpd) in H2 2023. Meanwhile, NEXA has already incurred almost half of the planned project CAPEX for Aripuana. Note that out of the total project CAPEX of $632 million, at least $355 million has been spent to date. Other project enablers include a long LoM (read: mine life) of approximately 14 years which is capable of extension based on ongoing exploration activities, the potential for enhancing the reserve base through conversion of mineral resources into reserves at promising orebodies such as Ambrex, Babacu, etc.

Nonetheless, it should be noted that Aripuana's zinc, lead, and silver production is expected to increase gradually over 3 years (2023-2025). Therefore, I believe Aripuana's development is less likely to have a notable impact on NEXA's production and cost profiles during 2023. Look at the figure below.

{kind=link}

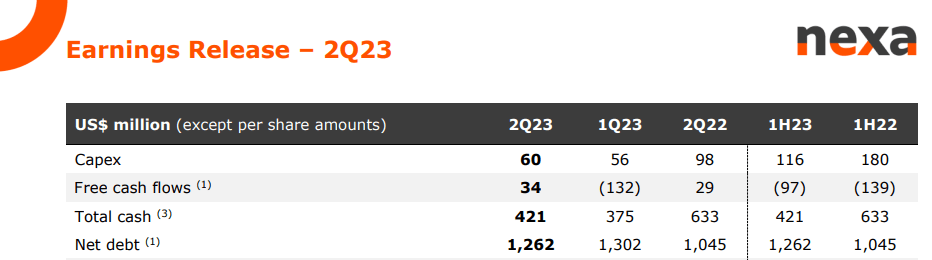

3) Positive FCF Generation During Q2 2023 - Is It Sustainable? I think NEXA has done well by generating positive free cash flows of $34 MM during Q2 2023. This compares favorably against the negative FCF of ~$132 MM during Q1 2023. Notably, this Q/Q FCF growth (to the tune of ~$166 MM) was achieved despite an increase in CAPEX (from $56 MM in Q1 to $60 MM in Q2) primarily due to favorable working capital changes.

{kind=link}

Can NEXA sustain this positive FCF generation?

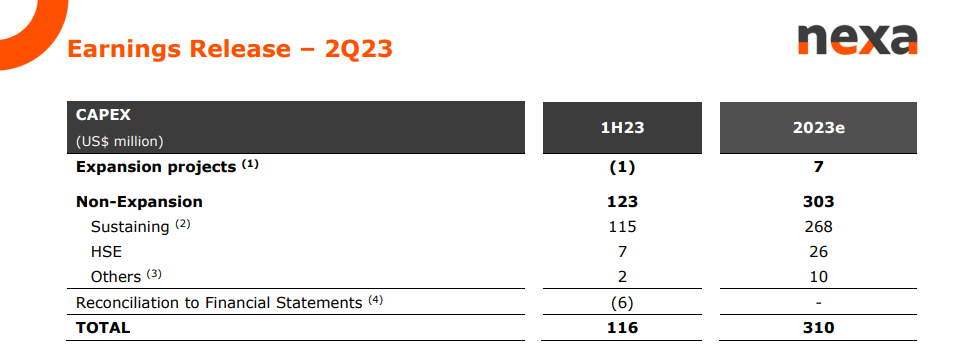

I think it would be challenging because CAPEX investments are likely to surge during H2 2023. On that note, NEXA expects to incur CAPEX of ~$310 MM during 2023 out of which only ~$116 MM has been incurred during H1 2023.

{kind=link}

This implies that NEXA's CAPEX spending during H2 will be ~$195 MM (or ~1.7x the CAPEX spent during H1) if it follows the 2023 guidance - and that is sure to put pressure on NEXA's FCF growth during H2 2023.

Valuation

NEXA's Wall Street Rating on the Seeking Alpha quote page shows that 10 analysts rated it during the past 90 days, out of which 2 rated the stock as a 'Strong Buy', 6 rated it as a 'hold', and 1 analyst each rated it as a 'Sell' and 'Strong Sell'.

Wall Street Rating - Source: Seeking Alpha

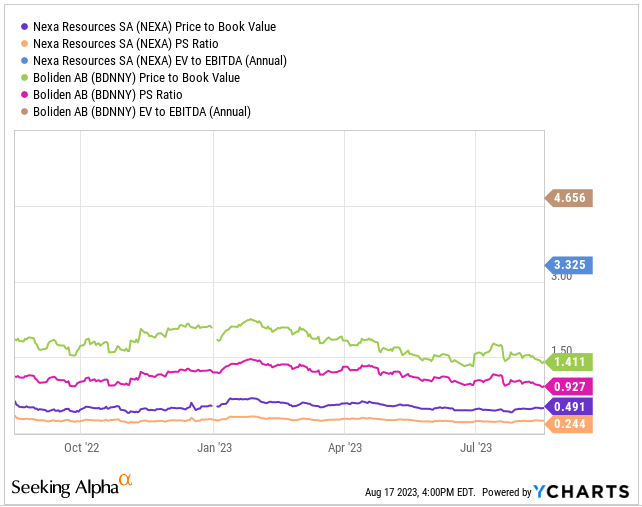

I think those rating it as a 'Strong Buy' must be impressed by the stock's apparently-attractive valuation. The company's TTM PB ratio is ~0.49x with a forward value of 0.50x. For comparison, I have selected Boliden AB ( BDNNY ) as its business model is largely similar to NEXA with a notable difference being its operational presence (which is in Europe rather than in Latin America). The Chart below shows that NEXA has a more attractive valuation than BDNNY on multiple valuation metrics including the Price-to-Book, Price-to-Sales, and the EV to EBITDA ratios.

{kind=link}

Nonetheless, a low PB valuation is not always indicative of an attractive valuation. It could also mean that the market has low expectations about the stock's near-term growth potential. So let's check the company's expectations for revenue and non-GAAP EPS for 2023 and 2024.

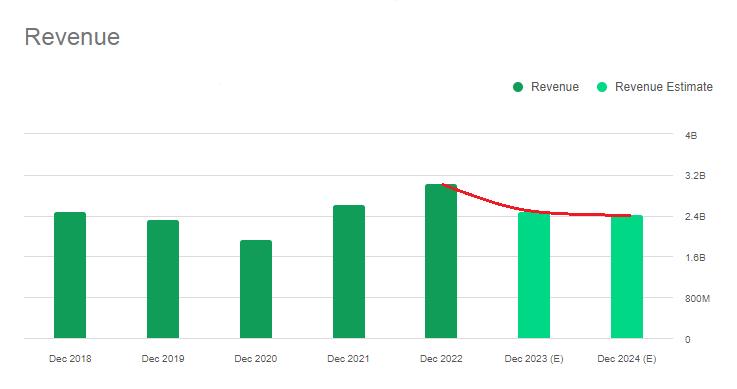

Revenues: NEXA's revenues are expected to shrink from ~$3.03 BB in 2022 to ~$2.48 BB in 2023, and further decline to ~$2.43 BB in 2024. Look at the chart below.

NEXA Resources - Revenue Expectations 2023-24 - Source: Seeking Alpha

{kind=link}

In my view, a depressed zinc price environment is primarily responsible for the lower YoY revenue expectations, besides the operational level challenges such as mine stoppages (e.g. Atacocha), or lost production from flooding triggered by heavy rainfall at some of the Brazilian assets during the dry monsoon season (October-April).

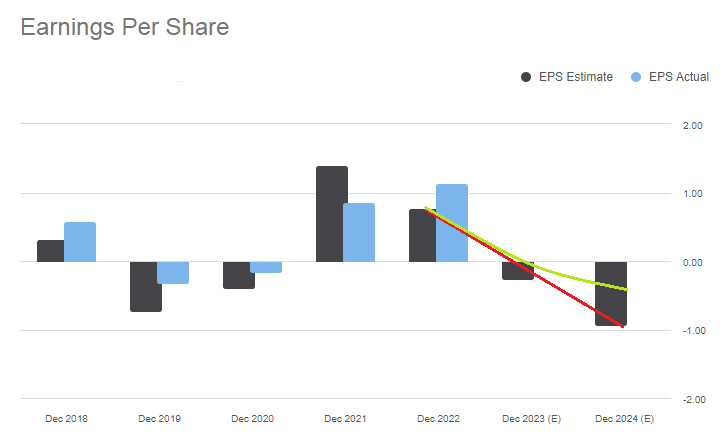

Earnings: Similarly, NEXA's non-GAAP EPS is expected to reduce from $1.14 in 2022 to a negative $0.27 in 2023, and further deteriorate to negative $0.93 during 2024. Look at the chart below.

NEXA Resources - Non-GAAP EPS Expectations 2023-24 - Source: Seeking Alpha

{kind=link}

NEXA's 5-year trend for non-GAAP EPS shows that the company beat expectations during 4 out of the last 5 years. Hence, we can assume that non-GAAP EPS for 2023 and 2024 will exceed expectations (due to, say, cost improvement attributable to higher YoY production from Aripuana).

Nonetheless, the annual non-GAAP EPS is likely to remain negative for the 2023-24 period, especially given the multiple cost optimization challenges (discussed in detail earlier) and lower revenue expectations, YoY, for the period under review.

The bottom line is, given the adverse trends in both expected revenues/EPS during the 2023-24 period, the stock's near-term growth prospects remain low. This explains the low PB valuation. The stock is not a 'Strong Buy' as it's only fairly valued, in my view.

Dividend Cut On The Cards?

With low near-term growth prospects (NEXA's 'Growth' rating is D+ on SA Quant Grades), one wonders whether the stock is an appealing income investment, given its leadership position in the industry and robust business model.

In my view, NEXA is not a promising income investment and due to the following reasons, investors could witness a dividend cut going forward:

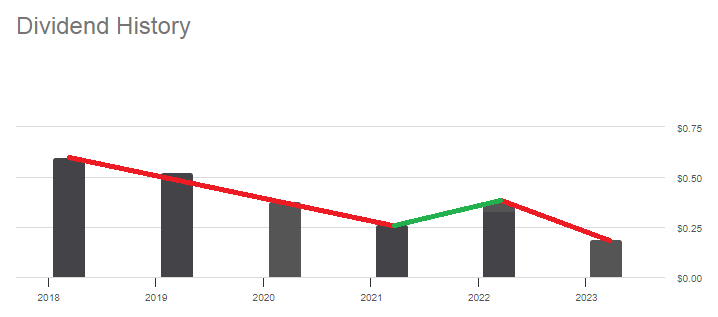

1) Dividend history shows a declining YoY trend in annual payouts (2022 was an exception when a favorable zinc price environment enabled the increase in payout).

{kind=link}

2) The YoY expectations for revenue and EPS growth for 2023 and 2024 are adverse (discussed earlier) which makes little sense for increasing the payout in the near term.

3) Expected higher CAPEX investments in H2 2023 (discussed earlier) will put pressure on FCF during H2. This may also impact future dividend payouts.

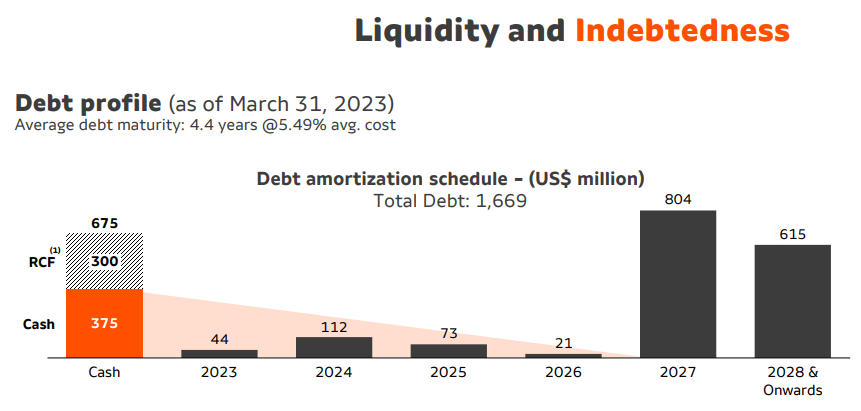

4) Finally the company's debt maturity profile indicates significant debt repayments falling due in the next 5 years. If low zinc prices continue to take a toll on NEXA's future cash inflows, the company will prioritize repayment of debt falling due in the next 5 years (to the tune of ~$1,010 MM by 2027, and ~$615 MM from 2028 onward), besides cash allocation for exploration activities and necessary CAPEX investments. NEXA may also restructure the debt. Nonetheless, these headwinds may impact future payouts.

NEXA's Debt Maturity Profile - Source: Presentation - May 2023

{kind=link}

On a related note, NEXA's 3-year dividend yield averaged ~3% (2.6% in 2021, 4.2% in 2022, and 2.8% in 2023). In my view, an attractive yield for a miner of NEXA's size should be around 5%.

3-Year Dividend Yield - Source: May 2023 Presentation

Investor Takeaway

The preceding analysis indicates that NEXA's share price has a fat chance of witnessing any significant near-term growth (say, 12-18 months) despite trading at the lower end of its 52-week range. This is primarily due to the depressed zinc prices which are impacted by volatility in the macroeconomic environment including a decline in industrial demand from China. These challenges are expected to persist in the near term. Another challenge is to improve the overall cost performance (the mining segment's cost performance deteriorated while the smelting segment's performance improved marginally) to notably improve bottom-line profitability.

Moreover, NEXA's revenues and EPS (non-GAAP) are anticipated to shrink in the 2023-24 period. However, the mediocre growth outlook doesn't help the stock's dividend appeal either. In fact, due to anticipated pressure on FCFs during H2 2023, and significant debt repayments falling due within the next 5 years, I believe NEXA may cut its dividend payout in the near term. The above factors also explain why NEXA is trading at an apparently cheap valuation.

Nonetheless, NEXA's following catalysts are capable of fuelling share price growth:

- A sustained improvement in zinc and copper prices (near-to-medium-term impact) ;

- Aripuana ramp-up to full capacity which would help improve NEXA's overall cost performance (medium-to-long-term impact) ; and

- Expansion of mineral reserves (through conversion from resources) through exploration at high-value targets like Babacu, Ambrex, etc., or the extension of LoM of existing mines (long-term impact) .

That said, I believe the stock is a 'hold' at present.

For further details see:

Nexa Resources: Things To Consider Before Jumping On The Bandwagon