NXRT - NexPoint Residential: A Solid Dividend And Large Discount

2024-01-03 14:54:39 ET

Summary

- NexPoint Residential Trust is a residential REIT that owns and manages multi-family properties in the Southwestern and Southeastern U.S.

- The REIT's portfolio is widely diversified across large markets and has shown strong operating performance.

- Most importantly, the stock price is currently trading at a discount to NAV and results in an attractive dividend yield which looks safe.

NexPoint Residential Trust, Inc. ( NXRT ), founded in 2014 and headquartered in Dallas, TX, is a residential REIT that owns and manages multi-family properties which are mainly located in the Southwestern and Southeastern U.S.

This company has a widely diversified portfolio, an attractive growth record, and a healthy solvency profile; its shares are also trading at a large discount to NAV and the dividend appears safe. Let's start with its portfolio...

Portfolio

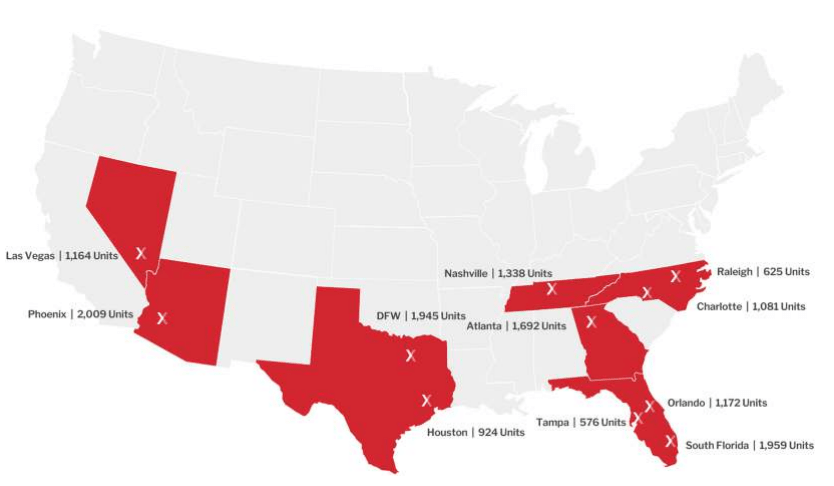

As of September 30, 2023, the REIT owned 39 multifamily properties which consisted of 14,485 apartment units spread across 11 markets in Texas, North Carolina, Georgia, Tennessee, Florida, Nevada, and Arizona. Below is the geographical distribution of these assets:

{kind=link}

Obviously, these are all large markets NexPoint operates in and the portfolio is widely diversified at that. That's useful if you are looking for multifamily real estate exposure and don't own any REITs operating in the same states.

Additionally, no market contributes to the REIT's NOI to an alarmingly high degree:

Investor Presentation

Performance

Coming to operating performance, you can see how fast the company's revenue grew over the years. Though FFO expanded too, it did so more erratically and it experienced a downtrend after 2020.

Coming to more recent results, approximately 94% of the REIT's apartments were leased as of September 30, 2023, which is a pretty common occupancy rate level these days for residential REITs. Within the context of NexPoint's diverse portfolio, I think it's decent, but there is surely a good margin for higher efficiency.

Now, the latest operating results depict even higher growth. Below, I have calculated the increase from the average annual figures of the past 3 fiscal years to the corresponding last quarter's figures annualized:

| Rental Revenue Growth |

| 21.45% |

| Same-Property Cash NOI Growth |

| 38.79% |

| AFFO Growth |

| 6.97% |

Regardless, the stock price is now trading around pandemic levels after it quadrupled from the 2020 low up until it started falling in 2022; about the time the Fed started raising rates.

Leverage

When it comes to its financial health, the REIT has two contradicting factors here. On one hand, its assets are 68.51% financed with debt, which is a bit high for my taste. On the other one, its liquidity is strong with a debt/EBITDA ratio of 6.9x and interest coverage at 1.38x.

Of course, I appreciate the lack of a chart depicting ever-increasing leverage; NexPoint's leverage level has been fluctuating around 65-75%. At the same time, I don't love the absence of a definitive upward trend when it comes to interest coverage.

Speaking of which, the company's mortgages and credit facility carry a weighted average 6.89% interest rate. This is high, but maturities both in the short and the long term don't pose any significant threat. Therefore, I don't expect a higher cost of debt in the future. I would argue that a lower one is more likely, considering where the Fed is expected to move the rate this year.

Investor Presentation

Dividend & Valuation

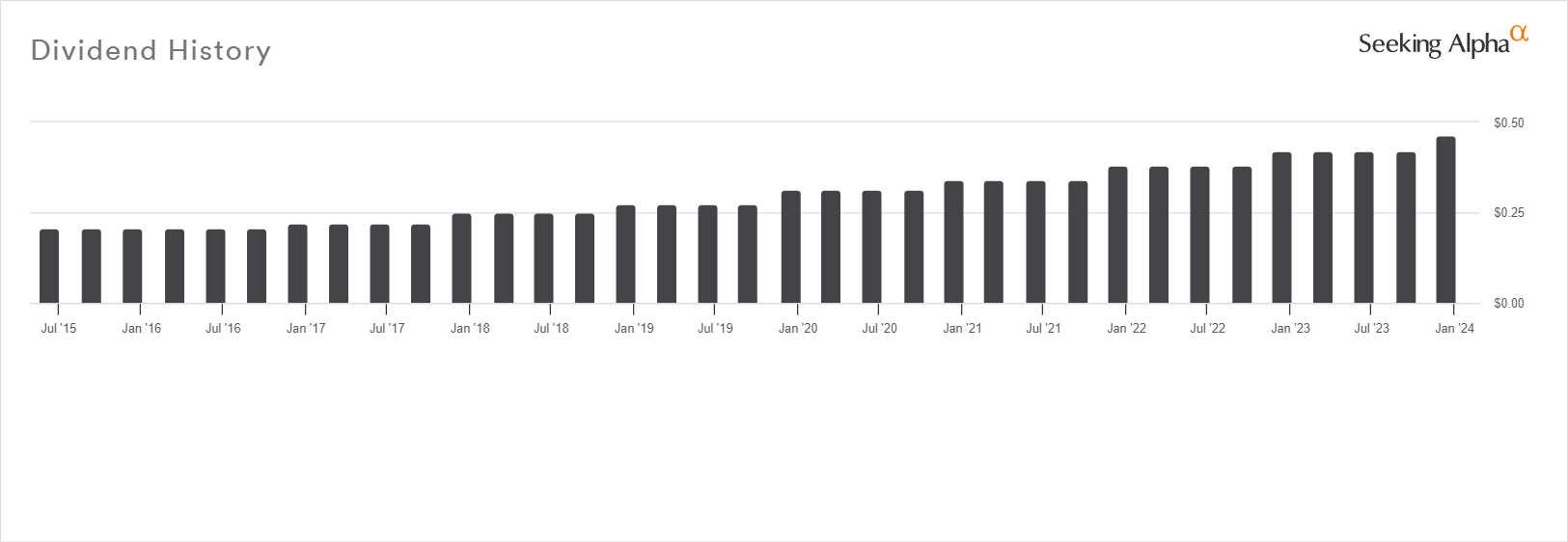

NexPoint currently pays a quarterly dividend of $0.46 per share which results in a 5.28% forward yield. I believe that the distribution is safe from the prospect of a cut or suspension. First, the REIT has established a dividend-growth status through its payment record, which depicts 8 years of consecutive dividend growth:

{kind=link}

Second, its payout ratio of 58.95% based on AFFO is low enough to provide both a margin of safety if profitability decreases and a margin for further business expansion.

The REIT also looks attractive because of the price its shares are trading at. Its current implied cap rate is 6.56%, which I find unreasonably high. First, a third-party review of NexPoint's properties gave a cap rate range of 5.5-6% as applicable as per the company's last investor presentation. Second, with average cap rates forecast to fall below 5% for multifamily properties in 2024, I believe that a range of 5-6% is the most appropriate here to capture both the value of the REIT's assets today and in the near term.

As a result, we can get a NAV approximation of $43.33 to $63.30, reflecting a 19.64% and 44.99% discount, as well as suggesting a 24.45% to 81.79% upside. This is a pretty wild range but it should serve as a reminder that NAV calculation is not an exact science.

Now, the stock price has actually increased above $90 per share in the recent past; much higher than NAV based on a 5% cap rate (the most aggressive assumption). It actually started falling around the time the Fed rate hikes began in 2022:

Therefore, this offers good ground for assuming that the recent fall from grace was driven by non-fundamental factors. And this is something important we should keep in mind when we observe an undervaluation.

Risks

There are two risks present that you should be aware of though. First, reality may not meet expectations and cap rates could expand. In that case, your margin of safety may narrow or be removed. How each investor handles that varies, so it doesn't have to necessarily shake your confidence in your decision. I, on the other hand, would look where to reallocate my funds if I become pessimistic about real estate values.

There is also an opportunity risk because the dividend yield is decent, but not as high as so many other REITs offer these days. In the scenario where the market doesn't reprice the stock to the degree that would realize the upside for years, the dividend wouldn't be able to offset an opportunity cost. I know I can't be alone in favoring a concentrated portfolio over dozens of REIT stocks at a time, so the opportunity risk applies to investors like me to a large extent; I want to be compensated to a high degree from the dividend returns if the price doesn't match NAV for years. This is not likely with NXRT.

Verdict

All in all, I believe that NXRT presents an attractive investment opportunity, so I am rating it a buy at current levels.

What's your opinion? Do you agree with this thesis? Let me know below and I'll get back to you as soon as I can. Thank you for reading and happy new year!

For further details see:

NexPoint Residential: A Solid Dividend And Large Discount