EYPT - Next Round Of Financing Will Be Transformational For Ocular Therapeutix

Summary

- Ocular Therapeutix is a promising platform play poised to disruptively transform ophthalmology. Based on its innovative and validated hydrogel platform, Ocular can fill and expand its pipeline with unlimited new applications.

- With Dextenza, Ocular has an approved and profitable commercial product and is confident that its new strategy will accelerate its growth in 2023.

- There are other compounds in the pipeline, each targeting a multi-billion dollar market with significant unmet medical need and blockbuster potential.

- By the end of the year, Ocular could advance these compounds into pivotal trials. First, however, Ocular needs to secure funding through business development activities.

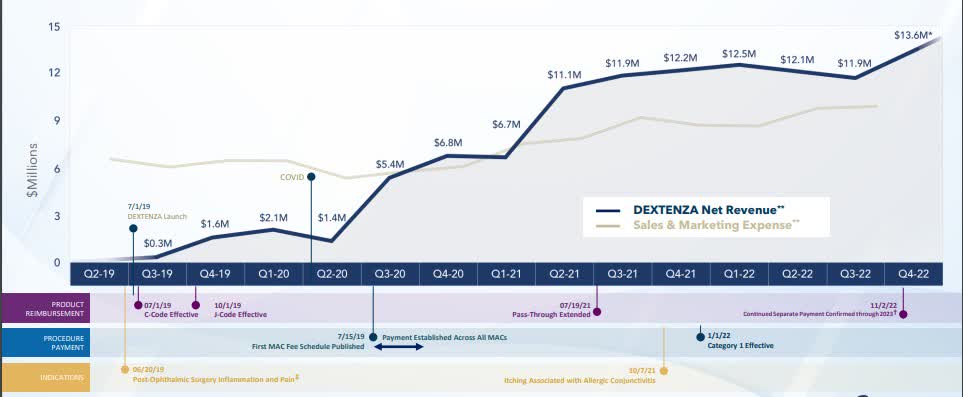

After almost a year, it is time to take another look at Ocular Therapeutix ( OCUL ). In summary, it has been a very mixed year for Ocular. On the one hand, positive study results were finally published, but stagnating Dextenza revenues raise questions about the value of the asset.

Dextenza was a key part of my investment thesis. While investors were able to benefit from the OTX TKI data run in the short term, the rally was not sustainable despite the strong data.

My expectations for Dextenza were not met by Ocular in 2022. My core idea of steadily increasing Dextenza sales in 2023, which would cover the majority of the company's costs and provide a value base, was not met. Instead, Dextenza was only marginally profitable in 2022, generating approximately $1 million in the last quarter after deducting sales and product costs.

Despite last year's mixed performance, I remain convinced of Ocular's potential. Dextenza continues to represent the value floor and the company is confident in its ability to return sales growth in 2023. In addition, recent pipeline developments are very encouraging. Including business development activities, Ocular aims to advance all relevant compounds into pivotal Phase 3 ready assets by the end of the year.

Therefore, in this article, I will review Dextenza's sales activities, highlight the pipeline developments, and discuss potential business development activities.

Business of Ocular Therapeutix

Ocular is a commercial-stage biopharmaceutical company focused on formulating, developing and commercializing innovative therapies for diseases and conditions of the eye. Ocular has an approved product, Dextenza , which is already profitable and offers further growth potential. Beyond the approved product Dextenza, the company is advancing its pipeline based on its proprietary bioresorbable hydrogel platform technology . Ocular is committed to disrupting ophthalmology by eliminating the need for eye drops and injections.

The hydrogel platform opens the door to new, innovative, differentiated and long-lasting drug delivery solutions. With the ability to deliver any ocular drug based on hydrogel technology, Ocular can fill and expand its pipeline with unlimited new application areas. The concept of the hydrogel platform has been validated by the approved drug Dextenza and is very safe. In addition, Ocular only uses established and approved drugs as active ingredients.

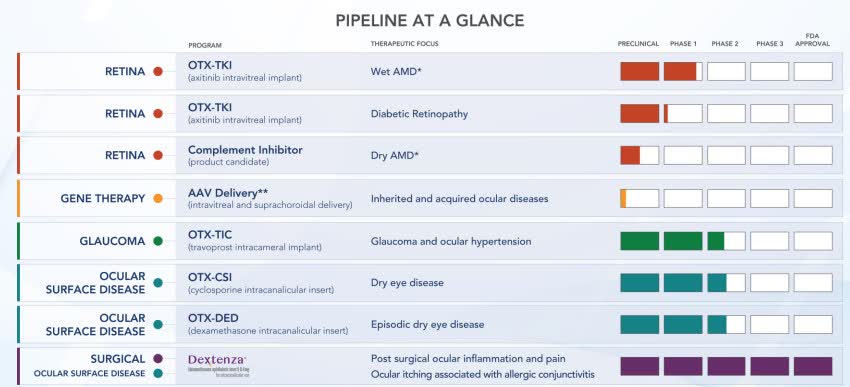

Ocular is committed to advancing a broad portfolio of ophthalmic products. (Source: Company Presentation)

{kind=link}

Although Dextenza is already approved and profitable given its small sales infrastructure, Ocular is focused on its clinical development pipeline as it addresses both larger and more attractive markets.

Each product candidate has blockbuster potential (Source: Company Presentation)

Each compound in the pipeline addresses a multi-billion dollar market with significant unmet medical need and blockbuster potential. In addition, all upcoming studies will be pivotal Phase 3 studies, with initial discussions with the FDA already underway and the first study could start as early as Q3 2023.

For interested readers, I recommend my other two articles on Ocular:

- Ocular Therapeutix: Positioned For Long Term Gains : An introduction to the Hydrogel Platform and targeted indications.

- Ocular Therapeutix Stock: Transformative Year Ahead : An introduction to the current treatment after cataract surgery and an assessment of the market potential of Dextenza

Reviewing Dextenza Sales Activities

Dextenza's sales force is lean and therefore profitable, which is very unusual in the biotech industry, but it is not able to sustain the growth rates and build on the momentum. Despite positive trends in the fourth quarter, the company missed its 2022 guidance and generated only $50.2 million in total revenue .

Dextenza's net revenues have exceeded sales and marketing expenses and continued overall growth (Source: Company Presentation)

{kind=link}

To get back on track, the company not only identified the limiting factors, but also developed a strategy to stimulate further growth.

Relative to the potential of the opportunity and our own expectations, the sales of Dextenza represent a disappointing result and is clearly unacceptable.

Source: Mattessich, Q3 Business Update

Factors creating headwinds for Dextenza sales

Dextenza had great momentum at launch in 2019, which was then squashed by the Covid hit. Ocular struggled in 2022, despite the removal of near-term restrictions, with three significant chronic pressures attributed to Corona.

The first problem , which affects a number of different industries, is a shortage of labor and the chronic understaffing that results from it. Ocular understands that its customers, ASCs and HOPDs, are in a difficult situation and are understaffed by as much as 20% , particularly on the administrative level. In the current environment, customers are reluctant to add additional work and complexity. Many potential customers simply do not have the capacity to introduce Dextenza, even though they know and appreciate its benefits. In addition, many customers continue to operate below capacity due to staffing challenges.

The second factor affecting Dextenza's performance was the inability to maintain an experienced field sales force with minimal vacancies. However, Ocular has announced that this issue has been resolved , as reflected in the strong fourth quarter. The team is fully trained and visiting customers on site, which should lead to continued growth.

The third reason is the changing reimbursement landscape for procedure codes. Ultimately, the biggest driver of revenue is adequate physician reimbursement. For example, product volume decreased significantly with the introduction of the Category I code in 2022. While Category I has the advantage of being reimbursed by all payers, physician reimbursement was reduced. As some physicians saw their reimbursement for procedure-related costs cut from up to $250 to $35, they stopped using Dextenza for economic reasons. Ocular expects that by early 2024, the value proposition for patients will also be reflected and balanced in fair incentives for physicians in both the ambulatory surgery center setting and the hospital outpatient department setting.

Most important going forward, though, is not about what has caused the slowdown but how we plan to reignite growth.

Source: Mattessich, Q3 Business Update

Factors driving future Dextenza sales

Overall, however, Ocular believes it is well positioned for further growth in 2023, for which it has developed a growth strategy. The strong fourth quarter is the first sign of success. This outlook is also supported by the following factors.

The first growth driver is local customer support and a clear focus on ambulatory surgery settings. Ocular's sales force is at full capacity and the team is well trained and in the field. In addition, it has been recognized that while the office setting offers a greater market opportunity, the focus in the short term should be on the ambulatory surgery setting. For one thing, the patients are concentrated in this area, and for another, Ocular benefits from the know-how and experience that has been built up, which improves the return on investment.

Office space needs investments to launch, I don't see going big into office environment within the next year or two without a partner or massive investments.

In addition to filling all vacancies, the focus is also on expanding the customer base and deepening engagement. On the one hand, existing customers are becoming more familiar with Dextenza, and on the other hand, Ocular has made tremendous progress with payer coverage and reimbursement. Today, Ocular focuses on Medicare B patients because they do not want their customers to have a bad experience in the market. In 2023, Ocular wants to help its customers move beyond Medicare Part B patients and bring Dextenza to commercial patients. These patients are an important source of growth, and management expects this approach alone to result in growth of more than 30% in billable units for the existing customer base. In addition, Ocular has been successful in convincing new customers of the benefits of Dextenza, including the acquisition of a large strategic customer with multiple facilities at the end of 2022.

Further growth potential arises from changes in reimbursement for Dextenza's competitor Dexycu from EyePoint Pharmaceuticals ( EYPT ). Starting this year, physicians will no longer be separately reimbursed for the use of Dexycu. Ocular expects 100% of these patients to switch to Dextenza (~10,000 billable units). Physicians are already convinced by the drop-free therapy and the two products are substitutable despite their differences. As there is currently no overlap in prescribers between Dextenza and Dexycu, this will increase Ocular's customer base with little to no effort.

Pipeline Developments

Ocular is currently advancing all of its programs with the goal of moving all of them into potential pivotal trials as the next step, so I will briefly discuss the developments in each program and explain the steps Ocular is taking to achieve this. For an introduction to each program, I would like to refer you to my first article .

Ocular Surface Diseases (OTX-CSI, OTX-DED)

In the current year, Ocular would like to explore an acceptable placebo insert with no effect on efficacy that can be used in future trials. If the trial results show what Ocular believes they will show, the programs will move forward. But the priority right now is to de-risk them by finding a more appropriate placebo.

Glaucoma (OTX-TIC)

Following the publication of the Phase 1 interim results for OTX-TKI, OTX-TIC results are attracting increasing attention. Glaucoma represents a slightly smaller market opportunity, however the market is less competitive and the barriers to regulatory approval are lower. If Ocular can demonstrate that OTX-TIC does not harm the eye and is therefore suitable for repeatable dosing, the chances of approval are very high. Top line results from the Phase 2 clinical trial are expected in the fourth quarter of 2023.

Retinal Diseases (OTX-TKI)

The interim results from the Phase 1 study of OTX-TKI demonstrate that Ocular is able to delay intravitreal injections by several months using OTX-TKI. Proof of concept has been established and Ocular is targeting a timely meeting with the regulatory authority to be ready to initiate a Phase 2/3 study in the third quarter of 2023.

The OTX-TKI study provided the most compelling data in wet AMD, particularly in terms of durability. The data are even more remarkable when you consider that many patients received rescue injections, even though this was not part of the protocol. Physician failures can be attributed to the standard of care. Today, fluid is a sign of drug degradation. In the case of OTX TKI, however, the drug is continuously administered; for example, some patients improved between months 5 and 7. For an analysis of the 10-month interim data, I would like to recommend the following article by Amit Ghate .

According to the protocol, the Phase 1 study will follow subjects until at least the anniversary of the first day of dosing.

Following the success and proof of concept of OTX-TKI in wet AMD, a trial in another indication was quickly initiated. A Phase 1 study in Diabetic Retinopathy ('DR') was initiated in December 2022. This indication could also move into a potential registration study as early as the first quarter of 2024.

Compared to wet AMD, Ocular believes this indication has the advantage of less competitive pressure, a lower regulatory hurdle and more cost-effective Phase 3 trials. While Ocular for example expects a Phase 3 trial in wet AMD to cost up to $450-$500 million, a pivotal trial in DR is expected to cost $80-$85 million. This is related to the fact that a trial can be tested against placebo due to the lack of standard therapies.

In summary, the durability of the hydrogel platform opens up many new opportunities and markets for Ocular.

Financials & Business Development Activities

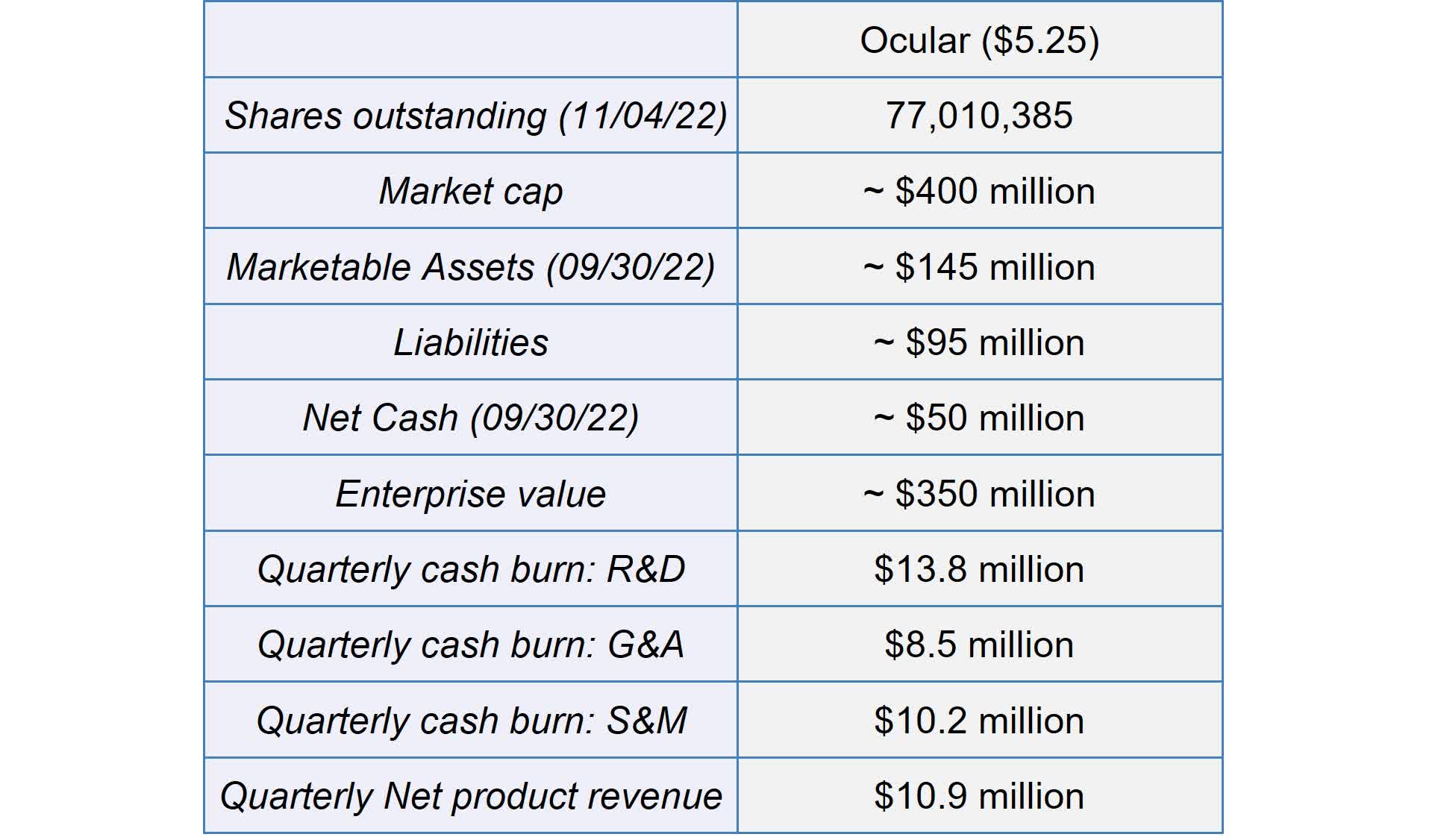

At the end of the year, Ocular had approximately $102.3 million in cash and cash equivalents and the cash runway is expected to last until mid 2024. Last year, over $50 million in revenue was generated from Dextenza, which slightly offset the cash burn. At the current share price, Ocular has a market capitalization of about $400 million, and the market ascribes the pipeline a value of $350 million.

Consistent with the strategy of bringing the Company's core development programs in wet AMD, diabetic retinopathy, glaucoma and dry eye to Phase 3-ready status, the Company believes that it has sufficient cash and cash equivalents to fund planned operating expenses, debt service obligations and capital expenditure requirements through the middle of 2024.

Source: Ocular Therapeutix

Financial overview (Source: Author's Chart)

{kind=link}

Due to the low cash position, cost management is a hot topic at the moment. Looking to the future, the company is carefully evaluating which investments to make. Fortunately, management rejects the idea of a capital increase and excessive dilution of existing shareholders. For this reason, in addition to increasing sales, I want to address the company's business development opportunities.

Selling more Dextenza is the best way to get more non-dilutive cash.

Source: Mattessich, Piper Sandler Annual Healthcare Conference

Business Development

In my opinion, the market will only appreciate and fairly value the potential of the pipeline once the funding for the pivotal trials is secured. Existing cash resources are currently insufficient to advance the clinical development pipeline into Phase 3 trials. However, Ocular has already announced that it will not pursue dilutive capital raises in the current environment and at current share prices. As such, the focus will be on potential business development activities.

Ocular has many options and believes it is in a strong negotiating position. With Dextenza, Ocular has an approved and profitable product. Ocular could leverage its sales force by in-licensing another product or make another company's sales force more efficient by out-licensing Dextenza.

In order to estimate the potential value of Dextenza, Ocular conducted a market research study. The study indicated that multiples in the range of 5 to 15 times trailing 12 month sales are reasonable for comparable transactions. Based on these calculations, an out-licensing of Dextenza with sales of $50 million in the last 12 months could provide Ocular with non-dilutive capital in the range of $250 million to $750 million. In addition, partnerships to market Dextenza globally are another option. All in all, Dextenza is definitely monetizable in many aspects.

With all assets ready for Phase 3 trials, these can also be incorporated into business development activities. There is strong interest in assets with proof of concept and addressing large markets with high unmet medical needs. The scope of business development activities is unlimited.

For Ocular, for example, partnerships to commercialize the products outside the U.S. play an important role. Another possibility for a partnership would be to share both research costs and revenues. Non-dilutive forms of investment, such as selling royalties or raising additional debt, also play a role.

Summary

Overall, I remain very bullish on Ocular and believe the stock continues to trade below fair value. The approved sales product Dextenza alone covers the current value, while the rest of the pipeline continues to represent blue sky potential. According to management, Dextenza is worth between $250 and $750 million, which hedges the downside risk. Moreover, the value tends to increase as sales growth continues to accelerate.

That said, Ocular is at a transformational pivot point. Management still needs to raise more money to advance the pipeline. Overall, Ocular is in a comfortable negotiating position with many business development opportunities coming out of its pipeline. For this reason, I am confident that Ocular will be able to successfully execute a deal and avoid excessive dilution. However, with the tremendous opportunity comes some risk. The path forward, as well as the potential, is highly dependent on this deal. In addition, there is still a long way to go before the clinical development products are approved and proof of concept must be demonstrated in pivotal studies.

The current market cap of $400 million reflects the uncertainty surrounding the unresolved financing. In my opinion, the stock should correct this undervaluation once the funding for the pivotal trials is secured. Personally, I would prefer a partnership outside the US or a cost and revenue sharing partnership. Licensing additional products to leverage the existing sales infrastructure is the riskiest of the options presented. In contrast, selling Dextenza would be the easiest and fastest way to create value.

For further details see:

Next Round Of Financing Will Be Transformational For Ocular Therapeutix