NEP - NextEra Energy Partners: Good Renewable Yieldco But Tight Distribution Coverage

2023-03-22 13:49:58 ET

Summary

- NextEra Energy Partners, LP is one of the few companies that allow investors to gain exposure to the renewable energy sector and earn a respectable yield.

- The company enjoys remarkably stable cash flows over time due to its business model based on power purchase agreements.

- The company has significant forward growth potential, as its parent company continues to construct renewable energy facilities that it can purchase.

- The company has a very reasonable debt load and leverage ratio.

- The company failed to cover its distribution in 2022 and overall has very tight coverage.

NextEra Energy Partners, LP ( NEP ) is a renewable energy yieldco. Admittedly, we do not discuss renewable energy companies very often here at Energy Profits in Dividends, which is mostly because these companies have not offered attractive opportunities for income investors since 2018 or so. In fact, even today they are nowhere near as appealing as traditional fossil fuel companies. This is evident by looking at the partnership units of NextEra Energy Partners, which currently yield 5.15%. While this is not as high as the companies that we normally discuss, I am choosing to open discussion here since the company is one of the only ways to generate a positive real yield from a renewable energy firm. The partnership also has some fairly strong growth prospects, which could ultimately allow it to raise the distribution to the point at which the yield on cost is over 7%.

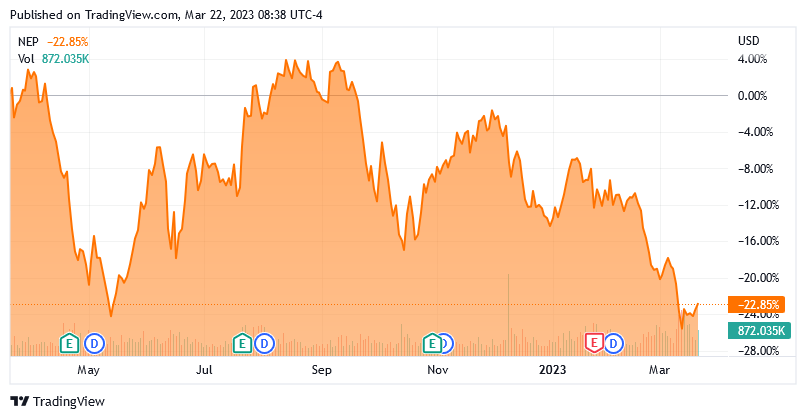

With that said, the company’s attractive yield today is partly due to the company’s very poor performance over the past year. Since last March, NextEra Energy Partners is down 22.85%:

{kind=link}

This is mostly because the entire renewable energy sector was overbought in 2020 and 2021, just like technology and similar sectors. This is what happens when there is too much free money available in the economy, as poor business models tend to get funded and people invest based on ideals instead of on rational thoughts. That all came to an end last year when the Federal Reserve started making it more expensive to borrow money and imposed an opportunity cost on using money, resulting in investors increasingly favoring companies that do generate positive cash flow and profits. The whole renewable energy bubble crashed as a result, which dragged down the partnership units of NextEra Energy Partners.

Fortunately, NextEra Energy Partners does have a sustainable business model and most certainly does generate positive cash flow. As such, the company could make some sense for our portfolios today. Let us investigate further.

About NextEra Energy Partners

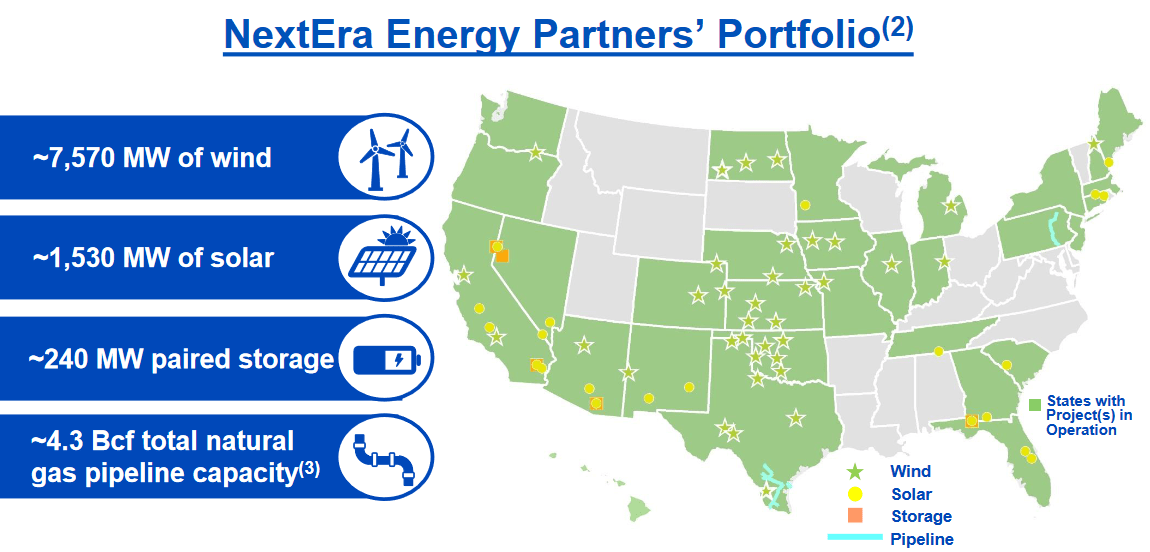

As stated in the introduction, NextEra Energy Partners is a drop-down partnership created by NextEra Energy, Inc. ( NEE ) as a yieldco. Essentially, the company purchases renewable generation facilities from the parent company after they are constructed. As NextEra Energy owns a significant equity stake in NextEra Energy Partners, this essentially allows the company to recoup the capital investment of constructing the generating plant while still getting most of the cash flows that it generates from the distributions paid by NextEra Energy Partners. The partnership currently owns 7.570 gigawatts of wind generation capacity and 1.530 gigawatts of solar generation capacity. Perhaps surprisingly, the partnership also owns a network of natural gas pipelines that are capable of transporting 4.3 billion cubic feet of natural gas per day:

{kind=link}

The presence of the natural gas pipeline system is undoubtedly going to appear to go against NextEra Energy Partners’ promise of being a renewable energy company. However, natural gas is an essential aspect of the energy transition, whether clean energy advocates are willing to admit it or not. As I discussed in a recent blog post , there are some major problems with solar power. In particular, it is unreliable and incredibly expensive. The biggest problem with it is that solar power does not work at night, and it is far less effective on cloudy and rainy days. However, people today are not willing to tolerate that sort of intermittent availability from a modern electric grid. After all, could you imagine not being able to use your television set in the evening during the winter? While batteries have been proposed as a solution to this problem, the technology still needs a significant amount of work before it ever becomes feasible. After all, the largest battery in the world cannot even power a midsized city for an hour.

As such, the usual solution to this is to pair solar power plants with natural gas turbines since natural gas burns much cleaner than any other fossil fuel and it has the reliability needed to ensure that the electric grid remains active at all times. Thus, it is generally considered to be an essential fuel for driving the energy transition. This explains why NextEra Energy Partners owns a network of natural gas pipelines despite being a renewable energy company.

In numerous previous articles, we have discussed how pipeline companies enjoy remarkably stable cash flows over time by virtue of their long-term volume-based contracts. This is true of NextEra Energy Partners’ natural gas pipeline infrastructure as well. Fortunately, the same thing is true of the company’s renewable energy plants, despite the fact that they only generate electricity intermittently. This is because the company sells the electricity that they generate under contracts known as power purchase agreements. A power purchase agreement is a contract under which the customer essentially buys a portion of the total output of a generation facility. For example, NextEra Energy has a news release on its webpage regarding a power purchase agreement that it has with Alphabet Inc. ( GOOG ). The company states the following:

“NextEra Energy Resources, LLC, the competitive energy subsidiary of NextEra Energy, Inc. and North America’s leading generator of wind power announced today that it has entered into a power purchase agreement with Google Energy LLC. Google Energy will purchase 100.8 megawatts of clean, renewable energy from NextEra Energy Resources’ Minco II Wind Energy Center under development in Grady and Caddo Counties in Oklahoma.”

Under the terms of this contract, Alphabet has to pay for that energy even though the wind facility will not be able to generate 100.8 megawatts of electricity at all hours of the day, every day. There are times when the power that Alphabet is actually consuming in its operations comes from other power plants, including fossil fuel-driven power plants, in the electric grid. Basically, this is nothing more than a “feel-good” contract that lets Alphabet brag about its environmental credentials to people that do not understand how the electric grid actually works. However, it ensures that the company’s wind facility will receive steady revenue regardless of what its electrical output actually is during any given period of time. This is the only way to make renewable energy facilities economical due to their intermittent nature. NextEra Energy Partners has similar contracts for the nameplate capacity of all of its power plants, which provides it with a steady source of revenue and cash flow. Obviously, we like companies with steady financial performance because steady cash flow provides a great deal of support for the partnership's distribution.

We can see NextEra Energy Partners’ cash flow stability by looking at its adjusted EBITDA (a proxy for pre-tax cash flow) and cash available for distribution over the past few years:

| FY 2022 |

| FY 2021 |

| FY 2020 |

| Adjusted EBITDA |

| $1,650 |

| $1,360 |

| $1,263 |

| Cash Available For Distribution |

| $634 |

| $584 |

| $570 |

(all figures in millions of U.S. dollars.)

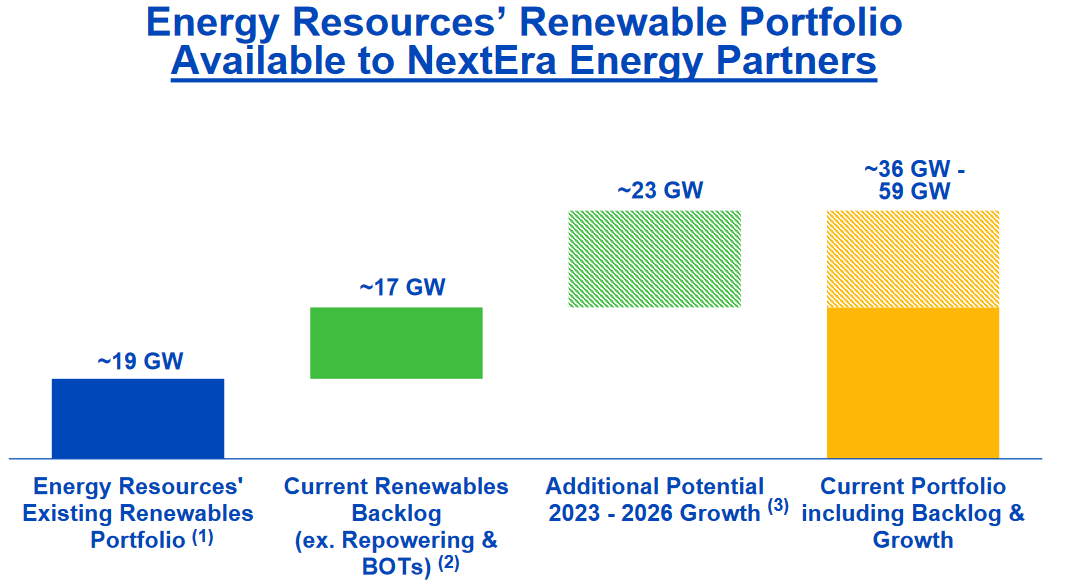

We can also see a great deal of growth here over time. That is fairly typical for companies like this, as NextEra Energy’s business model partly consists of purchasing renewable energy facilities that are constructed by NextEra Energy and managing to secure power purchase agreements. The company notes that there are several facilities that may be eligible to be purchased. Notably, NextEra Energy currently has 19 gigawatts of renewable energy generation capacity in operation that could be purchased by the partnership. The company also has another 17 gigawatts of capacity in various stages of development:

{kind=link}

The addition of new facilities will obviously increase the partnership’s generation capacity and revenue. All it has to do is purchase some of these facilities, although the company has not stated which of these facilities it intends to purchase. The company has stated that it plans to purchase sufficient operating renewable generation capacity to grow its distribution per unit at a 12% to 15% compound annual growth rate over the 2022 to 2026 period:

NextEra Energy Partners

This will require that the company grow its cash available for distribution at a faster rate since it typically needs to issue new partnership units to make acquisitions. Regardless though, NextEra Energy does have a sufficiently large pipeline for the company to accomplish this growth. As I noted in the introduction to this article, someone purchasing units of NextEra Energy Partners today should see their yield on cost quickly increase to the point where they are receiving the 7% yield on the amount of money that they invested, which is our target in this service.

Financial Considerations

It is always critical that we examine the way that a company finances itself before considering an investment in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. As few companies have the ability to completely pay off their debt with cash as it matures, this is usually accomplished by issuing new debt to repay the existing debt. That can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market.

As everyone reading this is no doubt well aware, interest rates in the United States are currently much higher than they were a year ago, so this is a very valid concern today. In addition to this risk, a company must also make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flow to decline can push it into insolvency if it has too much debt. Although NextEra Energy Partners has a fairly stable cash flow due to its business model that is centered around long-term contracts, we should still not ignore this risk.

The usual method that we analyze the debt load of a master limited partnership like NextEra Energy Partners is by looking at its leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how long it would take the company to completely repay its debt if it were to devote all of its pre-tax cash flow to that task. As of December 31, 2022, NextEra Energy Partners had a net debt of $5.0930 billion. The company’s trailing twelve-month adjusted EBITDA was $1.650 billion over the same period. This gives the company a leverage ratio of 3.09x today, which is quite reasonable. Wall Street analysts generally consider anything under 5.0x to be acceptable and sustainable over the long term.

As my regular readers know, though, I am somewhat more conservative and like to see this ratio under 4.0x in order to add a margin of safety to the position. As we can clearly see, NextEra Energy Partners appears to fulfill these requirements. Overall, the company’s debt level should not be a significant risk for us as investors.

Distribution Analysis

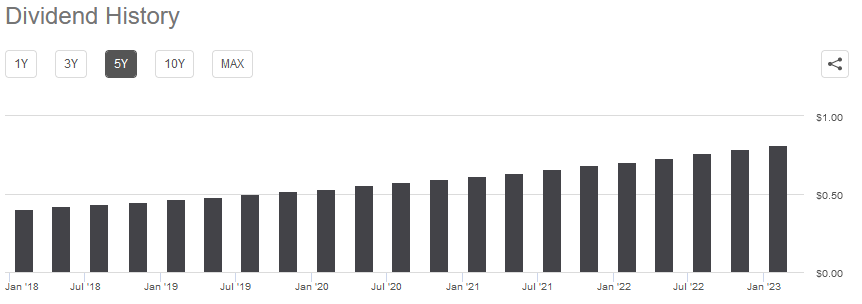

One of the major reasons to purchase partnership units of a yieldco is because of the fairly high yields that these companies typically possess. NextEra Energy Partners is certainly no exception to this as the units yield 5.15% at the current price. That is substantially higher than the 1.62% yield of the S&P 500 (SP500) as well as higher than the 2.53% yield of the U.S. Utilities Index ( IDU ). NextEra Energy Partners also has a very long history of increasing its distribution over time:

{kind=link}

This is a better track record than just about any other yieldco, utility, or master limited partnership. It might be expected though, given the company’s tendency to purchase new renewable generation facilities every quarter. It is also something that is very nice to see in today’s inflationary environment. This is because inflation is constantly reducing the number of goods and services that can be purchased with the distribution that the company pays out. That can obviously make it feel as though we are getting poorer and poorer with the passage of time. The fact that NextEra Energy Partners consistently increases its distribution every quarter, at a faster rate than the current level of inflation, helps to offset this effect and ensures that we are able to maintain our purchasing power over time.

As is always the case though, it is critical to ensure that the company can actually afford the distribution that it pays out. After all, we do not want it to be forced to reverse course and cut the distribution since that would reduce our incomes and almost certainly cause the company’s unit price to decline.

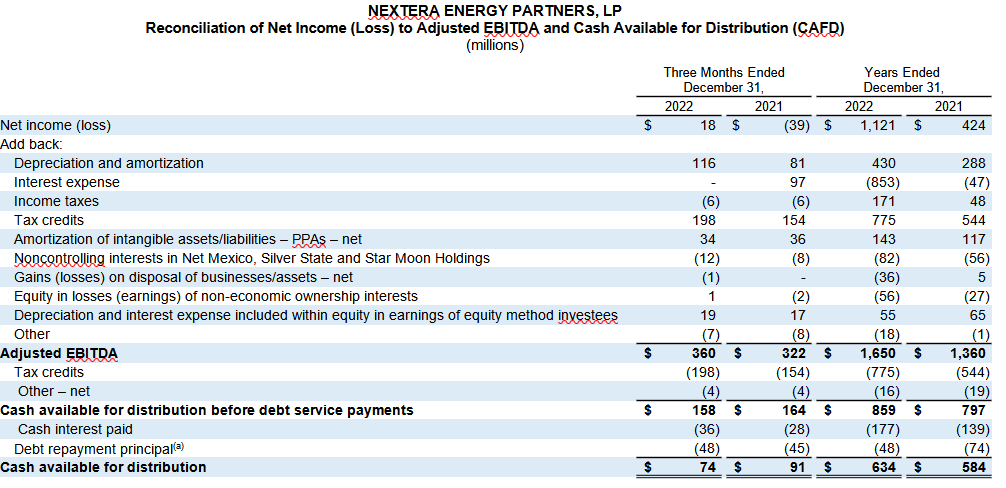

The usual way to determine the ability of a master limited partnership to pay its distributions is by looking at its distributable cash flow. However, NextEra Energy Partners does not report such a figure. Rather, this company reports something that it calls “cash available for distribution.” This is not exactly the same thing as the partnership calculates it as adjusted EBITDA minus taxes and debt service payments. That formula should give us a pretty good idea of the amount of cash that was generated by the company’s operations and is available for distribution though, so it should work pretty well. In the fourth quarter of 2022, NextEra Energy Partners reported cash available for distribution of $74 million. The full-year 2022 figure was $634 million, as shown here:

{kind=link}

As we can clearly see, the full-year 2022 figure was quite a bit higher than the 2021 number, although the company’s quarterly performance was not quite as good. The company paid out $636 million in distributions for the full-year 2022 and $168.0 million in distributions during the fourth quarter of 2022. That is concerning as the company failed to cover its distribution last year. I am not as concerned with the fact that the fourth quarter number was substantially above the company’s available cash for distribution, but the fact that it failed to cover the distribution over the course of the year is quite concerning. It does appear that the company is struggling much more than we really want to see to maintain this distribution so caution may be warranted here.

Conclusion

In conclusion, NextEra Energy Partners, LP is one of the few ways through which an investor can have a position in renewable energy and still generate an acceptable yield. The company’s history of consistent distribution growth is also very appealing, especially when we compare it to most midstream partnerships or pretty much anything else. This is one of the few companies lately that has had sufficient distribution growth to overcome inflation. It also has a very strong pipeline for continuing its growth going forward.

Unfortunately, it also appears that NextEra Energy Partners, LP is struggling to maintain its distribution, as it paid out more cash than it actually had available last year. It may be able to keep that up for a while, but it is not good for long-term distribution sustainability, so we will need to keep watching to see if NextEra Energy Partners, LP can grow its cash flow faster than the distribution going forward and correct this problem.

For further details see:

NextEra Energy Partners: Good Renewable Yieldco But Tight Distribution Coverage