DUK - NextEra Energy Partners: Long-Term Growth Potential Likely

2023-11-21 09:41:18 ET

Summary

- NextEra Energy Partners is a leader in renewable power, with a strong business model and a substantial project pipeline.

- Despite recent stock pressure, NEP is undervalued compared to peers and its historical performance, presenting a buying opportunity.

- NEP's strategic shift towards 100% sustainable energy and recent project acquisitions support its long-term growth potential.

Investment Thesis

NextEra Energy Partners' ( NEP ) leadership position in renewable power, attractive business model, and substantial project pipeline supporting 5-8% annual distribution growth promote solid opportunity. Despite these strengths, NEP units have faced pressure, creating a buying opportunity for long-term investors. I think the stock is undervalued relative to peers and its history, with inflation potentially peaking as a catalyst. NEP's strategic shift towards 100% sustainable energy is detailed as a tailwind, along with recent accretive project acquisitions. The durability of NEP's cash flows from its high-quality clean energy assets backing distribution growth is underscored. Secular demand trends driving the global energy transition are cited as NEP's growth driver for years to come. Ultimately, NEP is exceptionally positioned to deliver market-beating total returns, and that now represents an opportune time for investors to build positions. In my perspective, this is a compelling case promoting a "strong buy" recommendation based on NEP's strengths and depressed valuation.

Introduction

The clean energy revolution is well underway, with solar and wind power rapidly gaining market share as utilities and corporations seek to decarbonize electricity generation. NextEra Energy Partners sits at the epicenter of this seismic shift as the world's largest generator of renewable power from the wind and sun. Formed in 2014 as a subsidiary of industry giant NextEra Energy (NEE), NEP owns and operates contracted clean energy projects with stable, long-term cash flows backed by investment-grade counterparties. With over 10 gigawatts of generating capacity across 30 states and a sizable project pipeline, NEP is exceptionally positioned to capitalize on the accelerating transition to carbon-free sources of electricity.

Despite NEP's strengths as a premier clean energy platform, its stock has faced severe pressure, plunging 40.5% in September 2023 after second-quarter earnings missed estimates on both the top and bottom lines. There has since been a very minimal climb (down 67% YTD) where I believe this sell-off represents a compelling buying opportunity for patient investors, as NEP's long-term growth prospects remain intact. The company expects a 5-8% annual distribution growth through at least 2026, driven by acquisitions and a massive backlog of renewable energy projects (NEP Media Release). With inflation showing signs of peaking and the Federal Reserve potentially nearing the end of its rate hike cycle, NEP offers deep value trading at 5 times forward Price/Cash Flow, nearly -30% compared to the median sector. This article will detail why NEP's depressed valuation sets the stage for potentially enormous returns over a long-term outlook.

Overview of NextEra Energy Partners

Headquartered in Juno Beach, Florida, NEP owns and operates an attractive portfolio of contracted clean energy assets located primarily throughout North America. The company's facilities have a combined generating capacity of 5,622 megawatts ((MW)), making NEP a prominent producer of energy from the wind and sun worldwide. NextEra Energy Partners facilities sell power under long-term contracts known as power purchase agreements (PPAs) averaging 14 years in duration. These predominantly investment-grade PPA counterparties include utilities, municipalities, universities, and corporations with strong credit profiles that ensure stable cash flow visibility. NEP's PPAs have a weighted average remaining contract life of 14 years as well (Q3 earnings transcript).

The partnership owns and operates projects through two primary avenues: acquiring developed clean energy assets from its sponsor NextEra Energy Resources (NEER) and third parties or purchasing newly constructed projects from NEER upon completion. This external growth is funded through debt and equity issuances as well as occasional asset sales. NEP also expands existing projects through repowerings, which involve replacing old turbines with new, upgraded technology to drive higher efficiency and cash flow.

NEP is managed and operated by affiliates of NEER, allowing it to leverage NEER's industry-leading expertise in renewable energy development, construction, and operations. Currently, NEP owns approximately 48.6% of NextEra Energy Operating Partners (NEP OpCo) with NEER retaining a 51.4% stake (NEP 10-Q). This corporate structure provides NEP control over NEP OpCo and its portfolio of energy assets while enabling NEER to retain exposure to NEP's future growth.

Financial Performance and Distributions

In Q3 2023, NEP generated operating revenues of $367 million, a 21% increase over the prior-year period driven by portfolio expansion (Q3 earnings transcript). For the first nine months of 2023 net income attributable to NEP fell 80% to $88 million, primarily due to a tough comparison to exceptionally favorable mark-to-market gains on interest rate hedges in the year-ago period.

Despite earnings volatility stemming partly from non-cash accounting adjustments, NEP's cash flow from operations remained resilient, dipping just 10% to $552 million through the first three quarters of 2022 (NEP earnings results). As of September 30, 2023, NEP's liquidity position stood at a healthy $2.5 billion, providing ample capacity to fund growth investments (NEP 10-Q). The partnership generated Q3 2023 adjusted EBITDA of $488 million and cash available for distribution of $247 million (Q3 earnings transcript).

Critically, NEP has reaffirmed its guidance for 5-8% annual distribution growth through at least 2026. The company expects to increase its Q4 2023 distribution to an annualized rate of $3.52 per unit, paid in February 2024 (Q3 earnings transcript).

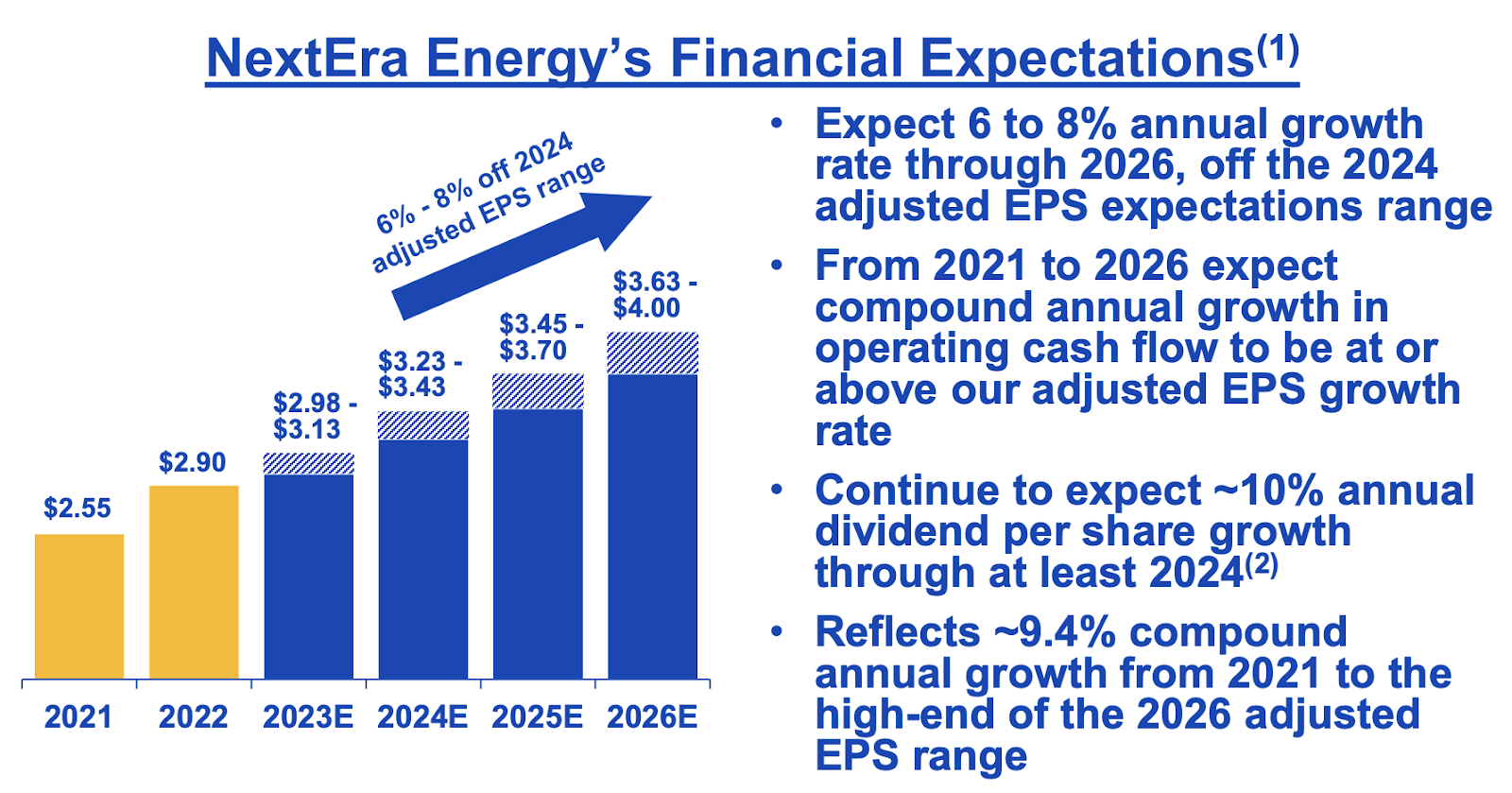

NextEra Financial Expectations (NextEra Energy Partners Q3 Presentation)

{kind=link}

Inflation Relief In Sight

One of the major headwinds facing NEP this year has been rapidly rising interest rates by the Federal Reserve seeking to tame the hottest inflation in four decades. Higher rates increase NEP's cost of capital, which can pressure returns on new renewable energy investments. But the latest consumer price index report showed inflation unchanged in October, raising hopes the Fed's aggressive monetary tightening is finally cooling price increases.

Further evidence arrived when the benchmark 10-year Treasury yield plunged from over 5% in late October to below 4.5% after the inflation data. Lower long-term rates ease pressure on NEP's cost of capital, boosting the profitability of new renewable energy projects it can acquire. With inflation potentially peaking, the Fed could halt its rate hike campaign soon, setting the stage for falling interest rates that would provide a strong tailwind for NEP's distribution growth in 2023 and beyond.

With that, Duke Energy Florida's ( DUK ) recently decided to reduce customer bills in 2024, a strategic move that caters to both new and existing customers. The $11.29 reduction for residential customers using 1,000 kWh symbolizes the company's commitment to affordability. This price decrease not only makes their service more attractive to potential customers, seeking cost-effective energy solutions but also enhances satisfaction among current customers. This could be a ripple effect amongst competing companies, where NEP may adopt this concept, which could be very beneficial.

Strategic Shift Away From Natural Gas

On November 6, NEP announced it had entered a definitive agreement with Kinder Morgan, Inc. in the sale of its Texas natural gas pipeline assets for $1.185 billion. This agreement is a significant part of NextEra's strategic shift, with the anticipated revenue primarily directed towards settling debts and completing equity buyouts. The transaction, slated for completion in early 2024, encompasses seven key pipelines and is a major contributor to the company's EBITDA. The sale's revenue will first address approximately $425 million in associated pipeline debt, followed by fulfilling a $1.1 billion buyout obligation for NEP Renewables II by mid-2025 (NEP Texas Media Release). Any surplus will be allocated to reducing corporate debt. This strategic sale is expected to bolster NextEra's financial stability and enable a consistent 6% yearly increase in partner distribution through 2026, deferring the need for additional growth equity until 2027 (NEP Texas Media Release). Plus, shedding the gas pipelines will allow NEP to focus solely on expanding its core renewable energy business.

As a pure-play clean energy vehicle, NEP anticipates becoming increasingly attractive to ESG-focused investors. This strategic shift will also enable NEP to market itself as a sustainable energy solutions company even more to corporate and utility customers working towards net-zero carbon emissions.

Strategic Acquisitions Driving Growth

NEP plans to repower 740 MW of wind facilities through 2026, a greatly beneficial organic expansion. The company has also actively pursued acquisitions of clean energy facilities from NEER and third parties to enlarge its project portfolio. Most recently in June 2023, NEP acquired a 688 MW portfolio of solar and wind assets located throughout the U.S. from NEER subsidiaries for $566 million (NEP earnings results).

This strategic acquisition included the Montezuma II 78 MW wind farm in California, the 70 MW Chaves County solar facility in New Mexico, the 51 MW Live Oak solar project in Georgia, and four other utility-scale wind and solar plants (NEP earnings results). It aligns with NEP's focus on adding high-quality contracted renewable energy projects to support distribution growth while maintaining strong credit metrics.

According to NEP, the acquired assets are situated in robust markets with enduring demand for low-cost clean electricity. With power purchase agreements averaging 14 years in duration, these facilities will provide NEP with stable, predictable cash flows well into the future. The projects also expand NEP's geographic diversification, reducing its exposure to resource variability in any single region.

Most importantly, the 688 MW portfolio offers significant optionality and upside potential for NEP. The company can optimize the assets over decades of useful life as electricity markets evolve. There is also an opportunity to upgrade equipment and repower facilities in the future to extend cash flow longevity. NEP's latest NEER acquisition demonstrates its external growth strategy in action, as the partnership continues selectively acquiring high-quality clean energy projects with durable cash flows. These types of accretive purchases will enable NEP to steadily expand its portfolio and distribution-paying capacity for years to come.

An Undervalued Clean Energy Leader

NEP offers a visible 5-8% annual distribution growth backed by long-term PPAs, a massive project backlog, and sponsorship by one of America's premier renewable energy companies. Yet after September's pullback, NEP trades at just over 5 times forward estimated cash flow, which is nearly -30% compared to the median sector. This is a significant discount to NEP's historical 5-year average cash flow multiple of 13 times, which is again cheaper than more mature utility peers.

NEP's depressed valuation likely stems from fear of a challenging macro environment with higher interest rates. However, with possible inflation relief on the horizon, NEP's cost of capital could soon improve, catalyzing a re-rating towards its normal cash flow multiple. Additionally, management continues working to enhance NEP's credit profile and cost of capital after this year's turbulence.

The bottom line is NEP offers a compelling opportunity to buy a high-quality clean energy vehicle at a bargain price. As power generation shifts increasingly to renewable sources, NEP's project backlog and development pipeline position it for potentially enormous growth over the next decade and beyond. While short-term headwinds rattled the stock this year, NEP's long-term outlook remains bright. Patient investors could see enormous returns buying NEP units around today's depressed levels.

Risks

The recent downgrade of NextEra Energy Partners by Seaport Global exposes several risks that cast doubt on the partnership's distribution coverage and growth prospects (NEP News Seeking Alpha). Most critically, Seaport predicts NEP's 6% distribution yield will require cutting when it refinances $1.25 billion of debt in 2024 at interest rates exponentially higher than its current 2.5% rate. This projection implies the current payout is potentially unsustainable. NEP's plans to utilize short-term interest rate hedges, its sale of Texas pipelines, and repower older wind projects are viewed, in this firm's eyes, as insufficient to maintain 6% annual growth either.

Adding to the concerns, Seaport flagged questionable accounting practices by NEP's sponsor, NextEra Energy Resources, related to tax equity partnerships that are artificially inflating NEER's earnings. After adjusting for these overstatements, NEP's parent NextEra trades at a steep 41% premium to utility peers based on 2025 earnings estimates, which the analyst finds unjustifiable. Mounting headwinds for another key subsidiary, Florida Power & Light, further tarnish the overall outlook for NextEra.

In summary, NEP faces obstacles to funding growth initiatives, an uncertain distribution outlook, and reliance on a sponsor with inflated finances and deteriorating subsidiary performance. These risks explain the terrible momentum, with NEP shares losing over 40% of their value in the past year. While the pessimism may be overdone, the downgrade highlights significant challenges NEP must overcome to sustain distributions and reward long-term investors. Any further deterioration of NextEra's finances could also have ripple effects on NEP's access to growth capital.

Conclusion

NextEra Energy Partners stands as a premier energy producer. Despite facing macroeconomic challenges throughout the year, NEP retains exceptional long-term growth potential as renewable energy displaces fossil fuel generation. With inflation potentially peaking and low Treasury yields reducing capital costs, I believe the 5-8% annual distribution growth is secure. The strategic shift towards 100% sustainable energy solutions also boosts NEP's appeal to ESG-focused investors. Trading at just 5 times forward cash flow compared to its sector median of over 7 times multiple, NEP offers deep value for long-term investors. As renewable power demand accelerates globally, NEP is exceptionally positioned to deliver market-beating total returns over the next decade and beyond, which I re-emphasize as a "strong buy."

For further details see:

NextEra Energy Partners: Long-Term Growth Potential Likely