NFYEF - NFI Group's Turnaround: A 'Mispriced Gamble'

2023-05-02 10:47:41 ET

Summary

- NFI Group’s balance sheet and operational challenges have brought the share price to a decade low. The company’s problems are significant, widely known, and will likely persist throughout 2023.

- However, the picture isn’t as grim as it might appear at first glance, and the odds of a successful turnaround are much higher than what is priced in.

- The company cannot keep pace with demand due to lingering supply chain challenges, though conditions are improving.

- The vast majority of revenue is derived from government funding (unrelated to the business cycle), of which there is a record amount.

- I see more than 3x possible upside by 2025 with negligible risk of permanent capital impairment.

Editor's note: Seeking Alpha is proud to welcome Luke Emerson as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Remember the movie Speed (1994)? "There's a bomb on a bus. Once the bus goes 50 miles an hour, the bomb is armed. If it drops below 50, it blows up. What do you do? What do you do?"

This quote has surprising relevance: through consolidation and riding industry tailwinds over the last decade, Winnipeg-based NFI Group ( NFYEF , NFI:CA ) quite literally got above 50 (C$50). Now, some would argue, they are in danger of blowing up.

While preparing to write this article, I solicited the opinion of several Canadian buy-side analysts and portfolio managers. The recurring themes in their responses were "too much debt" and "poor results." Only one indicated an interest in looking beyond the cover.

"Sometimes the baggage is so severe and so well known," says David Sambur, Apollo's Co-Head of Private Equity, "that most people don't even bother looking beyond the cover of the book."

The Cover

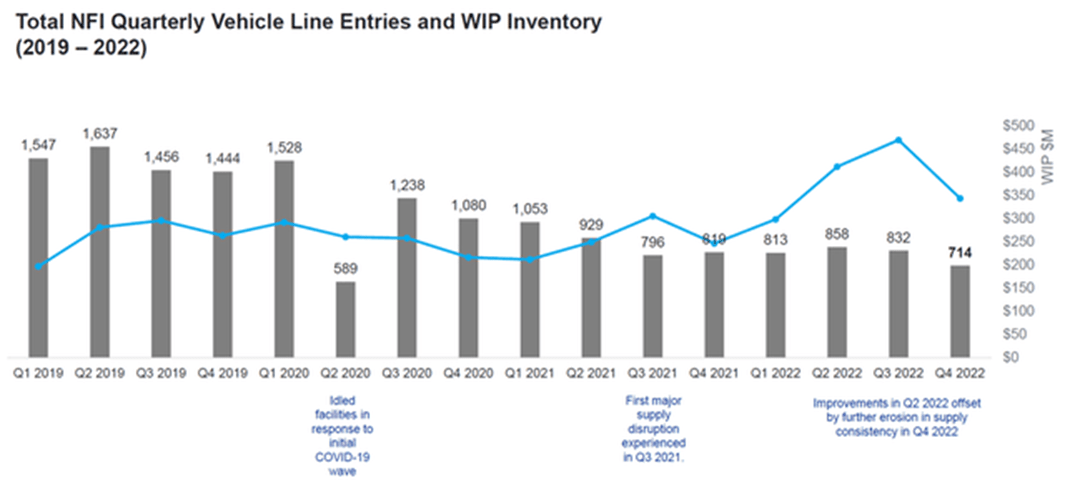

The present picture for NFI is not pretty, having been on the brink of insolvency for over twelve months and only eluding default on account of covenant relief. Although considerably below the 2022 peak, the company still has 19 high-risk suppliers and 71 moderate-risk suppliers.

In some cases, this has required holding 2-3x the typical number of components and has kept work-in-progress ((WIP)) inventory at historical levels: "While it's now starting to come down, we peaked at almost 500 vehicles built, then offline," said CEO, Paul Soubry. "Every one of those vehicles is about half a million dollars, so that's $250 million in cash tied up that we can't complete because we didn't have the parts."

Moreover, the company is still working through "inflation-impacted" orders - which have little to no gross margin - that represent approximately 20% of its backlog.

In early 2023, the Manitoba provincial government and the EDC came to NFI's aid with working capital loans collectively worth $87 million and $100 million for surety and performance bonding requirements from the latter. No doubt this is a positive for the company, but the optics of emergency government funding hardly inspire confidence.

Even with this assistance, considerable uncertainty remains about the terms of the seventh-amended credit agreement expected in June 2023. Without additional waivers, NFI will breach the covenants in place for the third and fourth quarters. Although further relief is near certain, it could very well come at the cost of a painful dilutive secondary offering and/or a wider spread reset.

Beyond The Cover

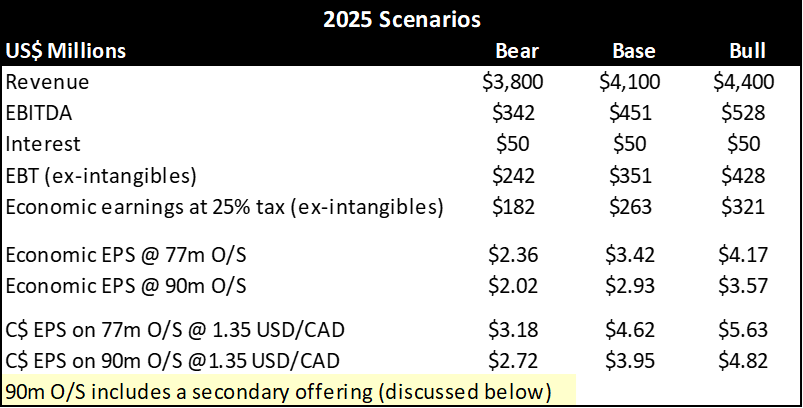

In my view, however, and to stick with the metaphor, this bus is turning around, contrary to the message derived from the decade-low share price. By 2025, we will be looking at a drastically different company, one which has comfortably grown into its over-levered capital structure (~1.5-3x leverage vs ~20x 2023E) and generates north of C$3/share in normalized economic EPS (ex-intangibles).

Although these numbers are a long, long way off 2022 results, I think you'll see by the end of the article that getting there doesn't require mental gymnastics.

{kind=link}

NFI's turnaround is predicated on the following points:

- Management anticipates the supply-chain environment to return to normal in 2023 and that suppliers will be able to support the production ramp in the back half of the year. This will free up some much-needed capital tied up in inventory.

- The industry backdrop is highly encouraging, with record government funding available for transit agencies in key markets, most notably, the 210% increase in transit bus funding as part of the IIJA compared to the FAST Act.

- This has resulted in a record backlog for NFI and a growing percentage of zero-emission bus ((ZEB)) orders, which carry a higher gross profit per unit.

- Recent changes in the competitive landscape have strengthened NFI's hand and should result in a higher market share and improved economics, all else equal.

- NFI's cost structure has improved materially by cutting 2,000 positions and consolidating operations through 25 facility closures. Management noted they would only need to hire an additional 150-200 employees to achieve 2023 guidance. Some, perhaps many, will be former employees, according to the Financial Post : " The way Soubry [CEO] sees things, all the employees who have lost their jobs are going to be hired back once the factory ramps up production "later" in the year."

These factors reveal a path to operating earnings in line with pre-pandemic levels or higher by the end of the forecast period. However, this thesis equally hinges on the extent to which these earnings are sucked back into working capital (a subject we'll return to) and, by extension, how quickly the company can de-lever and grow into its balance sheet.

Secondary Offering

The government loans will cover any liquidity gap that could reasonably be expected in 2023 without the need to draw on the remaining ~$120 million from the secured credit facility. Yet, it would not be surprising to see the banking syndicate push for a secondary offering in exchange for continued covenant relief. If so, the target is most likely to be C$100 - $150 million, in my view. Taking the lower end, at C$7.50/share (~30-day average), translates to 13.3m shares issued, bringing the total to just above 90 million outstanding shares. This is the assumption I have used in my financial model.

Author's estimates

It is important to note that most, if not all, of the lenders in the syndicate (Canadian and US banks as well as North American subsidiaries of international banks), have an interest in maintaining amicable relations with the company on account of future investment and commercial banking fees. It is primarily for this reason that I expect the offering to be at the lower end of the range if one takes place.

Ultimately, what's most important is that creditors have confidence in NFI's turnaround, as its collateral package cannot be easily liquidated. Put differently, NFI's value is in its operations, not its assets.

Financial Projections

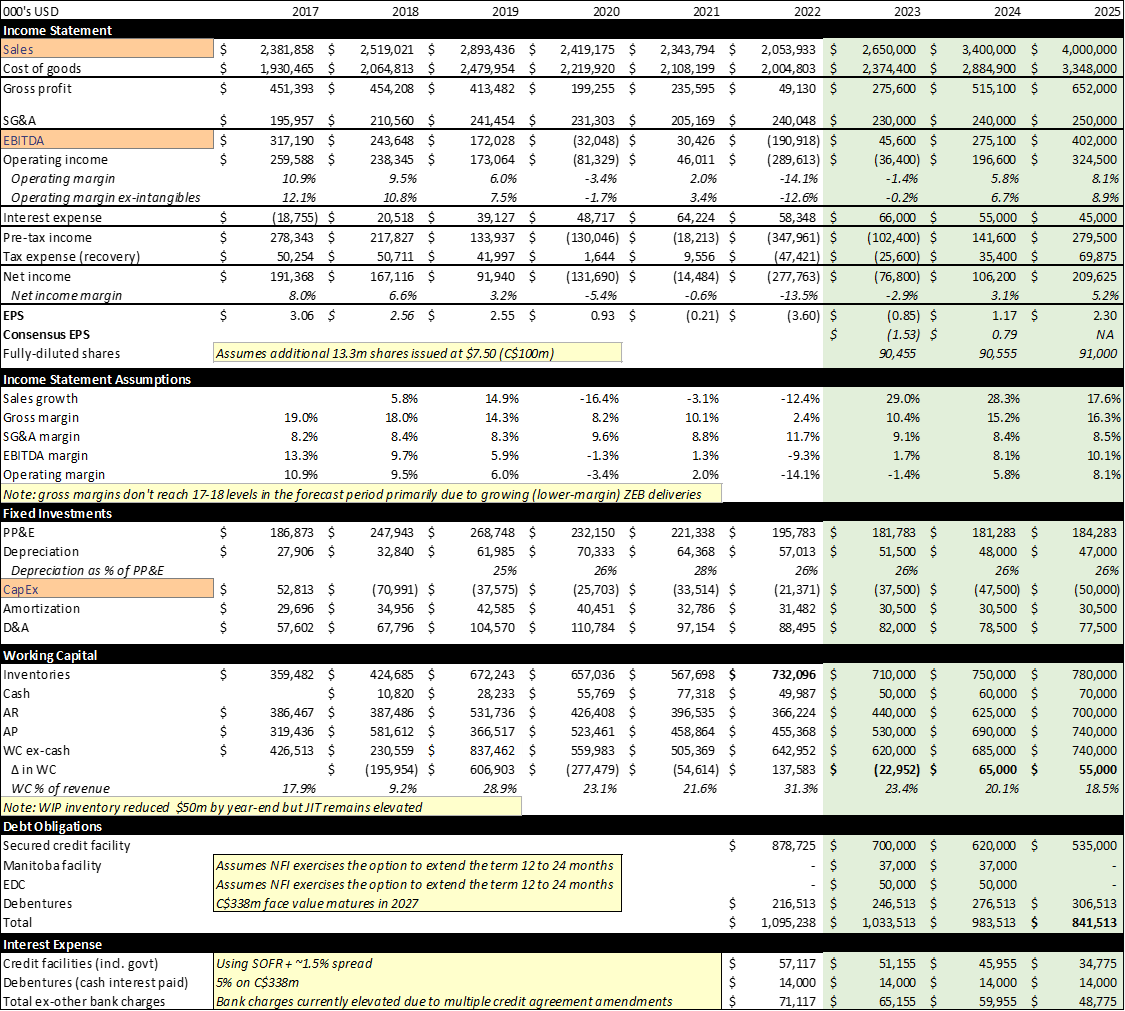

The model below is intended to approximate the financials using the mid-point of management's guidance ( line items highlighted orange).

{kind=link}

Some salient points are worth addressing before taking a closer look at working capital scenarios. The first is that the above projections do not factor in the sale and leasebacks the company is exploring. For example, based on prevailing industry cap rates, NFI could receive $50-$100m in proceeds from selling certain owned facilities, such as the one in Alabama and the two in Winnipeg.

The second point, to address the elephant in the room, is the unreliable nature of management's guidance in recent years. For instance, as late as August of 2021 , management reiterated guidance released on January 11th of that year, even though - as it would be revealed in 2022 - the number of moderate-to-high-risk suppliers jumped from five in the first quarter to 50 in the second (ending June 30th).

"We have confidence in the $220 million to $240 million [adj. EBITDA] today." - Pipasu Soni, CFO, August 4th 2021 , earnings call.

"We just reaffirmed our confidence of the $220 million to $240 million, knowing that the fourth quarter is going to be our strongest quarter of the year. So, at this point, we're feeling we can continue to deliver." - Paul Soubry, CEO, August 4th 2021, earnings call.

Six weeks later, on September 17th, guidance was revised to $165 - $195m. The actual result was $164.2m.

In light of the above, it is reasonable to contend that using guidance as a basis for analysis is unwise. This is why I have spent considerable time deconstructing it and systematically evaluating the merit of the possible assumptions at its core (see below). In doing so, I have concluded that not only is the path to getting there realistic, but it is also widely paved. In other words, unlike previous instances, there is ample room for error.

Moreover, lending this guidance credence is the level of scrutiny to which it is subjected. Per the current credit agreement, the company must provide monthly financial statements and 8-to-13-week delivery and cash flow forecasts to the banking syndicate. Translation: the consequences of over-optimism are far more significant. The obvious implication is that creditors are more likely to remain accommodating if such updates are consistent with guidance and unlikely to be if they aren't.

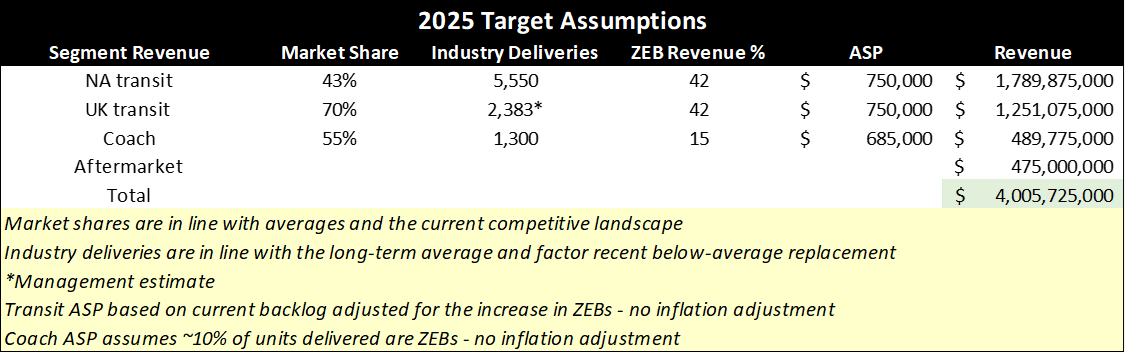

Below is an approximation of what I believe the assumptions are at the center of management's 2025 revenue target.

{kind=link}

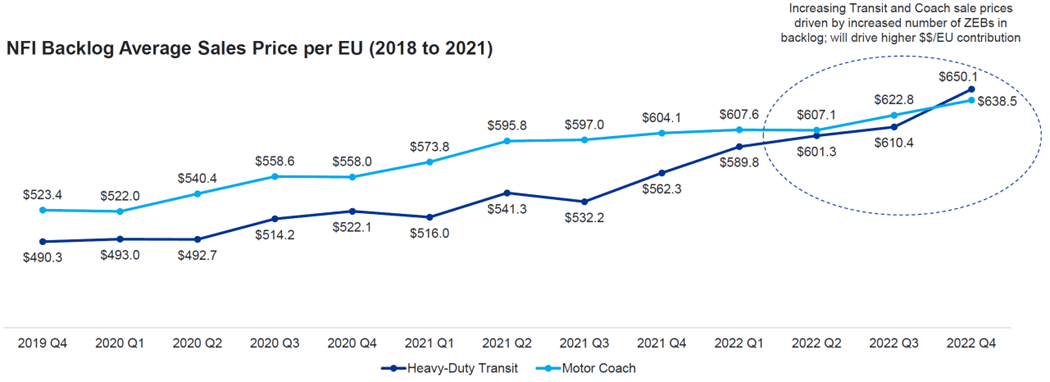

ASPs

NFI does not provide ASP breakdowns by propulsion system, and arriving at ASPs through other sources isn't easy. For example, press releases regarding contract wins rarely include dollar figures. When they do, sometimes isolating the amount attributable to the buses from other project costs is tricky or impossible. Complicating matters further is that "no two buses are the same," as CEO Paul Soubry notes . Due to customizations, a bus ordered from the NYCTA may differ materially from one ordered by the WMATA (Washington).

The most recent and reliable estimate (though there is probably some rounding) for a 40-foot battery-electric bus is US$1.1 million, as reported by the Financial Post in February 2023, which was likely provided by the CEO during his interview for the article. Adjusted for inflation and currency, this maps with OC Transpo's (Ottawa) contract of C$1.3 million per 40-foot battery-electric bus in 2021, as well as other sources .

A clean-diesel bus costs roughly US$500k, based on estimates from the Canadian Urban Transit Research and Innovation Consortium (CUTRIC) and a Canadian think-tank out of a prominent university, adjusted for inflation and currency.

When using these estimates (with the cost of a clean-diesel bus used as a proxy for the cost of "non-ZEB" buses), I arrive at an ASP of $670k. This is close to the $650k reported in the last quarter, in which ZEBs accounted for ~29% of the backlog. The 20% of "inflation-impacted" backlog partly accounts for the difference. However, given that other propulsion systems, like hybrids, are priced somewhere between diesel and battery-electric, one or both of these estimates must be too high.

{kind=link}

Given the discrepancy and the expectation that batteries will gradually become cheaper , I have used a slightly lower ASP estimate of $1.05m for ZEBs. In addition, I have used a $525k non-ZEB ASP to account for other propulsion systems. The above figures, using a 42/58 (ZEB/non-ZEB) split, result in an ASP of $750k in 2025. Below I will explain how I arrived at this split.

ZEB Percentage

The percentage of ZEBs in the coach segment is considerably lower than in transit and likely to remain so for the foreseeable future. Range and charging times are factors, but the primary reason is cost. Unlike battery-electric propulsion systems, hydrogen fuel-cell buses address the first two considerations (with >370-mile range and less than 20 minutes to refuel), but they are very expensive.

Most coach sales are to the private market, consisting of tour/charter operators, inter-city line-haul operators, etc., which are generally less willing or able to double their upfront capital investment for a bus. This is even more difficult when charging infrastructure is required for battery-electric fleets.

This explains why NFI delivered only 20 electric coaches as of March 2022. Although, this number is steadily rising due to the decreasing total cost of ownership ((TCO)) for electric vs. internal combustion engine ((ICE)) buses, which is already near parity. Some argue that electric buses already have a lower TCO, but this depends on several variables. Moreover, charging infrastructure continues to improve. "The pantographs [charging systems] are innovative because they are more efficient than older technology," observed a transit agency director, and they "take a third of the space and cost a third of the price."

Management estimates that ZEBs will account for 40% of total manufacturing revenue by 2025, up from 23% in 2022 and 25-30% in 2023. Given the smaller proportion of ZEBs in the coach segment, it follows that more than 40% of transit revenue must be derived from ZEBs.

Bull Case 2.0

Note that this is not the bull case mentioned earlier, which is more conservative, hence the "2.0". Rather, it is a conceivable path to beating revenue guidance by around 15%. The key differences between this table and the one above include a) higher market share in North America and UK transit, b) 850 additional deliveries across NA transit and coach.

{kind=link}

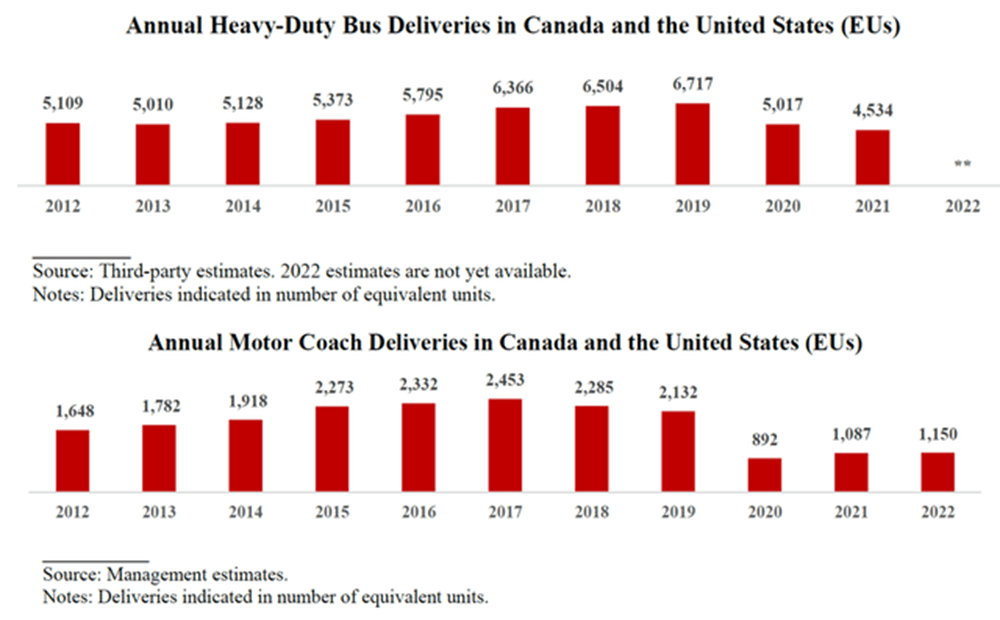

One could argue that NA transit deliveries reach 6,200 or so (bull case 3.0) based on the record level of government funding and below-average replacement in recent years. Note that FTA funding accounts for approximately 80% of total transit funding, with the remainder coming from states and municipalities.

From 2013-2019, there was an average of 2,168 NA coach deliveries, in contrast to 1,043 from 2020-2022. Three years of well-below-average deliveries should lead to some degree of mean reversion, even if there are structural differences behind the decade-low replacement levels. Per NFI's annual information form, private operators typically sell or trade-in motor coaches after 5 to 10 years of ownership in an effort to keep their product "fresh."

{kind=link}

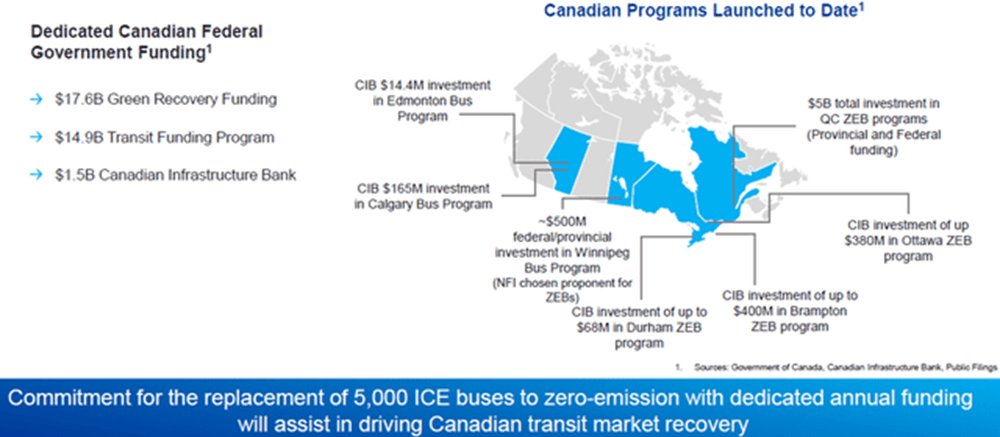

Government Funding Picture (non-US)

The Canadian federal government has committed to replacing 5,000 ICE buses with zero-emission buses by 2026 and providing funding to build the supporting infrastructure. This is incredibly significant, given that funding is primarily generated from local and provincial governments (in contrast to the US funding model).

However, this may be offset somewhat by provinces and local governments reducing available funding due to the increased federal funding. NFI Group is poised to be the primary beneficiary of this fiscal support, not merely through selling more ZEBs, but also through their fleet electrification infrastructure support business.

{kind=link}

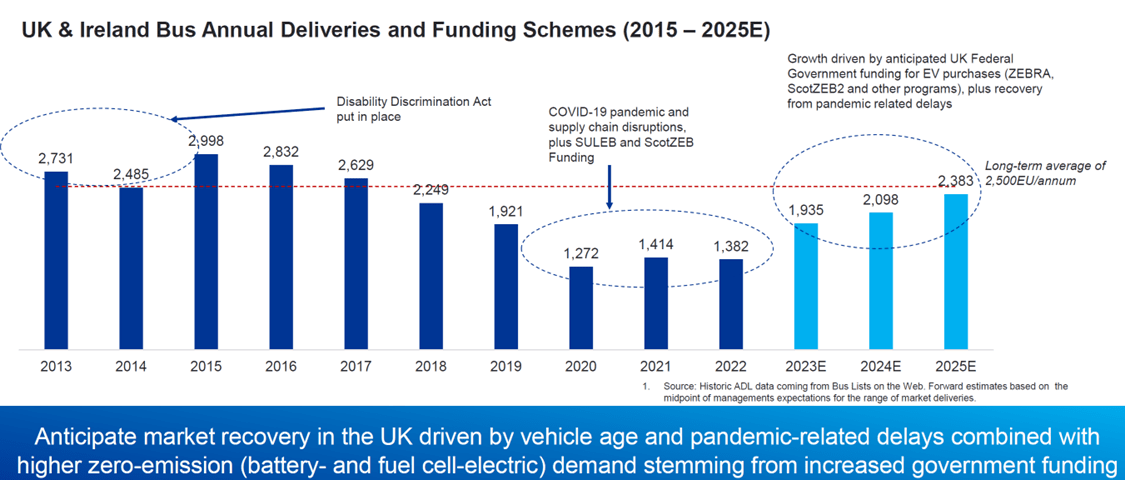

In the UK, private companies with local government contracts dominate the transit market. Historically, there has been no general grant funding for purchasing new buses. However, with the decarbonization agenda taking a more central role in policy, increased government involvement and subsidies are accelerating the shift to ZEBs.

{kind=link}

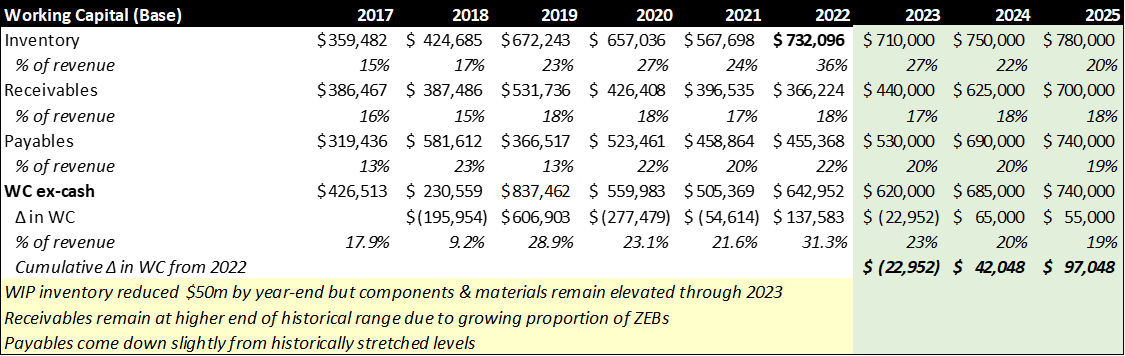

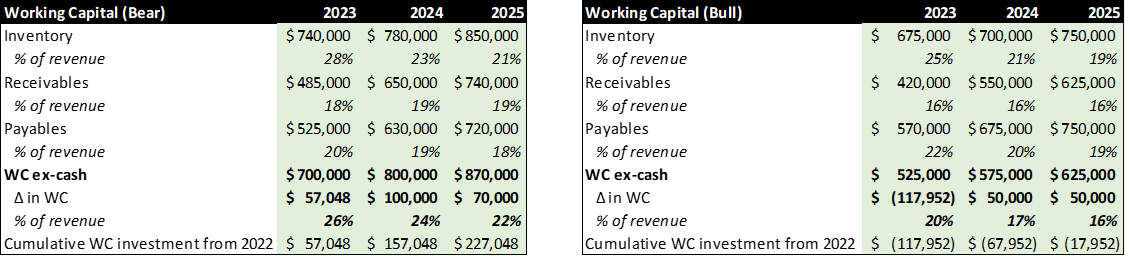

Working Capital

NFI typically receives payment from transit customers 30-40 days after delivery. It is important to note that as ZEBs grow as a percentage of total deliveries, so too will working capital. The reasons are a) ZEBs are considerably more expensive, and b) payment takes longer than other propulsion systems due to a standard 15-day testing window.

Moreover, in some cases, transit agencies withhold a percentage of the purchase price until after some specified reliability period is reached (generally 30 days). The Toronto Transit Commission, for example, increased the amount withheld from 5% to 20% in their latest ZEB procurement contracts .

Author's estimates NFI Q4'22 Presentation

{kind=link}

{kind=link}

I have included the tables below to illustrate how working capital requirements can vary over the forecast period (~$250 million cumulative difference) and, by extension, how quickly leverage can be reduced. Note that "bear" and "bull" scenarios are not synonymous with "worst" and "best."

{kind=link}

Competitive Landscape

There are several themes at play which have effectively removed two competitive threats from key markets. For instance, heightened nationalism and protectionism have all but eliminated Chinese-owned BYD from the North American transit market, a once formidable foe. Then there's the London-headquartered electric vehicle manufacturer Arrival, which looked poised to threaten NFI subsidiary Alexander Dennis' domination of the UK bus market. Setting aside Arrival's major operational issues, which prompted the layoff of half of its workforce, Russia's invasion of Ukraine may have inflicted a mortal wound upon the company's UK transit business, whose founder and majority shareholder is the Russian billionaire Denis Sverdlov.

NFI is the dominant player in the North American transit bus market, with approximately 43% market share, followed by Gillig and Nova Bus (a Volvo subsidiary), each having around 20% market share. The remainder has been split amongst Proterra ( PTRA ), BYD ( BYDDF ), and ElDorado, a REV Group subsidiary ( REVG ). Despite being NFI's largest competitors, Gillig and Nova Bus largely did not participate in the EV pilot programs, which almost exclusively consisted of NFI and Proterra buses.

Proterra, which by 2020, I estimate, had received over 30% of EV bus orders (compared to NFI's ~60%), has since dropped to around ~10%. Proterra's buses have had significant and well-documented reliability issues and are inordinately large relative to the number of buses on the road, likely behind their decline. Moreover, Proterra's cash burn is a concern, and they desperately need to recapitalize. This could very well prompt the liquidation of their transit bus division, with the company instead focusing on charging infrastructure and solutions. These factors have presumably removed Proterra as a serious competitor in the EV bus market.

I joined a meeting recently with NFI's head of IR, Stephen King, in which I asked Andy Grove's famous silver bullet question, "If you had a silver bullet and could take out one competitor, which would it be?" Without hesitation, he responded, "Nova." Unlike Gillig, Nova Bus has won several large contracts in recent years, including 134 hybrid buses (Toronto) and 135 buses ((NYC)), with options for hundreds more. In addition, Nova completed safety testing in September of 2022 for its LFSe+ long-range battery electric bus line, for which trials are ongoing with large transit agencies, including NYC, Washington, and Vancouver.

Nova's sister company, Prevost (also Quebec-based), is NFI's primary competitor in the North American coach market. In the years before the pandemic, NFI's market share was generally in the mid-to-high 40s, while Prevost's share peaked in the low 40s. However, Prevost dropped out of the market for public sector procurement in 2022, leaving NFI the only qualified provider based on Buy America requirements. NFI estimated they had a 74% market share in 2020 of the combined public and private coach market. There have been no market share estimates in 2021 or 2022.

Gillig, which has primarily been successful with smaller transit agencies, has managed through supply chain challenges commendably and was probably the least affected in the industry. This is likely attributable to a more standardized product offering, such as fewer bus sizes, seating configurations, propulsion systems, etc. Gillig has won several small ZEB contracts but has not announced any major wins since 2021. However, they received the highest-ever score for a battery electric bus at the Altoona, PA, testing facility for their 40-foot bus in December 2022.

With over 70% market share, NFI's subsidiary, Alexander Dennis, has only one significant competitor in the UK transit bus market; Wrightbus, which was the first company in the world to produce a double-decker hydrogen bus. In August 2022, it was announced that Wrightbus received the largest-ever UK order of electric buses outside of London to deliver 193 buses to five municipalities. They also won a contract to supply 120 buses to the Republic of Ireland.

NFI's key differentiators are that they offer customers the broadest range of bus sizes, propulsion systems, and customizations (i.e. seat design/layout, number of cameras, camera positioning, doors, window tints, AC capabilities, panel colouring, etc.) and the most extensive aftermarket support.

In addition, the US market is well insulated from foreign competitors thanks to Buy America requirements (70% US content and final assembly must be in the US). At the same time, NFI and Nova Bus have a natural oligopoly in Canada, which also has Canadian content and/or assembly requirements in the largest provinces.

Catalysts

- Generating cash from operations in 2023 (which will likely require a $20 million or greater unwind of working capital).

- Exceeding revenue/earnings, which, presumably, is more likely than missing guidance (based on my reasoning in the "Financial Projections" section.)

- Reaching anything approximating a "normal" supply chain will be a significant positive.

- Favorable terms on the revised credit agreement, including a small or no secondary offering.

- Significant contract wins.

- More colour on the nature of the 800+ buses characterized as "awards pending," which are not yet included in the company's backlog.

It is worth mentioning another possible catalyst. Turtle Creek, an investment manager with over C$5 billion in AUM, recently purchased a >10% stake in NFI Group. Turtle Creek invests in what they describe as "highly intelligent organizations," and they are "looking for companies that are both honest and well run." Thus, it shouldn't be surprising that they don't have a history of shareholder activism.

However, they don't strike me as a firm that is afraid of a brawl if that's the most expedient path to unlock shareholder value. Although their position size is small relative to their AUM, I don't expect they will remain a quiet spectator if they think the business is being mismanaged.

Moreover, NFI's long-time chairman is retiring after 17 years at the company. He is set to be replaced at the AGM by director Wendy Kei, who joined the board in 2022. This is apt to change the boardroom dynamic considerably. What I am getting at here is not that a leadership change is likely or even necessary, only that if it were, it is arguably much more likely now than at any other point in the company's recent history. If so, I would wager that this would be a positive for the stock, even if such a change doesn't leave the company better off operationally.

Risks

- Unfavorable terms on the revised credit agreement. For instance, if a secondary offering is required and above the range contemplated earlier. Although this would reduce leverage by a corresponding amount, it would considerably decrease the long-term upside potential.

- Supply chain improvement doesn't materialize in 2023 or even worsens.

- Higher than expected wage inflation associated with production ramp.

- Current backlog or future orders don't have the appropriate inflation indexing.

- Product recalls.

- A significant economic contraction, which would primarily impact the private coach business.

If one or more of the above risk factors occur (particularly the first two), this will cause a re-evaluation of the thesis.

Conclusion

By 2025, NFI's leverage ratio is apt to come down to a fraction of its current level. Moreover, I expect they will generate C$3 - $5/share in economic EPS (ex-intangibles), with C$3 looking like a reasonable floor in the ensuing years, even with the possible dilution in 2023. Although there is mark-to-market risk, particularly in the near term, the risk of permanent capital impairment is very low.

If NFI meets or exceeds current guidance, it is reasonable to expect a share price higher than $20 by the end of the forecast period. In other words, the upside potential is greater than 3x, while the downside is limited. Thus, NFI strikes me as what Charlie Munger would call a "mispriced gamble."

"We're looking for mispriced gambles; that is what investing is. We're looking for something with 2-to-1 odds that pays 3-to-1." - Charlie Munger, Poor Charlie's Almanac.

For further details see:

NFI Group's Turnaround: A 'Mispriced Gamble'