NFJ - NFJ: Deep Discount Looking Attractive

2023-12-19 10:49:08 ET

Summary

- NFJ is a hybrid fund that invests in equity and convertible securities; in addition, the fund employs a covered call strategy.

- The fund's historical performance has been lackluster, but it is currently trading at a wide discount that could make it more tempting.

- The fund pays a very reasonable distribution yield, and there is potential for a boost in the future or possibly a special.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Earlier this year, we covered the Virtus Dividend, Interest & Premium Strategy Fund ( NFJ ). In some places, you may continue to see the name incorrectly include "AllianzGI," as this was formerly a part of that investment firm before their U.S. ban and transferring over to Voya. A worthwhile reminder is that there wasn't any fraud with this particular fund, nor were any of their closed-end funds caught up in the fraud. The funds that were involved have been shuttered.

NFJ is a hybrid that allows for some flexibility in how and where it invests. It incorporates a mostly equity portfolio but also provides a sleeve of convertibles. Additionally, the fund employs a covered call strategy in an attempt to enhance its distributable earnings power. The fund tilts toward a more value-heavy portfolio and employs no leverage in the form of borrowings.

The historical performance of the fund has been fairly lackluster, but if it has one major selling point, it would be the fund's discount on where the share price is trading relative to its net asset value per share. Not only is it a wide discount on an absolute basis, but also on a relative basis, it is also looking quite wide.

In fact, since our earlier coverage , the fund has provided fairly respectable total return results, but the discount has actually widened even further. Had that not been the case, the fund's total return results would have been a bit better. So what looked like a relatively attractive discount previously became even more tempting at this time.

NFJ Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -1.77

- Discount: -15.89%

- Distribution Yield: 8.01%

- Expense Ratio: 1.07%

- Leverage: N/A

- Managed Assets: $1.370 billion

- Structure: Perpetual

NFJ's investment objective is "to seek current income and gains, with long-term capital appreciation as a secondary objective." To achieve this, the fund will "invest approximately 75% of its total assets in equity securities and approximately 25% in convertible securities." They will then "employ an option strategy of writing covered call options on equity securities held in the fund."

The fund's expense ratio is listed at 1.07%, but with "contractual expense reimbursements" to February 2024, the expense ratio is a tad lower at 0.96%. However, against peers, the fund's expense ratio is fairly average in the closed-end fund space.

Attractive Discount, But Track Record Leaves Questions

Finding an exact peer for this fund is fairly difficult. Not because there aren't other equity and convertible funds to look at, but with this mix and also employing a covered call strategy, it is the more difficult part. The fund lists its benchmark as a weight of 75% to the Russell 1000 Value and 25% ICE BofA U.S. Convertibles Index.

The first fund that comes to my mind would be the Calamos Strategic Total Return Fund ( CSQ ), which would be somewhat close. However, that's a leveraged fund and employs no specific focus on writing options. Though the fund also sports a similar weighting to equity and convertibles, it carries with it an additional sleeve of high-yield bonds as well as a tech-oriented lean.

That said, over the long term, CSQ blew NFJ away in terms of performance, with a key reason presumable being the leverage the fund employs and the value-oriented approach of NFJ in its equity sleeve. Most of this period had the market in a bull mode that treated tech well, aside from the notable Covid crash and weakness we saw in 2022.

Ycharts

Speaking of 2022, the downturn year should have resulted in NFJ showing its more defensive nature. Unfortunately, that did not happen, at least not in a meaningful manner, for the fund as it simply fell nearly as much as the leveraged CSQ peer-esque fund.

Ycharts

Even if the covered call strategy is limited to a partial overwrite of their portfolio and it isn't always the most defensive strategy, admittedly, the value-oriented portion of the portfolio should have performed better. During this period, I really did initially believe that NFJ would have provided materially better results.

Next, we can take a look at how the BlackRock Enhanced Equity Dividend Trust ( BDJ ) performed against NFJ, which I recently covered . To be clear, BDJ isn't a great peer because there are material differences, but for illustration purposes to provide some context, it can still be appropriate.

As a reminder, BDJ also has the Russell 1000 Value Index built in as its benchmark and that makes the fund lean toward a more value-oriented approach. However, BDJ does not incorporate any sleeve of convertibles and is a simple equity fund.

With those caveats out of the way, here's a look at the total returns for 2022, a down year where defensive funds should have performed better. And indeed, that's exactly what we saw from BDJ.

Ycharts

Finally, one last angle we could compare NFJ's performance to would be via creating some context of performance relative to some actual investable ETFs. We can look at the iShares Russell 1000 Value ETF ( IWD ) and iShares Convertible Bond ETF ( ICVT ) to illustrate long-term performance. Ideally, NFJ's performance would be somewhere in the middle of these two. ICVT was launched in mid-2015, so that's where the max charting starts and takes us to today.

Ycharts

NFJ here underperforms significantly, but that, too, could be fairly expected because of the covered call-writing strategy. To be fair, NFJ in the last 1-year period looks much more promising. Perhaps it was the seventh portfolio manager, Ethan Turner, who was added to the team in 2023.

Ycharts

Overall, this is why I believe one of the main selling points of NFJ is the fund's discount. Clearly, it isn't the fund's performance track record.

On the discount front, the fund is looking quite tempting here. The fund is trading below its 1, 3, and 5-year average discount levels as well as its longer-term decade-long average discount shown in the chart below. In fact, aside from the Covid crash, the fund's discount is about as wide as it has ever been, reaching a nearly 16% discount level.

Ycharts

Reasonable Distribution With Chance For Boost

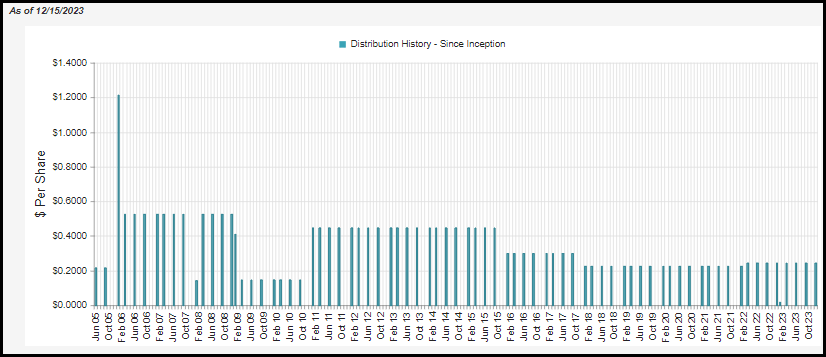

The fund pays a quarterly distribution, which is unappealing to some income-focused investors. However, for investors that don't mind, this could be a potential catalyst going forward as the current level looks reasonable and even has the potential for a boost, in my opinion.

While the fund has historically adjusted the payout as needed, they've maintained the current rate for a fairly lengthy period of time at this point.

{kind=link}

This currently works out to around 8%, but on a NAV basis, the fund's distribution rate comes to 6.74%. If the market can keep up its current momentum or even stabilize around these levels, that could suggest NFJ has room for a boost, or at the very least, a cut doesn't seem likely.

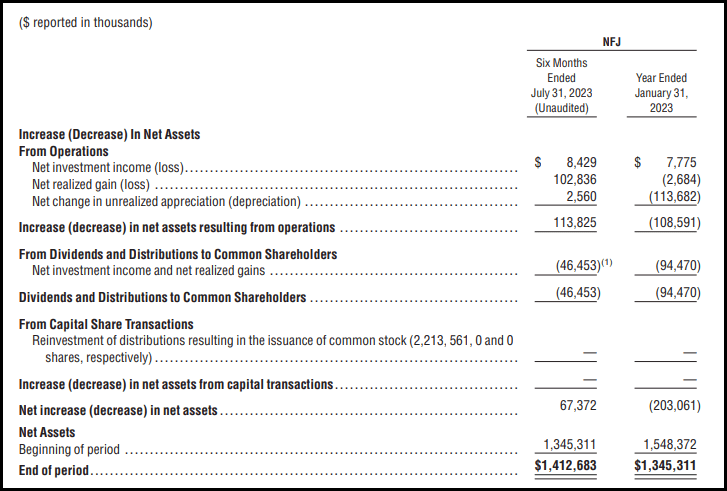

The fund relies significantly on capital gains to fund its distribution. However, that's not unlike any other mostly equity fund. Net investment income coverage for this fund in their prior six-month semi-annual report comes in at 18.15%. That said, the NAV rate is on the low end relative to other call-writing funds and equity/convertible funds.

{kind=link}

In the six-month period above, there was no problem realizing gains from its portfolio to cover the distribution. It is actually at the point where it almost looks like a special distribution could be in the cards at some point. That is unless they realize losses somewhere in their portfolio through the second half of the year to offset these sizable realized gains.

We previously discussed the tax character of the fund's distributions; 2023's official tax classifications won't be known until the start of 2024.

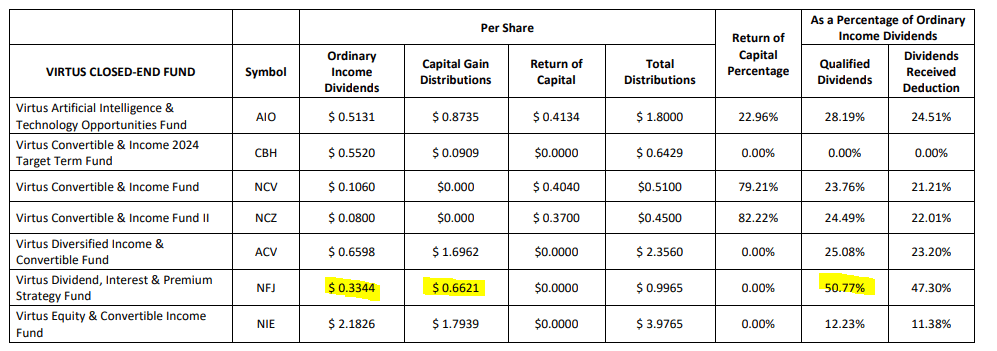

For tax purposes in 2022, the fund was fairly tax-friendly. The majority of the distribution was identified as long-term capital gains or qualified dividends. However, there was still about half of the fund's ordinary income being taxed at ordinary income rates.

NFJ Distribution Tax Classification 2022 (Virtus (highlights from author))

{kind=link}

NFJ's Portfolio

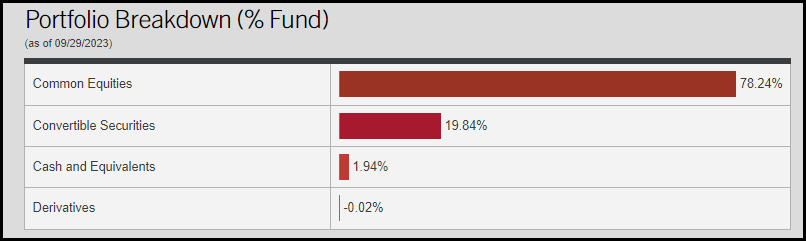

As expected, due to the fund's investment policy, the fund's overall asset allocation of equity/convertibles has been fairly stable since our prior update. In our prior update, we were looking at the weighting as of 12/30/2022, which put the equity sleeve at 75.98% and convertibles at 21.90%.

{kind=link}

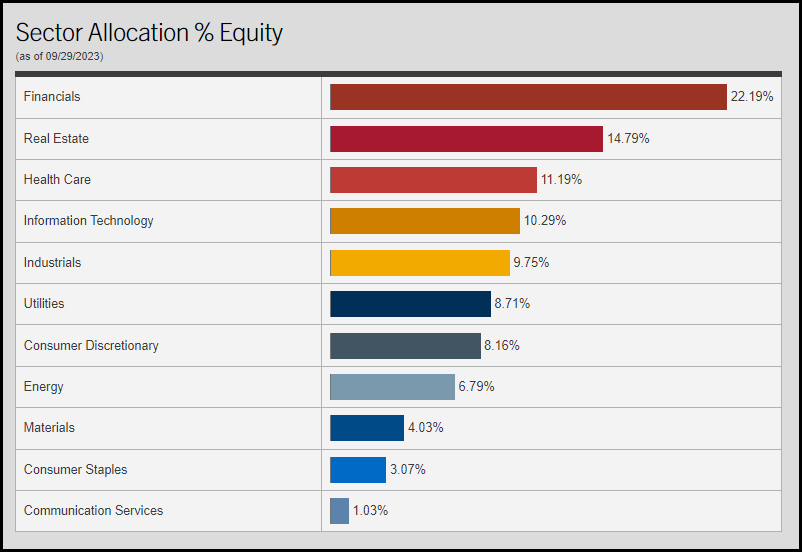

When looking at the fund's equity sector allocation, we see that the shift was fairly dramatic there. Given their benchmark of the value-oriented Russell 1000 Value Index, the below seems to make more sense than where the fund was positioned previously. Here, financials are the largest weighting by far. However, if we look back at our previous update, tech was the largest weighting at a 22.43% allocation for their equity sleeve.

{kind=link}

Given that the tech allocation was much higher in 2022, it could start to make sense why we didn't get that value-oriented defensive lift as we saw with BDJ. After all, CEFs are touted due to their active management, and they don't passively track an index; they merely use indexes for some relevant context to benchmark performance.

Further, real estate has seen a significant ramp-up in terms of its weighting for the fund from its prior 5.3% weight. It has now come to a sizeable allocation, and perhaps it is at the right time as rates are set to be cut by the Fed. That could have perhaps been one of the reasons why we saw better performance in the last year, with the fund, more specifically, ramping up against value-oriented IWD and convertible ICVT ETFs in the last couple of months.

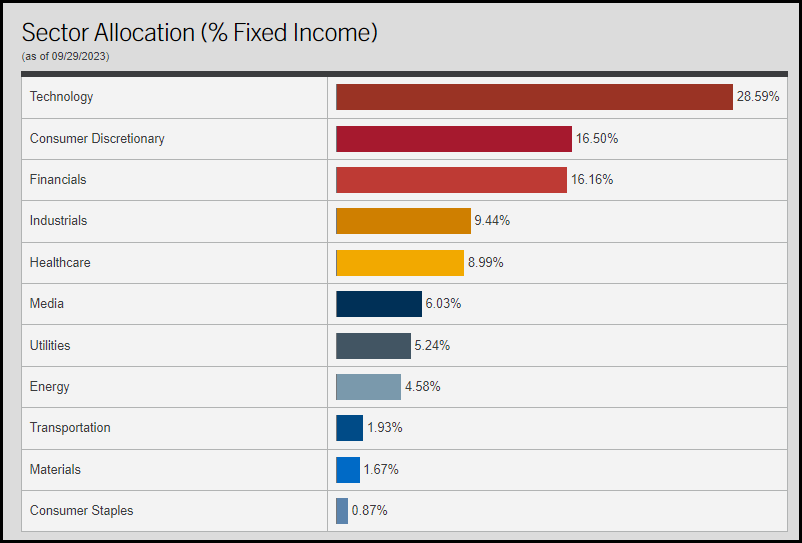

Looking back at the fixed-income sleeve, it had also favored tech at the end of 2022. As of their last quarterly update, that remains the same; however, it has become an even larger concentration as the fund had previously listed a 22.21% allocation there. Healthcare was the second largest sector weighting for the convertible sleeve at 21.15%. Healthcare's weighting has since fallen to the fifth largest weighting, coming in at just a hair under 9% now.

{kind=link}

The portfolio's turnover in their last six-month report came to 64%, which puts it on pace to have more than doubled the turnover of fiscal 2023's 60%. Additionally, it would more than double the fiscal 2022 turnover of 63%. It even would be greater than fiscal 2021's turnover rate, which came to a fairly high 104%. So, the fund had been much more active in the calendar year 2023, relative to what it has been in the prior couple of years, but it's an overall fairly active fund.

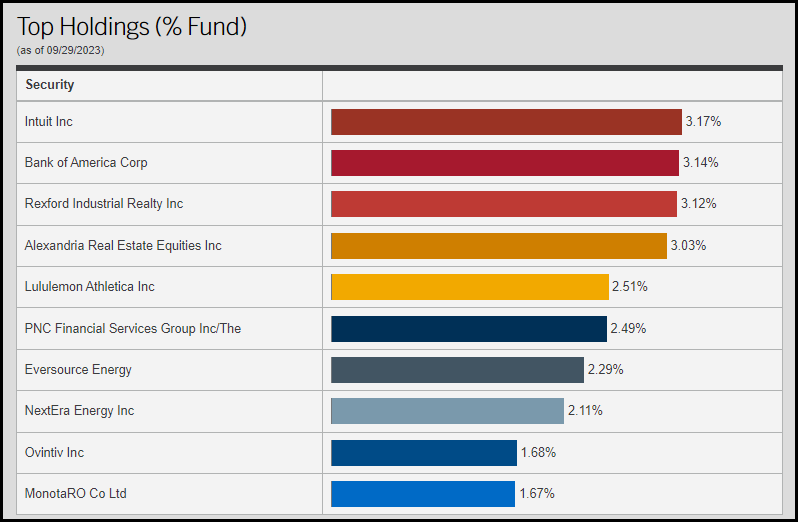

With the material shifts seen in the fund's sector weightings, particularly on the equity side, that is reflected in the fund's top ten holdings.

{kind=link}

Intuit ( INTU ), Rexford Industrial Realty ( REXR ), Alexandria Real Estate Equities ( ARE ), Lululemon Athletica ( LULU ), PNC Financial Services Group ( PNC ), Eversource ( ES ), NextEra Energy ( NEE ), Ovintiv ( OVV ) and MonotaRO ( OTCPK:MONOY ) are all new names to the top ten.

In fact, it would be easier to mention that Bank of America ( BAC ) is the only position in the top ten now that was also in the top ten last December 2022. That just wouldn't be as dramatic, though.

REXR and ARE are REIT investments, which are indicative of the fund's slight shift to more real estate exposure. At the same time, the fund had been holding Digital Realty Trust ( DLR ) previously as a top ten holding. DLR actually doesn't appear in the entire holding list at all anymore as of the end of November 2023 . In that more recent listing, BAC has actually climbed to the largest position. ARE has also climbed to become the second-largest allocation. Both BAC and ARE edged out INTU to push that holding down to the third largest holding.

Conclusion

The fund's track record leaves a lot to be desired from this fund, which really never performed well in the long term or when it would have been expected to perform better. However, the way they were positioned seems to have played a significant role in that outcome when thinking about 2022 more specifically and the poor results experienced. Given that being the case, this fund seems a bit more active than most in trying to position itself appropriately for a given period. They just haven't gotten it quite right yet, and future results will depend on their timing going forward.

All this said the deep discount here presents an opportunity for some possible downside cushion. It can also act as a potential catalyst for a fund that can deliver some upside returns even if the mediocre performance continues. A distribution bump or a special could be a possible trigger to get that catalyst kicked off.

For further details see:

NFJ: Deep Discount Looking Attractive