NGE - NGE: Nigerian Stocks Offer A High Potential IRR But Not Without Risk

Summary

- NGE offers a high IRR in nominal terms.

- Meanwhile, FX risk should in theory be limited.

- However, in more practical terms, the nature of NGE is high-risk; equity risk premiums and the apparent FX risk premium are high.

- NGE is somewhat alluring, but I do not think that the high potential IRR is without risk; any allocation should therefore be modest.

- Given that the fund is trading around fair value, I would take a neutral stance in any case.

Global X MSCI Nigeria ETF ( NGE ) is an exchange-traded fund that provides investors with exposure to Nigerian stocks. I have covered NGE in the past, most recently in May 2021 . Before that, I was bearish, and I was "correct" in terms of its subsequent under-performance. It has been some time since May 2021; I was neutral, and apparently correct to be so, as in spite of strong year-to-date performance in 2023 it has declined -14.77% on a total return basis since. It has fallen by -27.48% on a price-only basis, as compared to the S&P 500's move of -1.90% over the same time period (per data from Seeking Alpha).

Nigeria is demographically interesting as a nation and is likely to grow prominently over the next 50-100 years. However, that alone does not make its stock market particularly interesting. Until NGE is able to accumulate positions in more interesting and higher-growth-potential companies, NGE will remain uninteresting, except perhaps on a valuation basis from time to time. Otherwise, NGE's future is purely speculative, if one is assuming that the fund will begin to include, say, technology companies, or consumer discretionary. Currently, the largest sector exposures remain in "stodgy" sectors. The largest is Financial Services at over half of the fund as of recent.

Morningstar.com

The expense ratio is hefty too: as reported , it is 0.91%. Assets under management are unsurprisingly low, at just $41.29 million. Net fund flows over the past year have been essentially flat . NGE is not popular at all.

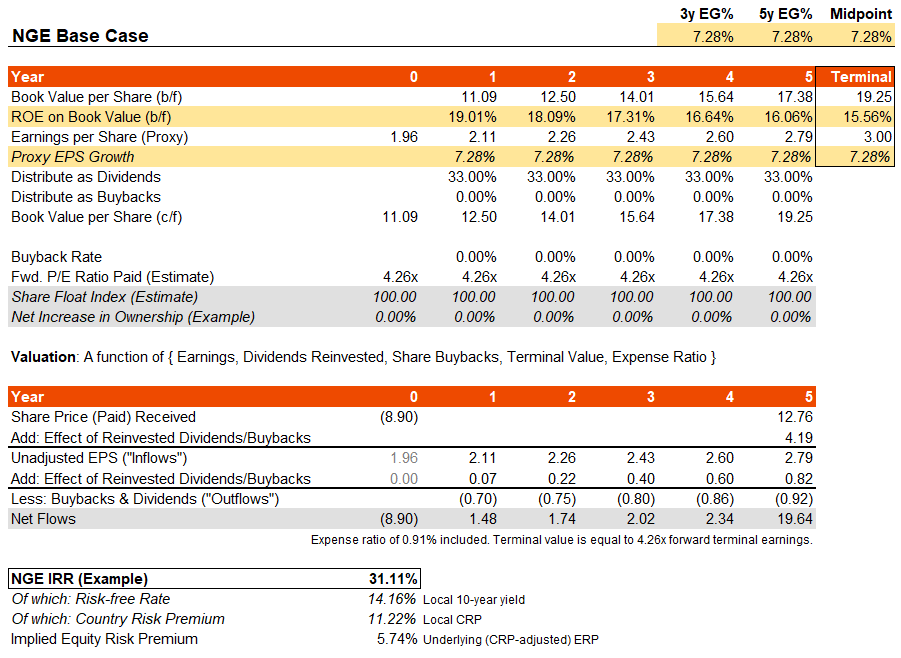

The fund seeks to track the performance of its chosen benchmark index, the MSCI All Nigeria Select 25/50 Index. The capped index offers financial data as at the end of January 2023 in its most recent factsheet. The data can serve as a proxy for NGE's position. The trailing and forward price/earnings ratios were 4.57x and 4.26x, respectively, with a price/book ratio of 0.81x. The dividend yield was 7.22%. While Morningstar offer a generous forward average earnings growth rate of over 15% (over three to five years), the forward one-year earnings growth rate projected by MSCI is 7.28%.

If I assume a constant 7.28% growth rate through to the final year in my base forecast, and a constantly "cheap" earnings multiple, the implied IRR is high at over 30%. That is, apparently, sub-consensus from the standpoint of my projected earnings growth rate (vs. Morningstar's >15%). This is only for illustrative purposes, but my calculation on this basis takes our portfolio return on equity down from about 19% on a forward one-year basis to about 15.5% by year six (my terminal year), which actually seems quite sensible (we are basically assuming the portfolio "matures" into a lower ROE by year six).

{kind=link}

There we have a "super-high" IRR of over 30%, but given high local interest rates (the Nigerian 10-year yield is over 14% at present) and a high country risk premium (based on a recommendation from Professor Damodaran ) of over 11%, means that our underlying CRP-adjusted equity risk premium is about 5.74%. That is a bit higher than what I would expect as a ceiling of 5.5%, but it is roughly in line with what I would expect. NGE offers a high potential IRR in nominal terms, assuming fixed FX rates, but is only modestly undervalued (actually probably fairly valued) based on my arbitrary circa 7% earnings growth rate assumption.

NGE has risen by over 20% year-to-date, at the time of writing. The hefty IRR and the apparent uncertainty surrounding various key inputs here, including earnings growth rates, risk-free rates, and the local equity risk premium, makes NGE a potentially volatile instrument. The fund's beta is reported as being 0.60x by Yahoo! Finance , but that is mostly owing to low liquidity/interest in the fund, and therefore the 'country risk premium' approach from Damodaran is a better input to use to account for the ETF's idiosyncratic risk .

Nigeria's currency, the naira, has depreciated against the U.S. dollar fairly consistently over time. Meanwhile, the country's risk-free rates are much higher than in the developed world (which is a positive for the currency, conventionally speaking) while the country's current account looks fairly stable and positive (suggesting potentially modest under-valuation).

TradingEconomics.com

In spite of a positive current account, the naira has continued to depreciate. PPP models for NGN (the naira) are not widely available, however I can compare the cost of living in the United States and Nigeria , and estimate that it is possible to justify that the Nigerian naira is trading at a steep discount of circa -50%. However, that is without making adjustments for the relative wealth in these countries. Still, following a similar logic to The Economist's Big Mac Index (its GDP-per-capita adjusted model), the naira is probably still trading at a -40% discount. I would put this down to another case of a heavy country risk premium embedded.

Into the next business cycle it is possible that NGE will trade higher, and that there may be some FX tailwinds as a potential upside factor too. Having said that, Nigeria still ranks very poorly on political risk / stability indexes, and so I wouldn't count on seeing the country risk premium (per equity risk) nor the FX risk premium get squeezed/tightened any time soon. NGE has an uninteresting underlying portfolio, is probably fairly valued, and yet offers a nominally high IRR potential. I would remain neutral given the uncertainty, but I would estimate a volatile future for NGE, and a continually waxing and waning level of interest (though remaining nominally low in interest, in terms of assets under management).

I think NGE could perform very well, as ultimately you would (hopefully) expect to be compensated for the level of risk involved. However, I personally would not feel safe putting my money into the fund. If you are investing in NGE, it would be wise to limit your allocation to only a small percentage of your overall portfolio.

For further details see:

NGE: Nigerian Stocks Offer A High Potential IRR But Not Without Risk