NGL - NGL Energy: Darkest Before The Dawn

Summary

- Back in late 2022, it was not looking good for NGL Energy which was struggling to deleverage.

- At the time, I feared too much damage was done with too little progress made but excitingly, perhaps it was merely darkest before the dawn.

- Fast forward to the present day and they have surprised investors with improved financial performance that sees higher guidance.

- Plus, they have finally reduced net debt and expect to reach their leverage target after the current fiscal quarter ends.

- Whilst much more work is left regarding their unpaid preferred distributions, I still believe that upgrading to a buy rating is now appropriate.

Introduction

The last two years have been painful for NGL Energy Partners ( NGL ) and their unitholders, especially because after struggling to deleverage and begin catching up on their unpaid but still accruing preferred distributions, it was sadly looking as though too much damage was done with too little progress made, as my previous article expressed. Fast forward to the present day and perhaps it was merely darkest before the dawn, as brightness returns on the horizon following their improved financial performance that if sustained, may facilitate a full recovery in the coming years.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

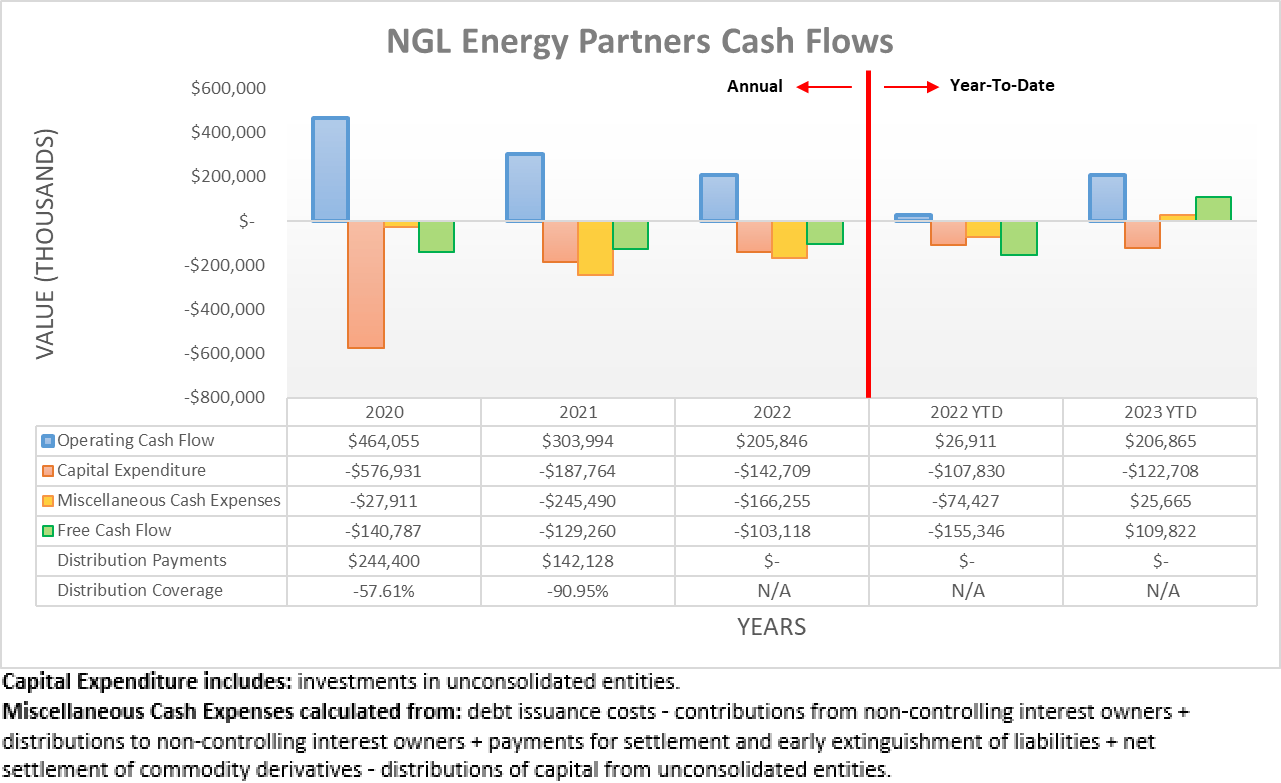

When conducting the previous analysis, much of their problems stemmed from their disappointing cash flow performance that caused a lack of progress deleveraging and thus formed the "too little progress" part of my previous analysis. Thankfully, this dramatically improved during the third quarter of their fiscal year 2023 with their operating cash flow climbing to $206.9m during the first nine months, which marks a massive improvement from their result of negative $31.7m during the first half. This finally sees free cash flow hitting their financial statements to the tune of $109.8m, which was completely absent during the last three fiscal years and thus contributed to their overleveraged financial position.

{kind=link}

When switching to a quarterly view, their reported operating cash flow of $238.5m is the highest result since at least the beginning of their fiscal year 2022. Admittedly, it was boosted by a very large $112m working capital draw, although this is certainly not negative for two reasons. Firstly, they saw respective working capital builds of $137.1m and $98.2m during their first and second fiscal quarters and thus their latest draw is merely these builds partly reversing. Secondarily, even if excluded, their underlying result of $126.5m is still the best result across this same period of time. Following this improved cash flow performance, it was also very positive to see management increase their guidance for their fiscal year 2023.

NGL Energy Partners Third Quarter Of Their Fiscal Year 2023 Results Presentation

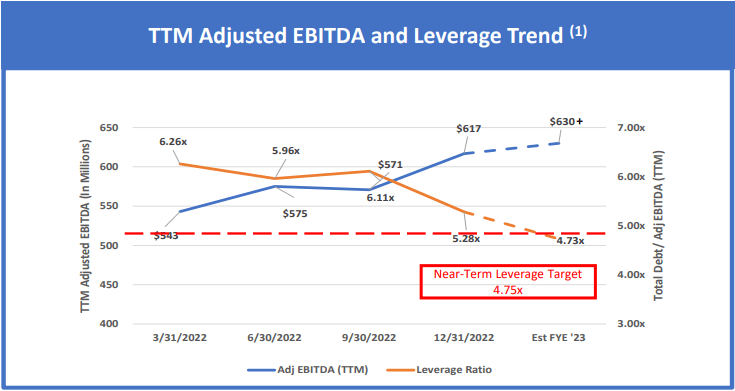

They have now lifted their guidance for their fiscal year 2023 adjusted EBITDA to $630m+ versus its previous forecast of $600m+, thereby representing a 5% improvement. Whilst this does not sound too impressive on the surface, it builds upon their adjusted EBITDA that was only $543m during their fiscal year 2022 and most importantly, it carries significant ramifications for their financial position that stands to see brightness returning on the horizon after many dark days. They have also edged their growth capital expenditure slightly higher too, which now sees their total capital expenditure guidance for their fiscal year 2023 at $120m at the midpoint, not $110m as per their previous guidance but in the grand scheme, this is not material.

{kind=link}

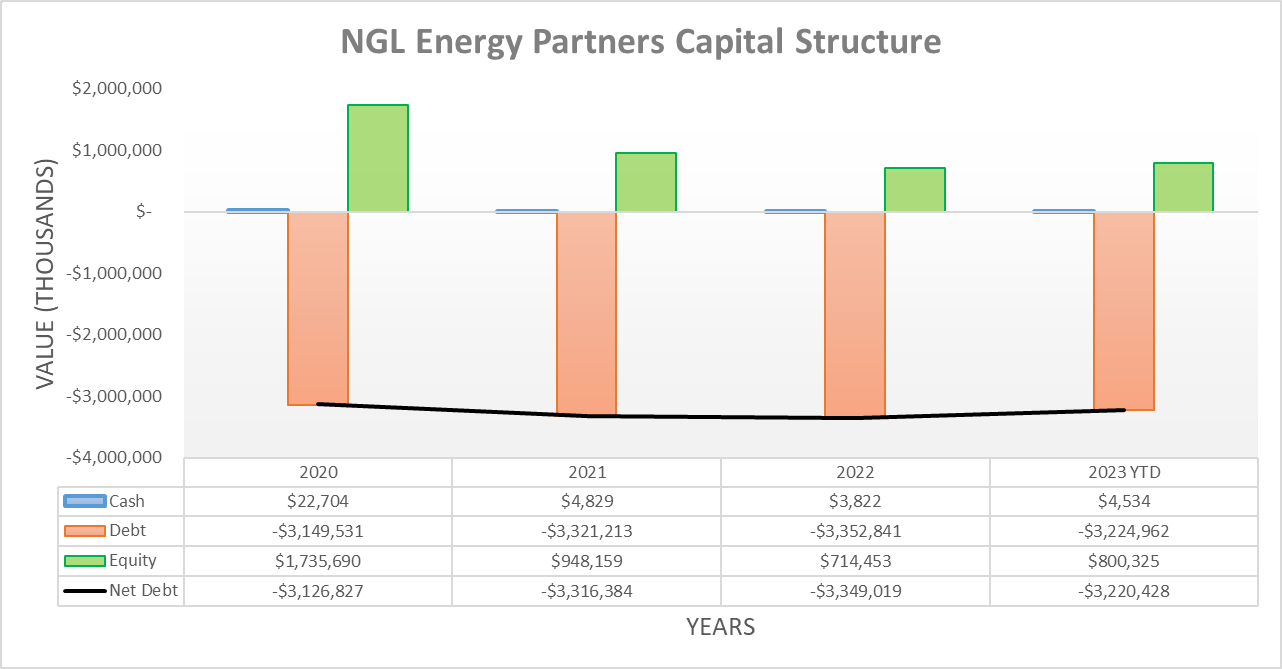

After making no progress reducing their net debt, the third quarter of their fiscal year 2023 finally marked a change, obviously thanks to their improved cash flow performance. As a result, their net debt dropped to $3.22b versus its previous level of $3.446b following their second fiscal quarter and whilst more work is ahead, they are already on the way with the current fiscal quarter seeing further progress reducing debt via aggressively repaying their 2023 notes, as per the commentary from management included below.

At the end of the third quarter, the balance in the '23 notes was $302 million, and during the first few weeks of January, we retired an additional $100 million of the '23 notes, leaving a current balance of $203 million. This is a significant progress in reducing the balance on these notes, and our plan is to fully retire the remaining balance no later than June 30…"

- NGL Energy Partners Q3 2023 Conference Call.

This is very positive and implies their improved cash flow performance is continuing, apart from avoiding bankruptcy via a debt default, it also helps their leverage, debt serviceability and liquidity, as subsequently discussed. When conducting the previous analysis, it was discussed how management was apparently looking at "certain corporate initiatives" in relation to reducing debt, which I suspected was a divestiture. Alas, there was no official news forthcoming but interestingly, during the conference call for the third quarter of their fiscal year 2023, they were asked about these "initiatives" that were apparently delayed, as per the commentary from management included below.

So it wasn't a fire sale. We were very thoughtful about timing, and I think one was pushed back some from like the third quarter to the fourth quarter, one we've we have signed and now we have to go get consent. Another one, the buyer was having difficulty getting financing, and it appears that they've been able to secure financing. So different reasons, but we didn't want to push because you're right, if you do that, then you're going to get a lower price."

- NGL Energy Partners Q3 2023 Conference Call (previously linked) .

Whilst they were scant on details, the way they speak strongly indicates these are divestitures, but the extent remains a mystery. If nothing else, these will further help their improved cash flow performance and expedite a full recovery but at the same time, I hope these are only non-core assets that do not degrade the long-term quality of their partnership.

{kind=link}

When net debt heads south and financial performance heads north at the same time, it creates a powerful combination for deleveraging. In turn, their net debt-to-EBITDA decreased to 5.01 following the third quarter of their fiscal year 2023 versus its previous result of 5.74 following their second fiscal quarter. Likewise, their accompanying net debt-to-operating cash flow saw its respective results drop to 7.31 versus 8.46 across these same two points in time. Despite both of these remaining above the threshold of 5.01 for the very high territory, it is very positive to see material improvements and even more importantly, their leverage ratio as defined by their debt covenants is now forecast to cross beneath its limit of 4.75.

NGL Energy Partners Third Quarter Of Their Fiscal Year 2023 Results Presentation

{kind=link}

Unsurprisingly, this forecast is fuelled by their aforementioned higher adjusted EBITDA guidance for their fiscal year 2023 and obviously, aggressively repay their 2023 notes. Until their leverage ratio is beneath 4.75, they cannot begin catching up on their unpaid preferred distributions, which as my previous analysis highlighted were already $185.9m following the second quarter of their fiscal year 2023, which formed the "too much damage" part of my previous analysis. By the time they reach this point following March 31st 2023, these will obviously be over $200m as they continue accruing and compounding each quarter, thereby meaning this is not a simple task and thus is likely to take many years, depending on the extent of their presently unknown divestitures.

Regardless, reaching a point whereby they can start chipping away at their unpaid preferred distributions is very important and marks the beginning of the road to a full recovery. It is nevertheless still important for their common unitholders to keep their expectations tempered and not expect their common distributions to be reinstated anytime soon.

{kind=link}

Not only does their improving financial performance benefit their leverage, it also benefits their debt serviceability accordingly. As a result following the third quarter of their fiscal year 2023, their interest expense as measured against EBIT sees coverage of 1.31, whilst their operating cash flow sees coverage of 0.98. Even though these are still dangerous, they are nevertheless improvements versus their previous respective results of 1.22 and negative 0.23 following their second fiscal quarter and going forwards, their debt repayments should see this continue and thereby reduce risks.

{kind=link}

When turning to their liquidity, it initially appears to have deteriorated following the third quarter of their fiscal year 2023 with their current ratio dropping to 1.02 versus its previous result of 1.36 following their second fiscal quarter. Whilst still adequate, the primary reason is nevertheless temporary because their aforementioned 2023 notes became a current liability. As a result, they added $302m to their current liabilities and thus hurt their current ratio but thankfully as already highlighted, these are being repaid aggressively and thus future fiscal quarters should see their liquidity improve.

Once repaying their 2023 notes, they will not see any further debt maturities until March 2025, which itself is only a modest $380m with the biggest hurdle not until February 2026 when they see slightly more than $2b maturing. Thankfully, this is three years away and thus, they have time to arrange a mixture of repayment and refinancing as necessary, although if they cannot lean heavily on the latter path, it would hinder their ability to catch up on their unpaid preferred distributions.

NGL Energy Partner Third Quarter Of Their Fiscal Year 2023 Results Presentation

Conclusion

It is surprising and very positive to see they are no longer making too little progress when it comes to deleveraging following their improved financial performance, as they are now on the cusp of achieving their leverage target. Whilst this will allow management to begin catching up on their unpaid preferred distributions, the task is formidable with upwards of $200m+ awaiting and compounding whilst they chip away. I fear there may still be too much damage done to see a full recovery that entails common distributions anytime soon. That said, following their surprisingly positive change I am going out on a limb and thus, I now believe that upgrading to a buy rating is appropriate versus my previous hold rating as the risks of bankruptcy subside and hope for a full recovery returns.

Notes: Unless specified otherwise, all figures in this article were taken from NGL Energy Partners' SEC filings , all calculated figures were performed by the author.

For further details see:

NGL Energy: Darkest Before The Dawn