NGL - NGL Energy Partners: Improved Business Performance But Risk Remains

2023-10-04 02:23:25 ET

Summary

- NGL Energy Partners has somewhat predictable cash flows thanks to long-term fixed fee contracts, but it is still far from becoming profitable and has a high debt load.

- The company's water solutions segment is currently performing well but the excessive debt load of the company remains a concern.

- NGL stock is cheaply valued, but its excessive debt load and underperformance compared to the market make it a risky investment.

NGL Energy Partners ( NGL ) has a somewhat attractive business model, as it boasts of having predictable cash flows thanks to long-term fixed fee contracts. The company has significantly improved its performance lately and thus its stock has tripled in the last 12 months, partly due to a depressed (10-year low) price a year ago. Nevertheless, the water solutions provider is still far from becoming profitable while it also has a material debt load. Given its dramatic underperformance vs. the broad market over the long run, the stock remains highly risky.

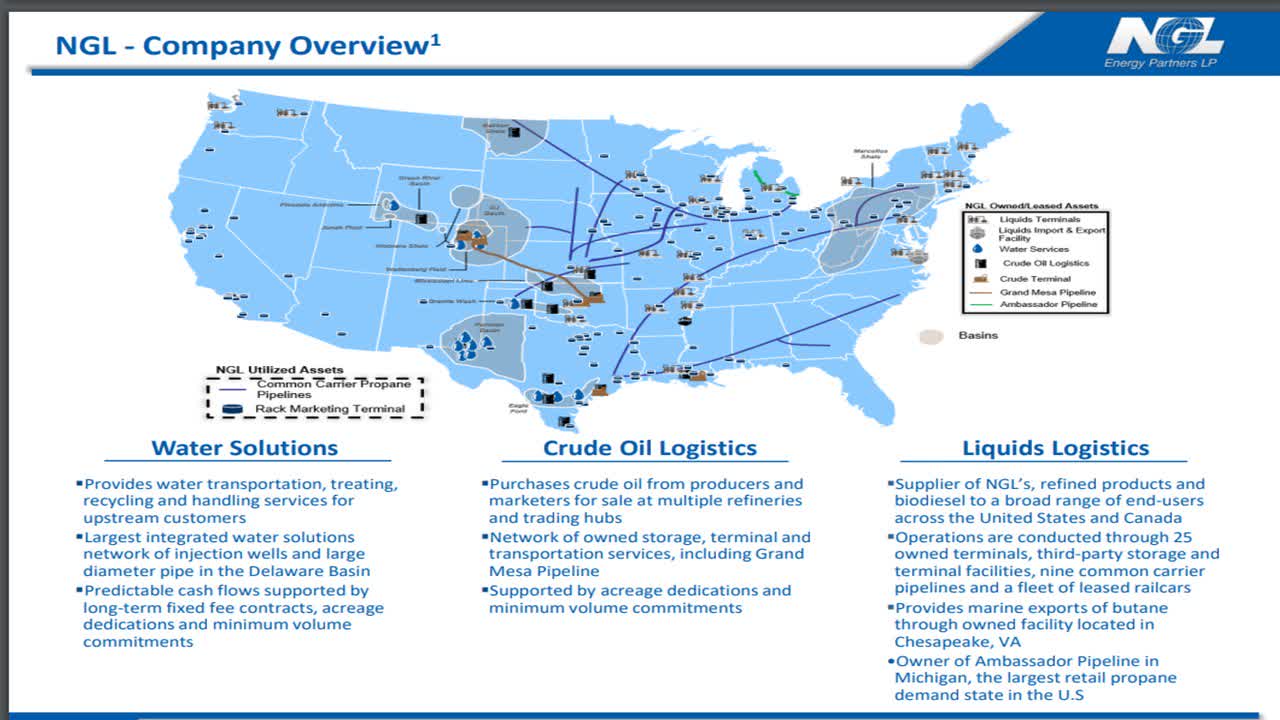

Business overview

NGL Energy Partners provides water transportation, treating, recycling and handling services for upstream oil and gas producers. It has the largest integrated water solutions network of injection wells in the Delaware Basin.

{kind=link}

The company also purchases crude oil from producers and trading companies and sells it to various refineries and trading hubs. Nevertheless, the most significant segment of NGL Energy Partners is its water solutions segment. To be sure, in the most recent quarter, this segment generated 91% of the total EBITDA of the company.

The water solutions division currently enjoys positive business momentum. In the first quarter of fiscal 2024, NGL Energy Partners grew its processed water volume by 14% and enjoyed a 10% increase in the average disposal fee over the prior year's quarter. As a result, the water solution division grew its adjusted EBITDA 17%, to a nearly all-time high of $123 million.

In the latest conference call , management hinted that the water solutions segment has good odds of exceeding the guidance of management for EBITDA of $450 million in the full fiscal year. In addition, management reiterated its guidance for annual consolidated EBITDA of $640-$645 million. Given the EBITDA of $135 million in the first quarter and the positive business momentum of the water division, the company has good odds of meeting the guidance of management. If it does, it will achieve its second-highest EBITDA in the last decade.

Debt

When a company begins its conference call by mentioning its deleveraging efforts, it is safe to conclude that there is a high debt load in place. This rule certainly applies to NGL Energy Partners, whose interest expense consumes 73% of its operating income. In addition, the company has a current ratio of only 1.2 and its net debt (as per Buffett, net debt = total liabilities - cash - receivables) is standing at $3.95 billion . This amount is nearly 8 times the current market capitalization of the stock and hence it is enormous.

Another confirmation that NGL Energy Partners is struggling to reduce its debt load is the suspension of its common and preferred dividend. Management recently stated that it does not expect to pay any preferred dividends in the current fiscal year. The common dividend was suspended shortly after the onset of the coronavirus crisis, in 2020, and is unlikely to be reinstated until the amount of debt falls to a more reasonable level.

On the bright side, management is focused on reducing debt. It repurchased $99 million of bonds during the first quarter and aims to pay off the unsecured notes that mature in 2025 the latest in March 2024. The efforts of management are undoubtedly in the right direction. Nevertheless, the recent purchase of debt was assisted by the sale of non-core assets. This is probably a non-recurring factor.

Moreover, while NGL Energy Partners will almost certainly pay off its 2025 debt before maturation, it will face a hefty debt maturity of $2.05 billion in February 2026. As this amount is nearly 4 times the market capitalization of the stock, it is excessive. As long as business conditions remain favorable, the company will probably be able to roll over this debt into the more distant future. On the other hand, if the company faces an unforeseen downturn, it will be greatly burdened by its high debt load.

Valuation

NGL Energy Partners generated distributable cash flow [DCF] per unit of $0.56 in the first quarter of fiscal 2024 and $2.59 in full fiscal 2023, which ended in March. The DCF per unit in the first quarter corresponds to an annualized DCF per unit of $2.24. This means that the stock is currently trading at only 1.5 times its DCF in 2023 and approximately 1.7 times its expected DCF per unit in fiscal 2024. These are remarkably low valuation levels.

However, NGL Energy Partners has good reasons for being cheaply valued. First of all, unlike the vast majority of MLPs, it does not offer a distribution in order to reduce its debt load. As a result, the stock is less attractive for income-oriented investors. In addition, the stock is highly risky due to its excessive debt load. As mentioned above, its interest expense consumes most of its operating income. Moreover, the company has incurred material losses for 4 consecutive years and is on track for another loss this year.

To cut a long story short, NGL Energy Partners is cheaply valued for good reasons. If the company maintains its decent business momentum for years, its stock has good chances of enjoying a rally. On the other hand, if water volumes in the Delaware Basin moderate, the company is likely to continue to struggle to service its debt.

Long-term underperformance

Companies with excessive debt loads tend to underperform the broad market by a wide margin. This rule certainly applies to NGL Energy Partners. The stock has declined 88% over the last decade and 67% over the last five years. The S&P 500 has rallied 151% and 47%, respectively, over the two time frames. It is thus evident that NGL Energy Partners has dramatically underperformed the broad market throughout these two periods. While most investors enjoyed excessive returns, the unitholders of NGL Energy Partners incurred devastating losses.

Of course, past returns are not reliable predictors of future returns. Nevertheless, the deeply negative returns of NGL Energy Partners are testaments to the weak business model and the highly risky nature of this company. Therefore, the stock should be avoided by conservative investors.

The bottom line

NGL Energy Partners enjoys decent business momentum and its stock appears cheaply valued right now. However, the cheap valuation is due to the excessive debt load of the company, the absence of distributions and its devastating losses over the last decade. While the stock may have a significant upside in the positive scenario (sustained business momentum), I advise investors to avoid highly indebted companies, as their upside potential almost never compensates investors adequately for their excessive risk. The daunting underperformance of NGL Energy Partners vs. the S&P 500 over the long run is a testament to the risk of the stock.

For further details see:

NGL Energy Partners: Improved Business Performance, But Risk Remains