NHS - NHS: Not A Bad CEF If You're Prepared For A Distribution Cut

2023-12-05 17:37:08 ET

Summary

- Neuberger Berman High Yield Strategies offers a high yield of 14.46%, higher than other closed-end funds investing in junk bonds.

- The NHS closed-end fund's net asset value has been declining, raising concerns about the sustainability of its distribution.

- The NHS fund is doing a reasonably good job at protecting itself from default risk, which seems to be increasing with interest rates.

- The fund's leverage is fairly reasonable right now.

- The fund is trading at a discount on net asset value, so the price is decent if you are prepared for a distribution cut.

The Neuberger Berman High Yield Strategies ( NHS ) is a closed-end fund aka CEF that can be employed by investors who are seeking to earn a very high level of income from the assets in their portfolios. The fund’s current 14.46% yield stands as a testament to its ability to provide investors with an income, as this yield is quite a bit higher than that of other closed-end funds that invest primarily in junk bonds. We can see this here:

| Fund |

| Current Yield |

| Neuberger Berman High Yield Strategies Fund |

| 14.46% |

| BNY Mellon High Yield Strategies Fund ( DHF ) |

| 7.96% |

| BlackRock Corporate High Yield Fund ( HYT ) |

| 10.60% |

| Credit Suisse High Yield Bond Fund ( DHY ) |

| 9.69% |

| PGIM High Yield Bond Fund ( ISD ) |

| 10.46% |

The fact that the Neuberger Berman High Yield Strategies Fund has a much higher yield than many of its peers could prove very attractive for any investor who is currently seeking to earn a high level of income from the assets in their portfolios. However, it could also be a sign that the market does not believe that the current distribution is sustainable. As the share price of these funds tends to decline whenever a distribution cut is imposed, this is something that we want to investigate before buying shares of the fund. After all, we do not want to be the victims of a distribution cut or the capital losses that will undoubtedly accompany one.

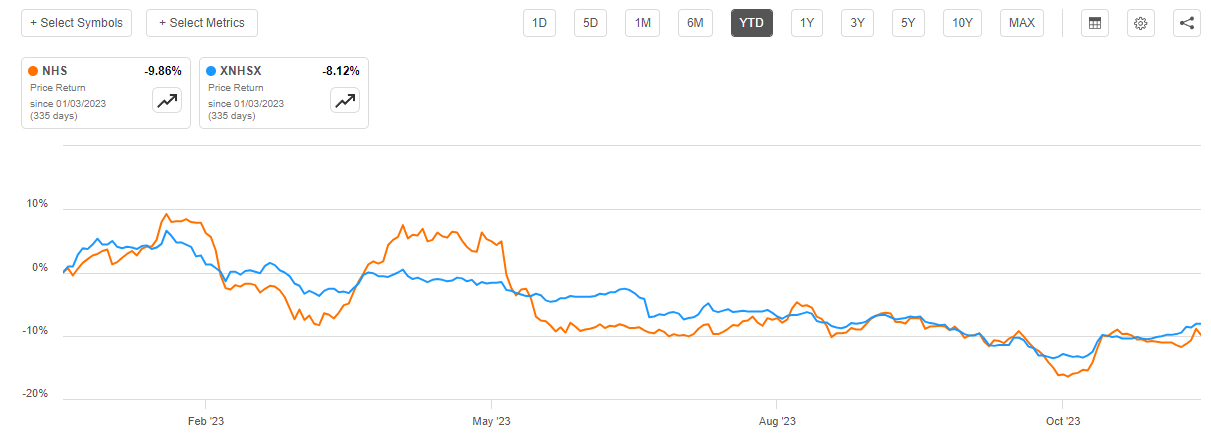

As regular readers may recall, we last discussed the Neuberger Berman High Yield Strategies Fund in the middle of September. At the time, the fund’s ability to sustain its distribution was a real concern, as the fund’s net asset value had been declining for more than eighteen straight months. That unfortunately continues to be the case, as the fund’s net asset value per share is down 8.12% since the start of the year:

{kind=link}

This is despite the fact that the market has been bidding up the price of high-yielding junk bonds recently due to the expectations that the Federal Reserve will reduce interest rates next year. If that does happen, the fund still apparently has a long way to go before it can reverse the declines that it has already seen. In short, the fund might be forced to cut the distribution in the near future, which explains why its yield is much higher than that of comparable funds.

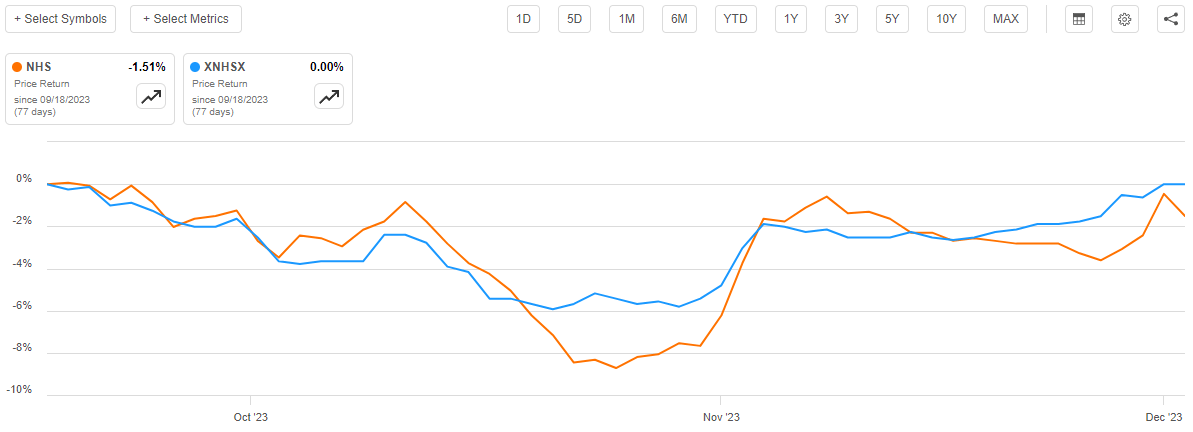

This seems to be reflected in the fund’s recent share price performance. The fund’s net asset value is basically flat since the last time that we discussed it, but its share price has actually declined by 1.51%:

{kind=link}

This is certainly a worse performance than the one that we have seen from other closed-end junk bond funds in recent weeks, and it only adds to my concerns that a distribution cut may be coming in the near future. The market appears to agree with this conclusion.

About The Fund

According to the fund’s website , the Neuberger Berman High Yield Strategies Fund has the primary objective of providing its investors with a very high level of total return. Curiously, the website itself does not specifically state the fund’s objective. Rather, it is necessary to consult the fact sheet to obtain this information. The fund’s website does describe how it seeks to achieve this objective, however. Here is what the fund’s website states:

Neuberger Berman

We immediately note that the fund invests at least 80% of its assets in below-investment-grade debt securities. These are what are colloquially known as “junk bonds,” and they have become something of a popular security type for income-seeking investors to purchase in recent months. Reuters noticed the growing popularity of these securities back in September:

U.S. junk-bond offerings have spiked in recent weeks on the back of strong demand from investors looking to boost their returns by buying the risky yet high-yielding debt.

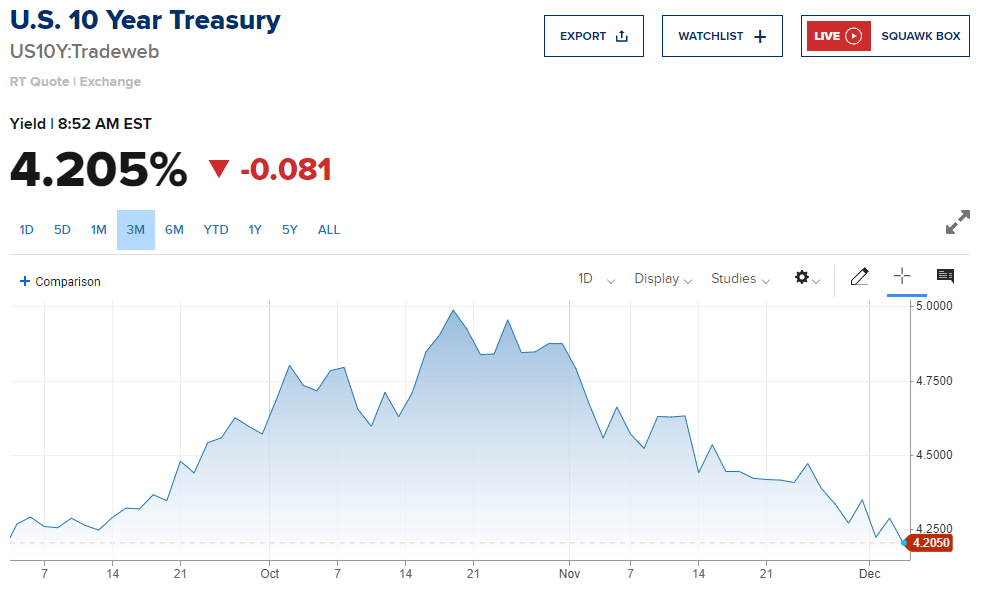

Other sources suggest that some of the popularity that we have been seeing with respect to these issues comes from the fact that investors are looking to lock in today’s high yields before long-term interest rates decline. There is a certain amount of sense here, as we did see long-term interest rates decline in November. This is immediately apparent by looking at the yield of the ten-year U.S. Treasury (US10Y), which is typically considered to be the benchmark for long-term interest rates. As we can see here, the ten-year U.S. Treasury’s yield has fallen from a high of 4.9880% in mid-October to 4.205% today:

{kind=link}

Thus, long-term yields have already declined despite the fact that the Federal Reserve has not reduced the federal funds rate yet. In fact, ten-year U.S. Treasury yields appear to be continuing to decline despite the hawkish comments that Jerome Powell made on Friday. This has had an impact on junk bonds as well, as the Markit iBoxx USD Liquid High Yield Index ( HYG ) is up 1.95% over the past month alone. As rising bond prices denote falling interest rates, this rise in the index clearly indicates that junk bond yields have declined over the past month.

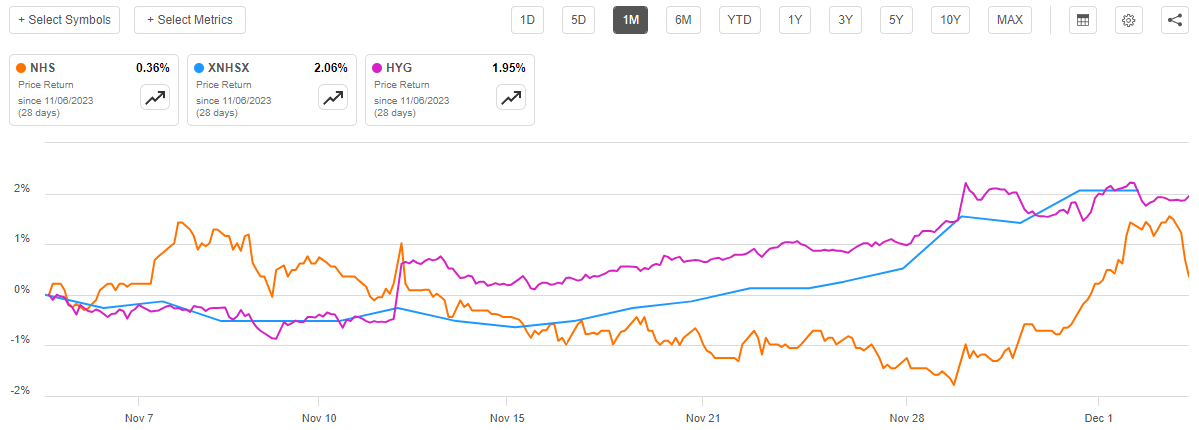

The Neuberger Berman High Yield Strategies Fund has risen with the index over the past month, as its net asset value per share is up 2.06% and its share price is up 0.36% over the period:

{kind=link}

The fact that the fund’s net asset value per share rose more rapidly than the index over the past month is not really a big surprise. This fund employs leverage as a method of boosting its effective total return. We will discuss this in more detail later in this article, but in short, the leverage increases the fund’s gains during periods in which junk bond prices are rising (and increases its losses during periods of hardship). As such, it seems likely that the fund’s net asset value per share will continue to increase as long as long-term interest rates continue to decline. However, this does not necessarily mean that the fund’s share price will show similar performance, as we can clearly see above. Usually, the share price somewhat correlates with net asset value though, so buying shares of this fund could work out as a play on falling interest rates. It begs to be careful though, since a distribution cut could potentially result in losses even if long-term interest rates continue to decline.

As the fund’s website states, the Neuberger Berman High Yield Strategies Fund invests at least 80% of its assets in junk bonds. This is something that could concern potential investors, particularly those who are concerned about the preservation of the principal. After all, junk bonds tend to have a much higher risk of losses due to default than investment-grade securities. Fitch believes that this risk of losses is likely higher today than it was two years ago due to today’s higher interest rates. Per the Reuters article that was linked to earlier in this article,

According to rating agency Fitch, junk debt defaults are expected to reach 4.5% of all outstanding U.S. junk debt by the end of 2023, up from 2.8% in July.

Moody’s Investors Service has issued a similar warning. According to Business Insider ,

Non-investment grade US companies face growing refinancing and default risks with interest rates expected to stay high and financial conditions for borrowers tightening, according to Moody’s Investors Service.

The ratings agency says about $1.87 trillion of junk-rated debt is maturing between 2024 and 2028. That signifies a 27% jump from the $1.47 trillion recorded in last year’s study for 2023-2027.

Debt maturing in the next two years accounts for about 18% of the five-year total, Moody’s said, though the absolute amount for those two years has surged 25% compared to last year’s study, to hit $333 billion.

Moody’s analysts expect the US speculative-grade default rate to peak at 5.6% in January 2024, before easing to 4.6% by August 2024.

Thus, there certainly appear to be significantly more risks related to default losses than would have been the case in previous years. Fortunately, the Neuberger Berman High Yield Strategies Fund appears to be taking precautions to protect its investors against outsized losses from defaults.

First, let us have a look at the ratings that have been assigned to the securities in the fund’s portfolio. Here is a high-level overview:

Fund Fact Sheet

An investment-grade security is anything rated BBB or higher, along with short-term investments and other cash equivalents. As we can see those account for 7.3% of the fund’s total assets. Thus, the majority of the securities in the portfolio are speculative-grade debt, which is exactly what we expected. However, we can see that 81.4% of the fund’s assets are invested in BB or B-rated securities. This is something that is very nice to see from a risk-management perspective since these are the two highest possible ratings for junk bonds. According to the official bond ratings scale , companies whose securities have been issued these ratings have sufficient financial strength to carry their current debt even in the event of a short-term economic shock. Thus, the majority of the assets held by this fund probably do not have substantially high default risk.

We should certainly not ignore the risk of default-related losses despite the fact that the majority of the fund’s assets are invested in high-rated junk bonds. After all, junk bonds still are not as safe as investment-grade credit even if they do carry respectable ratings. Fortunately, the fund has another way to protect itself and its investors against the losses that accompany a bond default. As of the time of writing, the Neuberger Berman High Yield Strategies Fund has 532 unique issuers represented in its portfolio. This should be sufficient to ensure that any individual issuer accounts for such a small percentage of the portfolio that any default will affect such a small percentage of the portfolio that it will not really be noticed. CEF Connect states that the largest holding in the fund’s portfolio only accounts for 1.52% of its assets, and that most of even the largest positions account for less than 1% of the fund’s assets:

CEF Connect

Overall, this should be sufficient to ensure that no single default will have a noticeable impact on the portfolio as a whole. After all, everything held by this fund is yielding well in excess of 1% so any losses will be quickly erased. Thus, we should not really have to worry too much about default-related losses here. The biggest risk is that interest rates will not decrease as quickly as the market is currently assuming and pricing into assets.

Leverage

As mentioned earlier in this article, the Neuberger Berman High Yield Strategies Fund employs leverage as a method of boosting its effective yield. This is a strategy that is employed by most fixed-income closed-end funds, so it is not unique to this one. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase junk bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Neuberger Berman High Yield Strategies Fund has leveraged assets comprising 37.26% of its portfolio. This is obviously well above the one-maximum level that I would normally like to see with any closed-end fund. However, it is generally in line with the 37.23% ratio that the fund had the last time that we discussed it, so the fund is clearly not increasing its leverage.

For the most part, this leverage should be okay as bonds (even junk bonds) are much less volatile than common stock. This lower level of volatility allows a bond fund to employ a bit more leverage than would be safe for a common equity fund. However, we still want to keep an eye on the fund as we do not want the leverage to go much higher considering that junk bonds appear to be somewhat riskier than they were a few years ago. The worst is probably behind us right now in terms of interest rate risk though, so it seems unlikely that things will get much worse for this fund.

Distribution Analysis

As mentioned earlier in this article, the Neuberger Berman High Yield Strategies Fund has the primary objective of providing its investors with a very high level of total return. However, in order to achieve this objective, the fund invests primarily in junk bonds that deliver the bulk of their total return in the form of direct payments to their investors. We can see this in the fact that the Bloomberg High Yield Very Liquid Index ( JNK ) has an average yield-to-maturity of 8.36% at the current price. The fund collects the payments that it receives from all of the bonds in its portfolio and even employs a layer of leverage to collect more interest payments than it otherwise could by relying solely on its equity funding. The fund adds any profits that it manages to realize by trading bonds during periods of falling interest rates. Finally, it pays out all of the money that it collects from these operations to its shareholders, net of its own expenses.

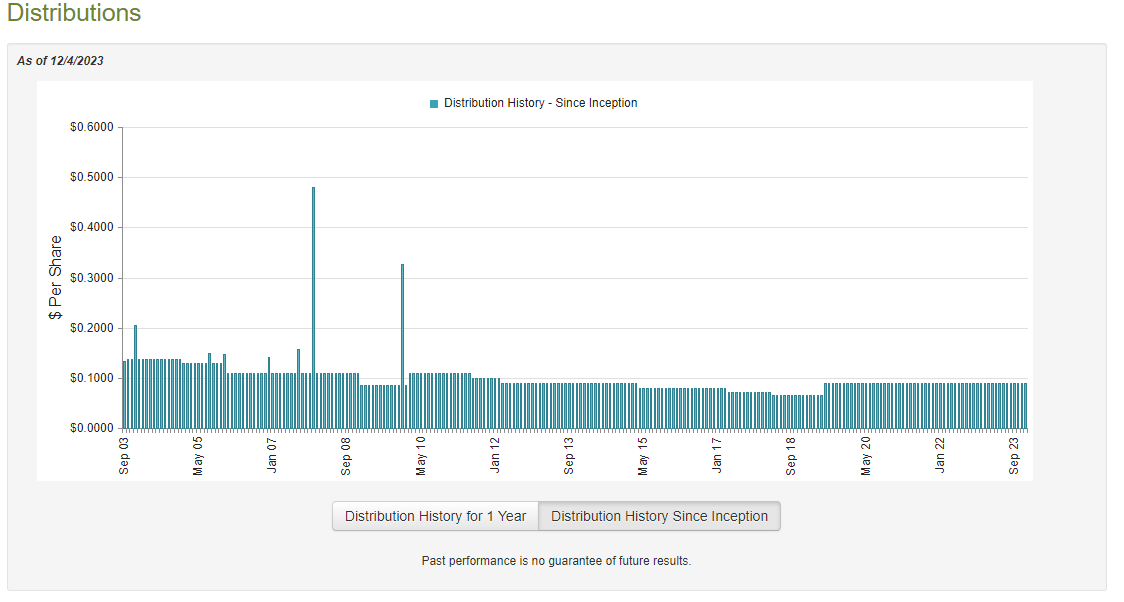

As such, we can probably expect that this business model would result in the fund’s shares having a very high distribution yield. This is indeed the case, as the Neuberger Berman High Yield Strategies Fund pays a monthly distribution of $0.0905 per share ($1.086 per share annually), which gives it a whopping 14.46% yield at the current price. This is a substantially higher yield than most other junk bond funds possess, and as mentioned in the introduction it might be a sign that the market fears that the fund will not be able to sustain its distribution. It has not yet cut so far though, as this is one of the few fixed-income funds that has kept its distribution stable straight through the current monetary tightening cycle. The fund’s distribution has been stable since June 2019, although it was more volatile prior to that date:

{kind=link}

The fund’s recent stability with respect to its distribution might be appealing to those investors who are seeking to receive a safe and secure distribution that they can use to pay their bills and finance their lifestyles. The fund’s very high current yield adds to this appeal, as we all need as much income as possible due to the rapidly rising cost of just about everything that we purchase in our daily lives. However, it is very curious that this fund has been able to maintain a stable distribution when other funds that use a similar strategy have not, so we want to pay special attention to its ability to sustain the current payout.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the Neuberger Berman High Yield Strategies Fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is certainly an interesting period of time for the report to cover, as the first half of 2023 was characterized by a euphoric market that expected that the Federal Reserve would slash interest rates significantly in the second half of 2023. While that expectation ultimately proved to be wrong, we still saw investors bidding up bond prices in accordance with this belief and that could have allowed this fund to earn some capital gains by trading appreciated assets. This report will give us a good idea of how successful the fund was at exploiting this potential opportunity.

During the six-month period, the Neuberger Berman High Yield Strategies Fund received $10,566,897 in interest from the assets in its portfolio. It had no other sources of income, but it did have to pay $34 in foreign withholding taxes. As such, the fund reported a total investment income of $10,566,863 during the period. It paid its expenses out of this amount, which left it with $5,399,261 available for shareholders. Obviously, this was nowhere near enough to cover the $10,553,716 that the fund actually paid out in distributions during the period. At first glance, this is almost certainly going to be concerning since we usually like a fixed-income or debt fund to be able to fully cover its distributions out of net investment income.

Fortunately, the fund has other methods through which it can obtain the money that it needs to cover its distribution. For example, it might be able to take advantage of interest rate changes to obtain some capital gains when the bonds that it holds in the portfolio go up in price. The fund had mixed results at this task during the period. It reported net realized losses of $10,569,197 but it was able to fully offset this by $13,577,214 of net unrealized gains. However, the fund still failed to cover its distribution, as its net assets declined by $2,101,340 after accounting for all inflows and outflows during the period.

The fund’s net assets declined by $12,813,238 in aggregate during the full-year 2022 period despite the fund conducting a capital raise that brought in $38,701,436 during the year. Thus, the fund has failed to fully cover its distribution over the past eighteen months for which it has reported results. This certainly explains why the market seems to be anticipating that the fund will cut its distribution.

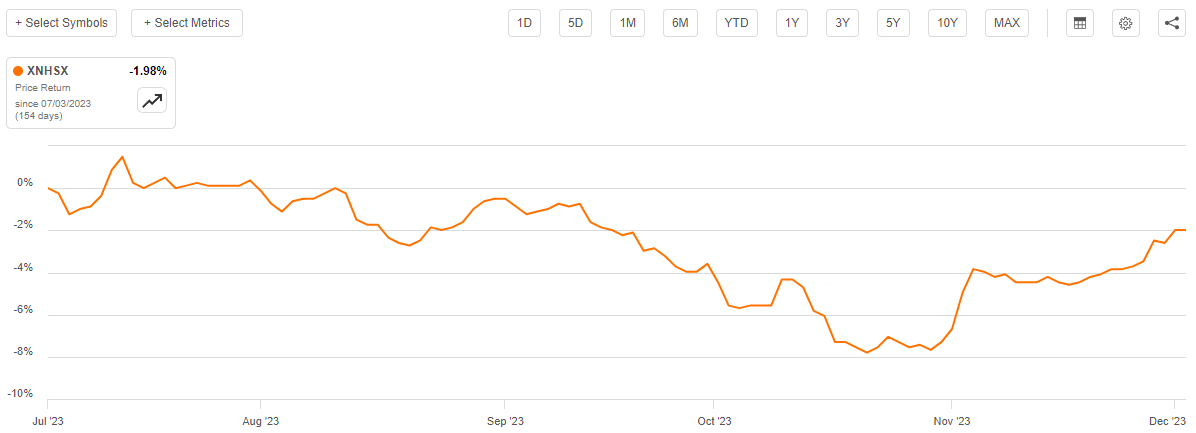

However, this report is now five months old, and the market has experienced a few swings since its release. In particular, we saw a tightening of financial conditions from mid-July until mid-October that pushed interest rates up and bond prices down. Then the market reversed, and interest rates have very rapidly declined since late-October, which has pushed up the price of the bonds held by this fund. As such, the question right now is whether or not the fund is continuing to fail to cover its distribution. Unfortunately, the answer to this question appears to be yes. As we can see, the fund’s net asset value per share is down 1.98% since July 1, 2023:

{kind=link}

Thus, the fund has clearly been paying out more than it has been able to earn from its portfolio over the second half of the year so far. This comes following the eighteen months of losses that were shown in the fund’s most recent financial report. As such, it is difficult to see how this fund can sustain its distribution at the current level unless interest rates decline significantly further than they already have. This seems highly unlikely, considering that the Federal Reserve has started to turn more hawkish, and inflation is still a pretty big problem. Thus, the market could be correct in pricing in a distribution cut.

Valuation

As of December 4, 2023 (the most recent date for which data is currently available), the Neuberger Berman High Yield Strategies Fund has a net asset value of $7.92 per share but the shares currently trade for $7.52 each. This gives the fund’s shares a 5.05% discount on net asset value at the current price. This is not quite as good as the 6.01% discount that the shares have had on average over the past month. As such, investors might be able to obtain a better price by waiting a bit. However, in this case, it might be best to wait and see what happens to the distribution before buying shares.

Conclusion

In conclusion, the Neuberger Berman High Yield Strategies Fund is a closed-end fund that provides its investors with an incredibly high yield by investing in a portfolio of junk bonds. However, there are some very real signs that the fund is struggling to sustain its distribution and destroying the fund’s net asset value at the same time. This could result in a distribution cut that would probably have a negative impact on the fund’s share price, at least temporarily. Then again, the Neuberger Berman High Yield Strategies fund could do pretty well if long-term interest rates continue to decline, but there is no guarantee that this will be the case. Overall, though, this fund might be worth taking a chance on if you are prepared for the potential distribution cut.

For further details see:

NHS: Not A Bad CEF If You're Prepared For A Distribution Cut