AY - Nightmare On REIT Street - Briefly Explaining The Bloodshed

2023-08-16 12:50:59 ET

Summary

- Rising long-term interest rates are causing a sell-off in rate-sensitive stocks like REITs.

- The sell-off is driven by increased borrowing costs, falling asset values, and competition from attractive bond yields.

- Despite the sell-off, the fundamentals of real estate remain strong, and the long-term benefit of higher interest rates is a reduction in new construction projects.

- Here is your daily reminder not to be scared into abandoning your investing strategy or making bad long-term decisions because of headlines or interest rates.

All of this digital red ink on the screen representing stock prices for real estate investment trusts ("REITs") reminds me of the slasher movie, A Nightmare on Elm Street .

I am currently in Europe and going to bed a little bit before the US stock market closes. In the classic horror movie, the characters struggle to stay awake, because when they fall asleep, they could be killed by the menacing villain in their dreams. I feel somewhat the same, going to sleep only to wake up to bloodshed in my portfolio.

Only, I suppose it doesn't matter whether I sleep or not. Freddy Krueger is coming for our REITs whether we're asleep or awake!

Since Fitch's downgrade of its US government credit rating from AAA to AA+ on August 1, the S&P 500 ( SPY ) has taken a slight hit, but more interest rate-sensitive sectors like real estate ( VNQ ) and utilities ( XLU ) have taken a particularly harsh beating:

They have been falling, of course, because interest rates on the long end of the curve have been rising. Take a look at Treasury bond yields from 10 years all the way out to 30 years, which were in an uptrend before August 1, but seem to have accelerated somewhat to the upside since then.

As I explained in my recent article " REITs Vs. BDCs: A Lesson In Contrarian Investing ," REITs (and for that matter, also utilities, renewable energy YieldCos, energy midstream companies, and certain other types of dividend stocks) primarily use long-term debt at terms of 5 years or longer. While they usually carry some floating rate debt, the lion's share of their debt is fixed-rate and long-term.

So, when the Federal Reserve pushes up its short-term policy rate, REITs and other rate-sensitive companies mostly suffer from it indirectly. The market believes the Fed's rate hike is likely to cause long-term rates to rise or at least not fall.

One of my largest holdings, Clearway Energy Inc. ( CWEN , CWEN.A ), has also dropped in response to the spike in long-term rates. So have its fellow renewable power producers, Brookfield Renewable ( BEP , BEPC ), NextEra Energy Partners ( NEP ), and Atlantica Sustainable Infrastructure ( AY ), to varying degrees.

For fun, I included in this chart Brookfield Infrastructure Partners ( BIP ), the cousin of BEP that invests in various non-renewable energy infrastructure as well as regulated utilities, toll roads, ports, telecommunications towers, data centers, and so on.

All of these companies share in common a relatively high long-term interest rate sensitivity. And it isn't merely because it raises their cost of debt as bonds and term loans mature and need to be refinanced at the higher prevailing market rate.

Rate-sensitive stocks also suffer from the market perception (if not the reality) that higher long-term interest rates cause the value of their assets, which are usually bought at a yield-spread above their cost of debt, to fall.

When asset values fall, or at least when the market perceives them to be falling, the stock price typically falls in response.

Here's CWEN's CEO Chris Sotos on the company's Q2 conference call on August 8th:

I think we all need to see where the treasury market kind of settles out at. This kind of four handle has been a pretty recent phenomenon, which I think has driven some of the weakness in the stock.

I would argue that the spike in long-term Treasury rates has driven most of the weakness in rate-sensitive stocks like CWEN.

Lastly, its notable to add that when long-term rates go up to a sufficient degree (especially nice, round numbers like 4% or 4.5%), many investors decide to throw in the towel on the dividend-yielding stocks and allocate that capital instead to bonds.

Why take so much risk in REITs when you can enjoy the safety of interest payments from a bond?

It's an understandable thought process, but it ignores inflation. Bond interest payments are fixed. They don't rise over time. Meanwhile, many if not most dividend stocks raise their dividends over time, which protects the real (inflation-adjusted) value of those income streams for shareholders.

So, in short, here are the three reasons why rising long-term interest rates trigger selloffs in rate-sensitive stocks like REITs:

- It incrementally increases borrowing costs over time

- It often causes companies' underlying asset values to fall

- It creates competition for scarce shareholder capital by making bond yields attractive in comparison

What's The Solution?

It is part of human nature to avoid pain. The more pain we feel, the more desperate we become to avoid that pain.

Sometimes, our desperation to alleviate the pain leads to very bad decisions with long-term negative consequences. My wife, who works at a hospital, has seen many sad cases of this firsthand.

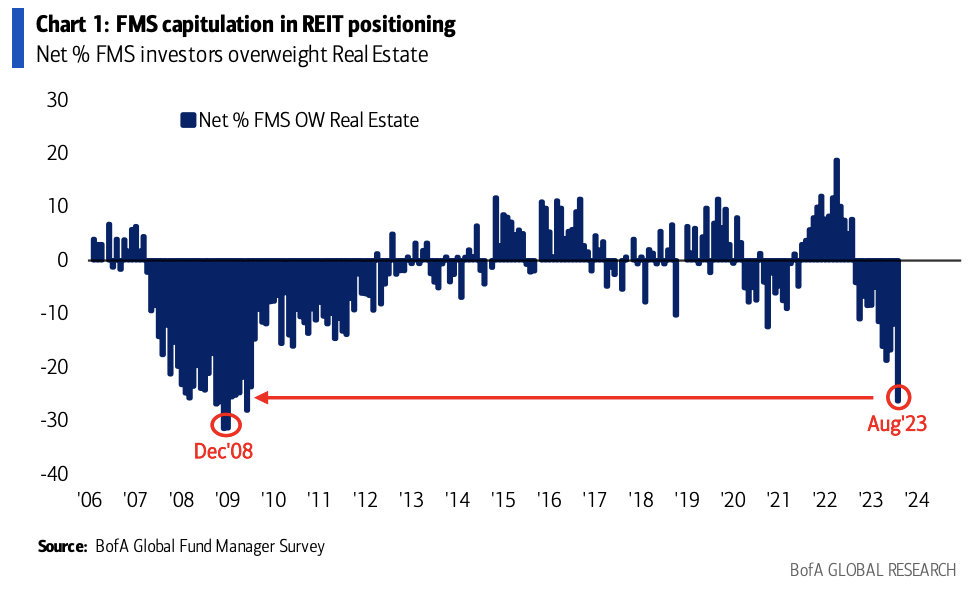

Right now, in order to alleviate the discomfort of showing big unrealized losses in REITs, money managers are realizing those losses by selling at steep discounts. This has made investment professionals almost as underweight REITs as the period after the collapse of Lehman Brothers in 2008.

{kind=link}

Recall that in 2008, Lehman Brothers collapsed mostly because of bad real estate-backed securities.

But there is a crucial difference between 2008 and today. Simply put, it's the fundamentals of real estate.

In 2008, real estate was dramatically overbuilt. Today, it is not. That's why rent rates are still rising across almost all sectors of real estate.

Moreover, in 2008, REIT balance sheets were much more stretched than they are today.

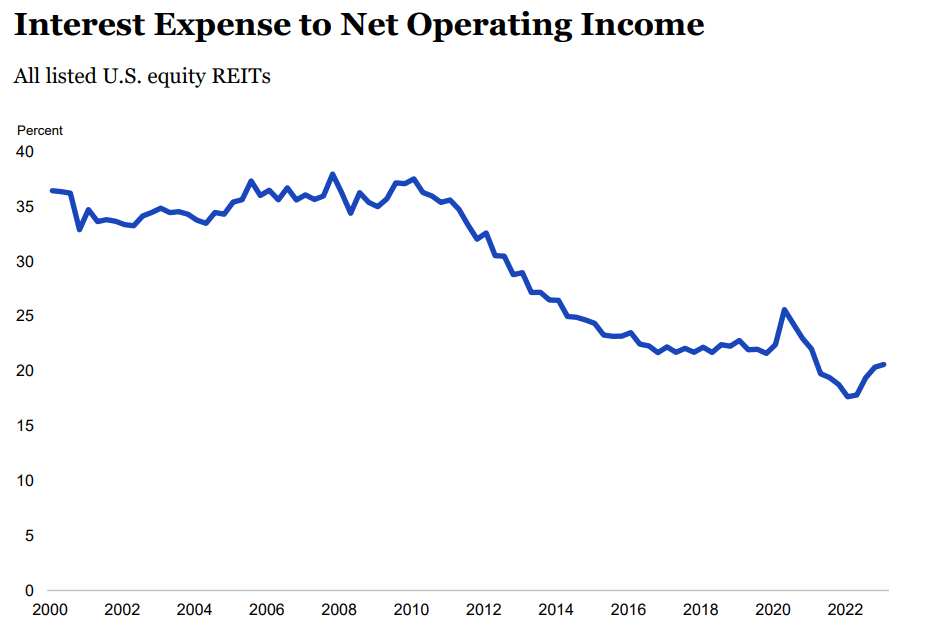

For example, in 2008, REIT's interest costs to NOI was around 35%. Today, that metric is in the low 20% area.

{kind=link}

During the long period of low interest rates, especially from 2019 to 2022, REITs gorged on long-term debt at ultra-low interest rates, extending out their maturity schedules as far as possible. Several high-quality REITs like Alexandria Real Estate Equities ( ARE ) and NNN REIT ( NNN ) issued 30-year bonds during this period at more favorable rates than they could likely get on 5-year bonds today.

The weighted average term to maturity for REITs is now about 7 years, compared to about 5 years in 2008.

REITs' interest coverage ratios average around 4.5x today, versus slightly under 3x in 2008.

The bottom line here is that REITs and other rate-sensitive stocks are reflexively selling off because of rising long-term interest rates, not because of fundamental weakness. In fact, in many cases, the fundamentals continue to strengthen even while higher rates cause the stock prices to drop.

And there is a long-term benefit of elevated interest rates for REITs worth mentioning.

As I explained in " Fed Rate Hikes Create Short-Term Pain But Long-Term Gain For REITs ":

The primary way that high interest rates will ultimately benefit REITs and their existing property portfolios is through dramatically reducing the development pipeline of new commercial real estate projects.

Take apartments, for example. Permits for multifamily housing have been plummeting over the last year as high borrowing costs make it harder to greenlight new development projects.

The same generally holds for other types of commercial real estate that have attracted activity from developers over the past few years, such as industrial buildings.

From 2021 through the end of 2022, developers collectively greenlit a surge in industrial space in response to incredibly high tenant demand and soaring rents.

Ian Formigle, Crowdstreet

But since the beginning of 2023, when borrowing costs have risen to nosebleed heights and construction costs remain high, new projects simply don't pencil out anymore.

Industrial construction starts have dropped by over half at this point. On the Q2 earnings conference call for Sunbelt industrial REIT EastGroup Properties ( EGP ), CEO Marshall Loeb stated:

[A]s we sit today at 98% leased and occupied, I've never seen supply falling as fast as it is.

And I think third quarter will be lower -- a bigger drop than second quarter was. When we say it was half of what [second] quarter last year was, I think third quarter will -- I'm estimating 60% drop, something like that in terms of starts.

Less construction starts = less new supply of buildings in the future = less competition for REITs' existing portfolios.

As I said in the previously cited article:

Less new supply in mid-2025 and onward makes REITs' existing property portfolios more valuable by funneling demand into a smaller-than-otherwise pool of supply.

In short, then, the fundamentals for REITs remain solid, and in a few years they will be even better because of the sharp slowdown in new construction activity we are experiencing right now.

Bottom Line

It's a nightmare on REIT street, but mostly for those who sell their fundamentally solid REITs at a steep loss in order to avoid further downside.

Pain avoidance is a normal, natural, and healthy human behavior. But it can cause us to make poor long-term decisions if we let it. It takes discipline to endure the pain rather than accepting destructive consequences in exchange for temporary relief.

Selling your REITs (or utilities, renewables, etc.) now may or may not stop your portfolio's market value from falling, but it won't help in the long run if you buy back many of the same stocks later at higher prices and lower yields.

The simple solution is to continue following your investment strategy, whatever that is, and to keep your eyes fixed on your ultimate financial goals.

Maintain proper diversification. Reinvest your dividends. And for heaven's sake, don't let Freddy Krueger scare you into believing that the only value your REITs have is the stock price!

For further details see:

Nightmare On REIT Street - Briefly Explaining The Bloodshed