NINE - Nine Energy Service: Approaching The Buy Zone Again

2023-03-28 23:49:57 ET

Summary

- NINE's correction is no surprise but its magnitude exceeded my expectations.

- The bond market suggests the correction may have been exacerbated by the stresses in the financial system.

- From a fundamental perspective, NINE is again approaching undervalued territory.

- The bankruptcy risks are low for now despite the weakness in natural gas.

- The 2028 bonds may be worth a look too soon.

Investment Thesis

This article updates my prior coverage of Nine Energy Service, Inc. ( NINE ). NINE is a small oilfield services stock with high volatility and is popular on WallStreetBets. Just because a stock has "meme" status doesn't mean it can't be a sound investment, though. NINE benefits from the gradual transition of pricing power from oil and gas operators to the services providers, and the company's operational metrics have been improving. The re-financing concerns that pressured the stock for much of 2022 were largely addressed in January 2023.

The problem with NINE stock has been that the tremendous volatility often makes it alternate between overvalued and undervalued territory. Three months ago NINE appeared to have gone quite ahead of its valuation and I warned a correction may happen:

{kind=link}

NINE actually went up to $17 before it corrected down to $5 so far. The correction is no surprise, but its magnitude exceeded my expectations. I suspect there were two compounding factors:

- The crash in natural gas ( NG1:COM ) scared away investors from smaller oilfield services companies on the fear that gas rigs counts will suffer major declines;

- The banking crisis has impacted high-yield credit spreads and NINE's 2028 notes also sold off a bit two weeks ago.

The bottom line is that NINE is again approaching undervalued territory. The enterprise value is now at 5.2x EBITDA which is comparable to the overall sector, but the sector valuations have also gone down. I see a valuation in the $8 to $10 range as fair. The Wall Street average price target remains over $13:

{kind=link}

The bonds also seem like a good deal with 15% yield although that could go up more with another systemic event. I have initiated small positions in both the equity and the bonds. If the market offers lower entry points, I will add more.

Gas market fundamentals

When it comes to the debacle in natural gas prices, the chart speaks for itself:

Freeport LNG out of commission and the warmer winter have been singled out as the main culprits, but rising gas oil ratios are probably contributing too. The market is expecting a significant drop in gas rigs and pressure pumping stocks such as ProFrac ( ACDC ), ProPetro ( PUMP ) and Liberty ( LBRT ) have been slammed:

The theory is that companies with more gas basin exposure as ACDC were hit worse:

{kind=link}

However, things aren't that clear cut. Appalachia is a gas basin but liquids rich so the economics works even with $2 gas. The main school of thought seems to be that most rigs will be pulled out of the Haynesville. Overall, gas rig counts have not yet responded:

NINE has Haynesville exposure but it is 16% only; management responded on a question about the Haynesville impact during their last earnings call :

The reality is that all of us had a really tough February looking at gas and now we're up over $3 on the gas side so that feels much more constructive. I think it would be surprising if OFS as a sector started to give up price because this is a sector that was negative net income in 2021.

And those are companies of outside of the mega caps. Those are companies of scale and small companies, negative net income for 2021 and single-digit EBITDA margin, not sustainable. So I would say the price that we garnered as a sector in 2022 was simply reflation. It was just reflation. These are normalized costs now. And I think we had a Goldilocks scenario for our customers in the past.

So I'll be very surprised if you see massive amounts of price being given up here because, again, this is still steady at and $3 is by no means the worst gas price this country has seen. So, we're not terribly concerned about this. We're just not going to forecast pricing inclining, which we certainly would have had we been in a scenario where instead of 30 rigs down, we have seen 30 rigs up, if that makes sense.

Gas is now closer to $2 than $3, but I think their logic still stands. Land drillers and pressure pumping companies have also spoken recently about diverting resources from Haynesville to other basins which remain tight; this could also help compensate for lost demand for NINE's own products and services in the Haynesville.

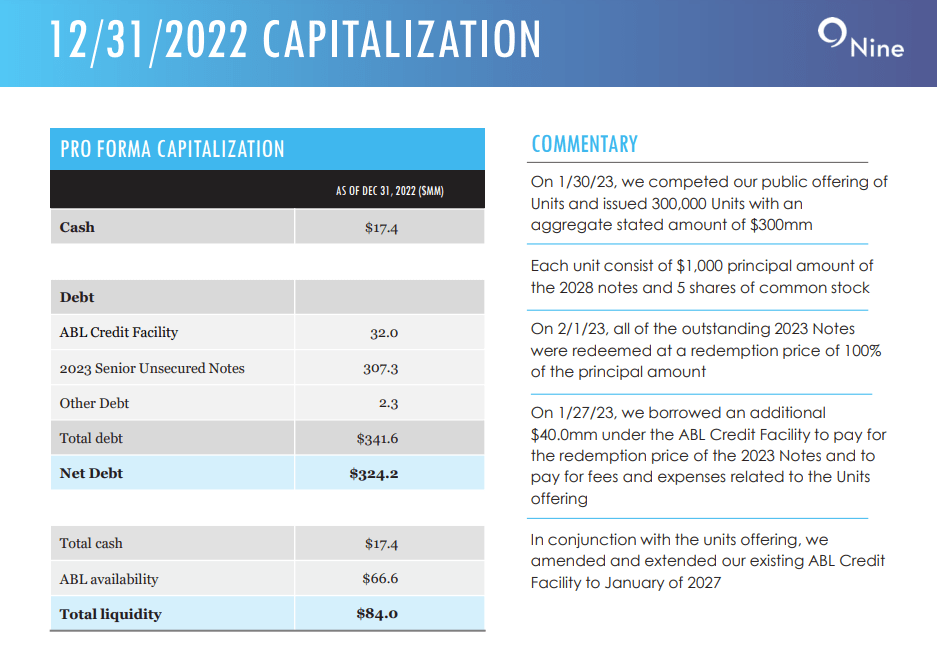

Debt concerns

The refinancing of the 2023 notes and extending the maturity to 2028 was a big success for management:

{kind=link}

The latest EBITDA estimate for 2023 is about $100 million; this implies about 3.5x debt/EBITDA; interest coverage should be about 2.5x now. It is far from ideal, but I think there is some safety margin to weather even a more pronounced decline in rig counts, which, of course, is yet to be seen.

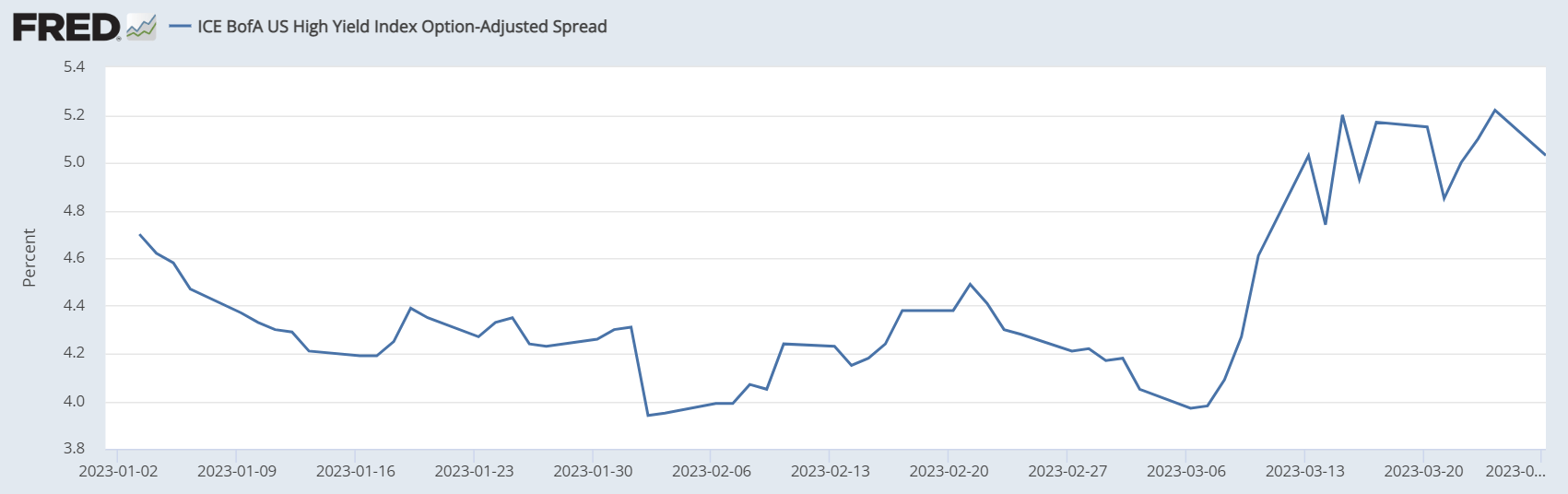

The bonds have sold off a bit though. According to Refinitiv, as of March 15, the yield was 12.8%; this was up to 15.0% a week later. It likely has something to do with the credit repricing in the broader market:

{kind=link}

NINE's rate on the 2028 notes is fixed, though. The only thing that really matters is the long-term prospect for its business.

Takeaway

My feeling is that the correction is getting a bit overdone. Technical indicators also suggest NINE may be oversold:

{kind=link}

The next month put option expirations show most open interest at $5, and we are close to this level.

Fundamentally, I think the market may have overreacted to the gas price decline. While we may still see better entry points, I am updating my views to a "buy." I think the bonds also deserve a look, but a recession may also offer them at a greater discount later in the year.

For further details see:

Nine Energy Service: Approaching The Buy Zone Again