NINE - Nine Energy Service: Successfully Refinanced Its Debt And Trades Undervalued

2023-07-10 21:58:16 ET

Summary

- Nine Energy Service has successfully refinanced its debt and issued new equity, but the market has reacted negatively.

- The company's technological advantages, relationships with large oil and gas operators, and geographically diversified clients suggest potential for stock price growth.

- Despite competition from large and small companies, Nine Energy Service's effectiveness gives it an edge.

Nine Energy Service, Inc. ( NINE ) successfully refinanced its debt, and issued some new equity, to which the market reacted with pessimism. In my view, the technological advantages offered like dissolvable plugs, relationships with large oil and gas operators, and the geographically diversified clients are sufficient reasons to expect upside stock price potential. Yes, I see risks from the total amount of debt, the action of competitors, or a decrease in efficiency. With that, I believe that NINE currently trades quite undervalued.

Nine Energy Service

Nine is a company formed in 2013 that provides services for oil and gas companies within the United States. Through its work model that requires commercial agreements with each of its clients for the development of infrastructure for extraction, the company offers technologies for the design and development of facilities and production plants.

Nine Energy offers its clients completion solutions for projects under development in unconventional areas with access to these resources, facilitating the production process and aiming at reducing costs. Some remarkable technological innovations offered are the dissolvable plugs, which offer almost 100% FCF conversion, and require minimal capex to generate significant growth.

Q1 2023 IR Presentation

The particular differential in the services of this company is that due to the nature of its business, it allows its clients to generate a customized action plan adapted to their needs, including all the design phases that range from the preparation of the wells with cementation until the final extraction of the machines used in the production. In some cases, these services are contracted in isolation, while they, in many cases, include packages for the entire production process, including the extraction of resources and the provision of patented technologies that are used in it.

All of Nine Energy Service's activities are encompassed by a single operating segment: the cementation process. Within this process are the main services that the company offers to its clients. The cementation process was, during 2022, calculated at more than 18,000 jobs carried out with 90% effectiveness within the agreed deadlines.

Other services include the finishing tools service, which includes both the physical tools and the patented technologies developed by the company itself that are used during the production phases of its clients. The company also offers wiring services, which serve for the security and containment of the electrical networks of the facilities, and the piping services.

By 2022, the company's top five customers accounted for 21% of the company's annual revenue. Some of the customers are massive corporations with multi billion budgets, which most investors would appreciate.

Q1 2023 IR Presentation

Beneficial Market Expectations

I believe that investors need to have a second opinion about the expectations of any company. With this in mind, I reviewed the expectations of other market analysts, which included double digit 2025 EBITDA growth of close to 19% and an impressive FCF growth in 2025. In my view, if the figures reported in 2025 are as good as expected, I believe that the stock price would most likely increase.

Source: Marketscreener.com

Balance Sheet

Nine reported cash and cash equivalents worth $21 million, accounts receivable of about $98 million, inventories close to $67 million, prepaid expenses and other current assets of $9 million, and total current assets worth $196 million. The total amount of current liabilities is significantly lower than the total amount of current assets, so I do not think liquidity appears to be a problem here.

The list of long term assets includes property and equipment of about $87 million, operating lease right of use assets close to $39 million, intangible assets of about $99 million, and total assets of about $426 million. The asset/liability ratio stands at less than 1x, which most investors may not appreciate.

Source: 10-Q

The list of liabilities includes accounts payable worth $37 million, accrued expenses of about $25 million, current portion of long-term debt of close to $1 million, and current portion of operating lease obligations worth $8 million. Long-term debt stands at $331 million, which is not a small figure. Besides, total liabilities are equal to $438 million.

Source: 10-Q

DCF Model

Nine is currently maintaining a strategy of growth and organic expansion, supported in part by the technological offer of its services as well as the geographical variety where it carries out its activities.

At the moment, Nine Energy operates in some of the most relevant resource areas in the country. Due to the facilities under its ownership distributed throughout the country, the speed of reaction to the needs of customers is high, allowing the operation and delivery of projects within agreed deadlines. I assumed that the geographic diversification will most likely enhance FCF growth and net sales growth.

Source: Q1 2023 IR Presentation

Nine maintains an active and open strategy of future acquisitions of emerging companies, specifically small companies with specific technological developments that serve to add functions or value to the company's services. The company seeks to position the brand as a benchmark in the quality and effectiveness of services as well as to expand its experience for the next decade. Considering previous goodwill increases, I believe that Nine Energy does have a lot of expertise in integrating M&A targets. I assumed that future acquisitions would be successful, and debt holders would accept the new acquisitions.

Source: Ycharts

Besides, I believe that the assets, the labor light business model, and stickier depreciation-based service lines will most likely improve FCF margins, and offer enhanced cash generation abilities. Nine discussed these strategic guidelines in the last annual report.

Source: Q1 2023 IR Presentation

Finally, under my DCF model, I assumed that the average rig count and other indicators of the oil and gas industry will continue to improve as we saw in the three years. Let's note that the expectations for 2023 included in the last quarterly presentation were quite beneficial.

Source: Q1 2023 IR Presentation

In 2023, the company received close to $300 million in a combination of debt and equity. As a result, the stock price declined from close to $15 per share to less than $5 per share. I believe that the decline in the stock price does seem too large. Even if the interest paid for the debt increased, this new money means money to finance new projects. It also shows that there is demand for the business model offered by Nine. Under my financial model, I assumed that investors will most likely reconsider the fair value of Nine. As a result, some new stock demand will most likely show up.

On January 30, 2023, we completed our public offering of 300,000 units with an aggregate stated amount of $300.0 million (the “Units”). Each Unit consists of $1,000 principal amount of our 13.000% Senior Secured Notes due 2028 (collectively, the “2028 Notes”) and five shares of our common stock. Source: 10-Q

Source: SA

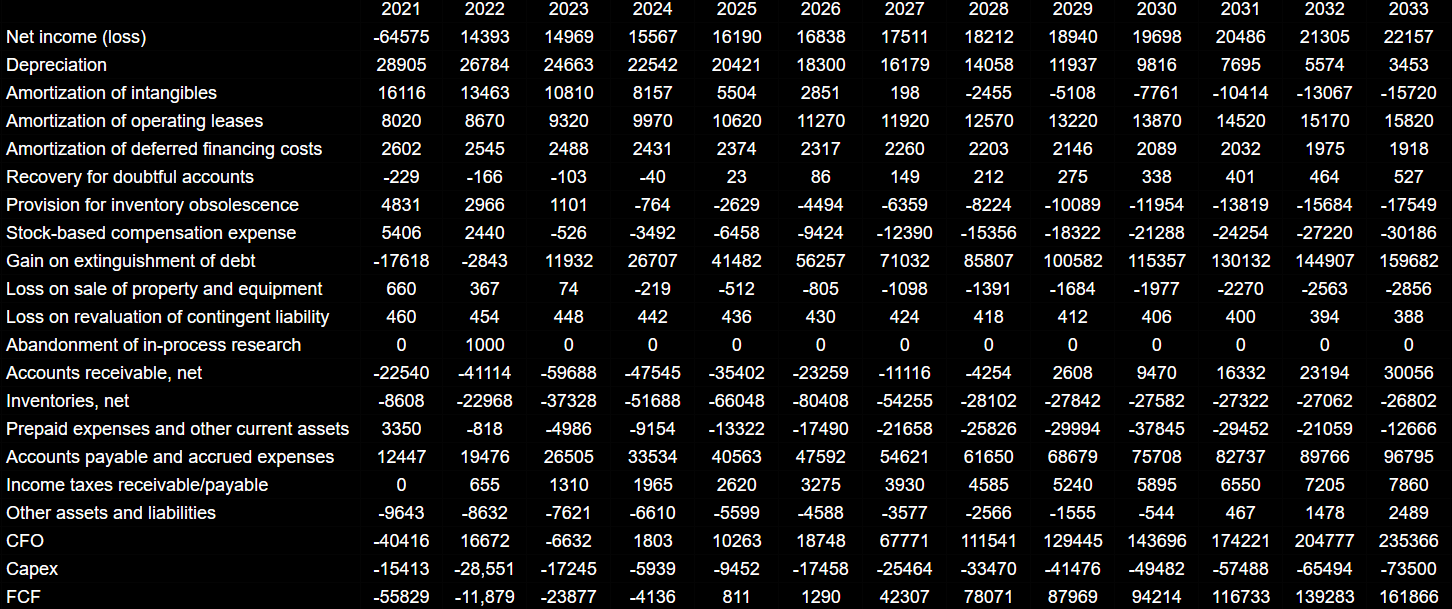

My financial model includes 2033 net income worth $22 million, 2033 depreciation of $3 million, and amortization of intangibles close to -$16 million. Besides, with amortization of operating leases worth $15 million, provision for inventory obsolescence worth -$18 million, and stock-based compensation expenses of -$31 million, I also included changes in accounts receivable of $30 million.

Additionally, I assumed changes in inventories of $-27 million, prepaid expenses and other current assets close to -$13 million, and changes in accounts payable and accrued expenses worth $96 million. Finally, with 2033 CFO of about $235 million and capex of about -$74 million, I obtained 2033 FCF close to $161 million.

{kind=link}

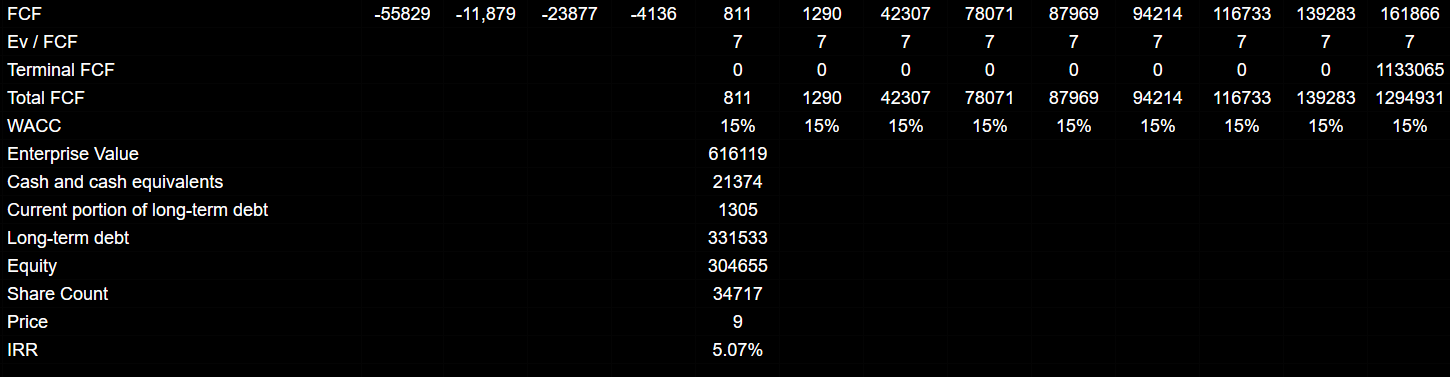

If we assume a conservative EV/FCF of close to 7x and a WACC of 15%, the implied enterprise value would be $616 million. The EV/EBITDA stands at close to 4x, but the figure stood at close to 45x a few months ago. I believe that my EV/FCF is quite conservative.

Source: Ycharts

With respect to the cost of capital used, I believe that my figure is also quite conservative. Let's note that the 2028 notes offered by Nine include an interest rate of close to 13%.

On January 30, 2023, we, and certain of our subsidiaries entered into an indenture, dated as of January 30, 2023 (the “2028 Notes Indenture”), with U.S. Bank Trust Company, National Association, as the trustee and as notes collateral agent, pursuant to which the 2028 Notes, which form a part of the Units, were issued. The 2028 Notes will mature on February 1, 2028 and bear interest at an annual rate of 13.000% payable in cash semi-annually in arrears on each of February 1 and August 1, commencing August 1, 2023. Source: 10-K

Adding cash and cash equivalents worth $21 million, current portion of long-term debt of close to $1 million, and long-term debt worth $331 million, the implied equity would be $304 million, and the fair price would stand at $8.77 per share.

{kind=link}

Large Competitors And A Lot Of Competition

Nine competes in the market with the service providers for oil plants in the United States and southern Canada, where there is a presence of large and small companies, including some of the best historically integrated companies in the country.

In some cases, Nine also competes with its clients' own self-development capabilities, particularly when it comes to infrastructure and mining technology. Some of the benchmarks in this market are companies with long recognition and experience such as Halliburton Company ( HAL ), Schlumberger Limited ( SLB ), NCS Multistage Holdings ( NCSM ), NexTier Oilfield Solutions ( NEX ), KLX Energy Services Holdings ( KLXE ), and Innovex.

Due to the nature of the market, contracts are made based on offers from the companies that provide services, generating a high level of competition. Within this framework, I believe that Nine is superior to many peers because of its great rate of effectiveness in technological advancements.

Risks

With regard to risks, first of all we may distinguish that all of the activities of this company depend on the activity of the oil industry in the United States. Although the oil industry has remained active and in force since its founding, it usually goes through cyclical moments, reduction of labor capacities, or extraction rates. In this sense, any delay or change in strategy in the disposition of its clients may affect the company's operations. In the same sense, any radical variation in oil prices and financial market activities can directly decrease the company's annual profits. To this point, we can also add that due to the general trends of the new forms of energy extraction and consumption, in the future, a series of measures may fall on the oil industry that restrict or change the internal logic of the market.

On the other hand, Nine reports certain financial complications, such as debt obligations or the possible inability to have sufficient capital flow to maintain active operations. If we relate this factor to future complications for access to credit or forms of financing often given by companies with greater experience and access to resources, we can consider it a relevant element in this reading.

I would add the dependence on certain clients that represent a large percentage of the income of the company. The dependence on the activities of clients that belong to a single item and the indirect dependence on the risk rates of its clients represent the risk factors that have to be taken into account to read a future outlook of the company's operations.

Conclusion

Nine Energy Service recently received close to $300 million in a combination of debt and equity, which proves that many debt and equity investors are interested in the business model. I believe that the technological advantages that offer the dissolvable plugs, the geographic diversification of the services provided, and relationships with large customers will likely offer stable FCF generation in the future. I see some risks from the total amount of debt, the actions of large competitors, or a decrease in the oil price, however the stock price appears undervalued.

For further details see:

Nine Energy Service: Successfully Refinanced Its Debt, And Trades Undervalued