NTDOF - Nintendo: Bullish On Gaming

2023-03-10 06:15:40 ET

Summary

- Nintendo is an international gaming company, known for such games as Pokémon and Mario.

- The company has had a wild ride in recent years with the release of the Switch and COVID-19-driven sales. Things have somewhat calmed down since then, but look healthy.

- The future still looks bright with Nintendo positioned well to grow due to quality of its IP. Pressure comes from continuing to develop quality games.

- Nintendo's financial profile is very attractive and superior in the market but lacks the growth of its peers.

- Nintendo's relative valuation is very attractive, trading at a 56% discount to its peers.

Company Description

Nintendo Co Ltd. ( NTDOY / NTDOF ) develops , manufactures, and sells home entertainment products internationally. It offers video game platforms, playing cards, Karuta, and handheld and home console hardware systems, alongside related software and goods. The company was founded in 1889 and is headquartered in Kyoto, Japan. They are listed in the Tokyo and Osaka exchanges.

Nintendo captured generations of people with game titles such as Pokémon, Mario Bros, Tetris, Super Smash Bros., Legend of Zelda, and Animal Crossing. Just these titles alone have sold over 1.2 billion copies . Alongside this, Nintendo has some of the most successful consoles in the world, including the Wii, Switch, and Nintendo 64 .

We have previously covered Embracer ( THQQF ) in the gaming space, which can be found here .

Nintendo's stock has performed well over 10 years, gaining 200% and having only two down years. Since its peak in late 2021, the stock has fallen c.30%, as market conditions have weakened, and demand has slowed.

With somewhat stabilization in the share price, now is a good time to consider the quality of the business relative to its share price. We will look at the gaming industry in conjunction with the macro conditions, as well as assess the financial quality of the business.

Macroeconomic Conditions

Economic conditions reflect the health of an economy and are a measure of demand. Demand very quickly increased after the onset of COVID-19 lockdowns as income support was provided across many nations. This began to slow in early 2022.

The reason for the slowdown can be attributed for the most part to inflation. Inflation remains above 5% in both the US and Eurozone , having reached the 10% region in 2022. The reason for the rise in inflation is attributed to many factors including money printing during the lockdowns, a decade of record-low interest rates, and the Russian invasion of Ukraine. The economic response has been in the form of increased interest rates, where possible, to cool demand. As inflation rates currently show, this has yet to be successful. This has led to a cost-of-living crisis for many consumers, who face rising prices and increased borrowing costs. With consumers tightening their wallets, less expenditure has been available for discretionary spending on such things as gaming.

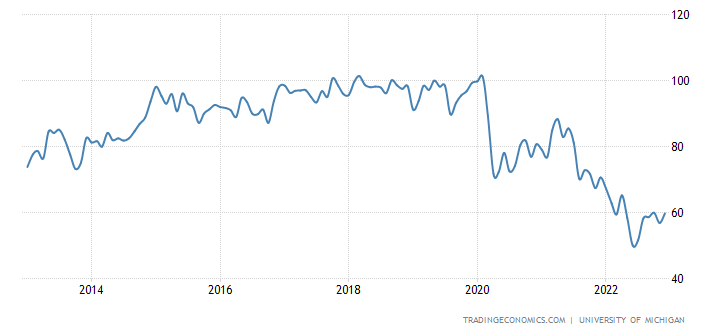

With conditions as they are in early 2023, we will likely experience much of the same. Things will only reverse once inflation returns to a sustainable level. Consumer sentiment has fallen significantly and looks to continue. Much of this outlook is based on consumers' views on inflation, and how this is affecting their finances.

Consumer sentiment (Trading Economics)

{kind=link}

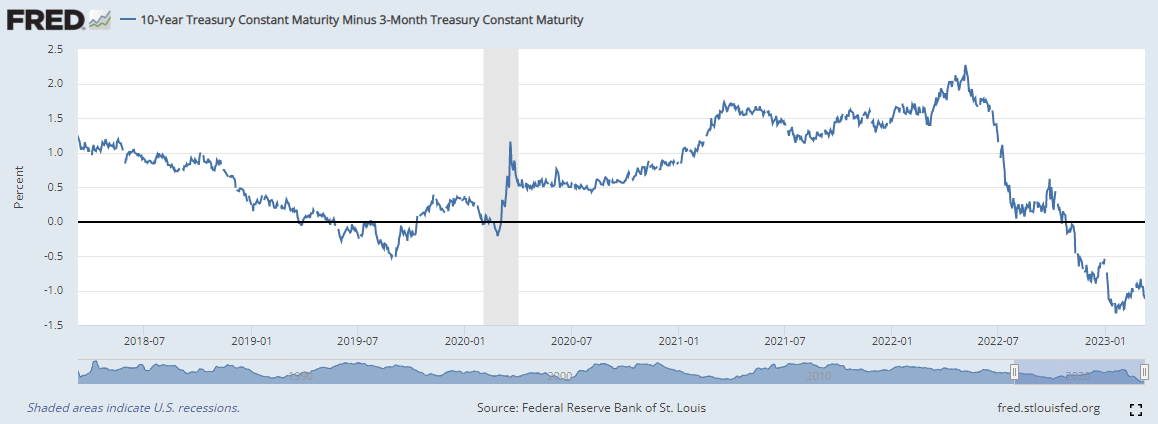

Further, the 10-year minus 3-month yield curve has inverted for the first time. This yield curve has historically inverted before an imminent recession. The level of inversion is concerning.

{kind=link}

The gaming industry requires consumers to have a healthy level of discretionary income, as the cost of entry (console purchase) can represent a material expenditure. That said, the industry is not hit as significantly as others due to the ongoing cost to consumers (buying games) being a small expense relative to income.

Gaming Industry

The current state of play and outlook:

An interesting dynamic observed during COVID-19 is that many consumers brought forward demand / changed spending habits due to lockdowns. The gaming industry saw record levels of growth from 2020 into 2021 . As an example, it was very difficult to get a Nintendo Switch during lockdown in the UK as many rediscovered their love of gaming in the boredom of the lockdowns. Being locked in at home with extra discretionary income in hindsight was the perfect situation for growth in gaming.

There is an argument to suggest that growth will now slow into the future for two reasons. Firstly, demand was brought forward on such things as console purchases which won't be replicated. Secondly, with lockdowns ending, people are returning to old habits and not continuing to game at the level they are. The evidence does not support this, however. PwC is forecasting the industry to continue strong growth, driven by casual gaming . The nuance here is the legacy of COVID-19. Many found gaming to help with their mental health, helping with relieving stress. Further, the switch towards working from home means greater free time and easier ability to socially game. This does not mean Nintendo's growth will necessarily continue to be positive during the economic conditions we are experiencing, but more so that the industry remains healthy. Casuals are not discarding gaming and will remain a part of their life going forward.

Prices:

One potential stumbling block identified is the rising cost of games. Although anecdotal, for most of my life, new AAA games were £40 in the UK. Very quickly, things have changed with games for as much as £80. Not only this, but many come with in-game purchases which could mean spending multiple times your initial purchase. G2A's CEO believes this could price out many people from the industry, as consumers are more careful with the number of games they purchase. Although Switch games are not at the top-end, they are still quite pricy for what are handheld games.

{kind=link}

Handheld/mobile gaming:

Handheld and mobile gaming has seen a rise in the last few years, as consumers look for more convenient and flexible sources of gaming, without compromising on the quality of the games relative to consoles. Further, technological innovation has only recently reached a level where this is possible to do in a functional form. Steam released the Steam Deck, Nintendo has the Switch and of course, we have iPhone and Android games. Although these are all aimed at different people, the growth in all has outperformed . This will only continue as computing power increases and better games can be played. The downside to owning a handheld console is very little as the cost-to-usage ratio is very good and it is not mutually exclusive with a console/PC. Nintendo has positioned itself perfectly here, with the potential to innovate the Switch every 5-10 years to keep up with market evolution. Microsoft recently announced they would bring Call of Duty to the Switch .

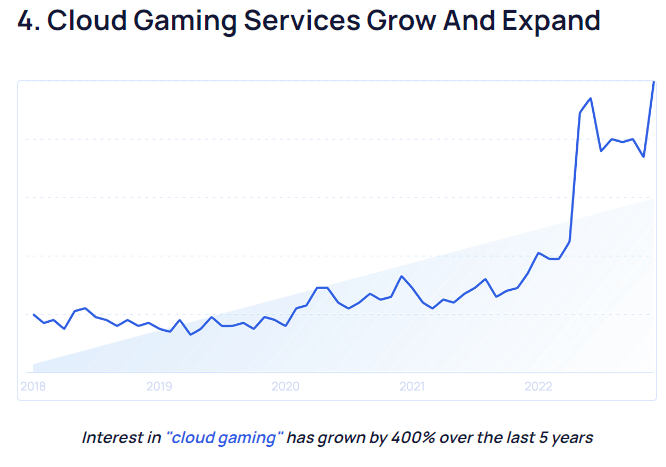

Cloud gaming:

Another theme in the gaming industry is cloud gaming. This is the process of "streaming" a game to your device and is a recent innovation. Why would you want to do this?

- You do not need to own the game

- You do not need to download the game

- You can play a lot more games with ease.

Xbox game pass, the most developed cloud gaming model, has been a huge success. This is still in its early stages relative to the traditional buy-and-own model, but consumers are enjoying the system and the growth is impressive.

Cloud gaming interest (Exploring Topics)

{kind=link}

Nintendo is still in its infancy here, but the company has a large back catalog of games and access to 3rd parties. This is still an area of growth and opportunity for the business.

Reboots, rereleases, remakes, and sequels:

One cannot assess the gaming industry without assessing the games themselves, you are only as successful as how popular your games are. Just like the entertainment industry, IP is king. Gaming has seen strong growth come from a handful of IPs, such as Pokémon and Call of Duty. For this reason, publishers are very quick to choose one of the 4 options in the sub-header before developing new ideas. Although consumers may desire new games, they vote with their wallets and people are still hungry for established IPs. Nintendo is a classic example of this, the company has a handful of wildly successful IPs which it has successfully monetized and developed over several decades. One way they have done this is by keeping their IP in-house, you will never see their games on Xbox or PS ( MSFT / SONY ). With Nintendo's extensive IP, we can only see success in the future with its gaming offering, although a gradual development of new ideas is preferable.

Overall, the gaming industry looks healthy, and we believe that sustainable growth will continue. Nintendo is positioned extremely well to benefit from this, having a good blend of historical competitive advantage and opportunities for growth through innovation.

Financials:

Nintendo - Financial analysis (Tikr Terminal)

{kind=link}

Nintendo's financial performance during the last six years has been extremely good. Revenue has grown at a CAGR of 23%, and over 100% in FY17. The driving force of this was the release of the Nintendo Switch in early 2017, which was a highly successful console release. Even in 2022, the Switch was the highest-selling console in the UK . The console has yet to reach its maturity and so the scope for further growth is possible, however, the early stages of 10%+ growth are unlikely.

Operational efficiencies have allowed the business to improve its margin at an impressive rate. GPM has grown 14% and NI 6%. Much of this has come from scale economies, as production has increased.

The impact of this has been an increase in inventory held during the period. Inventory turnover has fallen, causing their cash conversion cycle to increase. Given that buying and holding greater inventory has likely improved margins through the ability to service demand and avoid supply-chain issues, this operational downside is worth the cost. The business is flush with cash, and we see zero reasons to suggest inventory would ever be discounted and so holding more will not cause any problems.

Investors are directly rewarded for this profitability, their FCF is a mammoth 15%, accruing cash while funding dividends and buybacks. Importantly, we would like to see this reinvested into R&D and IP development. Nintendo does not have the financial might of Microsoft or Sony and so has to be ahead of the game and invest effectively.

We must remember that Nintendo is a 1 console brand with fewer resources than Sony and Xbox. I highlight this as Nintendo reached revenues of JPY1,838.62BN in 2009, over 10 years ago. Between 2010 - 2017 the company's revenue declined astronomically to 489BN JPY. The reason for this was the lack of follow-up / innovation to prior products. It is not out of the question that history will repeat itself in the future. If we look at 3 key periods during Nintendo's history, we see the following:

- '06-'10 - Growth was high but R&D expenditure was only 2-4% of revenue.

- '10-'17 - Growth was negative but R&D expenditure was 5-12% of revenue.

- '17-'LTM - Grow was high and R&D expenditure was 6% of revenue throughout.

We could be looking too deeply into this and the increase in R&D % is purely due to revenue falling but greater R&D expenditure seems to contribute to future revenue growth. For this reason, we would be keen to see if this 6% increases to 8-10% before sales begin stagnating.

Peer comparison

Peer group analysis (Tikr Terminal)

{kind=link}

An early observation of Nintendo and its peers is that the gaming industry is extremely lucrative. Everyone is very profitable, and the growth has been double digits. From a profitability perspective, Nintendo has the best metrics, only Activision Blizzard ( ATVI ) has better FCF, but an inferior EBITDA.

Nintendo has achieved consistent growth in line with the market but at a superior ROE. A notable weakness is the inferior analyst forecast growth. The reason for this is Nintendo's relative position in the market. It is not fast-moving or acquisitive, and is further down the company life cycle, relative to the majority of the businesses in this list. For this reason, Nintendo will move less quickly but will find itself with bursts of heightened growth.

With no debt, Nintendo faces no insolvency risk, although all industry participants are prudently leveraged.

Valuation

As established, investors receive superior profitability but may forego greater growth. In the console production life cycle observed previously with Nintendo, I believe it is fair to expect sub-10% growth in the coming 5 years. Generally, faster-growing businesses receive a premium, especially if profitable.

Nintendo is noticeably cheaper than its peer group, even when you consider growth. On an EV/EBITDA level, Nintendo is trading at a 56% discount while paying a greater dividend.

We believe that Nintendo should trade at a discount due to the lack of growth potential but 31% FCF for 8x is very attractive regardless of the business. Even if Nintendo was to see its multiple expand toward EA/Sq. Enix, similarly mature businesses, it would suggest substantial upside.

Peer group valuation (Tikr Terminal)

Conclusion

Nintendo is a household name for many generations, producing some of the most beloved entertainment the world has seen. The business has seen a renaissance in the last few years and is now in a great position. Profitability is high and growth looks to remain sustainable. Looking at the gaming industry and macro conditions, some weakness may be felt but the general trends and themes look positive for Nintendo long-term, which is the timeline investors should have with this stock.

We thus rate Nintendo a buy.

For further details see:

Nintendo: Bullish On Gaming