NTDOF - Nintendo Is A Classic GARP Investment At 14.3x TTM P/E

2023-10-25 04:31:27 ET

Summary

- Nintendo's shares are down 16% from their 52-week highs, but the company continues to report strong sales growth and a growing user base.

- Q1 results show a 50% increase in sales, driven by the Super Mario Bros. Movie, Zelda: Tears of the Kingdom, and higher-priced Nintendo Switch OLED Model sales.

- Nintendo looks like a great GARP investment with forward earnings yields and historical free cash flows, both around 5.5%, along with 5-year revenue growth rates averaging 10.2%.

- The company has a conservative financial structure with little debt and a large cash reserve, representing 27% of its market cap.

Shares of Nintendo ( NTDOY ) have my attention down 16% from 52-week highs and are trading at a TTM P/E of 14.3x with great growth. The company continues to report great results in the latest quarter with sales up 50% driven by the latest release of the latest Zelda game, the Super Mario Bros. Movie, and the annual active user base growing to 116 million (+10.5%) from the prior year. These sales are the latest success in Nintendo's strong results throughout COVID which saw the user base more than double from 2019 to 2021.

Conservative in nature like many other Japanese companies with little to no debt, Nintendo also has a record ¥1.9 trillion of cash and equivalents on the balance sheet representing 27% of Nintendo's ¥7.1 trillion market cap. The company is highly profitable and I look forward to the excess cash and profits slowly being paid out at higher rates in the years to come.

Latest Quarterly Results

In Nintendo's latest Q1 FY 2024 results for the quarter ended June 30th, the company reported sales of ¥461.3 billion which was up 50% YoY. The increase was driven by the Nintendo Switch ? OLED Model, which has a higher unit price, in addition to overall higher unit sales for hardware and software with the notable release of The Legend of Zelda: Tears of the Kingdom which sold 18.51 million units in the quarter. In the mobile and IP-related business, overall sales rose by 190.1% year-on-year to ¥31.8 billion, bolstered by an increase in income from royalties and income from visual content related to The Super Mario Bros. Movie.

With operating margins improving from +7.1% to 40.2%, operating profit increased a whopping 82.4% to ¥185.4 billion. SG&A expenses saw a 15.3% rise to ¥95.6 billion in the inflationary environment. Net income increased 52.1% to ¥185.4 billion with profit margins up 0.5% to 39.2%.

Q1 Highlights (from Nintendo quarterly earnings release)

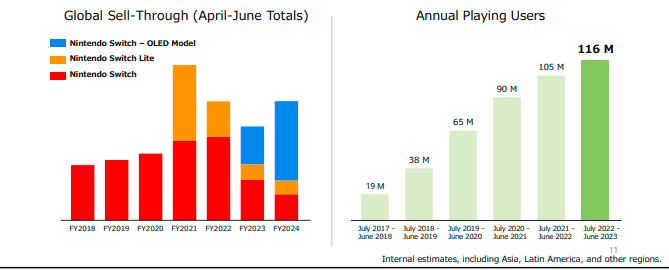

The annual playing user base for Nintendo Switch continues to grow and is now 116 million in the TTM up 11 million (+10.5%) from 105 million users in the prior year. The new OLED model of the Nintendo Switch continues to drive sales of the next iteration of the company's current gaming platform. COVID was great for gaming console sales with the user base growing by 27 million (+71%) in the year ended June 2020 and has slowed in recent years but is still growing nicely. The active 116 million user base should continue to drive sales of software games in the coming years and is a great customer base for the next generation of this classic company.

Growing User Base at Nintendo (from Nintendo quarterly earnings release)

{kind=link}

For the full year, management is conservatively guiding for net profit of ¥340 billion, down 21.4% which is being driven by a 9.5% decrease in sales. Management expects mid-teen unit sales volume to drop both in hardware and software as can be seen in the table below. Dividends are forecast to be ¥147 per share. Remember, for non-Japanese investors 1 NTDOY ADR represents one-eighth of a Nintendo share, while one NTDOF ADR equals one share of Nintendo. At the current $1 USD to ¥ 0.0067 conversion, this guidance would imply forward earnings yield around 5.54% and dividend yield of 2.40%.

Profitable and Growing

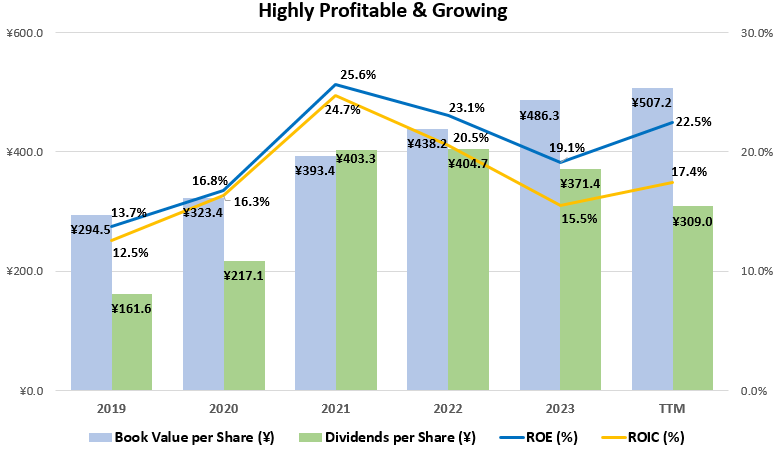

Nintendo's brand, character portfolio, and slim operations have allowed it to achieve an average return on equity and return on invested capital of 20.1% and 17.8%, respectively, over the past decade. The close proximity between ROE and ROIC is due to the conservative leverage being employed by the company. This type of conservative financial structure can be common among Japanese firms which has its positives in lower volatility and business risk but also obvious drawbacks in the lower leveraged equity returns. While less leveraged than I would like, this level of profitability is well above my rule of thumb of 15% ROE and 9% ROIC, allowing me to be confident that, in my opinion, the company is able to maintain and continue to increase its intrinsic value over a business cycle.

Historical Profits and Growth at Nintendo (compiled by author from company financials)

{kind=link}

On the growth side, revenues per share have grown by 10.2% annualized over the past five years with EPS up a solid 25.5% and dividends per share up 16.5%. This great growth is due to the continued growth in the annual playing users to 116 million as highlighted in the quarterly results. COVID was great for the company as more users returned to gaming and that should help support the user base and software sales for years. Let's analyze the potential for increased dividends more by looking at the cash flows.

Growth per Share at Nintendo (compiled by author from company financials)

Great Excess Cash Flow

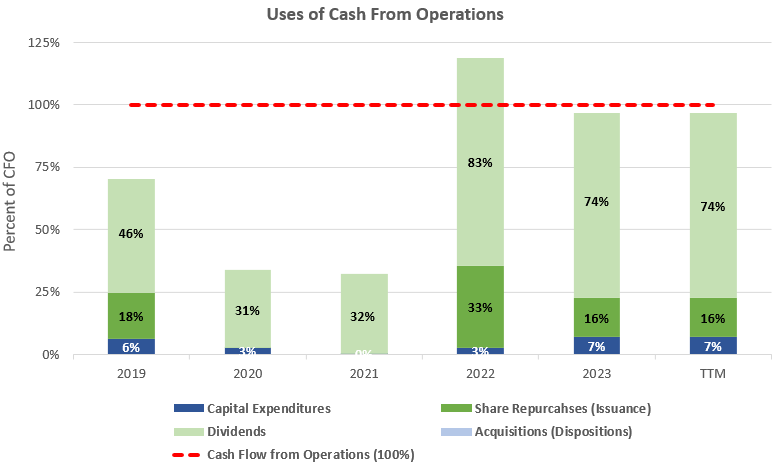

Strong businesses with global brands such as Nintendo are able to generate cash beyond what is needed to fund operations. With capital expenditures taking up an average 4% of cash flow from operations since 2019, this leaves approximately 96% to be returned to investors in the form of dividends and share repurchases. This is probably one of the best FCF rates I have seen at any company.

Cash Flow Analysis of Nintendo (compiled by author from company financials)

{kind=link}

With average cash flow from operations of ¥408.2 billion over the past three years, this 96% would imply free cash flow to shareholders of ¥392.5 million for around a 5.5% free cash flow yield at the current ¥7,105 billion market capitalization. For investors of the USD ADRs, Nintendo's market capitalization was $47.5 billion as of the writing of this article with the exchange rate at $1 USD equals 149.69 Japanese Yen. While this might not seem like a high yield by itself, adding the historic 5-year revenue growth of 10.2% would take this yield well above my target 9% rate.

How About The Debt? What Debt?

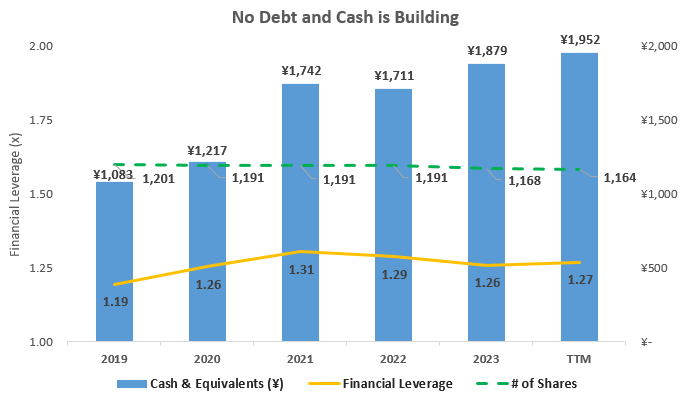

Financial leverage at Nintendo remains negligible but has crept up in recent years moving from lows of 1.19x in 2019 to 1.27x in the latest quarter. With ¥1,952 billion of cash and equivalents on the balance sheet as of the latest quarter-end, the company earned interest. I would personally like to see the company apply more debt in the capital structure, but I do not think will happen quickly any time soon at this conservative Japanese company. The ¥1.9 trillion of cash and equivalents on the balance sheet has grown steadily from ¥1.1 trillion in 2019 and is just begging to be paid to investors, this cash represents around 27% of Nintendo's ¥7.1 trillion market cap.

Capital Structure Highlights at Nintendo (compiled by author from company financials)

{kind=link}

Getting in line with North American competitors, Nintendo has also slowly started to return cash to shareholders in the form of share repurchases in addition to their dividend. Since its 2019 fiscal year, the company has bought back on average 3.1% of its outstanding shares each year (0.72% annualized), as can be seen in the graph above. Adding these share repurchases on top of the forward 2.40% dividend yield would imply a total shareholder yield around 3.1%.

Takeaway for Investors

Shares of Nintendo are looking like a great growth at a reasonable price investment down 16% from 52-week highs and trading with forward earnings yields and historical free cash flows both around 5.5%. The company continues to report great results with Q1 sales of ¥461.3 billion being up 50% YoY driven by Nintendo's blockbuster Zelda franchise release and Super Mario Bros. Movie. Nintendo remains a relevant classic brand for the casual gamer and the growing annual active user base supports the ongoing relevance of the company, its games, and its characters (some of which may even end up getting their own movies!).

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Nintendo Is A Classic GARP Investment At 14.3x TTM P/E