NTDOY - Nintendo: Still Lots Of Valuation Upside

Summary

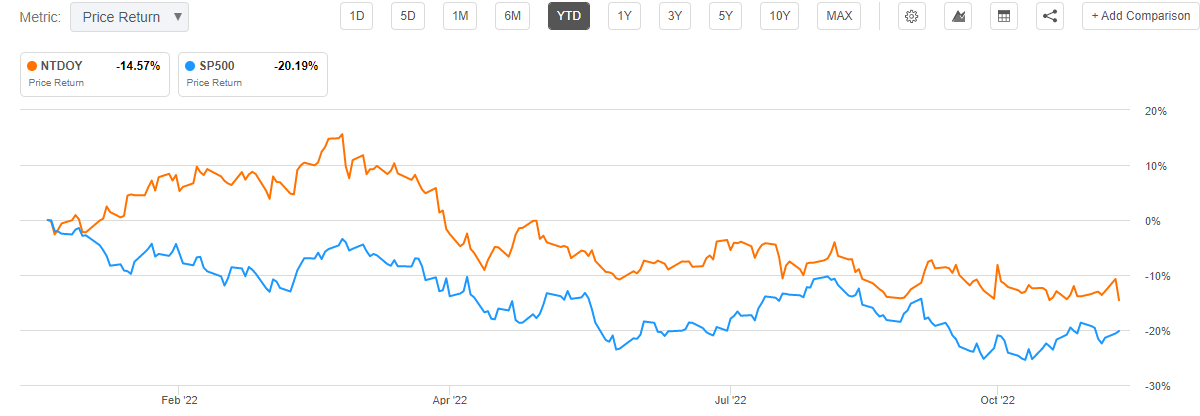

- Nintendo stock fell more than 7% the trading day following the company's September quarter results announcement.

- Although the Kyoto-based gaming company maintained strong profitability, market participants have arguably expected more.

- On one hand, the company managed to increase sales at an attractive rate versus the same period in 2021; on the other hand, operating income remained flat.

- Given a strong brand and IP portfolio, Nintendo remains exceptionally well-positioned to capture value in the gaming industry.

- On the backdrop of EPS updates (slight downward revision through 2025), I now calculate a fair implied share price for NTDOY of $14.45/share.

Nintendo

Nintendo ( NTDOY ) stock fell more than 7% the trading day following the company's September quarter results announcement. Although, the Kyoto-based gaming company maintained strong profitability, market participants have arguably expected more - especially given the strong currency tailwind from a weakening yen. Also the slowing sales numbers for the Nintendo Switch adds to investors' concerns.

Personally, however, I don't think the sharp sell-off is justified. Given a strong brand and IP portfolio, Nintendo remains exceptionally well positioned to capture value in the gaming industry. And valued at an EV/EBIT of about x10, the company is priced like a bargain.

{kind=link}

Nintendo's 1H FY 2023

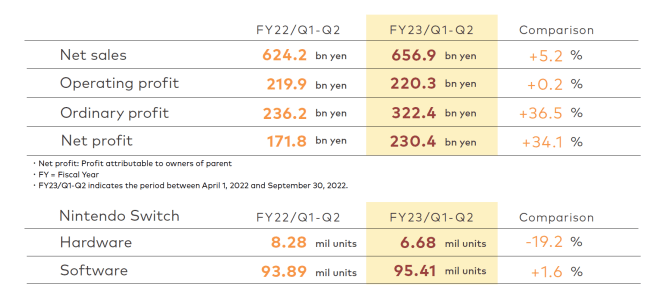

Nintendo delivered a mixed first half of FY 2023 . On one hand, the company managed to increase sales at an attractive rate versus the same period in 2021, but on the other hand, operating income remained flat.

From April to end of September, Nintendo generated total revenues of 656.9 billion yen, which compares to 624.2 billion yen for the same period one year earlier (5.2% year over year growth). The topline was impacted positively by software sales volume (up 1.6%), while hardware sales volume declined by about 19.2% - as Nintendo struggled to sell as many Switch consoles as in the same period of 2021.

Switch Consoles Sales Slowed

Nintendo Investor Presentation

{kind=link}

Although Nintendo said that Switch sales were still constraint by a 'chip-shortage' and the company has working hard to front-load production in order to meet end-of-year demand, I doubt that there is no structural challenge in the Switch's attractiveness for gamers and/or market saturation - given that the Switch console is already five years old.

Profitability Disappoints

Nintendo's operating income in 1H FY 2023 remained flat versus the same period for FY 2022. Although the failure to increase operating income in line with sales might be due to the production 'front-loading', investors should consider that the lack of 'currency leverage is most definitely disappointing (Nintendo is expensing costs almost exclusively in Japan (weakening currency), but selling internationally (strengthening currency).

For 1H FY 2023 Nintendo generated operating income of 220.3 billion yen and a net profit attributable to shareholders of 230.4 billion yen.

Nintendo investor presentation

{kind=link}

Guidance

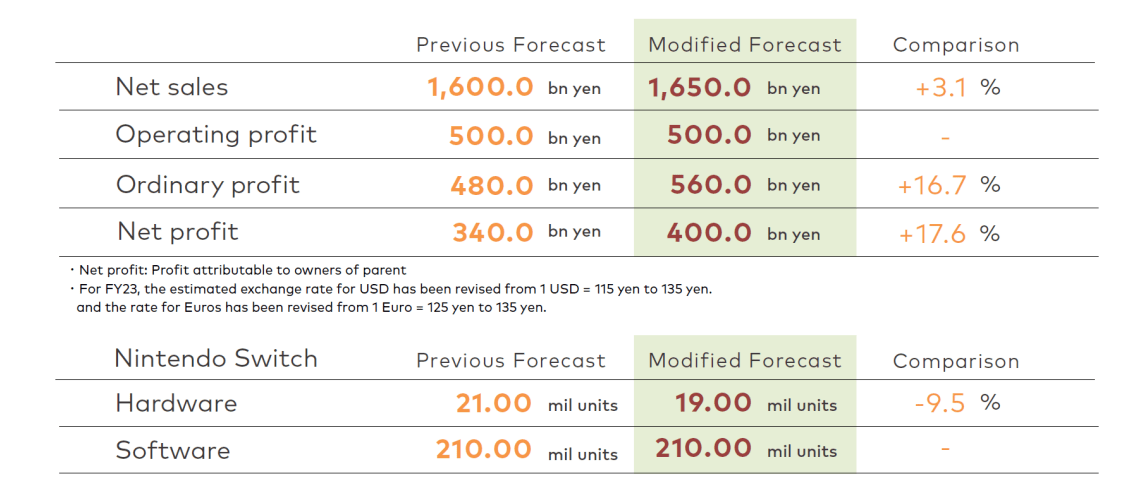

Nintendo increased its guidance for the FY 2023. The company now expects to generate total sales of 1.65 billion yen (versus 1.6 billion yen previously) and net profit of about 400 billion yen (versus 340 billion yen). However, it is disappointing to learn that the improved guidance is almost exclusively carried by a FX tailwind, not by product strength.

In fact, Nintendo decreased expectations for FY 2023 Nintendo Switch sales by 9.5%, to 19 million units (as compared to 21 million units estimated prior). Again, supply-chain challenges should not be the only reason, given that broad consensus agrees that chip shortages in the gaming/tech industry are easing. While I do not necessarily doubt Nintendo's claim that Switch demand remains strong, I most certainly advise to support a healthy dose of skepticism.

Nintendo investor presentation

{kind=link}

Splatoon 3 Topps Expectations

Perhaps the most cheerful news relating to Nintendo's earnings release is related to the super successful launch of Splatoon 3. The company said that the product sold 3.45 million units within the first three days of launch and sold almost 8 million units in September alone. Thus, the Splatoon 3 edition has become Nintendo's fastest-selling game title ever.

Moreover with regards to new games titles, Nintendo is expected to launch Pokémon Scarlet and Pokémon Violet in November 18, a combination that I believe could cumulatively generate as much as 20 million sales by year-end if previous Pokémon game titles could serve as a reference.

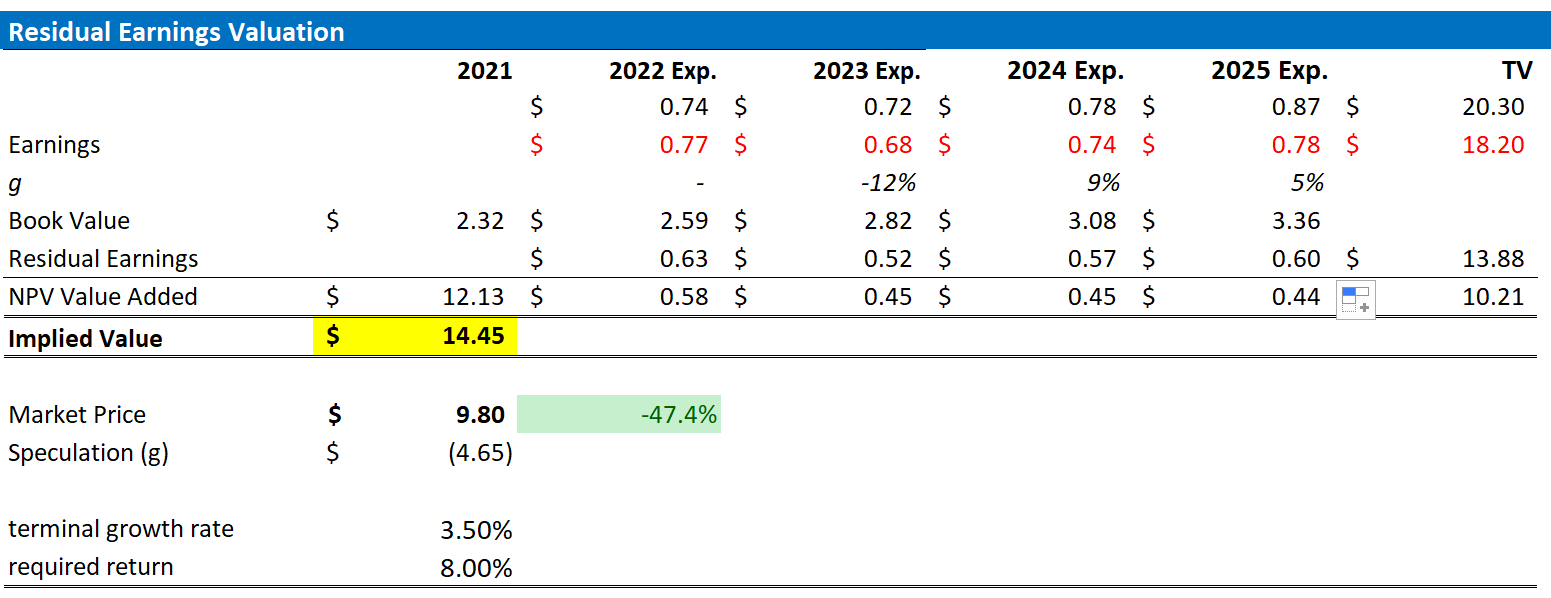

Valuation: Update

trading at an EV/EBIT of about x10, NTDOY stock is priced cheap and I continue to see material upside. However, reflecting on a challenging demand environment for the Switch platform - and given that there is no news on a new console as of November 2022 - I revise my EPS estimates for Nintendo through 2025. However, I continue to anchor on an 8% cost of equity and a 3.5%, terminal growth rate (about one percentage point higher than estimated nominal global GDP growth).

Given the EPS updates as highlighted below, I now calculate a fair implied share price of $14.45.

Analyst Consensus; Author's Calculation

{kind=link}

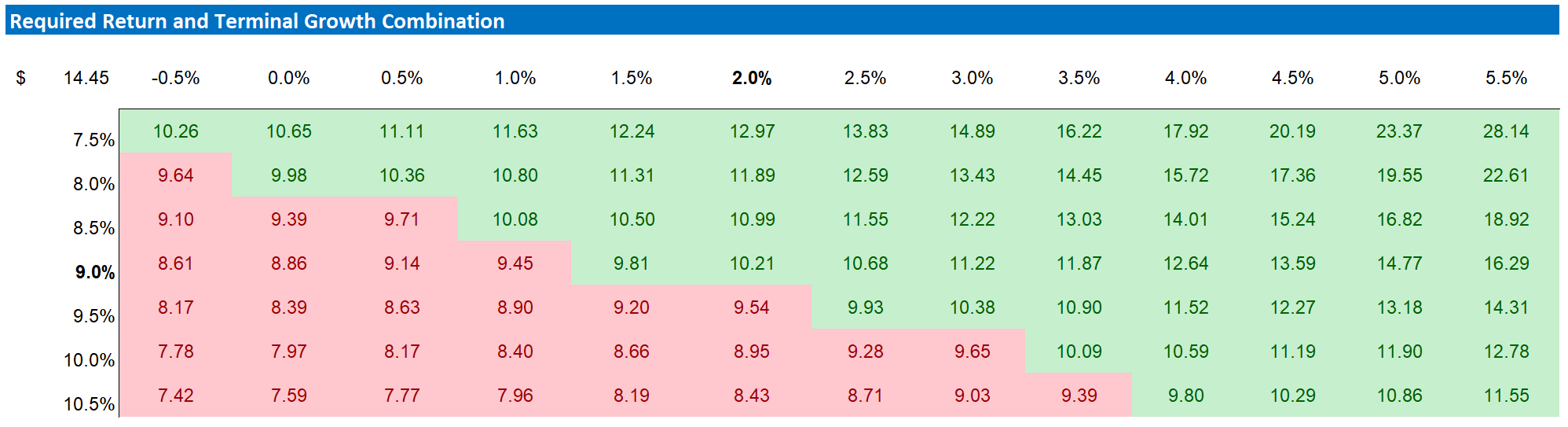

Below is also the updated sensitivity table.

Analyst Consensus; Author's Calculation

{kind=link}

Risks

As I see it, there has been no major risk-updated since I have last covered NTDOY stock. Thus, I would like to highlight what I have written before :

First, a worsening macro-environment could negatively impact Nintendo's business operations. On the demand side: including inflation, rising interest rates and falling asset prices might negatively impact consumer sentiment and entertainment spending. On the supply side: supply-chain challenges such as semiconductor shortage could slow Nintendo's production output. If challenges-both on the demand and supply side-turn out to be more severe and/or last longer than expected, the company's financial outlook should be adjusted accordingly.

Second, while high brand-equity company's such as Nintendo see relatively little impact from direct price competition or competitive cannibalism, Nintendo's competitive positioning and future success is deeply intertwined with the company's ability to successfully innovate and market new products. Nintendo's ability to innovate and launch industry-leading entertainment solutions must further be analyzed in a relative context versus competitors such as Sony and Microsoft.

Conclusion

I continue to be positive Nintendo. Although FY 2023 was slightly less profitable than what investors hoped, and although the Nintendo Switch platform is likely entering late-stage life cycle, I like Nintendo's strong brand and the company's attractive valuation as compared to fundamentals.

On the backdrop of EPS updates (slight downwards revision through 2025), I now calculate a fair implied share price for NTDOY of $14.45/share.

For further details see:

Nintendo: Still Lots Of Valuation Upside