BYDDF - NIO: Improving Risk/Reward (Rating Upgrade)

2023-09-15 13:18:58 ET

Summary

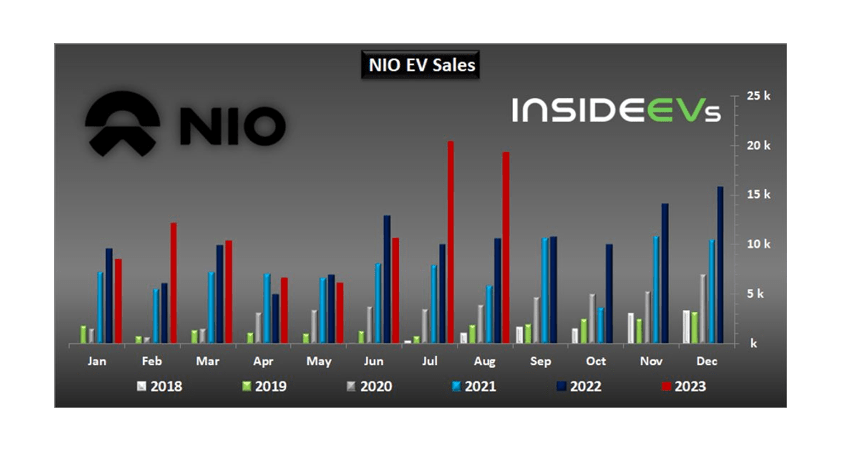

- NIO Inc. is experiencing stronger delivery growth, with an increase of 81% YoY in August 2023.

- The company's delivery rebound is a promising sign that supply chain issues and production delays are improving.

- NIO's profit margins need to significantly improve in order to warrant a higher stock rating.

Electric-vehicle company NIO Inc. ( NIO ) raised some alarm bells in terms of weakening profit margins. But NIO, despite all the concerns that I have had in the past, is seeing stronger delivery growth.

The company is seeing an upsurge in deliveries, with July and August 2023 being particularly successful months, amid a rebound in demand following draconian Covid-19 lock-downs that hurt consumers as much as EV producers.

Though I am happy to admit that the risk/reward has improved for NIO, particularly because 2Q-23 margins showed signs of expansion and deliveries are happening at a faster pace, profit margins need to drastically improve moving forward.

With brighter delivery prospects in 2023 and my price target of $10 being reached, I am now modifying my stock rating to Hold.

My Rating History

I placed a $10 fair value on NIO’s stock back in July 2022 which resulted in a Sell rating. In February 2023, I pointed to growing profit risks for NIO due to falling prices for electric-vehicles, following Tesla’s (TSLA) announcement to lower prices for a number of its models.

Taking into account that NIO has seen a rebound in delivery growth in the last two months and that (vehicle) margins show upside mobility, my stock classification for NIO is now Hold.

I would lift my stock classification to Buy under the condition that the electric-vehicle company is able to turn its profit/margin situation around.

NIO’s Delivery Performance Is Now Improving

NIO delivered 19,329 electric-vehicles in August 2023, representing an increase of 81.0% YoY. It was the second-best month for the electric-vehicle company in 2023 in terms of total deliveries in the current year: Only in July did NIO deliver more electric-vehicles, a total of 20,462.

Though NIO is not breaking down its delivery numbers in terms of models, the company revealed that its five SUVs in the portfolio accounted for 62% of total deliveries in August. The remaining 38% were attributable to the two Sedans in NIO’s growing portfolio, the ET5/ET5T and the ET7.

The rebound in deliveries, particularly over the second quarter, is a promising sign that supply chain issues and production delays are a thing of the past.

{kind=link}

The drop in deliveries at the beginning of the year as well as during the second quarter were primarily due to softening demand for electric-vehicles and some customers delaying purchases in order to take advantage of discounts and lower electric-vehicle prices. The improving delivery picture stands in stark contrast to NIO’s stock price trend since the beginning of August. The loss of investor interest, surprisingly, happened just when NIO said that it anticipates an ongoing recovery of its deliveries: For 3Q-23, NIO expects 55-57K deliveries, which reflects an almost 140% QoQ growth rate.

{kind=link}

Improving Margin Picture As 2Q-23 Showed Upside Momentum On Increased Volumes

Though NIO is seeing an improving delivery trajectory, NIO is facing a new problem that could keep the stock’s upside limited moving forward. Tesla’s price actions , particularly in the first quarter, have resulted in growing profit pressure for NIO, a situation that is not yet resolved.

NIO reported a concerning 1,300 basis point YoY drop in its (vehicle) margins in the first quarter, due to falling prices as well as soft demand.

In the second quarter, however, the margin picture slightly improved: NIO revealed a 2Q-23 (vehicle) margin of 6.2%, reflecting a QoQ improvement of 110 basis points. While the QoQ growth in margins is as promising as it points in the right direction, particularly because it has been achieved at a time of accelerating delivery growth, margins are still low. Thus, NIO’s margins will remain challenged in the short-term as NIO announced a price cut of 30,000 Chinese Yuan (approximately $4,200) as well as a reduction in service levels for new buyers of a NIO electric-vehicle in June. Buyers of an NIO electric-vehicle will no longer receive free battery swapping in the future, making the purchase of an NIO electric-vehicle less appealing to prospective buyers.

Margin compression is a major issue for NIO, particularly since the company is already losing a boatload of money. NIO reported an adjusted net loss of RMB 5.45 billion (US$751.0 million) in the second quarter, reflecting an increase of 140% YoY. NIO’s adjusted net loss adjusts for share-based expenses and losses are unsustainably high.

With that said, NIO’s profit margins will remain under pressure in the short-term and an improvement in the margin picture would get me to consider NIO as a Buy moving forward.

NIO Is Now Probably Fairly Valued

My price target on NIO was $10 and NIO’s stock closed at $10.04 last Friday. NIO is presently selling at a P/S ratio of 2.4x which, in my view, is a fair valuation multiple, particularly given NIO's margin situation.

XPeng Inc. ( XPEV ) and BYD Co. Ltd. ( BYDDF ) sell at 5.1x and 1.2x sales respectively. I will revisit NIO’s upside case in the event that the margin situation improves.

Improved Risk/Reward

NIO’s margins have taken in 2023, due to cut-throat competition in the electric-vehicle market and NIO, during the second quarter, suffered headwinds to its delivery growth.

With that being said, the situation, and therefore the risk/reward ratio, has improved for NIO because NIO’s 2Q-23 (vehicle) margins experienced QoQ expansion and delivery growth rates in July and August were impressive. If NIO can continue on this trajectory and meet its guidance for 3Q-23, then I could finally be warming up to NIO.

My Conclusion

I have been skeptical of NIO in the past because the company was trading at too high a valuation multiple, particularly during the pandemic.

Since NIO is seeing a solid rebound in delivery growth and (vehicle) margins finally saw some uptick momentum in 2Q-23, I am modifying my stock classification to Hold.

If NIO can maintain its current delivery run-rate and improve its (vehicle) margins, I would even be willing to reconsider my Hold classification moving forward.

For further details see:

NIO: Improving Risk/Reward (Rating Upgrade)