NWN - NiSource: A Stable Utility Trading At An Attractive Valuation

2023-09-10 01:31:26 ET

Summary

- NiSource is a regulated electric and natural gas utility serving customers in six states.

- The company's stock price has declined 4.69% over the past six months, but it has outperformed the U.S. Utility Index.

- NiSource has stable cash flows and a growing customer base and plans to invest $15 billion in infrastructure to drive earnings growth.

- The company should be able to hold up much better than most in the event of a recession, although its high debt load is a very real risk.

- The company is trading at an attractive valuation relative to its peers, but an interest rate increase could pressure the stock price.

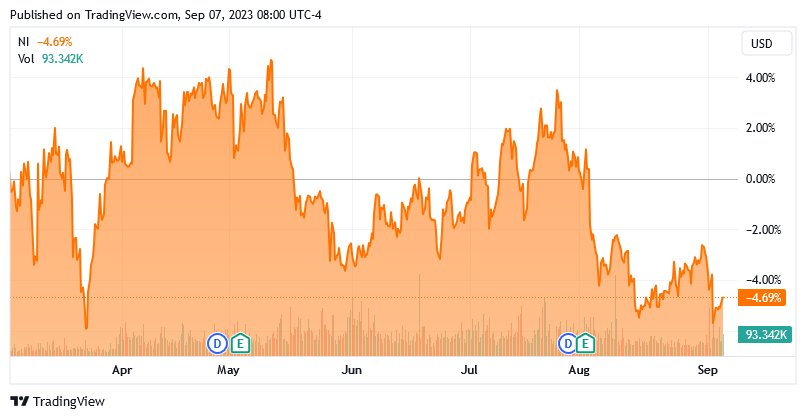

NiSource Inc. (NI) is a regulated electric and natural gas utility that serves customers in six states throughout the Rust Belt and Appalachia. In several recent articles, such as this one , I discussed how utilities such as NiSource could be good holdings for now as there are a growing number of signs that the economy is weakening and could soon fall into a recession. This is due to the general stability of the revenue and cash flows produced by these companies regardless of the conditions in the broader economy. NiSource is certainly no exception to this rule as I discussed in my last article on this company. Unfortunately, the company’s stock price has not exhibited the same amount of stability as it is down 4.69% over the past six months:

{kind=link}

This is not really out of line with the market, however. In fact, the U.S. Utility Index ( IDU ) is down 6.15% over the same period. When we consider that NiSource has a higher dividend yield than the utility index (3.80% compared to 2.73%), the appeal of this company begins to become apparent. After all, an investor in this company would have outperformed the index significantly over the trailing six-month period. When we combine this outperformance with the fact that NiSource has a very attractive valuation today, there could be some reasons to consider an investment in this company today.

About NiSource

As stated in the introduction, NiSource is a regulated electric and natural gas utility that serves customers located in six states throughout the Appalachian and Rust Belt regions. These six states are:

- Kentucky

- Maryland

- Ohio

- Pennsylvania

- Virginia

- Indiana

These are not exactly the states that many investors focus their attention on. Indeed, much of Appalachia and the Rust Belt is considered to be “small town America” with somewhat depressed economies. There are certainly parts of these areas that have seen an economic revival in recent years though, such as Pittsburgh, Pennsylvania transforming itself from an old steel-based manufacturing city to a technology and healthcare hub. However, a good portion of the company’s areas are in regions that have not benefited from the economic growth that has occurred throughout much of the 21 st century.

As mentioned in the introduction, one of the defining characteristics of utilities like NiSource is that they enjoy very stable cash flows over time. We can see this quite clearly by looking at the company’s operating cash flows. Here they are over the past eleven twelve-month periods:

{kind=link}

As we can clearly see, the company’s operating cash flows exhibit very limited variation from one period to the next. I explained the reason for this in my last article on this company:

“The reason for the general stability over time and regardless of broader economic conditions is that NiSource provides a product that is generally considered to be a necessity for daily life. After all, how many people do not have space heating in their homes and businesses? In fact, space heating is generally considered a government requirement for a building to be habitable and the government provides assistance to people that struggle to pay their heating bills. As a result of all of these things, people generally pay their natural gas bills before any other expense and certainly before making any sort of discretionary expenditure. In addition, people typically consume the same amount of natural gas from year to year, which results in even more stability.”

The time period above includes quite a few different macroeconomic conditions. For example, the earliest periods above would include the time period in which the COVID-19 lockdowns were still in effect throughout most of the United States. That was a period of extremely high unemployment that saw many people fall behind on their utility bills. In late November 2020, CNN even quantified this by running a report that about a third of American adults lived in a household that was in danger of falling behind on utility bills due to financial problems that were brought on by the pandemic. Fortunately, the economy quickly recovered once the lockdowns ended, although inflation rapidly took off. Now, we have inflation pressuring the finances of many average people. A recent survey conducted by GOBankingRates suggests that 43.72% of Americans had problems paying at least one of their utility bills over the past year. We can quickly see that none of these economic conditions had any real impact on NiSource’s cash flow. This is exactly the kind of company that you want to be holding in the event of a recession or an economic slowdown. After all, are people really going to risk having their utilities cut off so that they can buy Apple’s ( AAPL ) newest iPhone or go out to a restaurant? The obvious answer to this question is no, which tells us that anything dependent on consumer spending is going to be hurt much more in an economic slowdown than NiSource, which has a proven history of handling economic problems with ease.

Growth Potential

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see any company that we are invested in grow and prosper with the passage of time. Fortunately, NiSource is quite well-positioned to deliver the sort of growth that we desire.

One possible way in which NiSource could deliver growth is by increasing the size of its customer base. The company currently serves approximately 3.3 million natural gas customers and 500,000 electric customers throughout six states. Unfortunately, its service territory does not cover all of a given state so it can be somewhat difficult to do a demographic analysis. However, we do know that the general trend has been positive. In the company’s most recent earnings report , NiSource stated that it had 3.3 million natural gas customers but in its fourth-quarter 2022 earnings report , the company stated that it had 3.2 million natural gas customers. Thus, it appears that the company’s customer base is increasing.

The increasing customer base is generally a positive thing. After all, the more customers that the company has paying their monthly bills, the more revenue it will generate, all else being equal. These higher revenues mean that the company has more money available to cover its expenses and ultimately make its way down to earnings and cash flow. Unfortunately, a growing customer base is not going to be sufficient to give us the sort of growth that investors desire. After all, the fastest-growing state in the nation is only growing at a 1.87% rate:

World Population Review/Data from US Census Bureau

A 1.87% growth rate is not going to satisfy any investor. In the case of NiSource, the company does not even operate in any of the ten most rapidly growing states listed above. Thus, its own customer base is probably going to grow at a smaller rate going forward. As such, it seems highly unlikely that the company will be able to grow its earnings at a rate that will be satisfactory to investors solely by increasing its customer count.

The primary way through which NiSource will generate earnings growth is by increasing the size of its rate base. This is also the method that will allow the company to generate the kind of earnings growth that investors in the company would really like to see. I defined rate base in my previous article on this company:

“A utility’s rate base is the value of its assets upon which regulators allow it to earn a specified rate of return. Since this rate of return is a percentage, any increase in the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way for a company to grow its rate base is by investing money into upgrading, modernizing, or possibly even expanding its utility-grade infrastructure.”

In its most recent earnings conference call, NiSource presented a plan to invest $15 billion into its infrastructure over the 2023 through 2027 period:

{kind=link}

We can quickly see that its planned spending is higher than 2022 levels during most years. This is not unexpected, particularly considering today’s highly inflationary environment. After all, the rising price of things such as steel, labor, and other components required for a natural gas and electric distribution network are getting more expensive with the passage of time. In addition, the company’s depreciation expense will frequently increase over time as it adds more infrastructure to its network. We can see this quite clearly by looking at the company’s income statement:

{kind=link}

As depreciation is constantly reducing the value of the assets that the company has in service that contribute to its rate base, it needs to spend more and more money every year just to keep its rate base stable. Thus, a utility’s spending will almost always increase over time. This is exactly what we see here.

The company’s capital spending plan as detailed above should allow NiSource to increase its rate base at an 8% to 10% compound annual growth rate annually. This should result in roughly 6% to 8% annual growth in the company’s earnings per share. The reason for the lower earnings per share growth relative to the rate base growth is because NiSource will probably have to issue common stock to partially fund its growth program, diluting some of the benefits of the overall earnings growth. This should still result in shareholders getting a 9% to 11% total average annual return when we consider the 3.80% current dividend yield. That is a very respectable total return from a conservative utility stock and it is generally in line with many of the best companies in the sector.

Disappointing Market Return

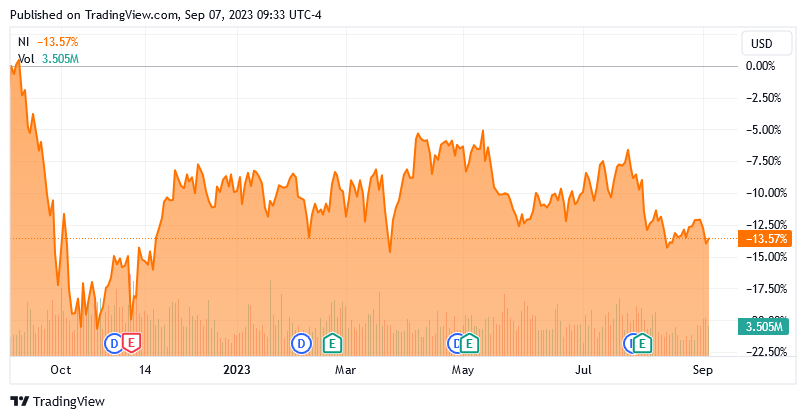

As mentioned earlier in the article, NiSource has delivered a somewhat disappointing return to the stock market when we consider all that the company has going for it. As of the time of writing, the company is down 13.57% over the past year:

{kind=link}

This is much better than the 18.73% decline in the U.S. Utility Index over the same period, but it is still a decline. This decline comes despite the fact that the company’s financial performance was not really all that bad. As we saw above, the company’s operating cash flow in the most recent twelve-month period was actually quite a bit higher than in the equivalent period that ended on June 30, 2022. However, the company’s net income was down over the same period. In the twelve-month period that ended on June 30, 2023, NiSource had a net income of $702.1 million compared to $722.9 million in the equivalent period of the prior year. That is a 2.88% decline, which obviously cannot fully account for the decline that we saw in the stock price. The fact that the U.S. Utility Index was also down over the same period also discounts the theory that this has anything to do with the company’s financial performance.

Unfortunately, it seems that the utility sector is being adversely affected by rising interest rates. Many investors consider utilities to be a relatively safe yield play. After all, the overall financial stability of most utility companies has made them somewhat classic “widows and orphans” investments. The rising interest rates have somewhat reduced the appeal of yield plays in recent months. As of the time of writing, a money market fund pays somewhere around 5%. That is higher than most utilities, including NiSource. In fact, it is higher than the yield of just about any common stock except for some companies in the oil and gas industry or telecommunications sector. That is a very different situation than what we had two years ago. As such, many risk-averse investors that are simply seeking income may opt for the safety of a money market fund or a fixed-income security as opposed to taking on the risk of owning a utility. This has caused the sector to sell off.

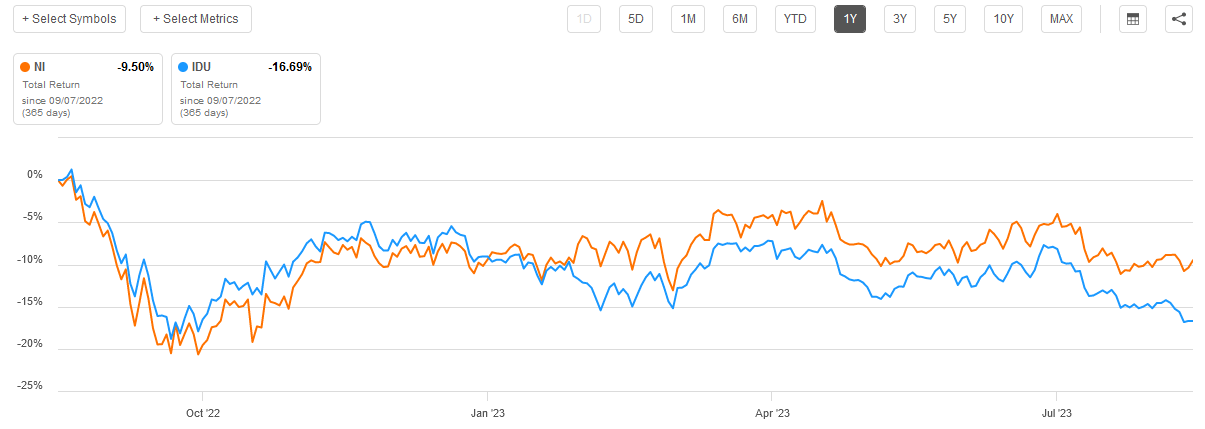

It is nice to see that NiSource has not been as affected by this as the broader utility sector though. In fact, NiSource is substantially outperforming the sector on a total return basis:

{kind=link}

This speaks quite highly of the company and our thesis as outlined above. With that said though, there is a very real possibility that the Federal Reserve will hike rates again in the near future, which could put some further downward pressure on the stock price for the reasons that were just discussed. As such, it might be a good idea to dollar-cost average a position so as to limit the damage from further weakness.

Financial Considerations

As of June 30, 2023, NiSource had a net debt of $12.4708 billion compared to $7.5714 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.65 today, which is unfortunately quite a lot more than the 1.43 ratio that the company had the last time that we discussed it. This could be a concern in today’s interest rate environment considering that we have already seen utility companies have their earnings pressured by rising interest rates and debt servicing costs.

Here is how NiSource’s financial structure compares to its peers:

| Company |

| Net Debt-to-Equity Ratio |

| NiSource Inc. |

| 1.65 |

| Atmos Energy ( ATO ) |

| 0.61 |

| New Jersey Resources ( NJR ) |

| 1.59 |

| Northwest Natural Holding ( NWN ) |

| 1.22 |

| Southwest Gas Holdings ( SWX ) |

| 1.50 |

As we can see, NiSource currently has a significantly higher net debt-to-equity ratio than its fellow natural gas utilities. This suggests that the company may be relying on debt to finance its operations more than it should. That obviously poses a risk to its investors, which should be considered before making an investment in the company.

Dividend Analysis

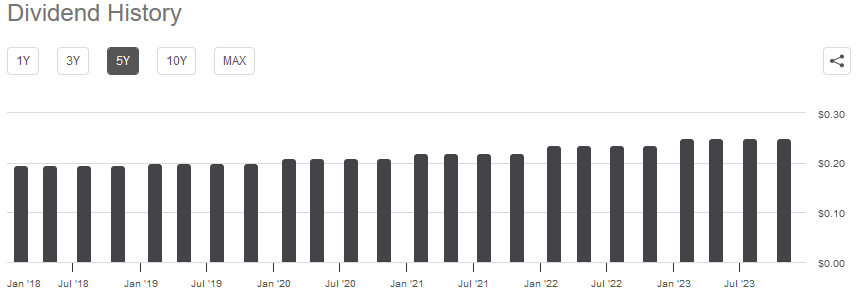

As mentioned earlier, one of the biggest reasons why many investors purchase the common equity of utility companies is because of the very high dividend yields that these companies tend to possess. We can see this quite clearly with NiSource, as the company yields 3.80% at the current price. That is substantially higher than the 1.46% current dividend yield of the S&P 500 Index ( SPY ) as well as the 2.73% current dividend yield of the U.S. Utility Index. In addition to its high yield, NiSource has a long history of increasing its dividend on an annual basis:

{kind=link}

This is something that long-term investors will inevitably like, as the steadily rising dividend will result in the company having a substantially higher yield-on-cost in a few years than it does today. This could even result in the yield that an investor today receives ten years from now being substantially higher than they would receive by putting their money into anything in the fixed-income sector. The rising dividend is also nice because it helps to offset the decline in the company’s purchasing power that an investor would suffer in today’s inflationary environment. This is nice for anyone that is dependent on their portfolios to generate the income that they need to support their lifestyles.

As is always the case, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and almost certainly causes the stock price to decline.

The usual way that we judge a company’s ability to pay its dividends is by looking at its free cash flow. In the twelve-month period that ended on June 30, 2023, NiSource reported a negative leveraged free cash flow of $883.0 million. Obviously, this is not enough to pay any dividends, but the company still paid out $452.6 million over the twelve-month period. Thus, at first glance, it appears that NiSource cannot afford the dividends that it pays out.

However, it is quite common for a utility to finance its capital expenditures through the issuance of debt and equity. The company will then pay its dividends out of operating cash flow. This is done because it is extremely expensive to construct and maintain a utility-scale infrastructure network over a wide geographic area. During the twelve-month period that ended on June 30, 2023, NiSource had an operating cash flow of $1.6932 billion. That is easily enough to cover the $452.6 million that the company pays out in dividends over the same period and leave it a substantial amount of money left over for other purposes. Overall, the company should not have any particular difficulty covering its dividend.

Valuation

According to Zacks Investment Research , NiSource will grow its earnings per share at a 7.00% rate over the next three to five years. This is actually the midpoint of the company’s own guidance based on its rate base growth over the period. As such, this estimate seems to be quite reasonable. This growth rate gives NiSource a price-to-earnings growth ratio of 2.39 at the current stock price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| NiSource Inc. |

| 2.39 |

| Atmos Energy |

| 2.56 |

| New Jersey Resources |

| 2.62 |

| Northwest Natural Holding |

| 3.90 |

| Southwest Gas Holdings |

| 3.57 |

As can be clearly seen here, NiSource looks to be very cheap relative to its peers. This could be partly due to the company’s high debt load, as already mentioned. After all, the company’s high leverage does make it a bit riskier than some of the other companies listed here. The attractive valuation could make up for this, however.

Conclusion

In conclusion, NiSource is a large electric and natural gas utility that has been somewhat punished by the market recently. The reason for this punishment probably has some relation to the rising interest rate environment, which has made it easier to find safe high-yielding investments elsewhere. However, the company’s overall stability could still serve investors very well in the event of a recession. This is especially true for those investors that are focused specifically on the long term, as NiSource’s historical track record of raising its dividend over time will almost certainly result in the stock having a much higher yield-on-cost than most fixed-income assets today if an investor is willing to hold it for a few years. The biggest risk here is that the company is carrying a high level of debt relative to its peers, which could have an adverse impact on its cash flows in a high interest rate environment.

For further details see:

NiSource: A Stable Utility Trading At An Attractive Valuation