ATO - NiSource: Strong Balance Sheet Cash Flow Stability Valuation Make It A Buy

2023-04-26 17:52:17 ET

Summary

- NiSource Inc. is a regulated electric and natural gas utility that primarily serves six states across the Rust Belt and Mid-Atlantic.

- Natural gas utilities like NiSource have a much more promising future than the media wants you to think, as consumers show a marked preference for gas versus electricity.

- The company enjoys remarkably stable cash flows regardless of economic conditions, which could prove attractive if the economy enters a recession.

- The company has a sustainable 3.49% dividend yield and a very strong balance sheet.

- NiSource Inc. is trading at an attractive valuation relative to its peers.

NiSource Inc. ( NI ) is a regulated electric and natural gas utility that serves customers in six states throughout the Rust Belt and Appalachia. Utility companies in general have long been among the favored holdings of more conservative investors, such as retirees, due to their stable cash flows and fairly high dividend yields. However, in recent years, natural gas utilities such as NiSource have lost some of their shine to electric utilities due to the widespread belief that natural gas is on the verge of becoming obsolete as a source of power for space heating and cooking.

As I have explained in many previous articles, this is highly unlikely to be the case, but it has still caused natural gas utilities to trade for much more attractive valuations than their electric brethren. For its part, NiSource certainly appears to trade at a reasonable valuation, and its 3.49% dividend yield compares fairly well to other utilities. This is a similar thesis to the one that I presented back in November, but a few quarters have passed since then so it is a good idea to update our analysis. There may thus be some reasons to consider purchasing shares of NiSource Inc. today, but let us analyze it further to be sure.

About NiSource

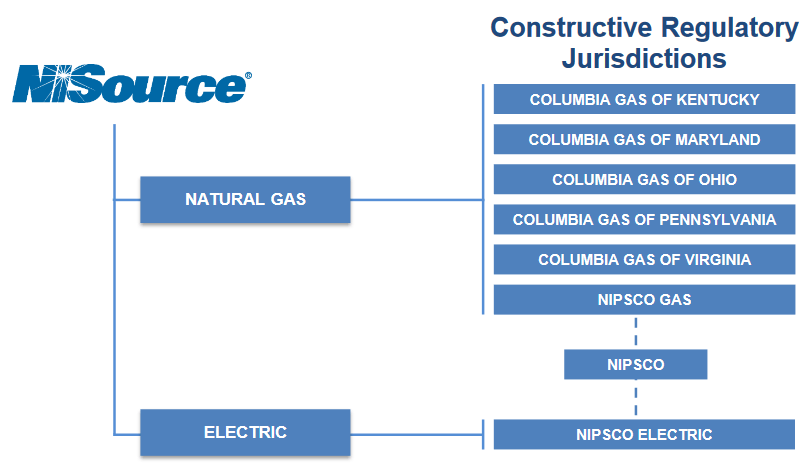

As stated in the introduction, NiSource Inc. is a regulated electric natural gas utility that provides service to customers in Indiana, Kentucky, Maryland, Ohio, Pennsylvania, and Virginia. The majority of this service is provided through the company's Columbia Gas brand name, which only provides natural gas service. The company only provides electric service in the state of Indiana:

{kind=link}

This clearly makes its gas unit much larger than its electric business. In fact, the company is one of the largest natural gas utilities in the United States with 3.2 million customers. It only has a paltry 500,000 electric customers in comparison. This is something that may concern some investors. After all, as mentioned in the introduction, natural gas has the perception of being obsolete and on the verge of being replaced. After all, we have all heard about efforts to convert homes from natural gas to electricity as their primary source of heat. The Consumer Product Safety Commission has also been rumored to be considering a ban on natural gas stoves , which has sparked a political debate.

Consumers seem to be pushing back against the electrification trend, however. As I pointed out in a previous article , homes with natural gas heating systems sell for an average of $50,000 more than the same house with an all-electric system. This may have something to do with the fact that natural gas is considerably more efficient at producing heat than electricity, resulting in it being cheaper to run. Thus, consumers do not seem to be willing to switch from natural gas to electricity anytime soon. Therefore, NiSource's business should be reasonably safe for the foreseeable future.

One of the defining characteristics of utility companies like NiSource is that they enjoy remarkably stable cash flows regardless of economic conditions. We can clearly see this by looking at NiSource's trailing twelve-month cash flows over time. Here they are for each of the past eleven reporting periods:

{kind=link}

It is important to use the twelve-month cash flows when looking at NiSource, as its operating cash flows do tend to vary considerably from quarter to quarter:

{kind=link}

This is because natural gas is primarily consumed as a heating fuel for homes and businesses. As such, it sees much heavier consumption during the colder months than during the summer. When we look at the company's trailing twelve-month figures, the effects of this seasonality are smoothed out. The reason for the general stability over time and regardless of broader economic conditions is that NiSource provides a product that is generally considered to be a necessity for daily life. After all, how many people do not have space heating in their homes and businesses? In fact, space heating is generally considered a government requirement for a building to be considered habitable and the government provides assistance to people that struggle to pay their heating bills. As a result of all of these things, people generally pay their natural gas bills before any other expense and certainly before making any sort of discretionary expenditure. In addition, people typically consume the same amount of natural gas from year to year, which results in even more stability. This allows NiSource to be somewhat of a recession-resistant play that could be appealing today considering all the emerging signs that the United States may descend into a recession in the second half of 2023.

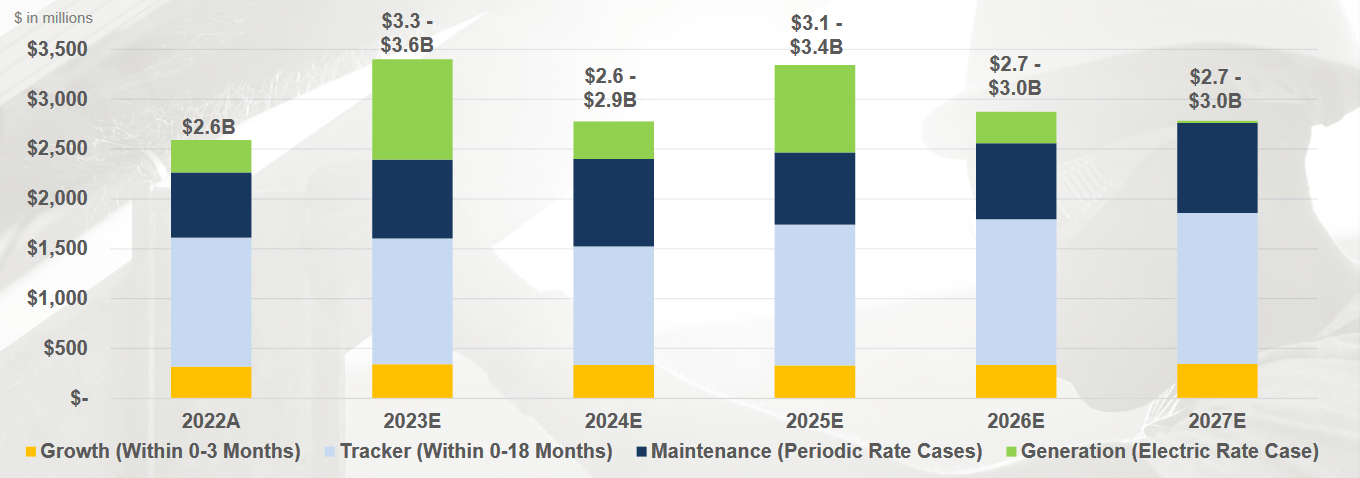

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, we like to see a company in which we are invested grow and prosper. Fortunately, NiSource is positioned to do exactly that. The primary way through which this will be accomplished is rate base growth. A utility's rate base is the value of its assets upon which regulators allow it to earn a specified rate of return. Since this rate of return is a percentage, any increase in the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way for a company to grow its rate base is by investing money into upgrading, modernizing, or possibly expanding its utility-grade infrastructure. NiSource is planning to do exactly this as the company has unveiled a plan to spend $15 billion on this process over the 2023 to 2027 period:

{kind=link}

It is admittedly quite nice to see this sort of visibility. There are some utilities, such as Entergy Corporation ( ETR ), that have only unveiled three-year growth plans. The fact that NiSource is giving us a much longer one gives us a certain degree of visibility and allows us to project a total return over a longer period of time than its peers. In this case, the company's plan as outlined above should allow the company to grow its rate base at an 8% to 10% compound annual growth rate. This should result in earnings per share growth of 6% to 8% over the period.

Undoubtedly, some readers will notice that the company's projected rate base growth is quite a bit higher than its projected earnings per share growth. This is due to financing costs. Basically, NiSource will have to issue some common stock over the period to finance its $15 billion investment program, which will have the effect of diluting some of the earnings growth that its investments will actually create. Overall, though, NiSource Inc. shareholders should still be able to expect a 9% to 11% total return annually on average over the period, which is certainly very reasonable for a conservative utility stock.

Financial Considerations

It is always important to analyze the way that a company finances its operations before investing in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. That can cause a company's interest expenses to rise following the rollover in certain market conditions, which could be especially relevant today as interest rates are currently at the highest level that they have been in more than a decade.

Thus, any company that has to roll over debt today will almost certainly experience rising interest expenses. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes its cash flow to decline could push a company into financial distress if it has too much debt. Although utilities like NiSource typically have remarkably stable cash flows, bankruptcies have occurred in the sector so this is still a risk that we should not ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio essentially tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. In addition, the ratio tells us how well the company's equity will cover its debt obligations in the event of a liquidation or bankruptcy event, which is arguably more important.

As of December 31, 2022, NiSource Inc. had a net debt of $11.3114 billion compared to $7.9018 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 1.43 as of the end of 2022. Here is how that compares to the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| NiSource Inc. |

| 1.43 |

| Atmos Energy ( ATO ) |

| 0.86 |

| New Jersey Resources ( NJR ) |

| 1.76 |

| Northwest Natural Holding ( NWN ) |

| 1.40 |

| Southwest Gas Holdings ( SWX ) |

| 1.87 |

As we can see pretty clearly, NiSource does not appear to have excessive leverage relative to other pure-play natural gas utilities. The company is certainly more indebted than Atmos Energy, but that company is rather unique in the sector as it relies more on equity than debt to finance itself. NiSource is the median company here and so we should not have to worry too much about the risk posed by its debt as it does not appear to be excessively reliant on it.

Dividend Analysis

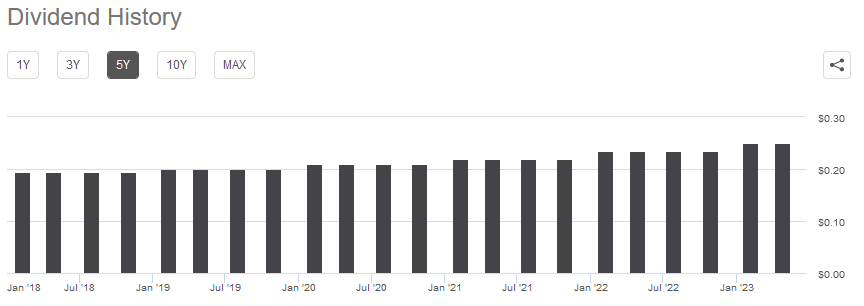

As stated in the introduction to this article, one of the reasons why many investors purchase shares of utility companies is that they typically possess fairly high dividend yields. This comes from the fact that utilities have slower growth rates than companies in some other sectors, so they pay out a relatively high percentage of their earnings in order to provide investors with a reasonable return. In addition, the market does not usually assign high multiples to low-growth companies, so the dividend ends up being a significant percentage of the stock price. NiSource is certainly not an exception to this rule as it yields 3.49% at the current price. This is well above the 1.59% yield of the S&P 500 Index (SP500) as well as above the 2.42% yield of the U.S. Utilities Index ( IDU ). Thus, its current yield seems certain to attract many investors. NiSource also has a long history of raising its dividend on an annual basis, further adding to its appeal:

{kind=link}

The fact that the company increases its dividend every year is something that is very nice to see, especially during inflationary periods like the one that we are experiencing today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are getting poorer and poorer with the passage of time. The fact that the company increases its dividend annually helps to offset this effect and maintains the purchasing power of the money that the company sends us every quarter.

As is always the case, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be in a situation in which it is suddenly forced to reverse course and cut the dividend. This would reduce our incomes and almost certainly cause the share price to decline.

The usual way that we judge a company's ability to pay its dividend is by looking at its free cash flow. The free cash flow is the money that was generated by a company's ordinary operations and is left over after the company pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that can be used to reduce debt, buy back stock, or pay a dividend. During the twelve-month period that ended on December 31, 2022, NiSource had a negative levered free cash flow of $685.0 million. This is obviously not enough to pay any dividends, yet the company still paid out $436.6 million in dividends during the period. At first glance, this is likely to be concerning as the company clearly has insufficient free cash flow to cover its payouts.

However, it is common for utilities to finance their capital expenditures through the issuance of equity and debt. The company will then pay its dividend out of operating cash flow. This is due to the fact that the costs of constructing and maintaining utility-grade infrastructure over a wide geographic area are immense. A company could not afford these costs and pay out a dividend if it attempted to do this all with free cash flow. During the trailing twelve-month period that ended December 31, 2022, NiSource reported an operating cash flow of $1.4094 billion. That was clearly enough to cover the $436.6 million dividend and still have a great deal of money left over for other purposes. Thus, we probably do not have to worry about a dividend cut in the near future.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility like NiSource, one metric that we can use to value it is the price-to-earnings growth ratio. The price-to-earnings growth ratio is a modified version of the familiar price-to-earnings ratio that takes a company's earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to the company's forward earnings per share growth and vice versa. However, there are very few companies with such low ratios in today's overheated market, so the best way to use this ratio today is to compare NiSource's valuation with that of its peers in order to determine which company offers the most attractive relative valuation.

According to Zacks Investment Research , NiSource will grow its earnings per share at a 6.90% rate over the next three to five years. This is in line with the figure that we got from the company's rate base growth as discussed above, so it seems pretty reasonable. This growth rate gives the company's stock a price-to-earnings growth ratio of 2.65 at the current price. Here is how that compares to a few of the company's peers:

| Company |

| PEG Ratio |

| NiSource |

| 2.65 |

| Atmos Energy |

| 2.59 |

| New Jersey Resources |

| 3.32 |

| Northwest Natural Holdings |

| 4.83 |

| Southwest Gas Holdings |

| 3.22 |

As we can see clearly, NiSource Inc. tends to compare very well to its peers in terms of valuation. The company is admittedly not the absolute cheapest firm here, but it is pretty close. The current price, therefore, seems reasonable.

Conclusion

In conclusion, NiSource Inc. continues to look like a very solid natural gas utility. Despite common belief, natural gas is in no way obsolete, and it seems highly unlikely that it will be replaced with electricity for space heating anytime soon. NiSource Inc. enjoys remarkable cash flow stability that should allow it to ride through any economic troubles that may come over the remainder of the year, helped along by its reasonably strong balance sheet . When we combine this with a high dividend yield and an attractive valuation, NiSource Inc. stock looks like a buy today.

For further details see:

NiSource: Strong Balance Sheet, Cash Flow Stability, Valuation Make It A Buy