NSANF - Nissan: A BB-Rated Automotive Cyclical Hold For Now

2023-05-01 02:23:43 ET

Summary

- There have been some positive signals from Nissan as of late. While my focus in the Japanese market has been primarily on Subaru and Honda, I'm looking at Nissan here.

- Nissan is a qualitative business with some things going for it - but only at the right price. Coming out of several years of negative earnings, care is warranted.

- I view Nissan, at best, as being able of performing at the market level. That makes it a "Hold" for me - learn why here.

Dear readers/followers,

In this article, we're going to be taking a closer look at Nissan ( NSANY ). Now, when looking at a company like this, or any company, I typically work from a 2-5 year time frame. That is the time during which I want to see the company deliver on my thesis. I'm willing to wait far longer if challenges present themselves, which is why I'm very careful only picking companies that I would be willing to own long-term. But in general, I want the picks I make to deliver the upside within that initial time frame.

When we look at Nissan here, it's my stance that the company doesn't have a clear pathway to delivering a market-beating upside based on the current trends.

We'll learn why that is here.

Nissan - Careful with the bullish thesis on this one

Nissan Motor Corporation, or Nissan Jid?sha Kabushiki gaisha , as it's known in Japanese Hepburn romanticization, is a global, Japanese-based automotive company with headquarters in Yokohama, Japan. It's a core component of the Nikkei 225 and the TOPIX Core 30.

The company has a storied past, and includes well-known brands such as Datsun, and Infiniti, and traces its roots back to the Japanese business conglomerate Nissan, now known simply as the Nissan Group.

The company is one of the oldest components of the Renault-Nissan-Mitsubishi alliance - almost 25 years now - which has also meant that Renault formerly held a significant, 43.4% voting stake in the company. However, this was actually overhauled only 3 months back, right-sizing the stakes to non-voting 15% stakes respectively in companies.

Historically, Nissan has often been among the top 10 automotive manufacturers in the world. It shares this with companies like General Motors ( GM ), Ford ( F ), Volkswagen ( VWAGY ), Toyota ( TM ), and Hyundai ( HYMLF ) - many of which I actually review on a recurring basis here on Seeking Alpha.

I won't go too much into history here - simply say that you can find Datsuns from 1920 and before, and the fact that Nissan is probably one of the most American-influenced automotive businesses in the world, with visits to Detroit as early as 1908, which greatly affected the company's future.

As with all automotive companies, COVID-19 was not a pleasant time - for Nissan, it was worse than for many of its competitors. The company curtailed capacity by 20%, shutting down factories across the world and entirely exiting the South Korean car market with Infiniti as well as Nissan. The company was also in the midst of the Ghosn scandal, which caused nearly half a billion quarterly loss in 2020, financials which would come to hound the business's results for years afterward.

The company finally went positive in earnings back in 2022, which an annual positive result of ¥55.07, following 2 full fiscals of negative results - never pleasant for anyone. Volkswagen, as a comparison, never went negative. It never even came close. 2020 results dropped by 38%, but still came in €12.68 EPS adjusted, and climbed back 78% in 2021. So Nissan has had a rough time of it.

I say these things to give you the context of why I don't own shares in Nissan, nor will I in the near future.

Nissan is, at best currently average. In its comp sector with other automotive/vehicles, it's average in gross margins, operating margins, net, RoE, and other key performance indicators. It does not outperform in any one specific profitability, instead managing only 50-60th percentiles in profitability, and being among the worst in terms of debt. The company's debt-equity stands at 1.36x, with a debt-EBITDA of 6.56x. While not at a level as some REITs, it's nonetheless bad enough in the context that Nissan is worse than over 83% of the sector (Source: GuruFocus). This is a sector made up of many of the companies I mentioned earlier, including companies like Tesla (TSLA), BYD, BMW ( BMWYY ), Stellantis ( STLA ), and others.

The simple fact is this. I look for quality outperformers for a cheap price - when your company, or the company, isn't even above average and isn't trading at bottom-level valuations, why on earth would I be interested?

To say that Nissan is in distress would be going too far. However, it's BB-rated in a market with ratings at BBB-A ratings. It yields less than 1.1% in a market where you can get 6-7% from undervalued VW prefs.

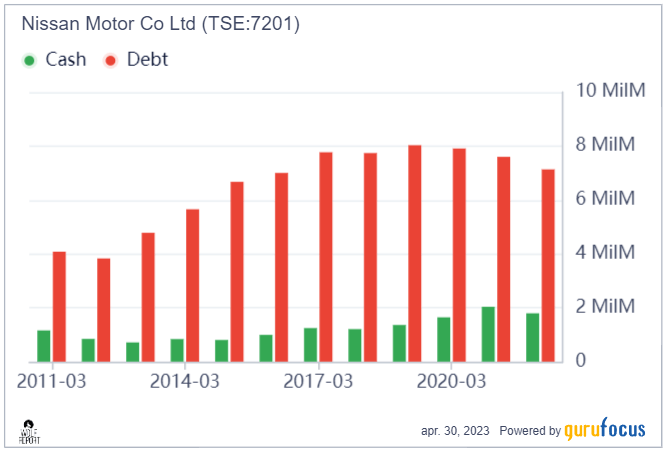

It has only very recently started putting a dent in some of its debt, and that process is going slowly.

{kind=link}

It is, in fact, an automotive producer that has been seeing a negative ROIC net of WACC for more years than most others since the GFC. The company simply, due to management or other reasons, isn't very capable of producing profitable investments for the money it has - at least not compared to other companies on the market.

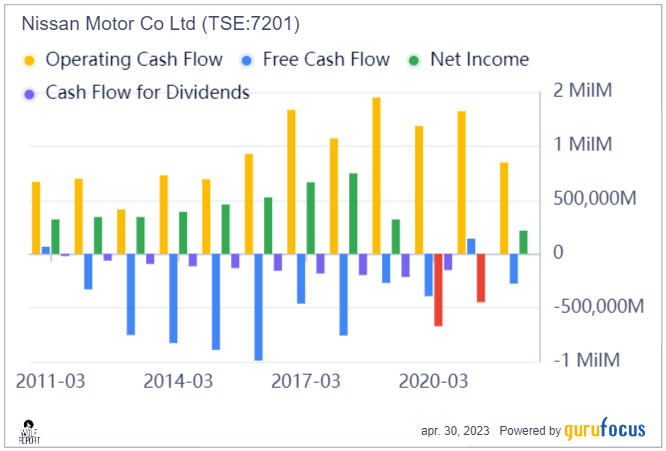

And while operating cash flows are positive, the sets of cash flows and the way they have trended for the past years, they do tell their own story here.

Nissan cash flows/net (GuruFocus)

{kind=link}

For some companies, I do need to provide a lot of context and look at portfolios, management, and product cycles, and pipelines. For other companies, it's actually enough to simply state that the company, in context, doesn't provide basic financial safety and undervaluation compared to other fully available investments in the sector.

My argument isn't against the company's products. Nissan has a whole host of attractive products and vehicles that do sell well. The LEAF is one of the best cars in its segments, and I would rather drive a LEAF than I would a Tesla. That is not the problem here.

You also shouldn't interpret this focus in the article as me not looking close enough at the company portfolio. I've looked closely at the Ambition 2030 plan, as well as the next few years until 2025-2027E in terms of estimated results. Its push for increasing the EV mix isn't exactly unique - all manufacturers are doing that, and most manufacturers are in some way talking about a "global ecosystem for mobility".

If the company's financials and results were better, I would go far deeper into that, because the company would have appeal.

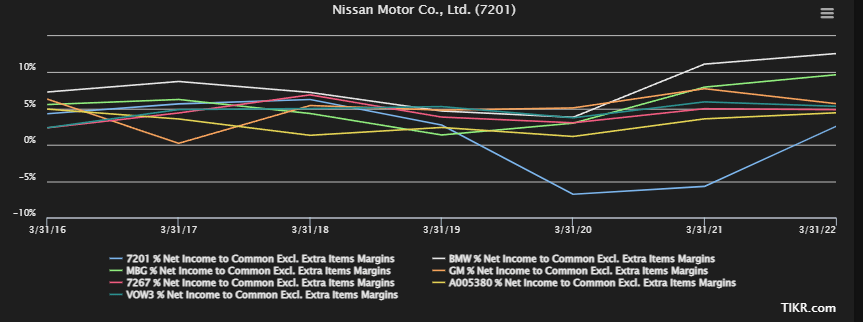

As it stands though, Nissan has the worst margins of any relevant peer in the industry - and I'm even excluding Tesla here. With Tesla, it would look worse.

Nissan Peer group net margins (TIkr.com/S&P Global)

{kind=link}

What worries me is that the company dove earlier, deeper, and stayed low while virtually all of the company's peers climbed back up - well up in some cases. This to me implies management, product, or financial issues - and looking at some of the relatively surface-level numbers, it gives enough indications and implications for me, that I do not even at this time feel the need to dig further.

The question becomes the following:

What should we pay for a below-average automotive player in a market where discounts in better and more profitable automotive companies is the rule, not the exception?

Valuation for Nissan - The answer is relatively easy

Now, quite obviously, we're not going to be paying a premium for that. Some basic stats to start things off Nissan typically trades at an average of 9.5x for the native ticker. It's currently at 11x P/E. The company is, as mentioned, BB rated, has a market cap of around ¥1.88T.

As things currently stand, and for the fiscal of 2023, Nissan is expected to not go positive, as many would hope, but to see yet another decline in its EPS to below 2022A levels - at least on an adjusted basis. On a GAAP basis, the company has been negative for 3 years at this point, even being GAAP-negative in 2022.

However, any credence given to forecasts here should only be given with the full knowledge that Nissan analysts have failed more often than not to provide accurate forecasts. Only 33% of the time have analysts hit the mark, with negative misses of several hundred percent back in 2020-2021 - and this isn't 1-2 analyst, these are dozens of FactSet/S&P Global analysts that often expected actual positive results, while the actual results went completely negative. 2021 is a great example - 19 analysts expected an average of ¥ 41.9, with the actual going -¥114.47. Remember, COVID-19 wasn't a surprise in 2021 - there is very little excuse for this sort of miss, as I see it.

These analysts haven't much changed their tune, instead believing that Nissan eventually will go up. 18 analysts give the company a range starting at ¥400 and going to ¥1,450 (I'd love to see those calculations). The average is ¥635, which according to these analysts is a 29.1% upside. But even these analysts, only 5 of them are at "BUY", with most at "HOLD", Underperform and even 2 "SELL".

Analyst conviction isn't high - and there is good reason for it, if you look at the way the company's financials are looking, and what is expected.

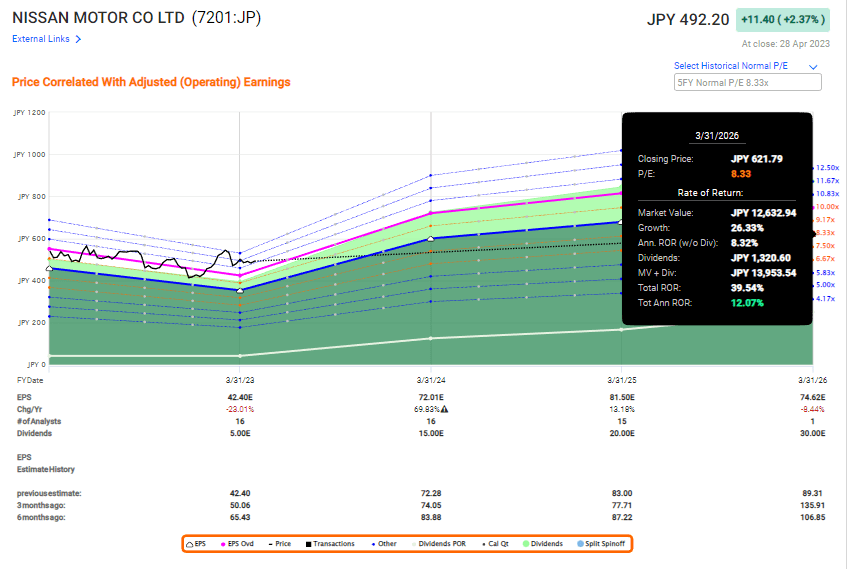

Double-digit upside in Nissan is possible under the circumstances of 2-4% EPS growth over the next few years, and essentially a 70% EPS normalization in 2024E, which is currently forecast.

Nissan Upside (F.A.S.T graphs)

{kind=link}

While such an outcome is entirely possible, I would say clearly here that I believe the risk taken in such an investment is not worth the reward, nor do I necessarily see it as likely to materialize.

At best, even with these growth estimates considered "in the bag", I would consider Nissan to be fairly valued at this time. There's too much volatility inherent to the company, and too many better companies - objectively in terms of profitability and finance as well as yield - available at much cheaper multiples with better and safer upsides.

For that reason, I cannot give Nissan anything but a negative or a "HOLD" rating. I don't necessarily see Nissan dropping further in share price. Some of the company's upside will no doubt be there - a combination of new sales, EV pushes and asset rationalization will see the company's bottom line improving. Just not enough, as I see it.

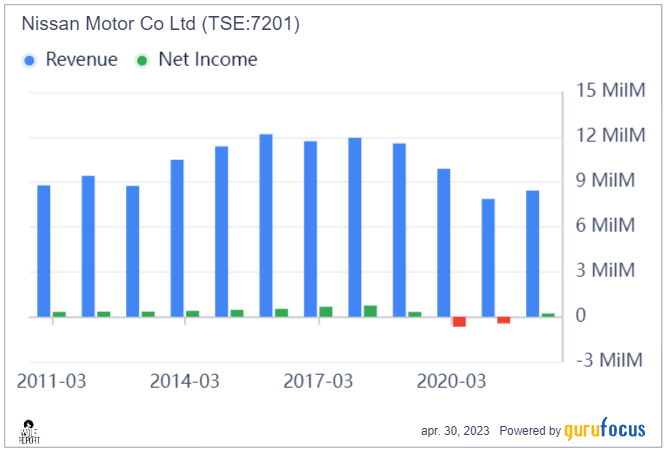

The simple fact is that Nissan is a company that over the past few years has seen significantly worse revenues and net income. The initial pushes from the LEAF and other models are "over". And this problem, by the way, goes well beyond just COVID-19. As you can see, the decline started well before the pandemic hit - the COVID-19 argument just doesn't fly.

{kind=link}

Sure, some of it is COVID-19. Without it, it wouldn't have been as bad - but the decline has been there prior to it. Nissan is one of the least profitable, least-growing automotive companies in an undervalued market filled with quality. Nissan is contextually inefficient as a business when compared to even ancillary competitors. It has a higher percentage of COGS and a higher percentage of overall costs along the entire value chain/production chain.

This is not the type of business that I buy at any time unless it's being grossly undervalued - and this is not the case here.

So while I would have loved to present you with a more comprehensive picture of its portfolio and plans, I do not think it necessary at this time to give you an accurate rating on Nissan.

That rating is "HOLD" - and here is the thesis.

Thesis

- While Nissan at some point will be theoretically attractive as a long-term investment, that time is not now. Nissan is currently fairly valued in a market where undervaluation and higher yield are the norm. Added to by its comparative inefficiencies, I do not see a good argument to be made why you should buy Nissan stock.

- I view Nissan as average in an above-average field. Because of that, I would discount it by 35% to FV, and give the company a native share price of ¥320. This is low, but I want to see improvements before I am prepared to move any higher.

- The NSANY ADR is a 2x ADR. That means my PT for the ADR is $4.7. This is a "HOLD".

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Neither cheap nor with an upside worth considering, I rate Nissan a "HOLD".

For further details see:

Nissan: A BB-Rated Automotive Cyclical, Hold For Now