NSANF - Nissan: Earnings Are Picking Up

2023-09-30 06:27:13 ET

Summary

- Renault and Nissan have entered a new phase in their decade-long relationship, with the Japanese carmaker investing approximately €600 million in Ampere.

- Despite lower unit volume, Nissan increased its operating profit guidance.

- A better FX environment will support the company's sales. This is coupled with a lower fixed cost structure and higher BEV earnings per car. Our buy rating is then confirmed.

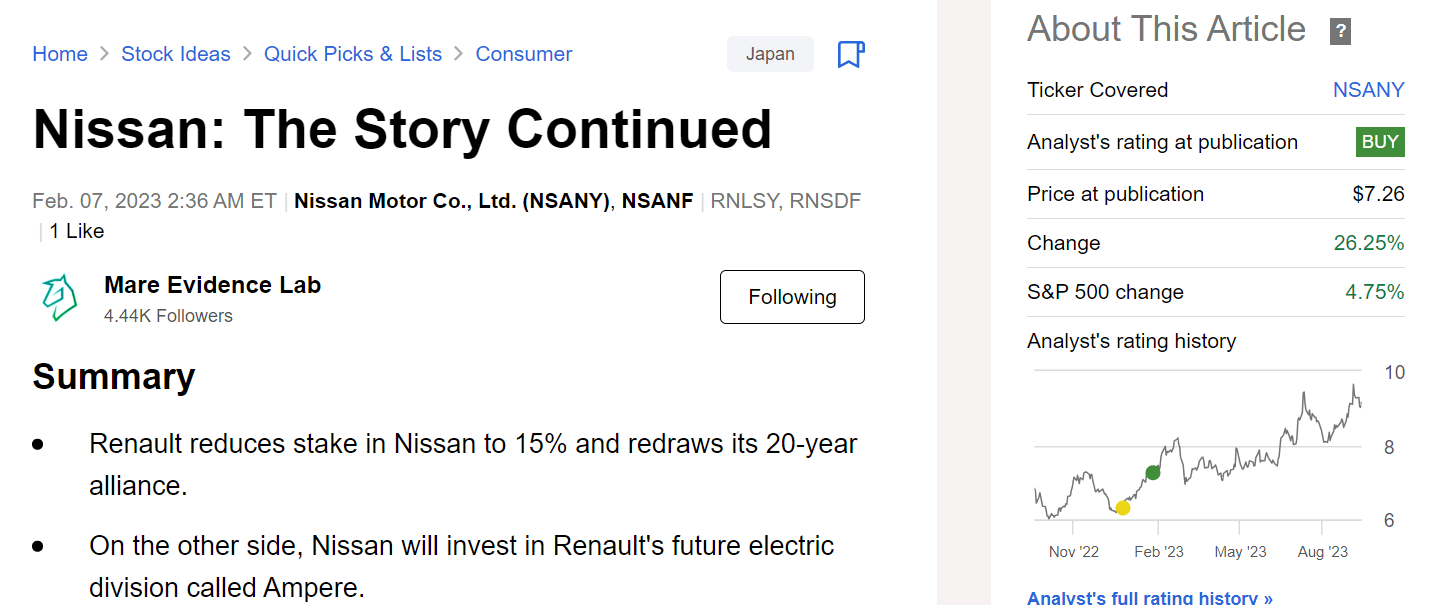

Here at the Lab, we look back to analyze Nissan (NSANF) (NSANY). This year, we have already commented twice on the company, moving our rating from neutral ' Waiting For A Dividend Increase ' to Buy ' The Story Continued ,' it was a positive investment call. Since then, Nissan's stock price has increased by 26%, outperforming the S&P 500 total return (Fig below).

{kind=link}

Before commenting on the company's latest news, our internal team sees the auto sector as highly attractive, even if the earnings cycle might likely peak. We have a positive view and remain favorable over the long-term growth estimates. This is mainly due to a higher earning per vehicle and a potential improvement in North American sales. As a reminder, here at the Lab, we have an overweight target price on Stellantis , Renault , and Volkswagen . Returning to Nissan, reporting the latest company's financials is vital to assess the next catalyst.

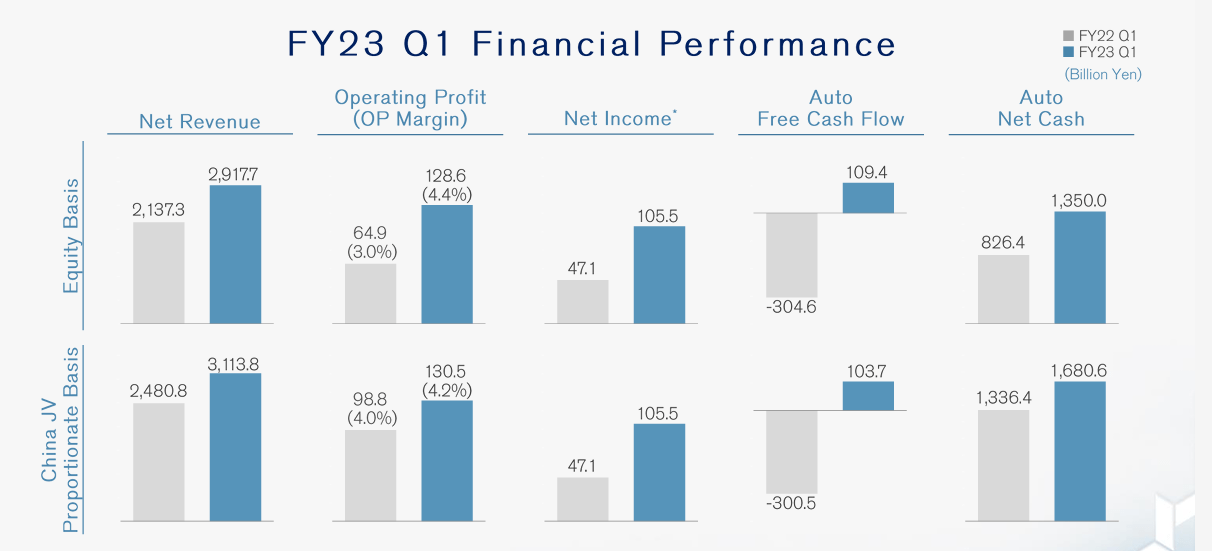

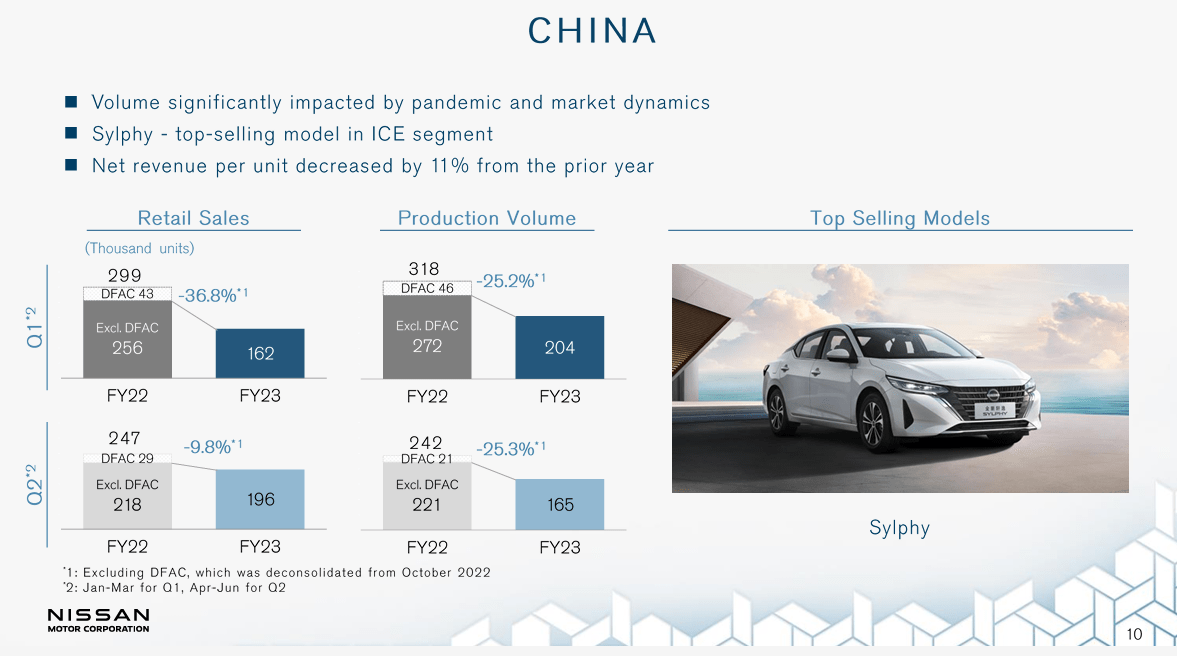

In Q1, Nissan increased net revenue reported a plus 37% on a yearly basis to ¥2.917,7 billion with operating profit that came in at ¥128.6 billion, with an increase of 98% vs. last year (Fig 1). Looking at the details, Nissan OP was described at ¥150 billion due to a one-off adjustment due to warranty costs. While Chinese sales volume declined due to intensified sales competition and the ongoing pandemic outbreak, the other regions achieved a remarkable performance year on year. This was also supported by the Yen depreciation, which coupled with product MIX and a strict cost discipline, led to a solid increase in profits (on a comparable basis, net income reached ¥105.5 billion, up by 124% year on year). Having analyzed Volkswagen, we know that business is more challenging in China, and in numbers, Nissan's Chinese JV operating profit decreased with a cut of production units from 1.13 million to 800k (Fig 2).

Nissan Q1 Financials in a Snap

{kind=link}

Fig 1

{kind=link}

Fig 2

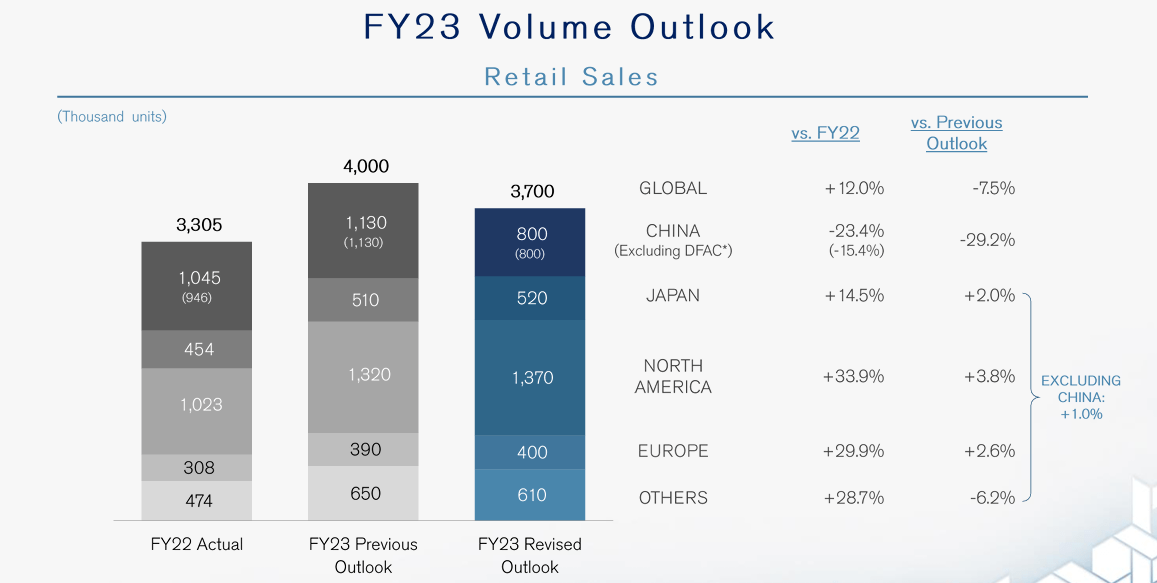

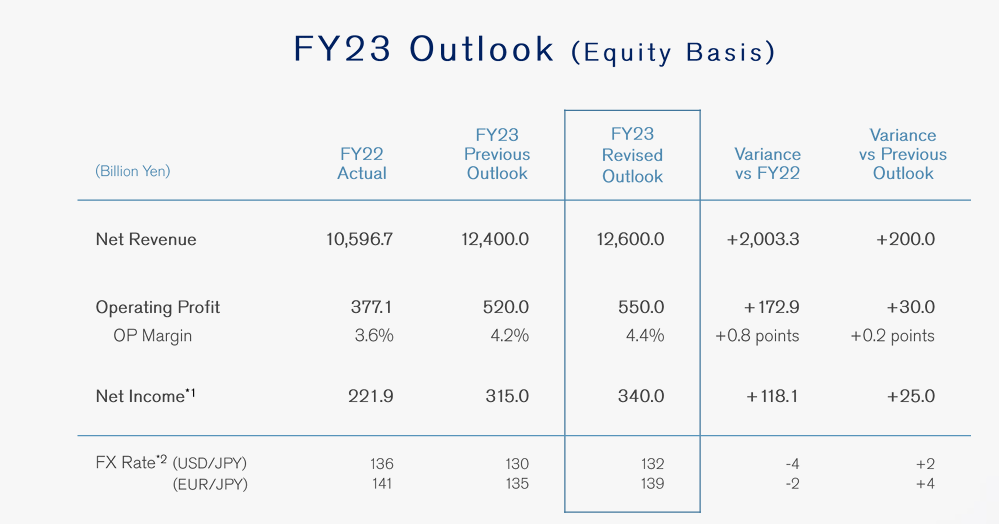

Key to report is the fact that although the company decreased its full-year global sales assumption to 3.7 from 4 million units (Fig 3), Nissan raised its operating profit to ¥550 billion (from a previous guidance of ¥520 billion), with a net profit estimate at ¥340 billion, which is ¥25 billion better than previously communicated. Here at the Lab, we see a further upside mainly due to the Nissan conservative FX assumption of 132 ¥/$ (Fig 4).

{kind=link}

Fig 3

{kind=link}

Fig 4

Why is Nissan still a buy?

- Starting with the recent news, Nissan announced that all new cars sold in Europe will be fully electric by 2030, confirming its commitments to comply with the region's stringent environmental regulations. " Electric vehicles are the ultimate solution for future mobility; there is no way back ," said the group's CEO , Makoto Uchida, in a statement on the twentieth anniversary of the carmaker's design center in London. Nissan's new target updates released in February 2023 aim to increase market penetration in hybrid and fully EV segments. In detail, the company plans to introduce 27 electric-powered models globally by 2030. Here at the Lab, we anticipate that the company will be able to confirm its revenue growth thanks to this ongoing new model;

- While we are waiting for the next medium-long horizon strategic plan, at this stage, we believe that Nissan's overall earnings improvement should reassure Wall Street analysts and investors;

- In this period, we should also report the final agreement between Nissan and Renault that was announced before the Q1 release and seems aligned with the February disclosure. A new era began for the Alliance, and based on this latest pact, Renault Group and Nissan will maintain cross-shareholdings of 15%. Renault will transfer 28.4% of its Nissan shares into a French trust, where the entrusted shares will be voted neutrally. On a strategic level, there is a strategic rationale to share CAPEX investments with projects in Latin America, Europe, and, above all, India. Furthermore, cooperation is strengthened with " mutual support in electrification and low-emission technologies by investing and collaborating in specific projects that can represent added value for the partners ." Under this agreement, Nissan will invest up to €600 million in the spin-off of Renault's electric car Ampere, securing a place on the board.

Conclusion and valuation

Nissan is now forecasting net revenue of ¥12.6 trillion; however, considering a better FX environment, as already anticipated, we believe that the company sales estimates are skewed to the downside. In our numbers, we are above Nissan's forecast and project top-line sales of ¥13.1 trillion. In addition, Nissan's operating leverage has improved with lower fixed costs and other savings, which started to make more significant and earlier earnings contributions. Here at the Lab, despite lower unit projection, we positively view the improvement in BEV per-vehicle earnings. Given the revised guidance, we anticipate an operating profit of ¥660 billion with an estimated ROE of 7% for the following year. We think Nissan still offers an attractive risk/return balance at this price. Updating our estimates, we value the company with a 7x P/E and a price target increase from ¥600 to ¥700 per share. Our buy rating is then confirmed.

For further details see:

Nissan: Earnings Are Picking Up