NMAI - NMAI: Better Performance Is Required To Make This Fund Appealing For Investors

2023-11-14 18:31:33 ET

Summary

- Nuveen Multi-Asset Income Fund has underperformed its benchmark and most asset classes since its inception in November 2021.

- The fund's performance has been disappointing, and it remains to be seen if it can recover and avoid distribution cuts.

- NMAI's allocation is diversified, with a focus on equities and debt securities globally. It has overweight exposure to real estate and utilities and underweight exposure to technology and financials.

While the recent rise in the share price of the Nuveen Multi-Asset Income Fund ( NMAI ) has brought some relief to investors, the performance of the fund since its inception in Nov 2021 has not been exciting so far, as the fund has lagged behind its benchmark and also most asset classes where it has capital allocated.

Of course, most asset classes have been without a clear direction during this period and this has been an additional challenge for asset managers. This is particularly concerning for funds that rely on capital gains to cover their high distributions like NMAI, the global allocation fund managed by Nuveen.

Therefore, time is needed to confirm whether this fund can recover so that it can avoid any distribution cuts over the coming quarters.

Fund Description & Highlights

As a global allocation fund, NMAI has the flexibility to invest in equities and debt securities around the world. The fund's target is to generate total return through income and capital appreciation. Given its broad investment strategy, its benchmark is comprised of 50% Bloomberg U.S. Corporate High Yield Bond Index and 50% MSCI ACWI Index, a stock index composed of large and mid-cap stocks from developed and emerging countries.

The allocation of the fund has been fairly diversified. As of Sep 30th, 2023, 40.4% of the fund was invested in common stocks, 12.7% in asset-backed securities, 13.5% in preferred stocks, 9.1% in senior loans, 5.8% in corporate bonds, 4.9% in emerging markets ETFs, 4.6% in U.S. government and agency obligations and 3.0% in sovereign debts. Most recent changes in the portfolio in the third quarter included a reduction in the allocation to equities and mortgage-backed securities, while the fund increased exposure to core bonds, and short-term bonds and added new allocation to inflation-protected securities.

Reflecting the high yield profile of the fund, NMAI's weighted coupon is 5.59%, somewhat higher than the category average of 3.52%, while its average maturity is relatively longer-dated than the category, as 36% of the portfolio's maturity is higher than 20 years. On the other hand, nearly 22% of the fund has maturity in the range of 3-5 years, as the fund has recently added short-term bonds to the portfolio.

And as for the credit quality, NMAI has nearly 60% rated as B, BB or BBB versus 27% of the category, which is not surprising given the fund's allocation in below investment grade assets, such as senior loans, asset-backed securities and corporate bonds.

Turning to the portfolio of common stocks, nearly 44% of NMAI's exposure is the United States, as opposed to the MSCI ACWI Index, where United States represents 62% of total equities.

From the sector allocation perspective, NMAI has a more balanced approach relative to ACWI index, with industrials accounting for 13.8% of the total stocks, real estate 13.3%, information technology 12.5%, financials 11.9%, energy 9.3%, consumer discretionary 9.0%, health care 8.7%, utilities 7.2%, basic materials 5.5%, consumer staples 4.9% and communication services 3.9%.

The most significant distinctions relative to ACWI index are the NMAI's overweight allocation on real estate (+11.0%), utilities (+4.6%), energy (+4.2%), industrials (+3.4%) and underweight exposure to information technology (-9.0%), financials (-3.7%) and communication services (-3.6%).

We have a similar picture in a comparison between NMAI and the S&P 500 index, as NMAI has overweight allocations on real estate (+10.9%), industrials (+5.5%), utilities (+4.8%), energy (+4.6%), but underweight exposure to information technology (-15.0%), communication services (-5.0%) and health care (-4.7%).

NMAI's website, ACWI and S&P indexes' websites, consolidated by the author

Looking at the individual stocks' allocation, NMAI's top ten constituents (Prologis, Novo Nordisk, Microsoft, Shell, Astra Zeneca, Apple, Linde, Samsung, Equinix and Exxon) account for nearly 12.3% of total equity exposure as of Sep 30th. That is in stark contrast with the ACWI index, where top ten holdings (Apple, Microsoft, Amazon, Nvidia, Alphabet Class A, Alphabet Class C, Meta, Tesla and UnitedHealth) are more concentrated on tech stocks and represent 17.9% of the index.

However, despite the sector allocation differences, NMAI is still mostly a large-cap fund, with only 12% of the stock exposure invested in mid and small-caps, compared to 17% for the ACWI and S&P 500 indexes. And from a valuation perspective, both NMAI and the ACWI index have P/E Forward of nearly 14.8, as NMAI's underweight exposure to the higher multiple technology sector seemed counterbalanced by its overweight allocation to the real estate sector, that also trades at P/E Forward above 20. Meanwhile, as expected, both NMAI and ACWI trade at a discount compared to S&P 500's P/E Forward of 18, given in large part by its worldwide allocation, as international stocks generally trade at a discount relative to U.S.-based companies.

Performance Has Not Been Encouraging So Far

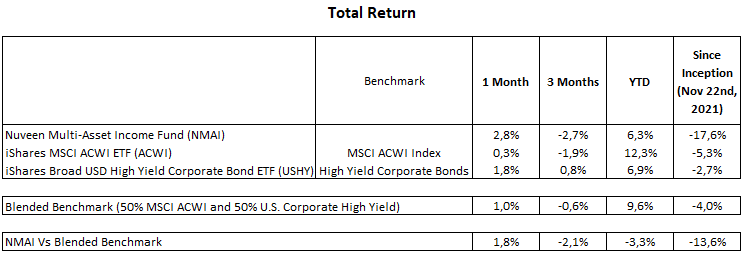

The performance of NMAI has been quite disappointing. Since inception on Nov 22nd, 2021, the fund delivered a total return of -17.6%, while its two benchmarks, MSCI ACWI index and U.S. Corporate High Yield have returned -5.3% and -2.7%, respectively, over the same period. Here we adopted the iShares Broad USD High Yield Corporate Bond ETF as the benchmark for High Yield Corporate Bonds.

As we can see below, despite the recovery of NMAI in the last 30 days, the fund has underperformed the blended benchmark, constituted of 50% MSCI ACWI and 50% U.S. Corporate High Yield, over different time frames (3-month period, year-to-date and since inception).

{kind=link}

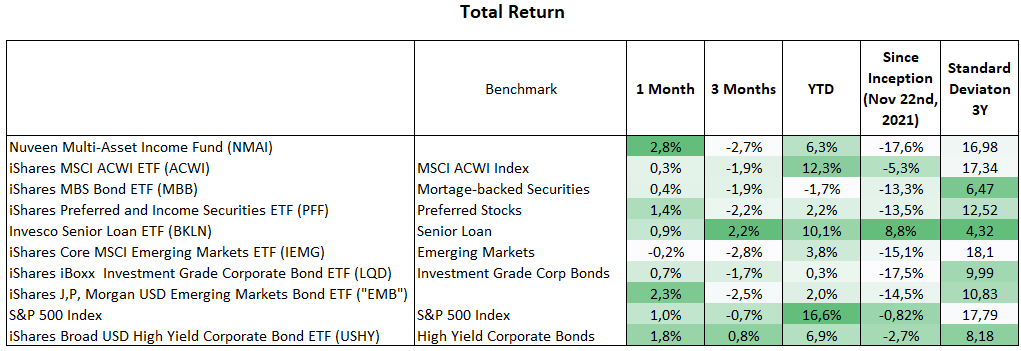

However, it is fair to say that as NMAI's investment strategy consists of capital allocation in a broad range of securities, we can expect that at least part of them have not high correlation with the fund's official benchmark. That is why it makes sense we also assess the fund's performance taking into consideration other benchmarks that can better represent NMAI's invested portfolio.

That said, we prepared the table below comprised of some relevant benchmarks for this analysis, including the performance of ETFs that we believe can adequately reflect those benchmarks.

{kind=link}

While NMAI has outperformed all benchmarks in the last month, the fund was one of the worst performers over the 3-month period. Year-to-date, NMAI's total return has been in the middle of the pack, once it underperformed stocks, senior loans and high yield corporate bonds, but outperformed mortgage-backed securities, preferred stocks, emerging markets and investment-grade corporate bonds.

Over a longer time frame though, considering the time frame since its inception in Nov 2021, NMAI had the worst performance compared to all benchmarks.

Of course, my view is that while NMAI's total return has not been encouraging so far, to say the least. However, it is not enough time to properly rate a fund as good or bad, as market cycles can remain in place for a long time, and certainly market conditions have been particularly uncertain and less predictable over the last couple of years, as we exited unprecedented business and economic conditions coming from the pandemic just to face rising inflation pressures, the rate-hiking cycle led by central banks and current geopolitical tensions.

An Early Warning Sign For NMAI's Distributions

The income generated by NMAI's invested portfolio is not bad. Equities' dividend yield is nearly 3.26% and the fixed income weighted coupon is roughly 5.59%. However, this isn't anywhere near the fund's annual distributions of 10.6%.

As reference, according to the fund's semi-annual report, over the first six months of 2023, the fund generated $6.46 million through dividends and $9.03 million through interests, totaling an investment income of $15.12 million. After netting out $9.11 million relative to net expenses during the period, net investment income was $6.02 million. In addition, there was a net realized loss from investments of $17.05 million.

As the distribution in the period was $20.06 million, the fund had to cover it using $14.04 million from unrealized appreciations. As these unrealized appreciations were $39.94 million as of June 30th, 2023, net assets increased by $8.85 million, despite this large distribution.

Turning to the second half of the year, the fund maintained its quarterly distribution of $0.30 per share in September. Assuming the fund will distribute another $0.30 per share by year-end, the total distribution for the second half is expected to remain in the neighborhood of $20 million. And if net investment income comes in at around $6 million in the second half, similarly to the first six months of the year, the fund management should continue to cover distributions through return of capital, as it is already occurring over the course of this year, unless there are enough realized gains on investments.

It is certainly something to watch at the fund's next annual report. If we continue to see a large proportion of its distribution as return of capital, at some point the fund management may need to review the distribution policy and trim distributions.

Price/NAV Discount In The Middle of The Range

The discount in shares of NMAI versus its Net Asset Value has just narrowed to -13.20%, coming up from the lows of -15%, following the recent recovery in the fund's prices. Now, the discount is near the level of -13% reached during the rise in the stock prices in September.

Meanwhile, this discount is still below previous levels seen in the January and over the course of last year, suggesting the discount has potential to narrow further to below -12%.

However, I believe that we are more likely to see lower price/NAV discounts only in case of a more sustainable move upward in stock prices and a consistent rise in NMAI's NAV over the coming months.

The flip side of the equation is that as long as markets remain without a clear direction, a steady recovery in NMAI's NAV may need to rely on an outperformance relative to the broader market, what has not been the norm for this fund.

That said, with NMAI underperforming its benchmark so far, as well as most asset classes where the fund has capital allocated, I do not see NMAI as an appealing investment for the time being. Therefore, I prefer to wait and see how it performs through the remainder of the year so that we can check if the fund can improve its performance and evaluate the potential impact on its distribution.

For further details see:

NMAI: Better Performance Is Required To Make This Fund Appealing For Investors