NMIH - NMI Holdings: Growth At A Cheap Price But Not Entirely Risk-Free

2023-10-20 16:23:39 ET

Summary

- NMI Holdings is an insurance company specializing in mortgage insurance, offering value for long-term investors.

- The company's risk management policies, including high credit scores and strict underwriting standards, contribute to its strong performance.

- NMIH has experienced significant growth in customer relationships and market share, with low default rates and a favorable valuation.

- Still, the company is relatively young, and its business hasn't been tested in a recession. Due to the nature of the company's business, investors should limit their position size in it.

NMI Holdings ( NMIH ) is an insurance company specifically focusing on mortgage insurance. The company offers a compelling value for long-term focused investors with its current valuation.

Typically, when people buy a house using a mortgage, if they have less than 20% equity on the house (either due to not having a large enough down payment or due to offering more money than the house's appraised value) mortgage issuers require them to buy a mortgage insurance plan. These plans basically cover the losses of the mortgage issuing (or mortgage holding) bank if the buyer defaults on their debt. Typically, monthly mortgage insurance payments are rolled into mortgage payments (along with home insurance and property taxes) and collected in an escrow account so that insurance coverage continues.

If the borrower fails to make a payment and defaults on their mortgage, the mortgage insurance company is liable for the difference between how much the bank can get from putting the house on the market (minus selling expenses) and how much debt there is so the mortgage insurance company doesn't have to pay the entire mortgage bill. Let's say someone borrowed $500k to buy a house that's worth $550k. They paid down $10k of this debt and then defaulted on their debt. Now the remaining debt is $490k, but the house is worth $550k, so the bank might be able to put the house on the market and get its money back without needing insurance to cover its losses.

Let's think of another scenario where the mortgage holder is actually underwater, which is what happened to a lot of people in 2009. In this hypothetical scenario, the house is worth only $400k but the remaining mortgage amount is $470k. Now the insurance company has to cover the remaining $70k, but this is not as bad as covering the whole $470k. Banks typically don't require mortgage insurance if a borrower has at least 20% equity in their homes because it allows for a decent amount of margin of safety, which makes it less likely that they will be underwater on their loan even if they default.

In 2009 several mortgage insurers went bankrupt because too many people were underwater not to mention many people having a second mortgage on their home or using their home equity for a personal line of credit which was a common practice at the time. Luckily, things have changed a lot since 2008. Banks are much more strict about who they issue mortgages to. Back in 2008, many banks didn't do employment checks or credit checks while issuing mortgages, but now they all do. Another difference between now and 2008 is that very few people are currently underwater on their loans, whereas many people were underwater in 2008 even before home prices collapsed because they had too much debt to begin with because of 0 down payment loans. Americans are currently enjoying record amounts of home equity, even though it is not guaranteed to last forever and things can always turn upside down in a quick fashion as we've seen many times before.

Now, back to NMIH. The company wasn't around in 2008, so we don't know how it would behave in a similar scenario, but so far it's been performing well due to its risk management policies in place. For example, the average credit score of customers of NMIH is 752 which is significantly higher than the US average which is around 700. The company almost exclusively insures properties where the borrower actually uses as their primary home and lives in. This is important because people are much less likely to default on mortgages involving their primary residence as opposed to a home they bought as an investment property or a vacation home. The company only covers fixed-rate mortgages as opposed to variable-rate ones, which is another advantage because fixed-rate mortgages have much lower default rates. Many people default on their mortgages when their rate suddenly rises, which makes variable-rate mortgages quite dangerous for those with a tight budget.

The company has other safety measures in place as well. For example, it will only cover policies that have full documentation where all background, credit, and employment checks have been made and 100% verified. The company refuses to insure mortgages that didn't go through its rigorous underwriting standards. Also, currently, the average insured home has a locked mortgage rate of 3.6% which is low enough that the risk of default is relatively low.

Between 2016 and 2022, the company was able to increase its customer relationships by almost 100% from 761 to 1,409. Having a larger customer base allows the company to diversify its risk and manage it better in case something goes wrong. Of course, no amount of customers can provide sufficient protection if the whole nation's mortgage policy blows up like it did in 2009, but that's a pretty extreme event.

Growing Customer Base (NMI Holdings)

In the last 4 years, the company has been able to grow its net income at an impressive rate as it grew from $161.9 million to $282.1 million. The company's ROE (return on equity) ranged between 15.9% to 21.1% during this period which can be considered strong but keep in mind that this was a very favorable period for mortgage companies and the housing market was on a roll, so this success might not repeat under less ideal conditions.

Growth of Income (NMI Holdings)

Below is one metric I find quite impressive, which could be the result of the safety guards employed by the company I described above. The company's customers currently have a current default rate of 0.71% which is much below the industry average of 2%. Currently, default rates are low across the board for the whole industry to begin with, but this company's rates are even lower than the industry average by almost two-thirds, which is impressive. Also keep in mind that not all these defaults will result in a payment because many of them might have enough equity where the bank doesn't need to collect money from the insurance company, especially considering how strong the housing market has been lately.

Current Default Rates by Company (NMI Holdings)

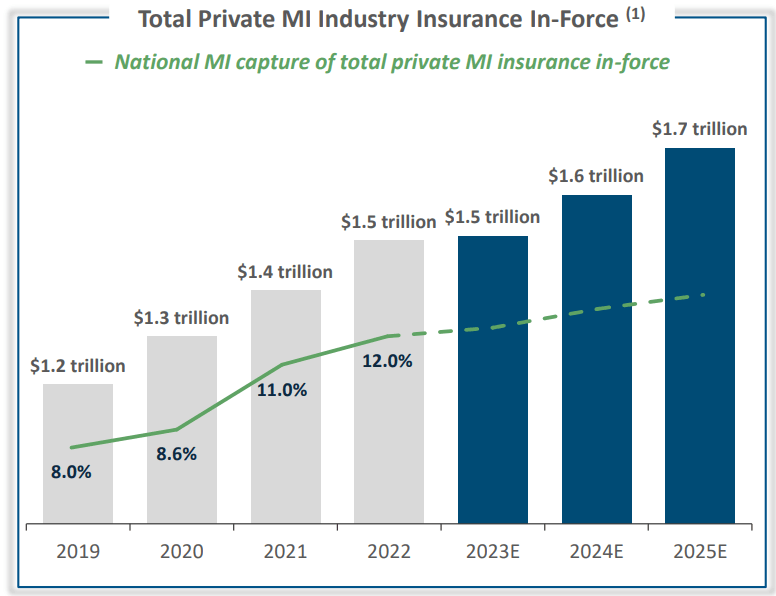

Currently, we are seeing two trends in the industry concerning this company. First, the mortgage insurance industry has been growing at a relatively rapid pace and is expected to continue growing well into 2025 and beyond. Second, NMIH is gaining increasingly larger amounts of market share in this rapidly growing market. Between 2019 and 2022, the company was able to increase its market share from 8% to 12% which is a growth of 50%, so the company was able to capture a bigger slice of a growing pie and its market share is projected to keep growing for the foreseeable future.

{kind=link}

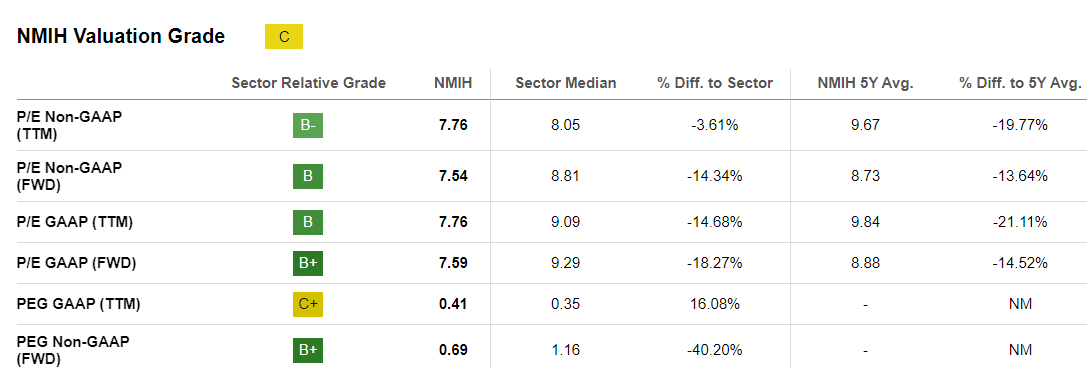

The company enjoys a pretty decent valuation at the moment. It has a trailing P/E of 7.76 and forward P/E of 7.54 on non-GAAP basis and roughly a P/E of 8 on GAAP basis, which is slightly lower than the sector average. More importantly, the company's PEG ratio is 0.41 which makes it appear exceptionally cheap. PEG is an important metric that takes a company's growth rate into account and to see if the company's existing P/E ratio is justified. A PEG ratio below 2.0 is considered fairly cheap while a PEG ratio below 1.0 is considered almost too cheap to ignore. The company's current PEG ratio is exceptionally cheap, to say the least. Keep in mind that insurance companies tend to have lower P/Es, so I wouldn't expect this company's P/E to climb to much higher levels anytime soon.

{kind=link}

Although the company is highly profitable and enjoys a low valuation, it doesn't pay a dividend, which bothers me a little bit. I believe the company could easily afford to pay a decent dividend, but it chose not to so far. Perhaps the management finds it more suitable to invest into the company's growth rather than pay dividends at this stage of the company's life.

The biggest risk for this company is obviously a total blow up of the mortgage market like what we saw in 2008. Though it's very unlikely at the moment, it's not impossible either. If the last 20 years have taught us anything, nothing is impossible in this economy as well as the market. Investors should never put too much of their money into an insurance company and keep their positions relatively small in their well-diversified portfolio. This is not only limited to mortgage insurers, either. You can apply this logic to any type of insurance company because you never know what kind of event could wipe out an insurance company.

For further details see:

NMI Holdings: Growth At A Cheap Price But Not Entirely Risk-Free