SRE - NML: A Solid CEF That Is Worth Buying Today

2023-04-05 16:29:17 ET

Summary

- MLPs and similar companies have long been among the favorite investments for those seeking income.

- Neuberger Berman MLP and Energy Income Fund Inc. invest in a portfolio of MLPs and other energy companies in order to deliver a high level of total return to its investors.

- The closed-end fund's exposure to upstream production, utilities, and renewables provides a greater amount of diversity than would be provided by a typical MLP fund.

- The fund currently pays a 10.46% yield and can easily sustain it.

- The fund is trading at a very attractive valuation.

For many years now, master limited partnerships have been among the favorite investments for those that are seeking income. This is because these companies tend to enjoy remarkably stable cash flows over time, regardless of conditions in the macroeconomic environment, and pay out a significant portion of their cash flows to their owners in the form of distributions. In addition to this, the distributions paid by these companies enjoy certain tax advantages that make them a bit better than corporations that have similar yields.

Unfortunately, the tax advantages enjoyed by these companies also make it very difficult to put them into retirement accounts. That is a shame because otherwise, midstream master limited partnerships would be perhaps the perfect vehicle for the generation of retirement income. It can also be difficult to put together a diversified portfolio of these companies without having access to a considerable amount of capital, but that is true with any sector of the market. There is a way around both of these problems, however. This is to purchase shares of a closed-end fund, or CEF, that specializes in midstream partnerships. As these funds are structured as corporations, they eliminate any tax problems that come with putting these firms into an investment portfolio. In addition, these funds provide easy access to a professionally run diversified portfolio that can usually deliver a higher yield than any of the partnerships in the fund. When we consider how high the yield of most master limited partnerships is, this is undoubtedly appealing to any investor that is seeking income.

In this article, we will discuss the Neuberger Berman MLP and Energy Income Fund Inc. ( NML ), which is one closed-end fund that specializes in midstream energy partnerships. As of the time of writing, this fund boasts a remarkable 10.46% yield, which is certainly enough to appeal to anyone that is actively seeking income. In previous articles, I have stated that any closed-end fund that has a double-digit yield is usually accompanied by some fear of a near-term cut, but most midstream funds are in very good shape financially and only have a high yield because the growing focus on environmental, social, and governance principles has resulted in many investors neglecting the sector. This applies to the entire traditional energy sector, which appears to be remarkably undervalued today. This is certainly the case with this fund as it appears to be trading at a very attractive valuation at the current price. Therefore, let us investigate and see if this fund could be a good addition to your portfolio.

About The Fund

According to the fund's webpage , the Neuberger Berman MLP and Energy Income Fund has the stated objective of providing its investors with a high level of total return. This is not surprising since pretty much every midstream master limited partnership fund has this as its objective. The fact that the fund invests primarily in common equity adds to the lack of surprise. As we can see here, currently all of the fund's assets consist of common equity, although it does keep a small amount of cash on hand:

CEF Connect

The reason that a focus on total return is not especially surprising given this portfolio is that common equities are by their very nature a total return instrument. After all, investors typically purchase shares of common stock in order to receive income in the form of dividends paid directly to the shareholders along with benefiting from capital gains as the issuing company grows and prospers. In the case of master limited partnerships, the majority of the return is provided by distributions paid directly to the investors. This is because these companies tend to have low growth compared to many other sectors, so they need to pay out a significant portion of their cash flows in order to deliver an acceptable return. This results in these companies having high yields, since the low growth generally results in the market assigning low multiples to their unit prices. The Alerian MLP Infrastructure Index ( AMLP ) currently has a 7.88% yield, so we can clearly see that most midstream master limited partnerships are going to have a high yield.

As just stated, midstream companies tend to enjoy remarkably stable cash flows regardless of conditions in the economy. This is because of the business model that these companies use. Although a midstream company's business is the transportation of natural gas, crude oil, and other petroleum products, it has very little exposure to changes in energy prices. This is because these companies enter into long-term contracts (usually five to fifteen years in length) with their customers under which the midstream company transports crude oil, natural gas, and other substances owned by the customer. In exchange, the customer compensates the midstream company based on the volume of resources that are handled, not on their value. These contracts also usually include minimum volume commitments that protect the midstream company in the event that a sustained decline in energy prices reduces resource production. Overall, this prevents these companies from being hurt by severe economic problems. As I pointed out in various previous articles, the cash flows of most midstream companies did not decline in 2020 in response to the collapse in energy prices that accompanied the pandemic. While it is true that the common equity prices of these companies got obliterated, there is a pretty big difference between a company's market performance and its actual financial performance.

As my regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing midstream partnerships and corporations both here at Energy Profits in Dividends and over on the main Seeking Alpha site. As such, everyone will likely be familiar with the largest positions in this fund. Here they are:

Neuberger Berman

The biggest surprise here is likely NextEra Energy Partners ( NEP ), which is a renewable energy yieldco and not a traditional midstream company. As I discussed in a recent article on the partnership though, it does have many of the same characteristics that midstream energy companies possess. In particular, NextEra Energy Partners sells its generated electricity under long-term power purchase agreements that cause the partnership to enjoy very stable cash flow over time. That lends itself well to providing support for the distribution, although this partnership does not nearly have as high of a yield as many of the traditional midstream companies in this portfolio.

We also see other companies here such as Antero Resources ( AR ), Cheniere Energy ( LNG ), and Sempra Energy ( SRE ), that are not midstream companies. Antero Resources is an upstream producer, Cheniere Energy is the largest producer of liquefied natural gas in the United States, and Sempra Energy is a utility. This clearly shows that this fund is more than just a stereotypical midstream energy fund. This could prove quite appealing to those investors that want to benefit from the energy transition, particularly since both Antero Resources and Cheniere Energy are poised to benefit from rising demand for natural gas, which is certain to happen alongside the expansion of renewable energy sources. This could certainly prove to have a long-term benefit, although upstream producers like Antero Resources do not have nearly the same cash flow stability that a midstream company does. They also have much lower yields, so the presence of companies like this will cause the fund's income to be lower than it would be with an all-midstream portfolio.

The diversification between the different types of energy firms extends over the entire portfolio. As we can see here, midstream companies only account for 64.0% of the portfolio:

Neuberger Berman

This has additional benefits due to the fact that there are relatively few midstream companies that have sufficient size to be included in a closed-end fund. As I pointed out in an article from last week, the Alerian MLP Infrastructure Index itself only has fourteen constituents. Admittedly, that index does not include midstream corporations like Targa Resources ( TRGP ), but even these do not bring the count up to a sizable number. Thus, the fact that the Neuberger Berman MLP and Energy Income Fund includes other types of energy companies allows it to choose from a much larger investment universe when assembling the portfolio. Currently, this fund includes 27 positions, which is not a lot, but it is still better than the dozen or so that it would have if it could only invest in midstream companies.

With that said, the fund still is not as diverse as I would really like to see. As my regular readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any individual position in a fund account for more than 5% of the fund's portfolio. This is because that is approximately the level at which an asset exposes the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio then it will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market in aggregate does not, and if that asset is too heavily weighted, it may end up dragging the entire fund down with it. As we can clearly see above, the Neuberger Berman MLP and Energy Income Fund currently has seven positions that each individually account for more than 5% of the fund's portfolio. While these are all generally stable companies that comprise some of the largest in the industry, there are still risks here that an event such as a distribution cut will pull the entire fund down. As such, potential investors should ensure that they are willing to be exposed to the risks of these companies individually before making an investment in the fund.

Leverage

In the introduction to this article, I stated that closed-end funds like the Neuberger Berman MLP and Energy Income Fund have the ability to boost their yields beyond that of any of the underlying assets in the portfolio. One of the methods through which this is accomplished is the use of leverage. In short, the fund borrows money and then uses those borrowed funds to purchase shares of master limited partnerships and other energy companies. As long as the interest rate that the fund has to pay on the debt is lower than the yield that it receives from the purchased assets, this strategy works pretty well to boost the overall yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are significantly lower than retail rates, that will normally be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not have too much debt since that would expose us to too much risk. I do not generally like to see a fund's leverage exceed a third as a percentage of its assets for this reason. Fortunately, the Neuberger Berman MLP and Energy Income Fund fulfills this requirement handily, just like most energy-focused closed-end funds. As of the time of writing, the fund's levered assets comprise 17.31% of the portfolio. This is a very reasonable level of leverage, and it clearly indicates that the fund is striking a pretty good balance between risk and reward.

Distribution Analysis

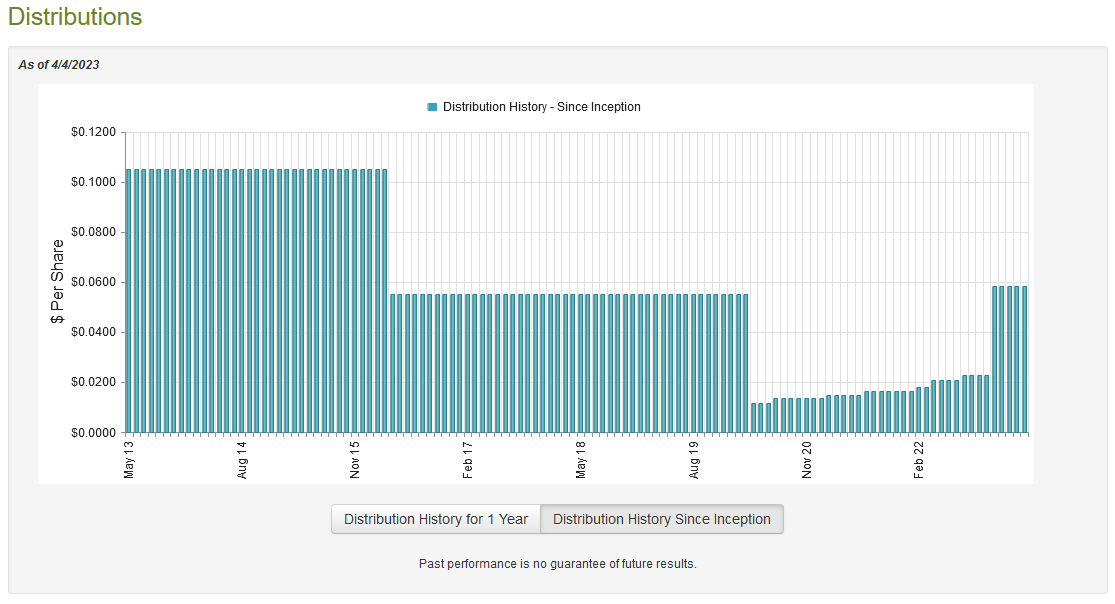

One of the biggest reasons that investors purchase the common equity of master limited partnerships is the incredibly high yields that these companies usually possess. This fund primarily purchases these partnership units and then applies a layer of leverage in order to boost the yield. The fund may also receive capital gains and dividends from the various energy corporations in the portfolio, providing a further source of money that can be paid out to the shareholders. As such, we might assume that the fund pays its investors a very high distribution itself. This is certainly the case as the Neuberger Berman MLP and Energy Income Fund pays a monthly distribution of $0.0584 per share ($0.7008 per share annually), which gives it a very impressive 10.46% yield at the current price. Unfortunately, the fund's distribution has not always been reliable, although it has increased it rapidly over the past two years:

{kind=link}

We see two distribution cuts here, which are undoubtedly going to be very concerning for some investors. However, they do make sense. The first of these cuts came in 2016, which was a period of transformation for the midstream industry. The energy bear market of 2015 resulted in master limited partnerships being essentially cut off from the capital markets, so they slashed their distributions in order to reduce their debt and become financially self-sufficient. The same thing happened following the pandemic-related lockdowns in 2020 and the crash of crude oil prices that accompanied it. Although neither of these events had a significant effect on the cash flows of these companies, some of them still cut their distributions in order to ensure that they do not have to care what the stock market thinks of them. These events reduced the fund's income, and it was forced to cut the payout because it cannot sustainably pay out more than comes in. The market has generally improved for energy companies over the past two years though, and we have fortunately seen the fund restore its distribution in response. However, anyone buying today does not really have to worry about the fund's past history. This is because anyone buying today will receive the current distribution at the current yield. Thus, the most important thing is how well the fund can sustain its current payout.

Fortunately, we do have a very recent report that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the full-year period that ended on November 30, 2022. This is nice as it should give us an idea of how well the fund performed both in the incredibly strong energy market during the first half of the year and the weakness that we experienced in the second half of 2022. During the full-year period, the Neuberger Berman MLP and Energy Income Fund received $26,217,783 in distributions and dividends along with $20,925 in interest from the investments in its portfolio. A large proportion of this cash inflow came from the various master limited partnerships in the fund though, so it is not considered investment income. As such, the fund reported a total income of $7,078,537 over the full-year period. This was not enough to cover the fund's expenses, resulting in a net investment loss of $1,104,400. As net investment income is the money that is officially available for the shareholders, the fund did not have enough to pay any distribution. However, it still paid out $13,679,731 to its investors. At first glance, this is concerning.

However, the fund's net investment income does not accurately reflect its income. This is because the fund received $19,159,056 in distributions from the master limited partnerships in the portfolio. Although this is not considered income, it is still money that can be paid out to investors. In addition to this, the fund had net realized gains of $21,855,152 and another $129,532,764 net unrealized gains. Obviously, this is more than enough to cover the distributions, and the net investment loss, and still give the fund a great deal of money to be reinvested. Overall, the fund's assets increased by $136,603,785 after accounting for all inflows and outflows. The Neuberger Berman MLP and Energy Income Fund Inc. can easily cover its distribution several times over and there does not appear to be anything to worry about here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Neuberger Berman MLP and Energy Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of a fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy a fund's shares when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of April 4, 2023, the Neuberger Berman MLP and Energy Income Fund had a net asset value of $7.95 per share but the shares currently trade for $6.72 per share. This gives the fund's shares a discount of 15.47% at the current price. This is a very reasonable price to pay for the fund, and the current discount is much better than the 10.09% discount to net asset value that the shares have averaged over the past month. Overall, right now looks like a pretty good time to buy.

Conclusion

In conclusion, master limited partnerships are an excellent way for retirees and other investors to obtain income due to their high yields and overall stability. The Neuberger Berman MLP and Energy Income Fund invests in a portfolio consisting of master limited partnerships and other energy companies in order to provide a high level of income and total return to its investors. It appears to be succeeding at this as its 10.46% yield is highly sustainable and the fund is trading at a reasonable price. Overall, this Neuberger Berman MLP and Energy Income Fund Inc. is worth buying today.

For further details see:

NML: A Solid CEF That Is Worth Buying Today