WES - NML: A Solid Midstream CEF For Income

2023-07-19 15:54:49 ET

Summary

- Midstream corporations and partnerships are excellent assets for anyone seeking income because of their stable cash flows and high yields.

- Neuberger Berman Energy Infrastructure and Income Fund Inc invests in a portfolio of these companies and eliminates tax problems that can accompany them.

- The NML closed-end fund has greatly underperformed the Alerian MLP Index over time but does sport a higher yield.

- The fund's 10.31% yield appears to be well covered for a while as the fund delivered massive gains in 2021 and 2022.

- The fund is currently trading at an attractive discount to the net asset value.

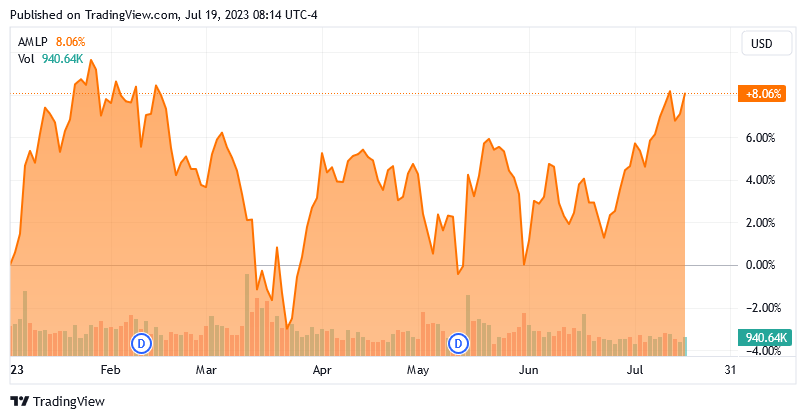

For many years now, midstream corporations and master limited partnerships ("MLPs") have been among the most popular assets in the market for those that are looking for income. There are some very good reasons for this, including the fact that these companies tend to enjoy remarkably stable cash flow over time and pay out a high percentage of their cash flow to their investors as dividends or distributions. The market does not normally assign high multiples to these low-growth firms, so the distribution ends up being a substantial percentage of their stock prices. We can see this quite clearly in the fact that the Alerian MLP Index ( AMLP ) has a current yield of 8.50% despite the fact that the market price has climbed 8.06% year-to-date:

{kind=link}

Unfortunately, there are a few problems with this asset class. First, it can be difficult to include master limited partnerships in a tax-advantaged account such as most retirement accounts. This comes from the fact that these companies can actually expose your retirement account to tax liability. While this problem can be easily avoided by only buying midstream corporations, some of the best companies in the sector are structured as master limited partnerships such as Enterprise Products Partners ( EPD ), Energy Transfer ( ET ), and MPLX LP ( MPLX ). This is a real shame because, otherwise, these companies would be perfect for most retirees. In addition to this problem, it can be difficult to put together a diversified portfolio of midstream companies without having access to a considerable amount of capital. This is a problem that affects pretty much every sector though, not just midstream firms.

One way around both of these problems is to purchase shares of a closed-end fund that invests in midstream companies. These funds are usually structured as corporations, which removes all of the tax problems that you might encounter with including these companies in your portfolio. These funds also provide easy access to a diversified, professionally-managed portfolio of companies in the sector with one easy trade. Finally, a closed-end fund, or CEF, is able to employ certain strategies that have the effect of boosting its yields beyond that of any of the underlying assets and indeed just about anything else in the market.

In this article, we will discuss the Neuberger Berman Energy Infrastructure and Income Fund Inc ( NML ), which is one fund that falls into this category. As of the time of writing, this fund yields a whopping 10.31%. That is more than enough to appeal to any income-seeking investor, and it is more than the Alerian MLP Index. This confirms the statement that I just made about these funds sometimes being able to deliver higher yields than any of the underlying assets. We have discussed this fund before, but several months have passed since then, so naturally a few things have changed. This article will, therefore, focus specifically on these changes as well as provide an updated analysis of the fund's finances. Let us proceed and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the Neuberger Berman Energy Infrastructure and Income Fund has the objective of providing its investors with a high level of total return. This is not particularly surprising considering that this is an equity closed-end fund. As we can see here, the fund's portfolio is entirely invested in common equity with a small allocation to cash:

CEF Connect

The reason why the fund's objective is not particularly surprising in this light is that common equity is by its nature a total return vehicle. After all, investors generally purchase common equity in partnerships and corporations for two purposes:

- To generate income through dividends and distributions paid out by the issuing company.

- To receive capital gains as the issuing company grows and prospers.

This differs somewhat from fixed-income securities as fixed-income securities do not have any inherent link with the growth and prosperity of the issuing company. This fund is apparently not investing in any fixed-income securities though, so we do not really have to worry about this. The fund's description of its investment strategy does not specifically state that it will never include these securities, though. Here is how the fact sheet describes the fund's strategy:

At least 80% of total assets will be invested in master limited partnerships or energy companies, with an emphasis on the midstream natural resources sector, and up to 20% in income-producing securities of non-MLP or energy-related issuers.

The fund's description of its strategy specifically states that it is investing in "income-producing" securities, not common equities. Thus, it could conceivably invest in fixed-income securities issued by master limited partnerships or similar companies. With that said though, it does not usually make sense to do this as common equities issued by most midstream companies actually have higher yields than either preferred stock or bonds issued by the same companies. Common equity also has much more upside potential, so this is almost always the preferable investment. This fund's management seems to agree as currently, only common equity is in the portfolio.

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing midstream partnerships and corporations both on Seeking Alpha and here at Energy Profits in Dividends. As such, the largest positions in the fund are likely to be familiar to most readers. Here they are:

Fund Fact Sheet

I have discussed every one of these companies except for Western Midstream Partners ( WES ) multiple times over the years. As such, the majority of the companies on this list should be quite familiar to all of you. There are a few surprising companies on this list considering that this fund bills itself as an energy infrastructure fund. In particular, Antero Resources Corporation ( AR ) is an upstream exploration & production company that specializes in the production of natural gas in the Permian Basin. It is not a midstream company in any sense of the term, nor does it have the cash flow stability that is inherent in these companies. Here are Antero Resources' annual operating cash flows over the past decade:

{kind=link}

As we can clearly see, the company's cash flows tend to be all over the place due to the impact that natural gas prices have on its revenues. Fortunately, as I discussed in a recent article , the forward growth potential of natural gas is quite good as demand for the substance is rising around the world. That should prove to be a strong positive tailwind for Antero Resources and ultimately give the company some upside potential.

The largest positions in the fund are the same as they were the last time that we discussed it, although a few of the weightings have changed. This could be caused simply by one stock outperforming another in the market and is not necessarily evidence of the fund's management actively trading assets to change the portfolio allocation. The fact that so many of the fund's positions are the same as they were the last time that we discussed it could lead one to assume that this fund has a very low turnover. This is, in fact, the case as the fund reported a 19.00% annual turnover last year. That is one of the lowest turnovers that I have ever seen an equity closed-end fund possess and it is certainly much lower than most other energy infrastructure funds. This is something that is nice to see.

The reason that the low annual turnover is nice to see is that it costs the fund money to trade stocks or other assets. These expenses are billed directly to the shareholders and create a drag on the fund's performance. They also make management's job much more difficult because the fund's managers need to generate sufficient returns to cover these costs and still have enough left over to deliver a satisfactory return to the shareholders. There are very few management teams that manage to accomplish this on a consistent basis, which is one of the biggest reasons why actively-managed funds usually underperform their benchmark indices. This one is certainly no exception as it has generally lagged behind the ALPS Alerian MLP ETF:

| YTD |

| 1Y |

| 3Y |

| 5Y |

| 10Y |

| Since Inception |

| ALPS Alerian MLP ETF |

| 7.34% |

| 22.78% |

| 27.29% |

| 3.62% |

| -0.11% |

| 2.61% |

| NB Energy Infra and Income Fund |

| 1.31% |

| 14.19% |

| 35.39% |

| 3.18% |

| -1.62% |

| -1.34% |

(all returns are NAV total returns as of June 30, 2023)

As we can see, with the exception of the trailing three-year period, the Neuberger Berman Energy Infrastructure and Income Fund has lagged behind the ALPS Alerian ETF. However, this is not a perfect comparison because the Neuberger Berman fund includes some things that are not midstream master limited partnerships, including renewable energy stocks. However, this does still seem like the best index fund to use for comparison purposes. As we can see, an investor generally would have been better off with the index fund, although the Neuberger Berman fund does have a higher yield, which may appeal to those individuals that are not planning to reinvest the distributions.

Leverage

In the introduction to this article, I stated that closed-end funds like the Neuberger Berman Energy Infrastructure and Income Fund have the ability to employ certain strategies that can boost their effective yields well beyond that of anything else in the market or even higher than the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase units of midstream partnerships and corporations. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case. With that said though, the beneficial effects of leverage are not as great today with interest rates at 5% as they were two years ago when interest rates were at 0%. Fortunately, most midstream partnerships have yields that are well above 5% so the strategy still works to boost the effective portfolio yield.

Unfortunately, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I do not usually like a fund's leverage to exceed a third as a percentage of its assets for this reason. This fund satisfies that requirement as its levered assets comprise 17.33% of the portfolio as of the time of writing. Thus, this fund appears to be striking an acceptable balance between risk and reward. We should not have to worry too much about its leverage today.

Distribution Analysis

One of the biggest reasons why investors purchase the common equity of midstream corporations and partnerships is the high yields that these companies usually possess. As already mentioned, the Alerian MLP Index yields 8.50% today, which is one of the highest yields available on any American market index. There are several midstream partnerships that have yields well above even this level, so clearly anyone investing in the sector can easily obtain a high yield. The Neuberger Berman Energy Infrastructure and Income Fund has assembled a portfolio of these companies and then applies a layer of leverage to boost the effective yield of the portfolio.

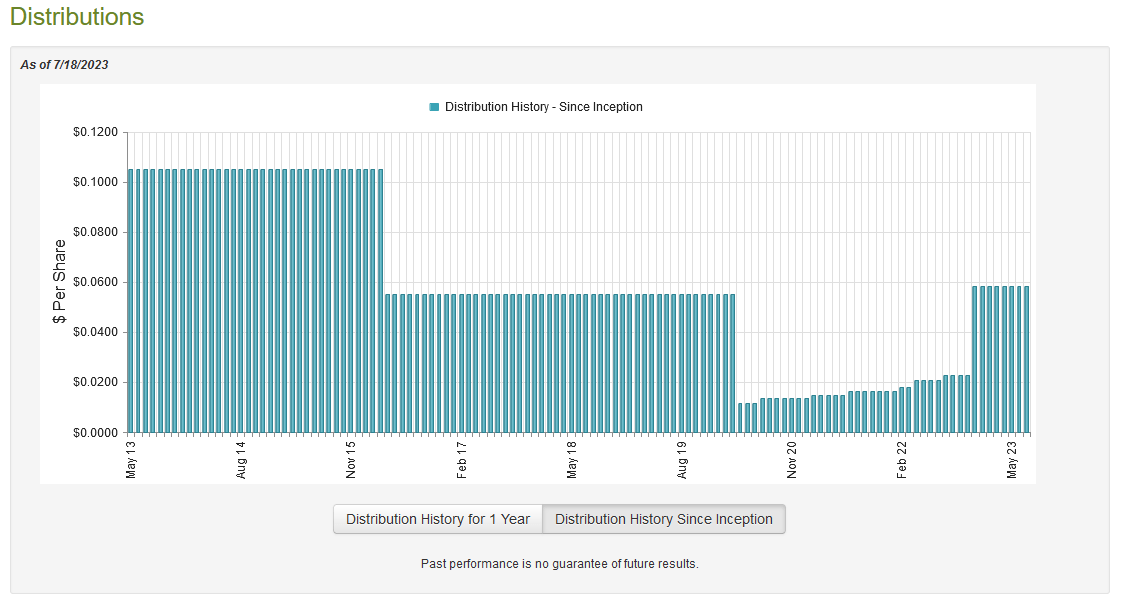

As such, we can assume that the fund itself probably sports a very high yield. This is certainly the case, as NML currently pays a monthly distribution of $0.0584 per share ($0.7008 per share annually), which gives it a very appetizing 10.31% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over the years:

{kind=link}

In particular, we can see that the fund cut its distribution significantly in both 2016 and 2020. This is something that will likely prove to be a turnoff for any investor that is seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. However, the fund's cuts in both of these years are not surprising. As long-time followers of this sector may recall, both 2015 and 2020 were incredibly challenging periods of time for the energy industry. In 2015, the Saudi Arabians were keeping the world oversupplied with crude oil in an effort to crush the emerging American shale industry. In 2020, the pandemic-related lockdowns reduced oil demand and resulted in a similar oversupply.

While most midstream companies were able to maintain their cash flows just fine during both periods, the market essentially became unwilling to supply them with capital. As a result, they cut their distributions in order to strengthen their balance sheets and become entirely self-supporting. The goal is so that these companies would no longer have to care about how the market responds to their attempts to raise capital because they would no longer need to. The distribution cuts and equity declines forced the fund to cut its distributions since it does not want to pay out more than it can actually make from its investments.

One very nice thing that we see here is that the Neuberger Energy Infrastructure and Income Fund has managed to increase its distribution back to the level that it had prior to the 2020 cut. This is much better than most of its peers and speaks well to the skill and shareholder-friendly nature of the fund's management. As is always the case though, it is critical that we ensure that the fund can actually afford the distribution that it pays out. After all, we do not want it to be forced to reverse course and cut the distribution once again since that would reduce our incomes and almost certainly cause the fund's share price to decline, thus wiping out some of our principal. Let us investigate this.

Unfortunately, we do not have an especially recent document that we can consult for this purpose. As of the time of writing, the most recent financial report of the Neuberger Berman Energy Infrastructure and Income Fund corresponds to the full-year period that ended on November 30, 2023. As such, this report will not include any information about the fund's performance over the past eight months. That is a disappointment because the midstream sector has performed reasonably well this year so the fund had some opportunities to earn some profits. The report will still tell us how the fund performed in the second half of last year though, which saw both crude oil and natural gas prices decline fairly substantially.

During the full-year period, the Neuberger Berman Energy Infrastructure and Income Fund received $26,217,783 in dividends and distributions along with $20,925 in interest from the assets in its portfolio. A substantial percentage of this money came from master limited partnerships and so is not considered income for tax purposes. As such, the fund only reported a total investment income of $7,078,537 over the period. It paid its expenses out of this amount, which actually gave it a net investment loss of $1,104,400 during the period.

Obviously, this was not enough to cover any distribution, yet the fund still paid out $13,679,731 in distributions to its shareholders. At first glance, this is likely to be concerning as the fund is clearly not covering its distributions out of the net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, it might have been able to earn capital gains that can be distributed. The fund also received distributions from the master limited partnerships in its portfolio that were not included in the net investment income. As might be expected, the fund did have a great deal of success at earning income from these other sources.

During the full-year period, it reported net realized gains of $21,855,152 and had another $129,532,764 net unrealized gains from the portfolio. Overall, the fund's assets went up by $136,603,785 after accounting for all inflows and outflows. This comes on the heels of a $116,369,608 increase in assets during the previous year. Clearly, this fund had no trouble covering the distribution and will likely be in good shape for a while.

As of November 30, 2022, the fund had total assets of $494,747,950 compared to $241,774,557 on December 1, 2020, despite the fact that this fund never did a capital raise and paid out its monthly distribution the entire time. We have nothing to worry about here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Neuberger Berman Energy Infrastructure and Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of July 18, 2023 (the most recent date for which data is available as of the time of writing), the Neuberger Berman Energy Infrastructure and Income Fund had a net asset value of $7.94 per share but the shares only trade for $6.85 each. This gives the fund's shares a 13.73% discount to the net asset value at the current price. This is quite a bit better than the 11.68% discount that the shares averaged over the past month so the current price looks acceptable.

Conclusion

In conclusion, the Neuberger Berman Energy Infrastructure and Income Fund appears to be a very good midstream fund for anyone that is seeking a high level of income. Unfortunately, it does have a history of underperforming the MLP index, but it has had two very good years and is the only closed-end fund that has fully restored its distribution to its pre-pandemic level. The fund is also trading at a discount to the intrinsic value of its shares. The trade-off here is that Neuberger Berman Energy Infrastructure and Income Fund Inc has a higher yield but overall lower total returns than the most comparable index.

For further details see:

NML: A Solid Midstream CEF For Income