NNBR - NN Inc.: Too Speculative To Merit Its Current Valuation Sell

2023-07-28 00:42:21 ET

Summary

- With an EV of 8 times my estimate of 2023 EBITDA, NN is too richly valued given the optimistic assumptions that are needed for it to provide a solid return.

- NN is a very different business now when compared to its past. After selling its Lifesciences segment in 2020, NN is attaching itself to the EV market.

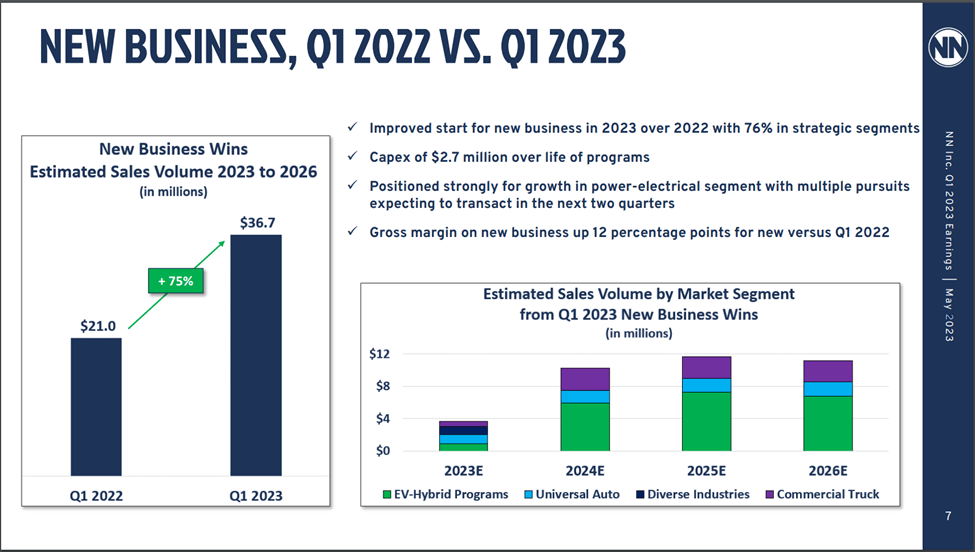

- NN announced a new business win with an EV producer that produced 3 million EV’s in 2022. I believe this producer may be BYD.

- I believe investors sniffed this out after digesting the poor Q1 results and sent the stock up over 200% in the time since earnings were released.

- Even with this new major customer, high-margin growth is far from guaranteed, and the current valuation does not provide investors with enough protection from multiple compression.

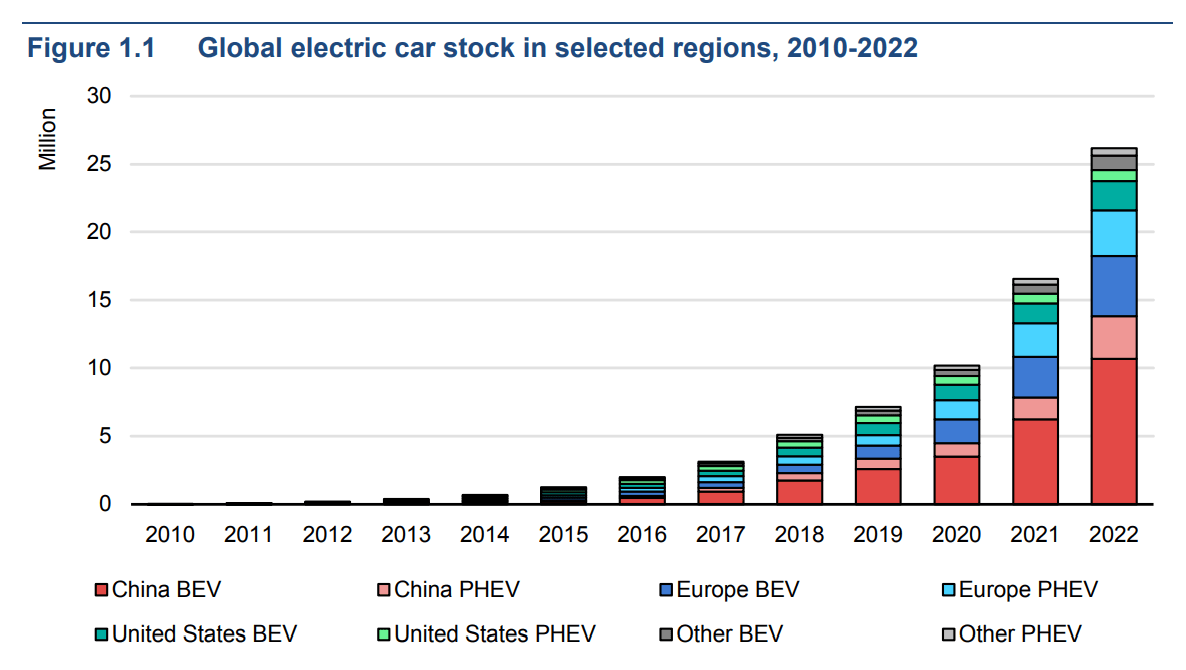

The electric vehicle transition is a known and accepted story, and many investors want a part in it. The reason for this is straightforward: the EV market is already large, growing rapidly and will continue to grow rapidly for decades to come.

Global EV Stock in Selected Regions (International Energy Agency)

{kind=link}

There are many ways to get in on this growth. Investors can put their money into the businesses that manufacture electric vehicles such as Tesla, Inc. ( TSLA ) or legacy automakers that are transitioning to making electric vehicles, they can put their money in businesses that develop batteries such as Enphase Energy, Inc. (ENPH), or they can put their money businesses that develop electric vehicle charging stations such as ChargePoint Holdings, Inc. (CHPT).

These are the more straightforward ways but there are a few ways that are more obscure and involve smaller businesses that are attempting to attach themselves to the growth of a business that has a larger part in the electric vehicle story.

NN, Inc. ( NNBR ) is one of those more obscure ways. While NN is a global diversified industrial company that designs and manufactures products for a variety of industrial end markets, the most exciting part of their story at the moment is their association with the electric vehicle market. Along with the fact that they recently announced that Harold Bevis, the previous CEO of Commercial Vehicle Group, Inc. ( CVGI ) which is a business with an already established electric vehicle story, they announced a new deal with a major electric vehicle manufacturer during the Q1 earnings call and it was the point of most optimism from the management team. This new business win is exciting, but it is unclear what it means for the future of the business and in turn makes NN difficult to value.

This lack of clarity into the potential value of the business leads me to believe that it is best to be conservative when considering an investment into NN. This will be clear when I get into more detail of how I am valuing NN. At this point, after rallying 200%+ after Q1 earnings results, I am rating NN as a sell due to its valuation at 8 times my estimate of 2023 adjusted EBITDA, and the lack of clarity on the value of its new relationship with the major electric vehicle manufacturer. In this article I will discuss the other aspects of NN's business, its past financial performance, and more details about its valuation and why I am assigning a sell rating to the stock.

Business Overview

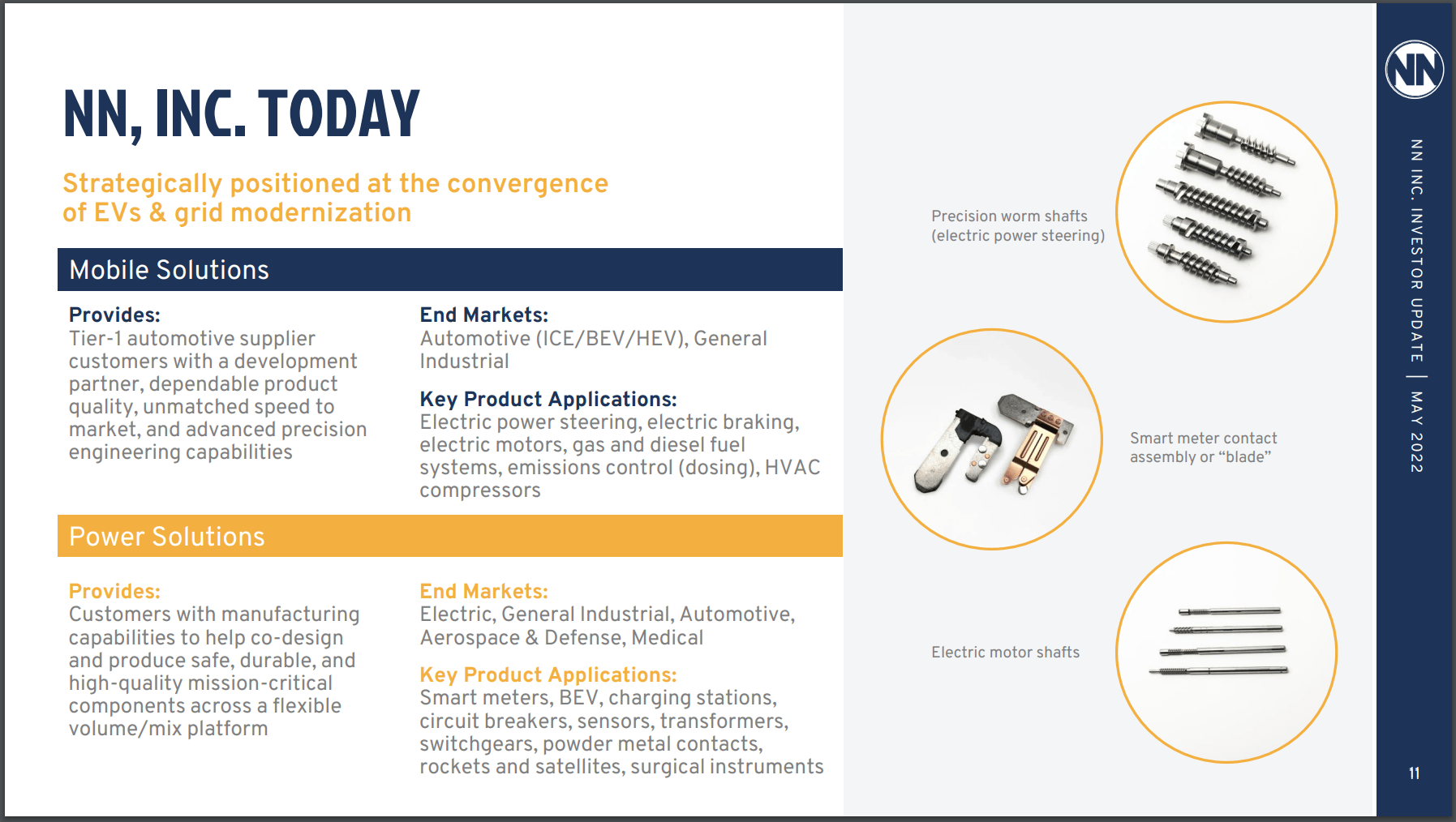

Despite the excitement about its involvement in the electric vehicle market, NN has a history of manufacturing products for a variety of industrial end markets. Currently, NN breaks its business down into two segments, Mobile Solutions and Power Solutions.

The Mobile Solutions segment is focused on growth in the automotive and general industrial end markets and includes the manufacturing of components on a high-volume basis for use in power steering, braking, transmissions, and gasoline fuel system applications, along with components utilized in heating, ventilation, air conditioning, diesel injection and diesel emissions treatment applications. This is the segment that includes business for manufacturers of battery electric, hybrid electric, and internal combustion engine vehicles.

The Power Solutions segment is also focused on the automotive and general industrial end markets, but also focuses on electrical and medical end markets. For this segment they manufacture a variety of products including electrical contacts, connectors, contact assemblies, and precision stampings for the electrical end market and high precision products for the aerospace and defense end markets. Their medical business includes the production of tools and instruments for the orthopedics and medical/surgical end markets.

NN, Inc. Product and Market Overview (2022 Investor Day Presentation)

{kind=link}

The Mobile Solutions segment is larger than the Power Solutions segment in terms of total sales, it is less profitable and more capital intensive. On a consolidated basis, a majority of sales comes from the United States, but NN also does business in China, France, Mexico, Brazil and Poland.

{kind=link}

Past Financial Overview

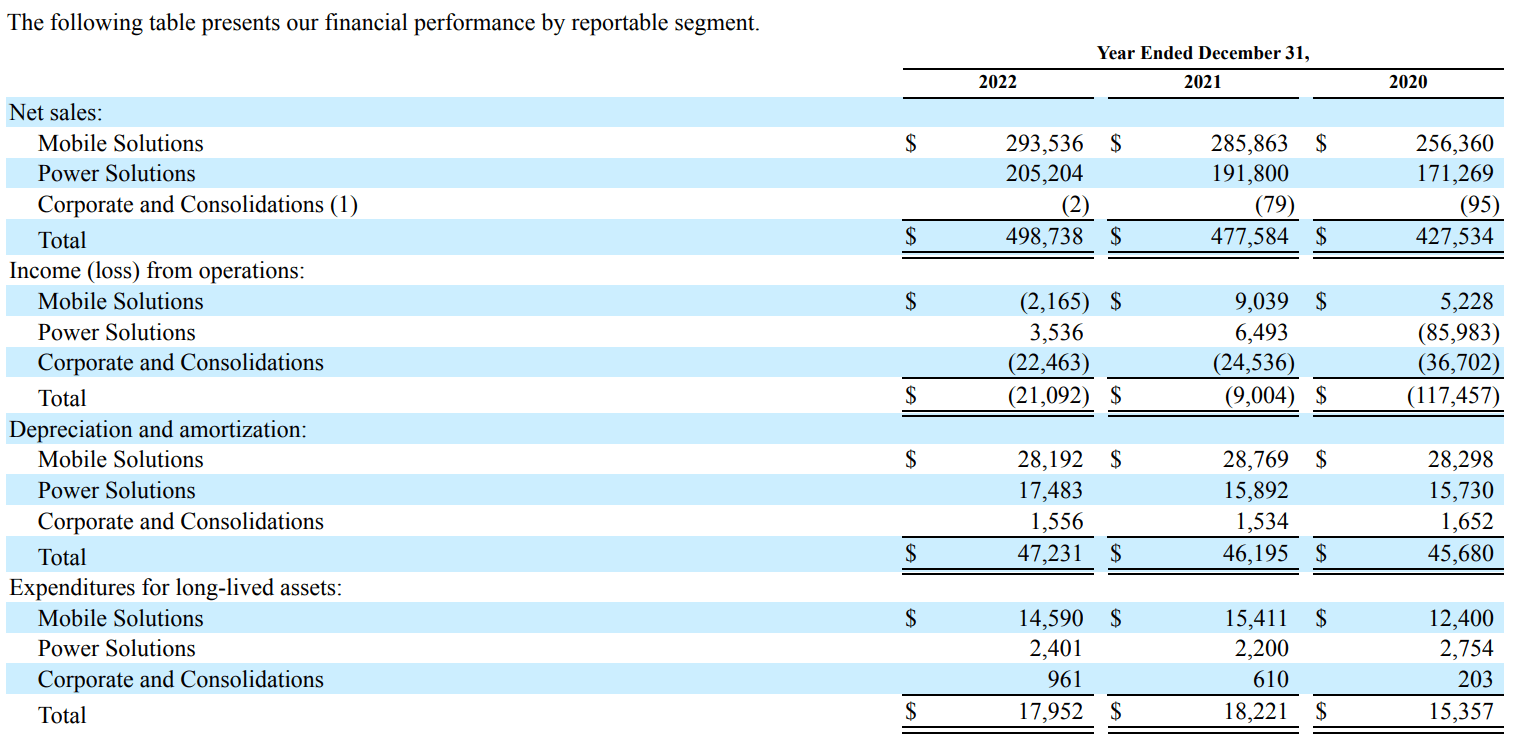

Comparing year to year financials for NN over the past decade is not very meaningful due to the constant M&A and divestitures of different parts of the business. It has essentially operated as a publicly traded LBO firm with a focus on industrial end markets. It has not had much success in this endeavor.

There have been a few major transaction over the past decade. NN acquired Precision Engineered Products in late 2015 for $615 million. As a result of this acquisition, the shares outstanding increased by about 30%, NN's total debt more than doubled from $328 million to $800 million and EBITDA grew 68% from $54 million in 2015 to $91 million in 2016. This was the FY peak in EBITDA as it gradually declined to $25 million in 2022. The stock has followed and is down 90% from its peak in early 2017 following peak EBITDA in 2016.

In early 2018, NN took on more debt and issued equity to acquire Paragon Medical for $375 million. Despite this, EBITDA again dropped in 2019 and NN eventually sold their entire Lifesciences segment for $825 million in 2020. Most of this cash went to paying off debt.

The stock peaked in 2017, with an EV of $1.5 billion and trailing EBITDA of about $120 million which put it at 12.5 times EBITDA.

While it's important to know the history of the business, all of these transactions along with the many changes to the board of directors and management team makes it almost meaningless to compare the current business to the business of the past. This will lead me to compare NN more to a peer in the electric vehicle component space. In general, what this past performance can tell us is that there is no history of solid business performance and good capital allocation for investors to rely on.

New Strategy and Valuation

NN's new strategy and story is centered on growth in the electric vehicle market which makes the newly revealed new business win with a manufacturer that produced 3 million EV's last year very exciting. The only EV manufacturer that I could find that has a production capacity of 3 million vehicles is BYD so I suspect it could be the manufacturer in question. I believe this is what has driven the 200% rise in the stock since the Q1 earnings release.

NN's stock actually dropped following the results due to poor Q1 results and lowered 2023 guidance, so I believe investors eventually sniffed out this potential BYD detail after digesting the results and the info from the conference call.

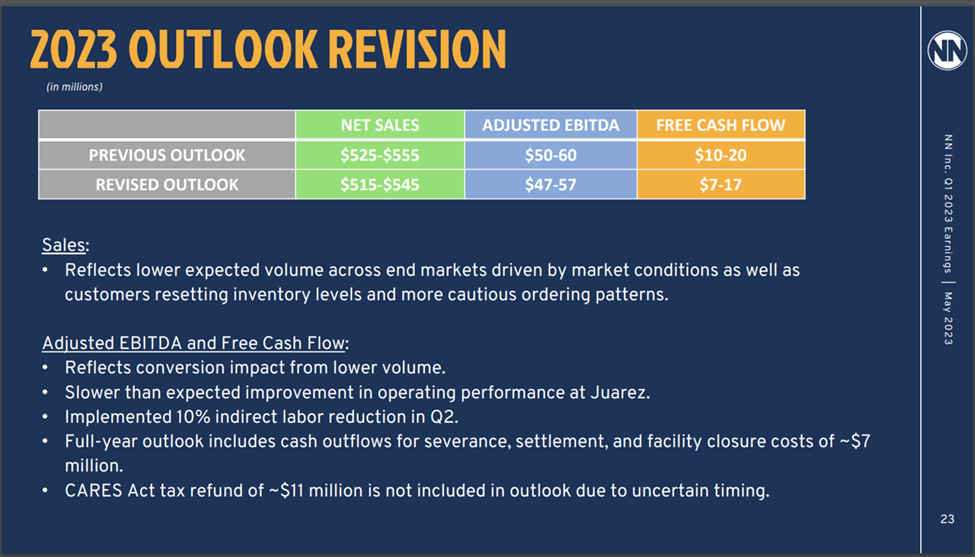

Adjusted EBITDA guidance was lowered from a range of $50-60 million to $47-57 million. Q1 adjusted EBITDA was a disappointing $8.1 million which I will optimistically call $35 million annualized as I am assuming more growth in new business wins as the year goes on. Add to this $11 million in savings for facility closures, and $4 million in savings for layoffs, both of which will become accretive to EBITDA starting in Q2, and I expect 2023 adjusted EBITDA of $50 million. This would come in at the lower end of guidance and makes the forward EV/ EBITDA ratio equal to about 8.1.

{kind=link}

What an investor thinks of this valuation should depend on their view of NN's future growth in the EV space and NN's relationship with the mystery EV manufacturer. If they believe that the Q1 new business win rate will continue for the next few years, then it should seem reasonable.

For example, if the new business win rate grows at 50% over the next two years and this new revenue has a 15% EBITDA margin, it would add $12 million of EBITDA to my expected $50 million for $62 million of total EBITDA in 2025, all else equal. If NN then traded at 12 times EBITDA, its EV would be $744 million which would provide investors with a return of 20%+ per year through 2025.

{kind=link}

Additionally, the valuation would seem reasonable depending on the value of NN's relationship with the manufacturer that I think is BYD. It's difficult to value something like this because this contract currently is only providing $3.5 million in sales at program peak, which is not enough to make a large dent in NN's financials. Management however was quite optimistic about it on the call. Chief Commercial Officer Andrew Wall provided some details on the outlook:

It's an awesome win for us… And what that already has represented is now that they've seen what we can do, what our capabilities are, how we do things, how we're ramping up the business, we're already seeing a number of other opportunities from that same customer, right? So, we're in that early stage, proving ourselves out, but based on the size of where this particular customer is, we anticipate this opening. It's a really good market for us and they're a true leader in the space.

This all seems very positive for NN, but the assumptions that lead to 20%+ returns per year are quite optimistic. A look at another player in the EV component space shows that the current multiple is more than reasonable.

Commercial Vehicle Group's EV is 6 times projected 2023 EBITDA and it is historically a more stable business with better interest coverage. It does get a large portion of its revenue from the production of Class 8 heavy duty trucks which is very cyclical and extremely sensitive to GDP so it may deserve the lower multiple. But as an industry peer, I don't think NN deserves double the multiple given its unproven track record and lack of solid financial results in its past.

Additionally, basing the value of the business on potential future contracts with BYD is a bit too speculative for me. If the valuation was more in line with that of Commercial Vehicle Group, this potential BYD relationship could be seen as more of an OTM call option. However at the moment it seems too speculative to build assumptions of potential future contracts into a valuation of NN.

At the low point after Q1 results, NN was trading at an EV/EBITDA ratio of 6 based on my estimate of 2023 EBITDA. While getting back to this valuation would require a drop of almost 65%, I think an investment closer to that valuation provides proper protection against multiple compression.

It seems that insiders shared this belief as there was significant insider buying from March-May 2023 when the stock was around $1 per share. Additionally, the new CEO, Harold Bevis, was previously the CEO at Commercial Vehicle Group which also has a large EV opportunity. He may have left for any number of reasons, but it could signal that he was more confident in NN's future in the EV space.

Final Thoughts

After the stock's 200% rise after Q1 earnings, I think that NN is valued too richly at 8 times my estimate of 2023 adjusted EBITDA and I am assigning a sell rating to the stock. The company is unproven based on its history, and much of the valuation seems to be driven by very optimistic assumptions of organic growth at high margins, and speculation regarding a relationship with a major EV producer which I believe to be BYD.

I would recommend to buy the stock closer to 6 times 2023 EBITDA. This is in line with Commercial Vehicle Group which is, despite being more sensitive to changes in GDP, more stable on an earnings basis, and is better able to cover its interest expense. This valuation would require a very large drop in the stock but it provides investors with much more protection against multiple compression if the optimistic growth and margin assumptions don't pan out.

For further details see:

NN, Inc.: Too Speculative To Merit Its Current Valuation, Sell