NNN - NNN: My First 'Buy' In The REIT Here's Why

2023-08-29 02:04:33 ET

Summary

- National Retail Properties has a strong track record with 33 consecutive years of dividend increases and a high credit rating.

- The company focuses on owning single-tenant freestanding retail properties and has a high occupancy rate of 99.4%.

- Despite potential risks, such as exposure to struggling tenants like Walgreens, NNN remains confident in its ability to collect rent, and I agree with this assumption.

Dear subscribers,

I haven't offered comprehensive coverage of National Retail Properties ( NNN ) until now. My coverage of the space has mostly been in peers and other investments, which have traditionally constituted the bulk of my capital investing in the subsector. However, with valuations compressing and things being what I would call underappreciated, I'm starting to see a lot of value in this sector once again.

Back when the office sub-sector crashed, I invested heavily in quality names like Boston Properties ( BXP ), Highwood, ( HIW ), Kilroy ( KRC ), and Alexandria ( ARE ). ARE alone now constitutes over 1% of my total portfolio.

Some RoR of those investments since I bought?

Boston is up 34.12%. Highwood is up 21.48%. Kilroy is up 29.27%. Alexandria, the largest, is up 7% - but that's more of a slow burner.

My point is, buying undervalued when they're undervalued is a good way of getting some very impressive returns. But you need to be there when things go down the toilet, so to speak.

In this article, I'll look at National Retail Properties and give you my take now that we're definitely declining.

National Retail Properties - A Look at the Business

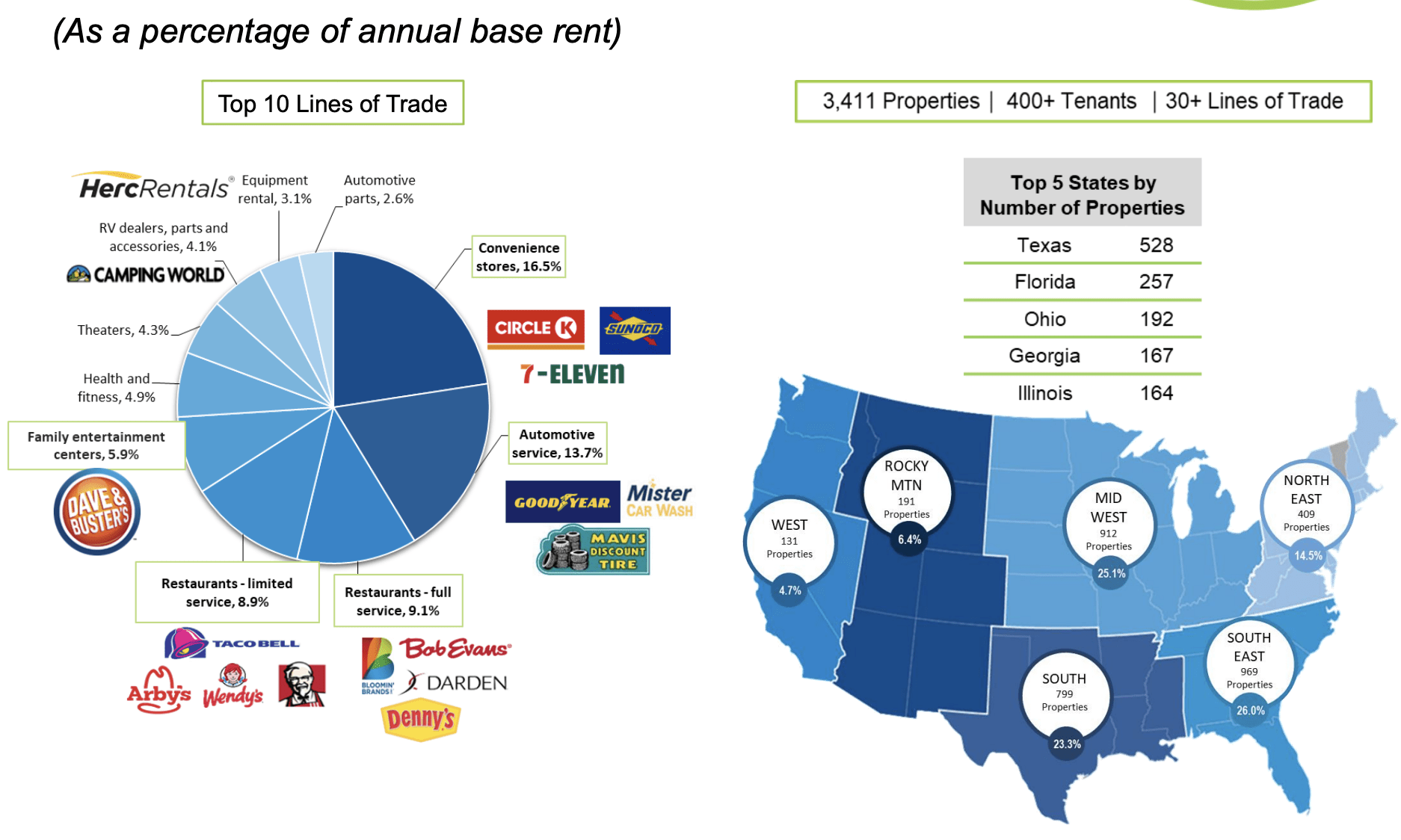

33 consecutive years of dividend increases from 3,4111 properties with a total of 35.0 million square feet. Investment-graded balance sheet by both S&P Global and Moody's, an EV over $12B, and WALT of over 10 years with an occupancy of 99.4%.

This dear readers, is National Retail Properties.

The company is headquartered in beautiful Orlando FL, and as of this morning when I am writing this article, yields a massive 5.63% yield. This is from a BBB+ rated REIT.

The company's dividend comes at a very conservative sub-70% FFO payout ratio, and the high credit rating is indicative of just how good the company's fundamentals are. Its 38-year+ operating history means it has sustained through every conceivable situation, and its long-term debt is very attractively structured.

The company's strategy is simple. Owning, long-term, single-tenant freestanding retail properties, but no malls or strip centers. The company avoids E-commerce risky businesses, in order to sustain a high occupancy and retain a high property value on average. On a tenant level, there's both geographical and sector diversification. Heaviest, we'll find the company in the South, Midwest, and Southeast, with only minor exposures in the West and some in the Northeast and the Rockies. From that perspective, I like the company's overall exposure.

{kind=link}

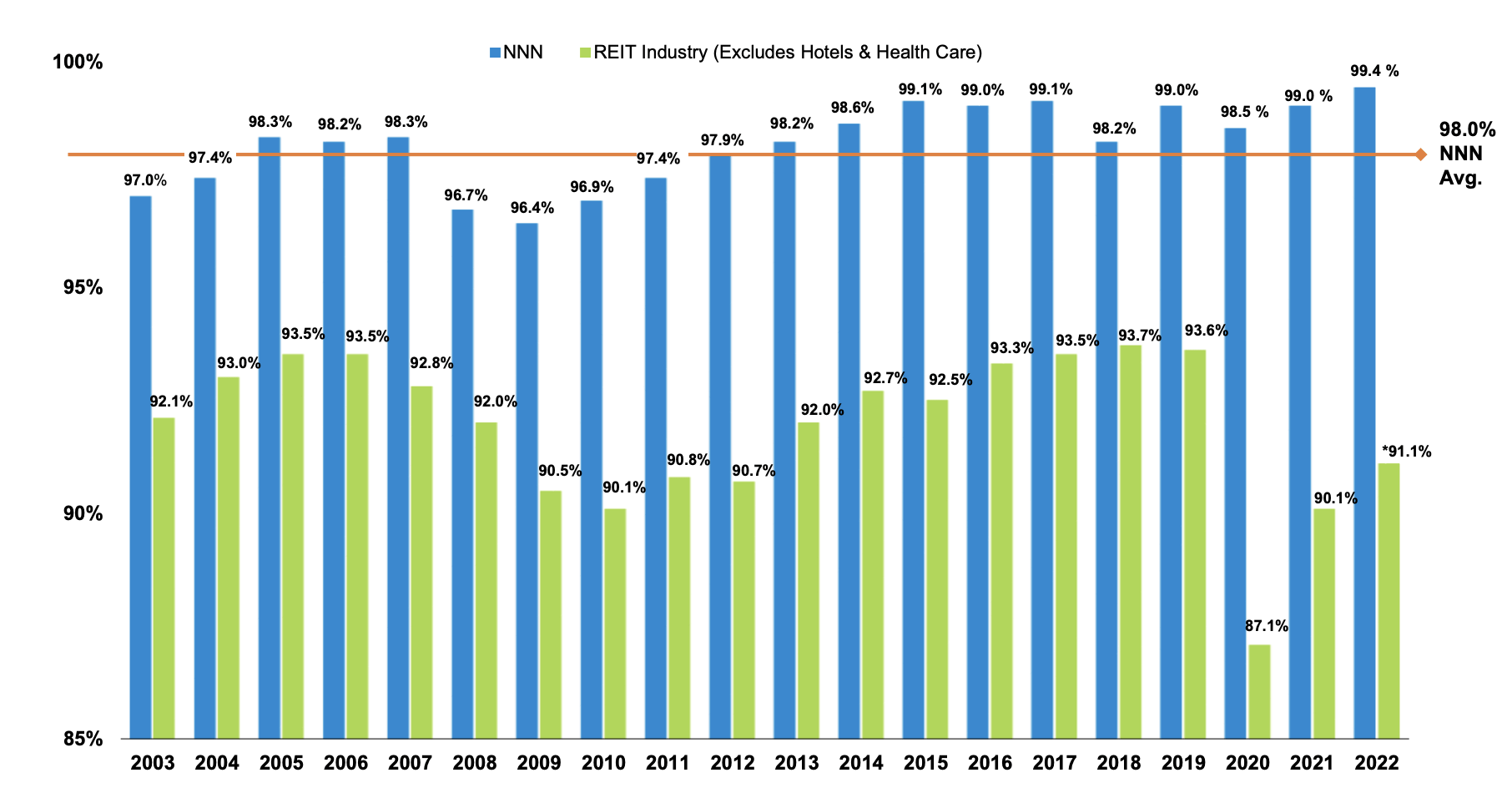

Going by what's happened over the past weeks, you might expect based on share price movements, that NNN has seen significant occupancy drops or maybe even a dividend cut. This is not the case. The company consistently outperforms the REIT industry average occupancy, which is of course an immense positive. The high occupancy at this time despite what the market is showing is another feather in the company's cap.

{kind=link}

The company has never fallen below 96.4% in occupancy. Lease expirations, as mentioned, are extremely conservative. Less than 4.5% expire through 2024, with over 55% after 2031. As long as the underlying companies remain solid, rent will continue to come in.

The company very recently reported its results, reporting a 1.3% FFO growth on a per-share basis. Investment yields are still solid at 7.2% cash yield. The company's portfolio occupancy also did not shift a hair, but remains at a strong 99.4%, the 4th consecutive quarter this has been achieved. This is above the company's own target of 98%. In terms of pure assets, only 22 assets are currently vacant.

The company's active M&A pipeline and performance confirm the fact that NNN is continually able to make deals that make sense financially. Cap rates seem to reach their plateau level here, starting to stabilize over time. Selling also "works", with NNN selling at an average of 5.1% cap rate, easily investable into accretive acquisitions at a 7.1% 6-month cap rate. The YTD difference is around 1.5% compared to the 6-month divestment cap rate of 5.6%. Many of the properties the companies divest are vacant. It's important to note though that there's a widespread in the disposition cap rates. Some of the sales were actually executed at a cap rate higher than the acquisition average, as high as 7.5%, more defensive sales - but then there were a few sales in the low 4% range which brought it down. With thousands of assets with varying ages, there's bound to be a wide difference in quality here.

Due to the company being one of the oldest in the sector, it has no issues with debt or financing at this time.

{kind=link}

The impact that's causing the share price to move down is likely a mix of lack of high-end guidance increase due to AFFO drag due to overall capitalized interest expense, and increased use of company credit lines which at 6% interest (even without the next hike) is relatively sub-optimal compared to other forms of funding that are not so exposed to float.

Some of the company's risk also includes exposure to Walgreens (WBA), which is experiencing store closures. Unlike some other retail REITs we cover, the company has more exposure to tenants that could be considered at a sub-optimal level of financial health. Bed, Bath & Beyond is another example. Not many stores here - with BBB, the company only had 3 stores, or about a 0.2% exposure on an ABR level. When it comes to Walgreens, here is the company's answer less than 2 days ago.

Yes, yes. Walgreens, I'm not worried at all about their ability to pay rent. I guess that's the most important thing. They did announce store closures, none of ours are in that list. And so we don't have any concerns at all on that front. And just a reminder, even to folks, investors, even if a tenant closes a store, the rents did -- the first. It doesn't change their obligation to pay us rent for those properties. And so -- but -- and this particular case, Walgreens, we don't have any closed stores on their closure list.

(Source: Kevin Habicht, NNN Earnings Call)

I'd keep a bit more on this, as I don't believe the headwinds for Walgreens are cursory or temporary, but more of an overall negative trend. That is why I am not investing in Walgreens, and why I've actually been out of the company for several years. Clearly, this is not a near-term impact, and I share the confidence in the company's ability to pay its rent - but it's worth noting that NNN has a bit more exposure than others to sub-optimal tenants. This constitutes, I would say, the biggest risk for investors in NNN - but to me, isn't enough of a risk to keep me interested in the business.

It's worth noting that the properties with tenants that went bankrupt were at a relatively high rent on a square foot basis for what they were - so replacing BBB will become a challenge, even at just 0.2%.

But this shouldn't impact or cloud your view on the company as a whole, or from a valuation perspective.

Here's how valuation is currently looking for the company.

NNN REIT Valuation - A lot to like, a lot of upside

The upside at this juncture and valuation is very compelling to me. The company typically has a valuation of around 16-17x P/FFO, depending on what sort of timeframe you look at. With the company's BBB+ and around a 4% yearly FFO growth rate on a 20-year basis this is "okay".

However, in the current interest rate environment, I'd be looking for a better valuation to offset some of the rate risks. When we can get 4-5% risk-free, I'm not paying 13-15x P/FFO for 5.63% - that's a simple fact. Not unless there's a significant upside.

As the company has now dropped, we're starting to see some of that compelling upside.

Even just on a 14.38x P/FFO basis, we're now at a near-14% annualized RoR with an annual FFO growth of just 2.94%. Typically, I want at least 15% annualized on a conservative basis if I am to put my capital to work outside of options strategies. The reason I consider this one a "BUY" here is that I view 15x P/FFO as valid due to the company's quality and history - and 15x turns this investment to a 15.2-15.3% annualized, depending on what sort of estimates you give. However, you don't have the basis to really give this company any issues with any of its forecasts.

Why?

Because NNN or its analyst do not miss targets. They hit them. 100% of the time, both on a 1-year and 2-year basis, without fail.

NNN Forecast accuracy (F.A.S.t Graphs/FactSet)

I view this recent normalization in share price as necessary. it wasn't that the upside wasn't there prior to the decline - but for conservative investors like me, the upside in this recent rate environment, wasn't high enough to justify putting capital to work. It was too high estimates and assumptions to reach my 15% annualized.

That's no longer the situation we have. While I'd be thrilled to be able to get NNN below that $40/share mark now that we have 2Q, I view this as unrealistic. As I'm writing this article, the company is already rising in the pre-trade, and I'll be lucky to get it under $40/share.

13 S&P Global analysts follow NNN REIT. These give the company a range from $41 low to $54 high, with an average PT of $48/share. 6 out of 13 are at "BUY" or "Outperform" here, but this is not updated for the trend of the latest week, and I believe tit would/will look different here.

The current company's NAV estimates put it at a mean of $44.47/share (Source: S&P Global). That means you're getting the company at a NAV discount - no analyst believes them worth less than $39.5/share, and some would go as high as $52/share. Again, a NAV discount and discounts are what we want in this operating environment.

The combination of valuation discounts, recent trends, a well-covered yield of over 5.6%, sector-leading accuracy ratings and management quality manages to "beat" the fact that some portions of the portfolio are less qualitative than peers, and the fact that growth seems almost guaranteed to be sub-4% in the next few years.

If you're fine with long-term ownership of quality retail at a 5.6% yield with a reversal potential that could easily go 15% per year at a historical FFO discount, then NNN is a choice you may want to look at.

As of the market opening today, I will add shares of NNN to my portfolio. I consider the company a "BUY" here. At iREIT we have a "BUY" at around $48/share. I would look at buying it below $44/share to maintain this conservative upside, but if this is done, then this is a "BUY" to me.

Here is my thesis on NNN

Thesis

- NNN REIT is one of the longest-existing retail REITs. It has a quality portfolio with exposure across the US, good tenants, very good fundamentals, and a solid yield of over 5.6% at the time of writing this article.

- At a conservatively-calculated FFO upside, this has a potential outperformance of 15% or above annually inclusive of the yield - and this is what I look for. That makes the company, as I see it, into a solid income investment with the potential to outperform the market.

- Because of this, I give the company a "BUY" rating here and a PT of $44/share. I'd trim above $52/share. The company isn't the best in terms of growth, but it's worth more than the market is currently assigning to it.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

At around $40/share, I do consider the company cheap - and so, it fulfills all of my investment criteria.

For further details see:

NNN: My First 'Buy' In The REIT, Here's Why