VNQ - NNN REIT Still Looks Undervalued And Yields Over 5%

2024-01-19 09:00:00 ET

Summary

- Goldman Sachs predicts S&P 500 to hit 5,100 in 2024, indicating a continued rally.

- National Retail Properties presents an opportunity as shares trail VNQ and have an attractive valuation and yield.

- NNN has a strong occupancy rate, utilizes triple net leases, and has a track record of annual dividend increases.

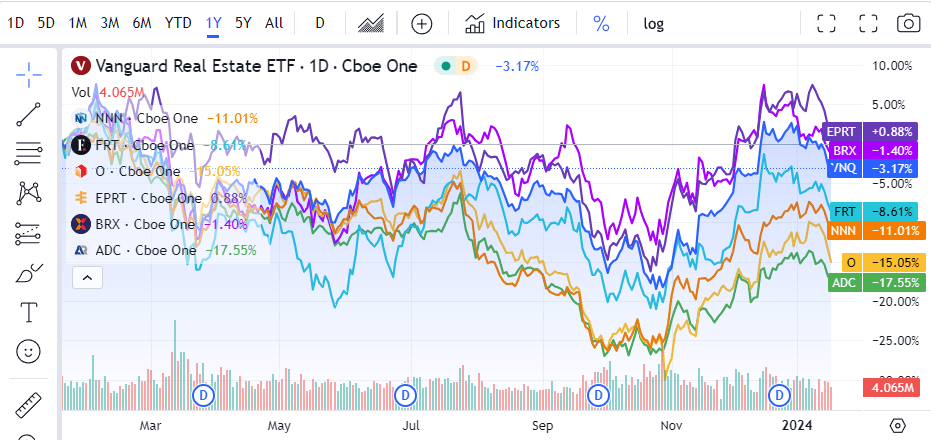

We're off to a choppy start in 2024 after finishing 2023 on a high note. In December, Goldman Sachs ( GS ) came out with their 2024 forecast and saw the S&P 500 hitting 5,100 , indicating the rally will ultimately continue. While tech is still red-hot going into earnings season, I am still of the opinion that we will see a broad market rally rather than a replication of 2023, where most of the gains were generated by a handful of stocks. While real estate investment trusts ((REIT)) jumped sharply off their November lows, the Vanguard Real Estate Index Fund ETF ( VNQ ) is still trailing the S&P 500 by a wide margin as it's still down -3.12% over the previous year. When it comes to generating income, REITs are at the top of the list, especially since I have no desire to own rental properties and be a landlord. I would much rather allocate capital, sit back, and collect the dividends while someone else deals with the headaches. I have been tracking which REITs have been lagging VNQ, and I believe there is still an opportunity in shares of National Retail Properties ( NNN ) as shares still trail VNQ while trading at an enticing valuation and yield.

{kind=link}

Following up on my previous article on NNN

My last article on NNN was published on October 10th, 2022 ( can be read here ), and since then, shares have appreciated by 7.52% while having a total return of 14.99% when their dividends are factored in. I had discussed the macroeconomic factors that were impacting REITs in addition to outlining NNN's moat and why I felt it was undervalued. I am following up on this idea now that we have more data on a macro level. I think that REITs will continue to rebound in 2024 and that NNN presents an opportunity as shares trail VNQ and some of its peers that have less attractive valuations.

National Retail Properties is my preferred way to generate income from commercial real estate than direct ownership

I hear many people discussing how great investing in real estate is, but I rarely hear about the hardships and headaches that come with it. Real estate is a great asset class, but outside of my personal real estate, I don't want to have anything to do with the day-to-day operations. The idea of buying a home, a multifamily location, or a commercial real estate property has always been enticing, but I am not handy, I don't have much spare time, and I don't want to deal with tenants. For some people, real estate is a phenomenal investment, and while my personal property has appreciated in value, I am not looking to complicate my life by investing in additional real estate. This is why I invest in an array of REITs. I own several REITs including ones that specialize in malls, office buildings, medical facilities, and commercial properties. I may not make as much as if I took the risk of owning and operating a property by myself, but a company such as NNN allows me to sit back and collect a modest dividend while getting a raise every year. I would rather invest in NNN and get a professional team that can handle every aspect of the operation than have the responsibility falling on me.

{kind=link}

When I purchase shares of NNN, I am purchasing a REIT that has 3,511 properties across 49 states. There are a lot of important factors when it comes to real estate, but at the top of the list is the occupancy rate, in my opinion. If a real estate asset is purchased with the intention of being rented to generate income, you need it to be occupied otherwise, you're carrying the payments. Since 2003, NNN has never fallen below 96.4% and during the entire 2020 year, NNN had an occupancy rate of 98.5% while the REIT industry, excluding hotels and healthcare, fell to 87.1%. This is important to me because it indicates how desirable NNN's locations are and the quality of their tenants. NNN Is very diversified as it has a tenant mix that exceeds 400, with companies such as 7-Eleven occupying 138 of its locations. I can't remember the last time I saw a 7-Eleven close, to be honest.

The other significant detail for me is, just like the ticker symbol, NNN utilizes triple net leases, which are my favorite structure in the REIT sector. Triple net leases typically require the tenant to pay property operating expenses such as insurance, utilities, repairs, maintenance, capital expenditures, real estate taxes, and assessments. They are generally longer leases, with initial lease terms of 10-20 years. In my opinion, this leaves less to chance and takes a significant portion of the risk out of the equation.

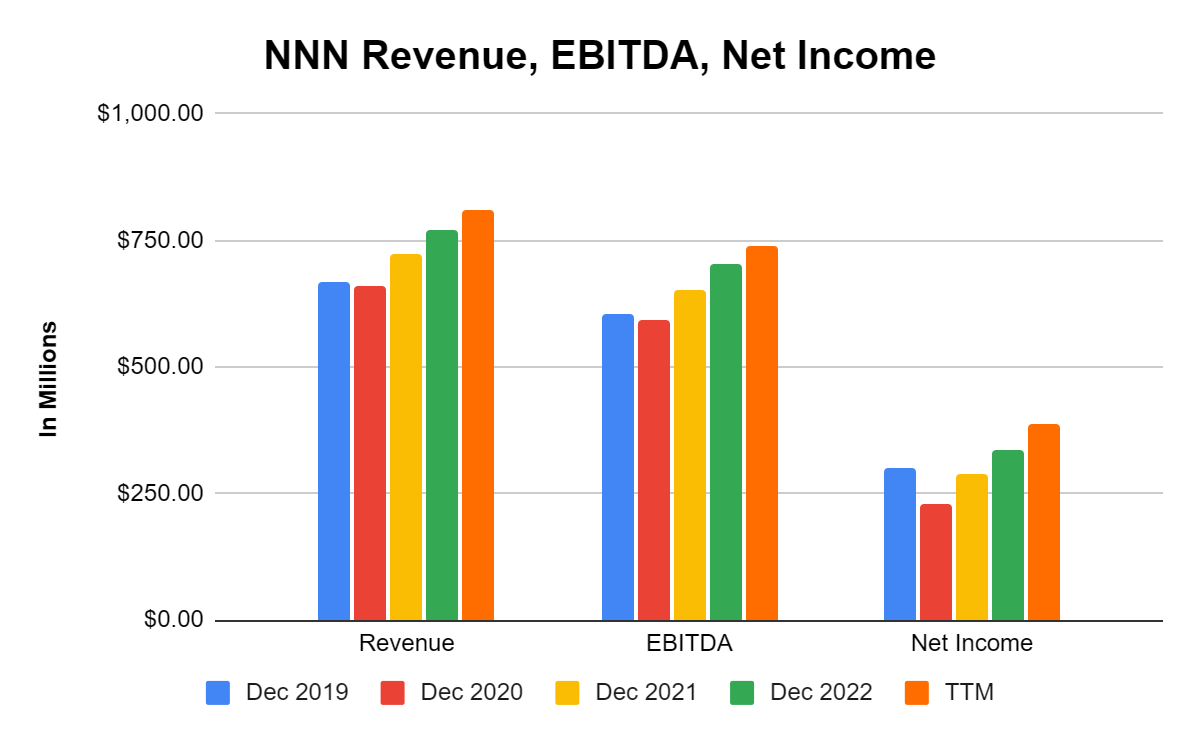

This structure has been beneficial to NNN, and the proof is in the numbers. As a REIT, net income isn't necessarily a measure that investors look at, but I am adding it in for good measure. NNN's revenue, EBITDA, and net income barely took a hit during 2020 and have been growing ever since. In the trailing twelve months (ttm) they are operating at a 91.33% EBITDA ratio and a 47.74% profit margin. NNN has great margins and is efficient at driving profitability from its revenue.

{kind=link}

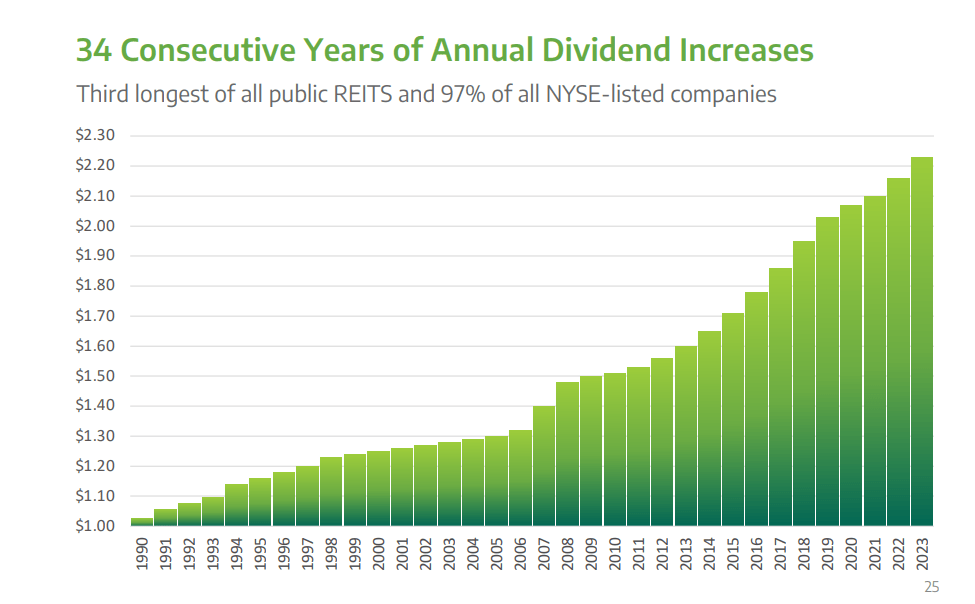

NNN's efficiency at turning a profit and their expertise in real estate have put them in a position where both their top and bottom lines have been able to expand. This has correlated to over 3 decades of annualized dividend increases for shareholders. Today, NNN is paying a dividend of $2.26 per share, which is a 5.33% yield. Its dividend has a 5-year growth rate of 2.72%. By owning NNN, I am a shareholder in 3,511 properties, and I am collecting a quarterly dividend without having to do any of the work.

The Fed is expected to cut rates at some point in 2024, and while some are calling for a March cut, I think May is more realistic. Either way, the Fed has signaled they are at the end of the tightening cycle, which means sooner than later rates will decline. This should be a tailwind for REITs in general as the cost of capital declines and the pressure from refinancing maturing debt at elevated levels dissipates. I believe that investors will also move the capital from the sidelines back into the market, and when they do, companies such as NNN, with 34 years of consecutive dividend increases, will look very attractive to generate income.

{kind=link}

National Retail Properties looks undervalued compared to its peers

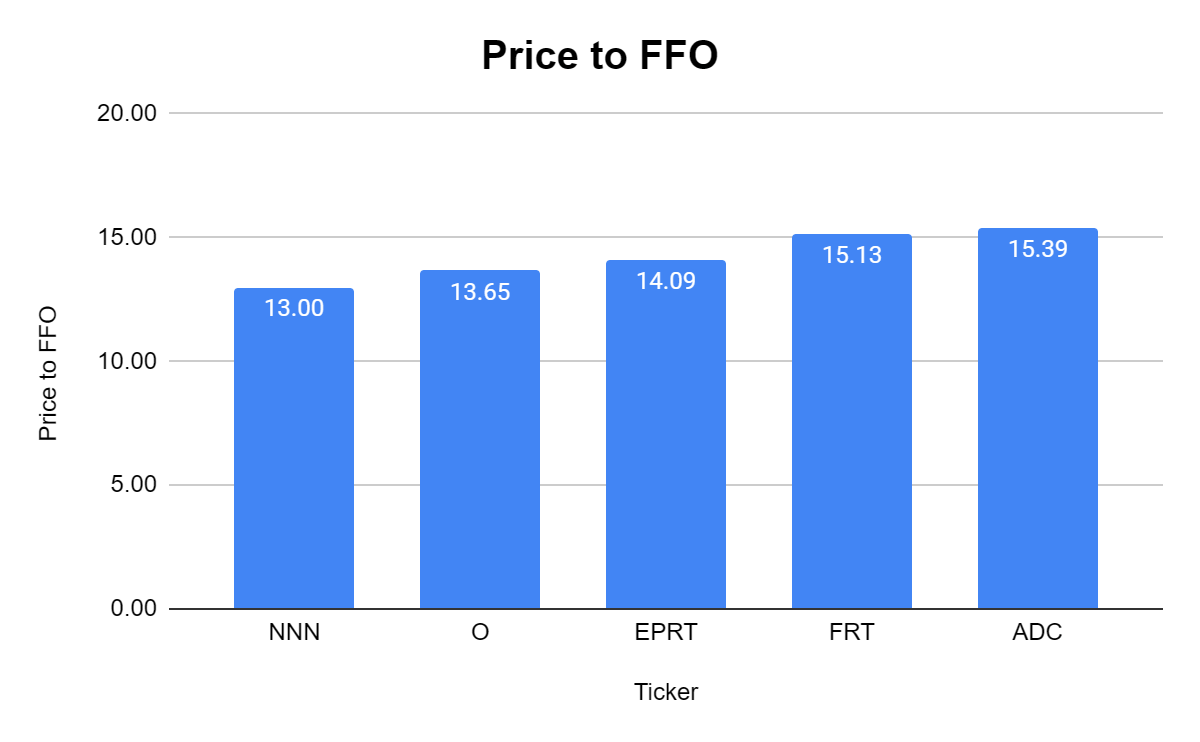

I compared NNN to several other REITs, and I looked at their price to Funds From Operations ((FFO)), net debt to EBITDA level, dividend yield, and the FFO dividend coverage ratio. FFO is the equivalent of EPS for REITS, and this is why I use the FFO metric. I compared NNN to Realty Income ( O ), Federal Realty Investment Trust ( FRT ), Essential Properties Realty Trust ( EPRT ), and Agree Realty Corporation ( ADC ).

I want to pay the best price possible for a REIT's FFO, the same way value investors want to pay a low P/E for traditional equities. NNN is trading at 13 times its FFO, which is the lowest in the peer group. The peer group average is 14.25x, placing NNN at an enticing valuation.

{kind=link}

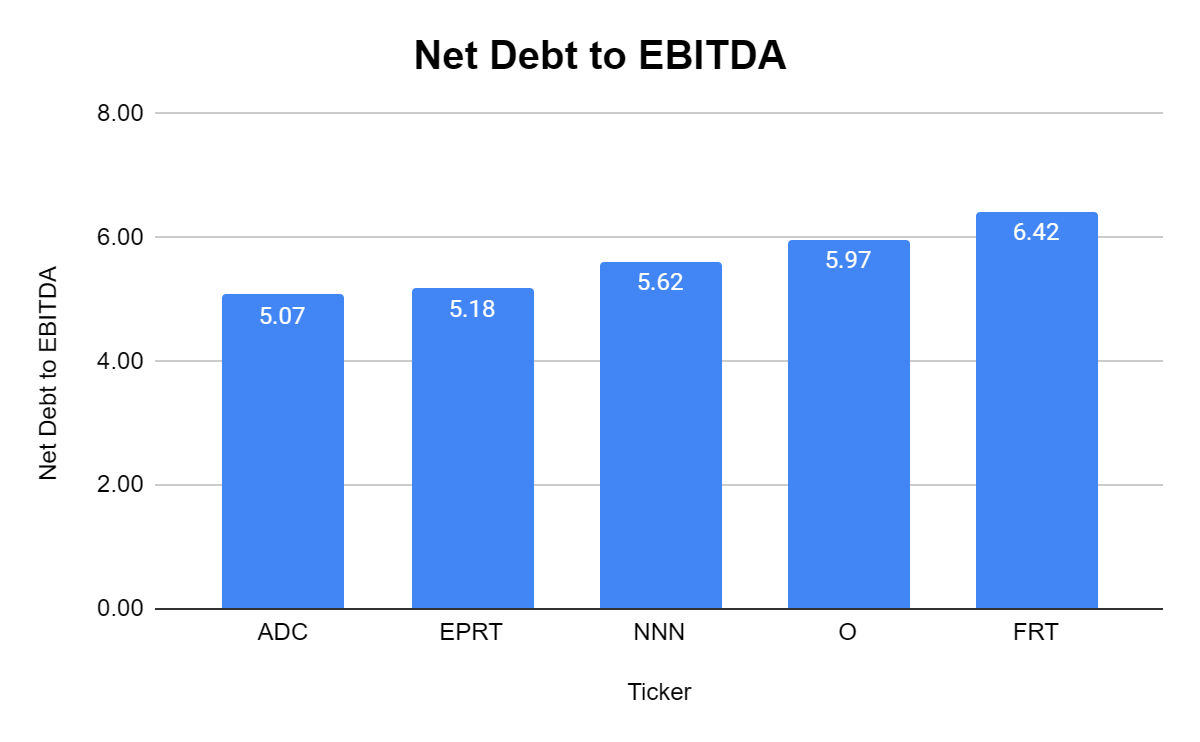

I also look at the net debt to EBITDA ratio to make sure that a REIT isn't too leveraged for my risk appetite. NNN trades at a net debt to EBITDA level of 5.62x, which is just under the peer group average of 5.65x. Due to its level of profitability and debt maturity structure, I am happy with a 5.62x net debt to EBITDA ratio for NNN.

{kind=link}

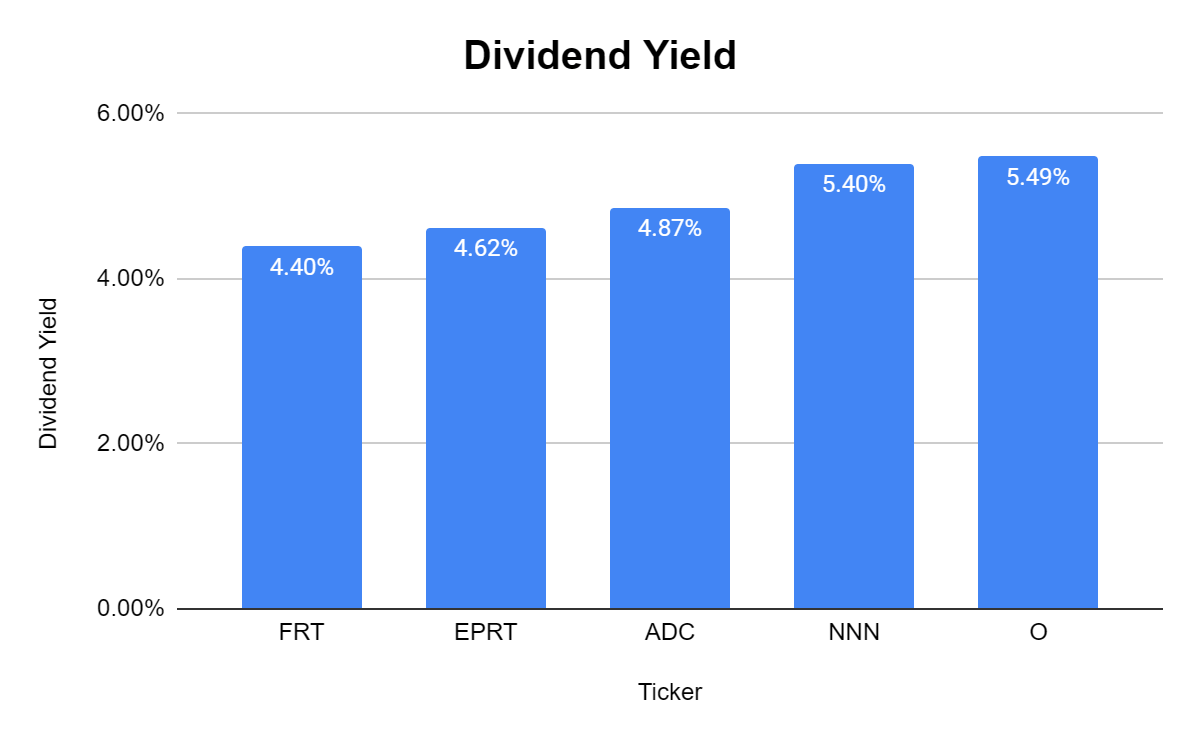

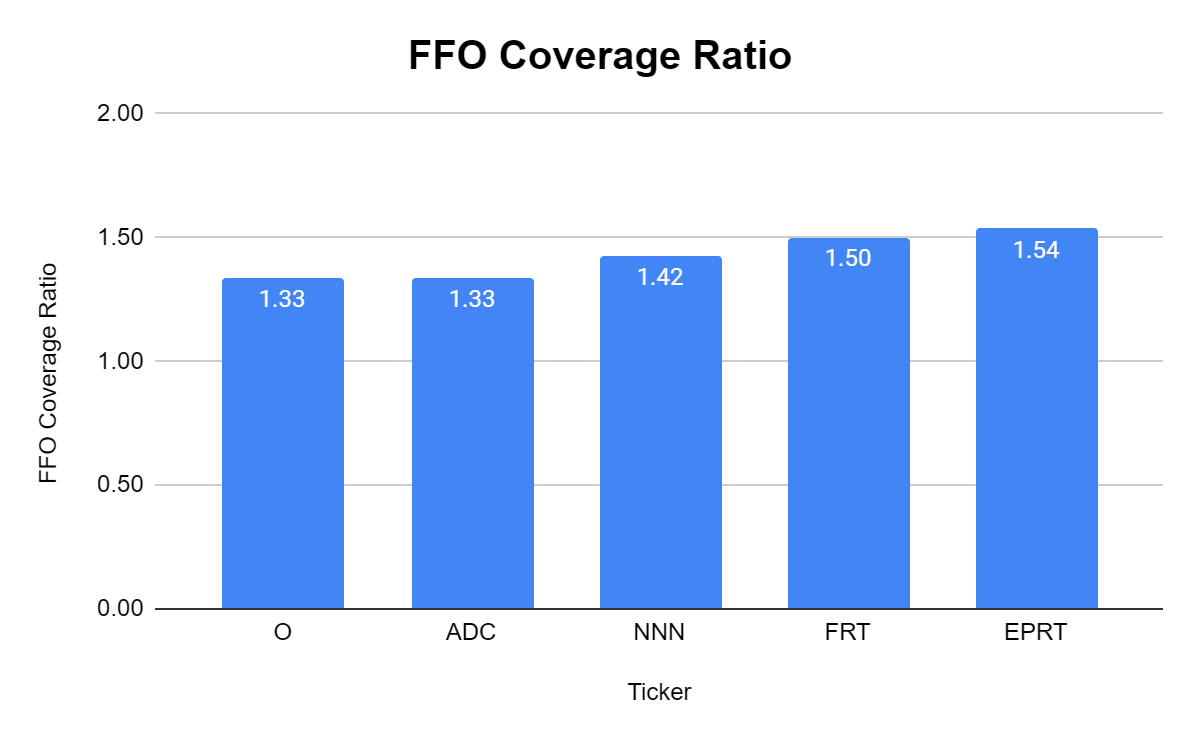

Most investors are probably investing in REITs to generate income. I want to make sure I am being compensated for allocating my capital toward REITs, considering there are other income investments I can make. NNN has a dividend yield of 5.4% which is above the 4.96% peer group average. This is more than enough yield to keep me interested as I am getting an increase every year, causing my yield on cost to expand. I also need to look at the FFO dividend coverage level as the dividend is being paid from the FFO generated. NNN is producing 1.42x the amount of FFO they are paying in the annual dividend. This indicates that the dividend is healthy and there is room for future growth.

{kind=link}

{kind=link}

Risks to my investment thesis

While I am bullish on NNN, and their underlying metrics look solid, there are still risks to the investment thesis. Investing isn't just about numbers, as market sentiment plays a large role in the overall results. Over the past 5-years, NNN has declined by -15.23% as it has never gotten back to its pre-pandemic levels. We have endured a pandemic, geopolitical tensions, and macroeconomic uncertainty. Within the macroeconomic landscape, there has been higher inflation and interest rates. The biggest risk to my investment thesis at this point would be the macroeconomic landscape, which is completely outside of NNN's control. If inflation continues to tick higher, it could cause the Fed to hold rates higher for longer or retract their previous statements about being at the end of their cycle. If inflation goes higher for even a short period of time, the Fed may use that as fuel and unexpectedly hike rates due to the change in data. If that occurs, the REIT sector will probably sell off as we will be back to the narrative of writing down assets, and foreclosures on properties. NNN has a great track record, and their maturity schedule is strong, but they would be lumped in with the group, and if the Fed takes rates higher, then REITs will likely sell off.

Conclusion

I think that 2024 is going to be a strong year for income-producing assets once a cut occurs. As of now, CME Group is factoring in a 57.1% chance of a rate cut in March and a 100% chance in May. As rates start to decline, I think capital will flow into the markets, and a portion will look to find a home in income-producing assets with growing dividends to recreate the yields they were getting from risk-free assets. I think REITs will come back into favor, and names like NNN will be very attractive as it is still trailing VNQ while having a 5.33% yield with a growing dividend. I am planning on adding more shares to my position prior to the Fed cutting rates.

For further details see:

NNN REIT Still Looks Undervalued And Yields Over 5%