JEPI - No DIVO And JEPI Are Not Underperforming They Are Performing As Expected

2023-05-01 00:19:35 ET

Summary

- Covered call ETFs are underperforming rising stock markets.

- The low volatility negatively impacts the income from selling calls.

- But actually, covered call ETFs are simply performing as expected.

- The VIX can be expected to return to its long-term average and rising equity markets are a tailwind for covered call ETFs.

Both the JPMorgan Equity Premium Income ETF ( JEPI ) and the Amplify CWP Enhanced Dividend Income ETF ( DIVO ) are underperforming the S&P 500 and the VIX Index is low, which negatively impacts the income from selling calls. Should we sell both ETFs?

Our answer is a clear “No!”.

“Underperformance”

Our previous article about JEPI and DIVO started as follows: “Covered call writing is a defensive, low(er) beta, strategy. When the markets rise, you get a nice return. That return will probably lower than the return of the equity markets itself, but that’s something you know in advance. “

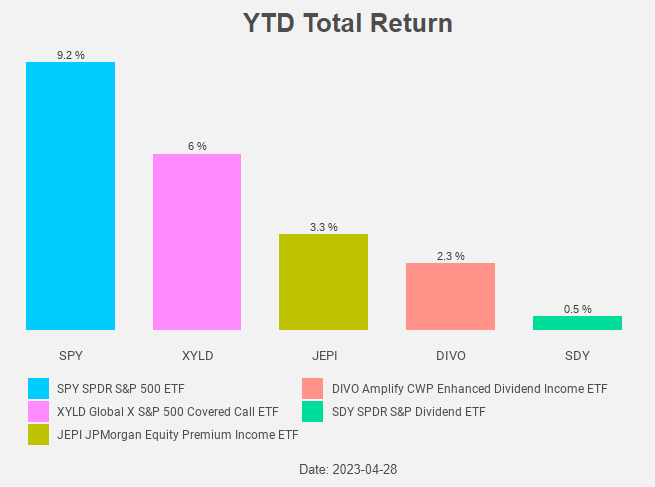

And that’s exactly what we see this year. The equity markets are rising and covered call ETFs have a positive total return that is lower than the return of the equity markets itself.

{kind=link}

The Global X S&P 500 Covered Call ETF ( XYLD ) is performing better than JEPI and DIVO because it has a passive approach. It simply buys the complete S&P 500 and writes calls every month on the index.

JEPI and DIVO have a more actively managed concerning stock selection. DIVO buys 20 to 25 high-quality large-caps with a history of dividend growth. JEPI has a less concentrated defensive equity portfolio that employs a bottom-up fundamental stock selection. JEPI considers also financially material Environmental, Social and Governance ((ESG)) factors.

No investment style can outperform all the time and currently defensive strategies like dividend growth are underperforming.

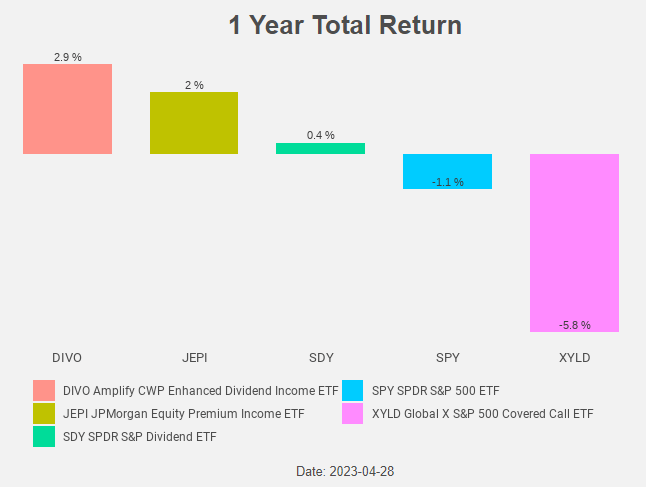

Over the past 12 months DIVO is still creating more than 3% alpha and JEPI almost 3%!

Figure 2: DIVO Contribution analysis (Finominal)

Figure 3: JEPI Contribution analysis (Finominal)

And both DIVO and JEPI have a history of alpha creation.

Figure 4: DIVO Alpha creation (Finominal)

Figure 5: JEPI Alpha creation (Finominal)

JEPI is only in existence since May 2020. For a longer lookback on the alpha potential we can take a look at sister-fund JPMorgan Equity Premium Income Fund Inst ( JEPIX ).

Figure 6: JEPIX Alpha creation (Finominal)

The results for JEPI and JEPIX aren’t as stellar as DIVO’s, but the alpha potential is clearly there.

All-in-all, we can only conclude that given the performance of the market and the performance of more defensive strategies, both DIVO and JEPI aren’t underperforming, they’re simply performing as expected.

Rising equity markets are for us even a prerequisite to invest in covered call ETFs. When the equity market really goes down, a covered call strategy can’t shield you from a negative return. That’s why we prefer not to invest in such a strategy when the equity market is in a long term down trend. This is not the case now. Rising stock markets are a tailwind for covered call ETFs.

{kind=link}

VIX is low

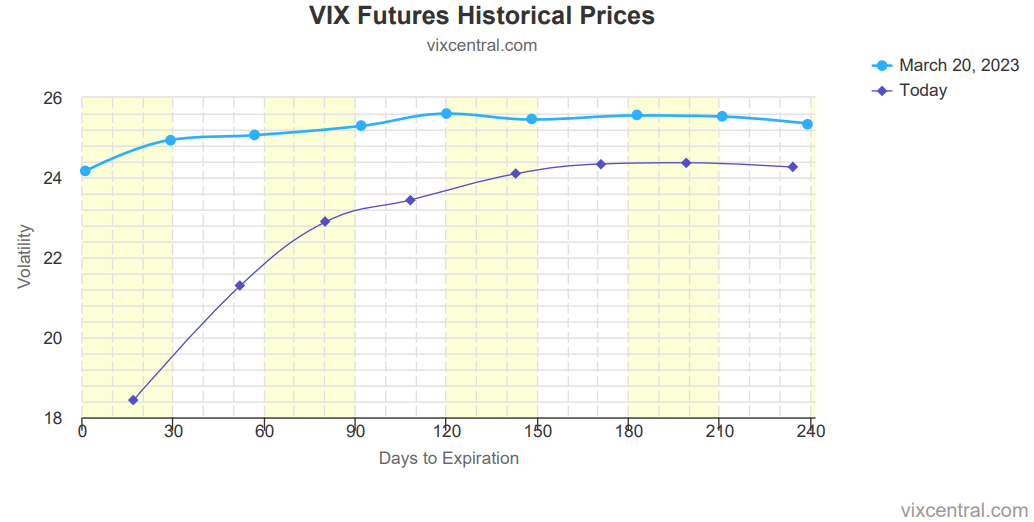

The VIX index is at a rather low level (15.78) now after the spike due the banking crisis. This low volatility negatively impacts the income from selling calls for covered call ETFs.

Figure 8: VIX Index (CBOE)

The VIX Index is known to be mean-reverting. Its level is expected to trend toward its long-term average over time. Unlike e.g. stock indices, volatility cannot move lower or higher indefinitely. So we can expect the VIX Index to move higher in the near future and this expectation is also visible in the term structure of the VIX futures .

{kind=link}

For XYLD the level of the VIX is rather irrelevant. It simply buys the complete S&P 500 and writes calls every month on the index, no matter what the level of the VIX index is. Of course, the higher the implied volatility, the higher the premiums they can collect when writing options.

DIVO has not only an active approach concerning stock selection, but also regarding its covered call writing strategy. Based on market observations and income targets, the portfolio managers use a rules-based set of triggers to identify the best covered call opportunities on the stocks in their portfolio. They look for opportunities to write covered calls when the VIX is at 15 or higher. And this is currently still the case. And like we said before, we can expect the VIX to trend higher back to its long term average.

Although I read in a recent article on Seeking Alpha that JEPI uses both covered call options and equity-linked notes (ELNs), this is in fact not the case. JEPI only uses ELNs to implement its covered call strategy. These are derivative instruments that are specially designed to combine the economic characteristics of the S&P 500 Index and written call options in a single note form and are not traded on an exchange. Compared to DIVO, JEPI uses its covered call strategy more systematically and this allows them to pay out higher dividends while it limits at the same time a bit more the upside potential of the underlying portfolio.

The use of ELNs exposes JEPI to counterparty risk if any of the counterparties would go bankrupt. The counterparties mentioned in the prospectus are diversified and well-known names like Barclays, BNP Paribas, Citigroup, Goldman Sachs and Royal Bank of Canada and … Credit Suisse. We don’t know if JEPI had any ELNs outstanding with Credit Suisse as a counterparty. We do know that the counterparty risk cannot be neglected. On the other hand, the stress seems to ebb regarding those big counterparties.

Figure 10: Credit default swaps (Bloomberg)

So, regarding the covered call strategy of DIVO and JEPI we can only say that they are (also) performing as expected.

{kind=link}

Conclusion

Covered call ETFs like DIVO and JEPI are underperforming the rising stock market. But this a completely normal behaviour, not a bad performance. Covered call ETFs give up some upside potential in exchange for option premium income. We even prefer to invest in covered call ETFs only when markets are moving up or sideways (because covered calls only offer limited downside protection). Rising stock markets are a tailwind for covered call ETFs.

The VIX Index is currently rather low and this negatively impacts the option premium income somewhat. But it’s only a matter of time before the VIX will return to its long term average. So also on this level, covered call ETFs are performing as expected.

The current state of the stock markets and the VIX allow us to reiterate our view on both DIVO and JEPI: buy.

For further details see:

No, DIVO And JEPI Are Not Underperforming, They Are Performing As Expected