BORR - Noble Corporation: Strong Quarter Raised Guidance Undemanding Valuation - Buy

2023-11-16 00:18:24 ET

Summary

- Leading offshore driller Noble Corporation reported strong Q3 results with revenues and profitability reaching new multi-year highs.

- The company raised full-year guidance and increased its quarterly dividend by 33% to $0.40 per share.

- Cash generation was impacted by higher working capital requirements, and Noble warned of more near-term white space in the company's contracting schedule.

- Management remained confident in the industry's long-term prospects and expects the upward trajectory in day rates to resume once previously sidelined capacity has been absorbed.

- While offshore oil and gas service stocks have been volatile as of late, I consider the recent setback an opportunity to start scaling into the shares.

Note:

Noble Corporation Plc ( NE ) or "Noble" has been covered by me previously, so investors should view this as an update to my earlier articles on the company.

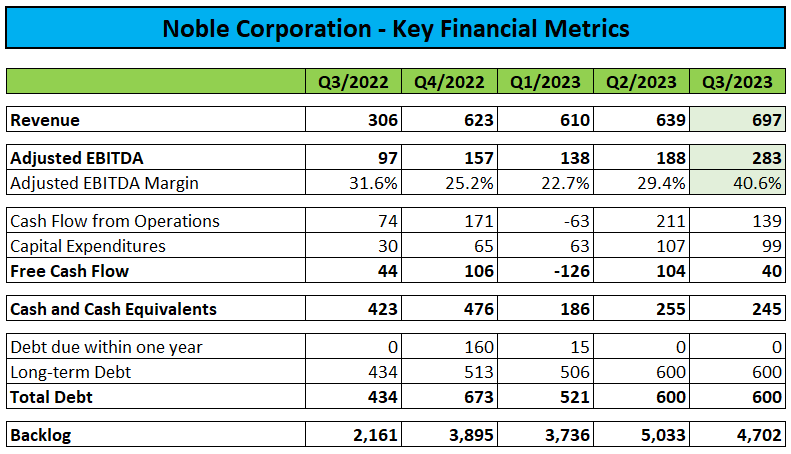

Earlier this month, leading offshore driller Noble Corporation or "Noble" reported strong third quarter results with revenues and profitability reaching new multi-year highs:

{kind=link}

The company's sixteen marketed floaters were 92% utilized during the quarter up from 90% in Q2 with the average day rate increasing to $404,000, up from $363,000 in Q2. Noble's thirteen marketed jackups were 61% utilized with an average day rate of $141,000 in the third quarter as compared to 59% and $129,000 in Q2.

Adjusted EBITDA of $283 million increased by 50% sequentially with margins exceeding 40%.

However, the strong operating performance failed to translate into improved free cash flow generation due to required working capital investments as outlined by management on the conference call :

As our past few quarters have shown, the quarterly variability of working capital can create some short-term swings in free cash flow. During the third quarter, we generated $40 million of free cash flow despite over a $100 million build in working capital. While some of this is a function of a growing top line, we do expect a portion of this bill to reverse in Q4.

In addition, backlog was down 6.5% sequentially to $4.7 billion but management wasn't really concerned about the decrease:

As shown, our backlog stands at $4.7 billion currently, down slightly from $5 billion as of last quarter. However, excluding our long-term commitments from Exxon Mobil in Guyana and Aker BP in Norway, our backlog was essentially flat quarter-over-quarter.

Accordingly, we're much more focused on the quality of backlog additions rather than an absolute dollar total, as we progress through time and we remain overall quite constructive on the re-contracting opportunities confronting our available rigs.

In contrast to some of its peers, Noble's floater fleet is not exposed to low-margin legacy contracts as evidenced by the company's average floater backlog day rate of $408,000.

Moreover, approximately 62% of available floater days will be up for re-pricing next year with a meaningful part relating to four drillships on long-term contracts with Exxon Mobil ( XOM ) offshore Guyana.

Weaker Short-Term Outlook

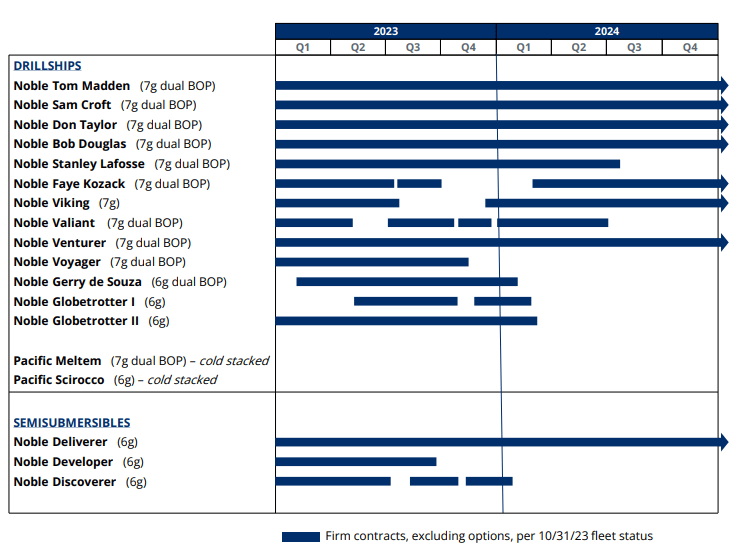

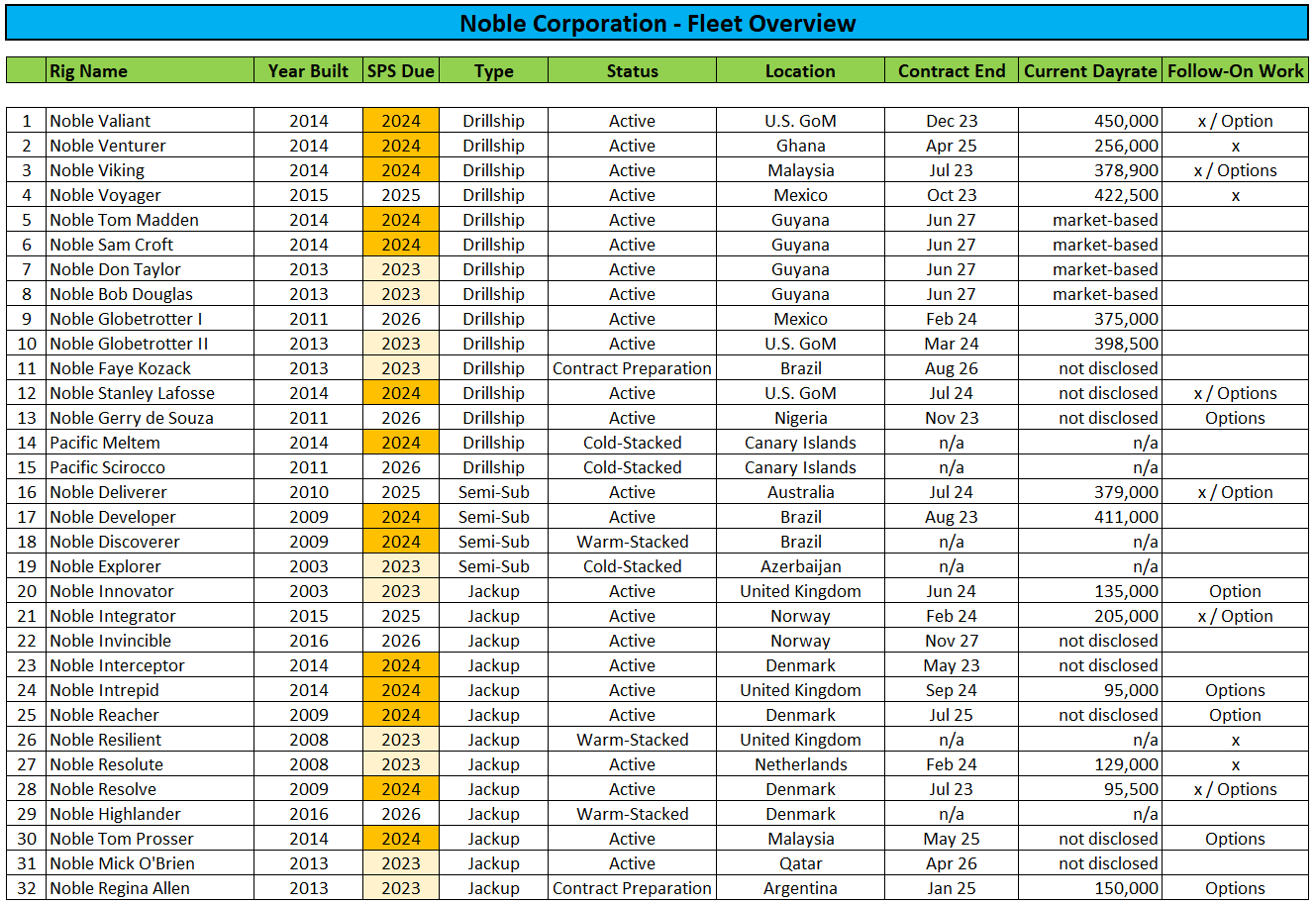

That said, management warned of " more white space " in the near- to medium-term for the drillships Noble Voyager , Noble Globetrotter I and II as well as the semi-submersible rig Noble Developer.

While the Noble Developer is already sitting idle in Brazil and Noble Voyager is expected to roll off contract later this month, the company recently secured small extensions for the Noble Globetrotter I and II with both rigs now contracted well into Q1/2024.

Noble also added a six-month contract for the drillship Noble Valiant in the U.S. Gulf of Mexico at a day rate of $470,000.

{kind=link}

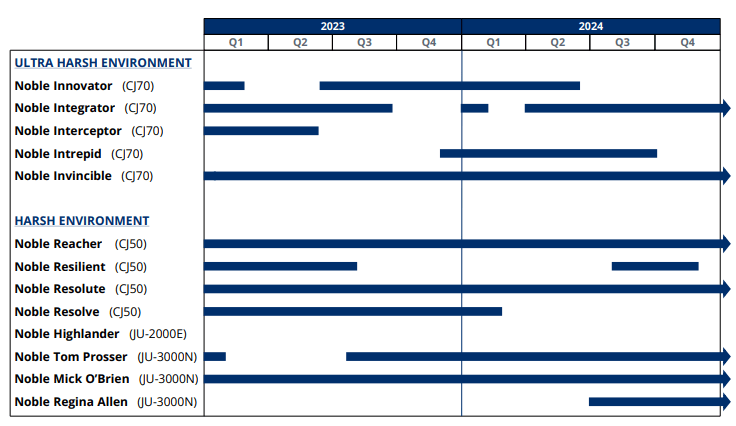

On the jackup side of the business, the company secured new contracts for the rigs Noble Regina Allen and Noble Resilient as well as an extension for the Noble Reacher .

However, ongoing weakness in Norway will continue to impact the jackup segment at least throughout 2024 thus resulting in less-than-stellar near-term utilization for the company's North Sea fleet.

{kind=link}

On the conference call , management addressed concerns regarding lower floater demand following a recent lull in contract awards (emphasis added by author):

Although contracting activity and utilization rates have remained firm throughout this year, we recognize there has been some concern in the market recently over the lack of apparent demand growth over the past few quarters as indicated by the contracted UDW rig count. We see nothing to indicate any type of underlying problem with demand growth, although it has been slightly slower to materialize in the short-term. (...)

So we're approaching the $500,000 day rate threshold, a bit more slowly than we had previously expected. But if you scratch a little deeper, what you find is that the UDW market is still in fact tightening, due to the steady absorption of the sideline capacity .

Looking ahead throughout 2024, we continue to expect a double-digit increase in UDW rig demand globally driven primarily by incremental requirements throughout the Americas and West Africa.

The methodical absorption of sideline capacity has had a bifurcating effect on day rates over the short-term.

However, we believe the structural trend with day rates will continue to correlate positively with demand growth over time, which in fact is one of the key reasons why we are beginning to see the emergence of more long-term tenders in the market as the inventory of sideline capacity continues to dwindle and the economics for new rig construction are at such a dramatically higher plane as we discussed in detail during last quarter's call.

Full-Year Guidance And Quarterly Dividend Raised

The company also raised full-year guidance for revenue and Adjusted EBITDA but still expects Q4 to be down sequentially as a number of rigs recently finished their respective contracts.

{kind=link}

In addition, Noble increased its quarterly dividend by 33% to $0.40 per share for an approximately 3.3% annualized yield at prevailing trading prices. However, management made clear that investors should not expect the payout to move up each quarter:

Following the dividend initiation last quarter, we have signed additional contracts to bring our 2024 scheduled backlog to $1.8 billion currently with near-term visibility to additional bookings that could increase 2024 backlog to over $2 billion. So, we have taken the decision to make this upward revision just one quarter after the dividend initiation.

While you should not expect us to continue to adjust the dividend each quarter, we will remain focused on maximizing free cash flow generation and as previously stated returning the significant majority of free cash via dividends and buybacks.

The company also continued share repurchases albeit at a measured pace. During the quarter, Noble bought back approximately 0.2 million shares for $10 million.

Directional 2024 Guidance

While management did not provide formal guidance for 2024, the company's current expectations are for " a nice step up in Adjusted EBITDA and free cash flow " with a higher weighting towards the second half of the year.

However, profitability and cash flow generation will continue to be impacted by elevated special survey requirements with approximately 45% of the marketed fleet scheduled for drydocking next year. Consequently, management expects capital expenditures to increase slightly in 2024.

{kind=link}

Valuation and Price Target

Valuation-wise, Nobly currently trades at approximately 4x EV/Adjusted EBITDA based on my estimates for 2025:

Author's Estimates

Assigning an EV/Adjusted EBITDA multiple of 6x would yield a $59 price target for the shares thus providing for close to 25% upside from current levels:

Author's Estimates

While the recent lull in contracting activity has impacted offshore drilling stocks, long-term industry prospects remain intact.

Consequently, I consider scaling into the shares on weakness an appropriate strategy.

Key Risk Factor - Oil Price Correlation

Please note that offshore drilling stocks remain heavily correlated to oil prices so any sustained down move in the commodity would almost certainly result in industry shares taking a further hit.

Bottom Line

Noble Corp. delivered strong quarterly results and raised full-year guidance.

In addition, the company increased its quarterly dividend by 33% to $0.40 per share.

On the flip side, cash generation was impacted by required working capital investments and Noble warned of more near-term white space in the company's contracting schedule.

That said, management remained confident in the industry's long-term prospects and expects the upward trajectory in day rates to resume once the market has absorbed previously sidelined capacity.

While offshore oil and gas service stocks have been volatile as of late, I consider the recent setback an opportunity to start scaling into the shares.

For further details see:

Noble Corporation: Strong Quarter, Raised Guidance, Undemanding Valuation - Buy