ERIC - Nokia Stock: Not Looking Great Anymore (Rating Downgrade)

2023-12-06 07:00:00 ET

Summary

- Nokia's performance has declined significantly, with margins contracting and macroeconomic uncertainties impacting the company's growth.

- The loss of a major client, AT&T, to Ericsson has further affected Nokia's recovery and long-term strategy.

- Despite challenges, Nokia has had success in non-main regions like India and maintains a decent financial situation with cash reserves and decreasing long-term debt.

Investment Thesis

Nokia (NOK) has been on a free fall this year, erasing 40% of its market cap in the last year. I wanted to take a look at what has changed since my first coverage of the company where I recommended a buy rating. Fast forward 8 months, the company´s performance did not go as my model assumed, with margins contracting significantly, macroeconomic uncertainties still prevailing, and a loss of a major client forcing me to downgrade the company to a hold until the management can show us real proof that the company is on track of growth.

Comments on Nokia's Outlook

It´s been around 8 months since I covered the stock first time . I argued that the company was a good buy at that time due to the fast-growing 5G market and eventually the 6G market, where the company looks to be the leader going forward. Or so at least it looked like that back then.

Margins ever since FY22 have started to come down significantly, affected by macroeconomic economic conditions of high-interest rates and inflation. Back in Q4 ´22, the company´s operating margins had improved tremendously, which gave me a false sense that everything was going very well and that the three-phase plan was going according to plan. This has not been the case in the last three-quarters of operations, which led to the company´s share price tumble. Expenses increased, while revenues declined. This is not what the company wanted to see, but no one could have predicted such an environment.

Margin deterioration (Main Street Data)

{kind=link}

In the latest quarter , the Mobile networks segment saw a 24% decline y/y in sales and 520bps or 5.2% decrease in operating margins, which no doubt was the biggest contributor to the overall margin contraction.

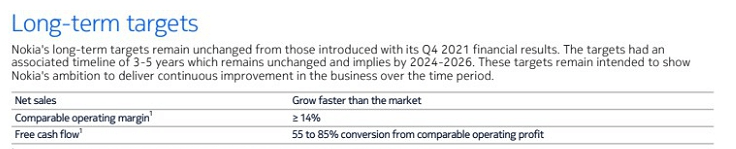

The company´s long-term targets introduced in Q4 ´21 were unchanged, and everything looked like it was going according to plan. Margins achieved the long-term goal but then everything started to go downhill. To be fair, the company still has 3 more years to achieve its goals but so far it is not looking good, especially when we take into account the loss of a major customer.

{kind=link}

AT&T going with Ericsson

The most recent blow to the company´s recovery was the loss of AT&T´s ( T ) contract to revamp its infrastructure, as T wants to have 70% of its wireless traffic flow through open cloud-based platforms by 2026. The $14B contract went to Ericsson (ERIC), which already had two-thirds of T´s network gear in the U.S. This was a huge blow, which resulted in the company losing potentially $14B over a few years. The share price tumbled around 20% after the market closed on Monday but recovered most of that the next morning. AT&T was a key partner in NOK´s Open RAN strategy that aimed to diversify the 5G equipment market. This will certainly change the company´s long-term strategy and we will hear some updates on this in the next quarter report at the end of January.

Investors have been losing confidence in the company for a while now, and to be honest, my confidence has wavered in the last 6 months as the disappointing quarterly results kept rolling in. In my first article, I argued that the company doesn't need to grow its top line, because the company was efficient in its operations and was making good bottom line due to decent margins. Ever since then, that has changed as margins did not hold up, which were the main bullish points for my buy recommendation. Now that this is not the case anymore, I need to reassess accordingly.

Macroeconomic Environment

It was a tough year for many companies but many have also started to recover, whereas NOK is still in a free fall. The two regions where the company makes most of its revenues are still very uncertain. The high-interest rates in the US and the EU are causing sales declines for the company, which do not seem to be ending any time soon. Interest rates may still be hiked but the FED hasn't increased them for a couple of months, however, J. Powell doesn't rule anything out. The same goes for the EU. The pandemic introduced 0% interest rates, which is very unrealistic that these would return, however, the rates will come down to around the US historic rates of around 2%.

Margins need to improve significantly

As I mentioned before, margins were the main driver for my buy rating back in April. These have deteriorated significantly due to the many macroeconomic factors. I am confident that these will improve over the next couple of years because the company is taking quite a drastic cost-cutting measure, which is to reduce employee numbers by roughly 14,000 . This should save the company around 10% to 15% in personnel expenses. I don't like when companies take such drastic measures to improve profitability, however, it is one of the most effective ways of improving efficiency. 14,000 people is a big number and I´m sure it won´t come cheap, in terms of monetary value in the short run and in terms of morale and productivity, but that is harder to quantify.

Not all doom and gloom

Nokia is having a lot of success in non-main regions like India, which saw a doubling of sales y/y. If the company can build on the success of this, India will become one of the main drivers of sales growth in the next couple of years, which will certainly ease the blow of sales decrease in the EU and the US if these continue to decline for the next while. Eventually, the US and the EU will start to pick up again, and we will see sales growth return, or even be the new catalysts like India in the next couple of years but that remains to be seen.

The company´s financial situation is still decent in my opinion. NOK still has over $6.6B in cash and long-term debt that has been slowly but surely decreasing, which will help the company´s cash flow situation in the long run. The current ratio is also decent, hovering at around 1.6 most recently, so it has no liquidity problems or is at risk of insolvency.

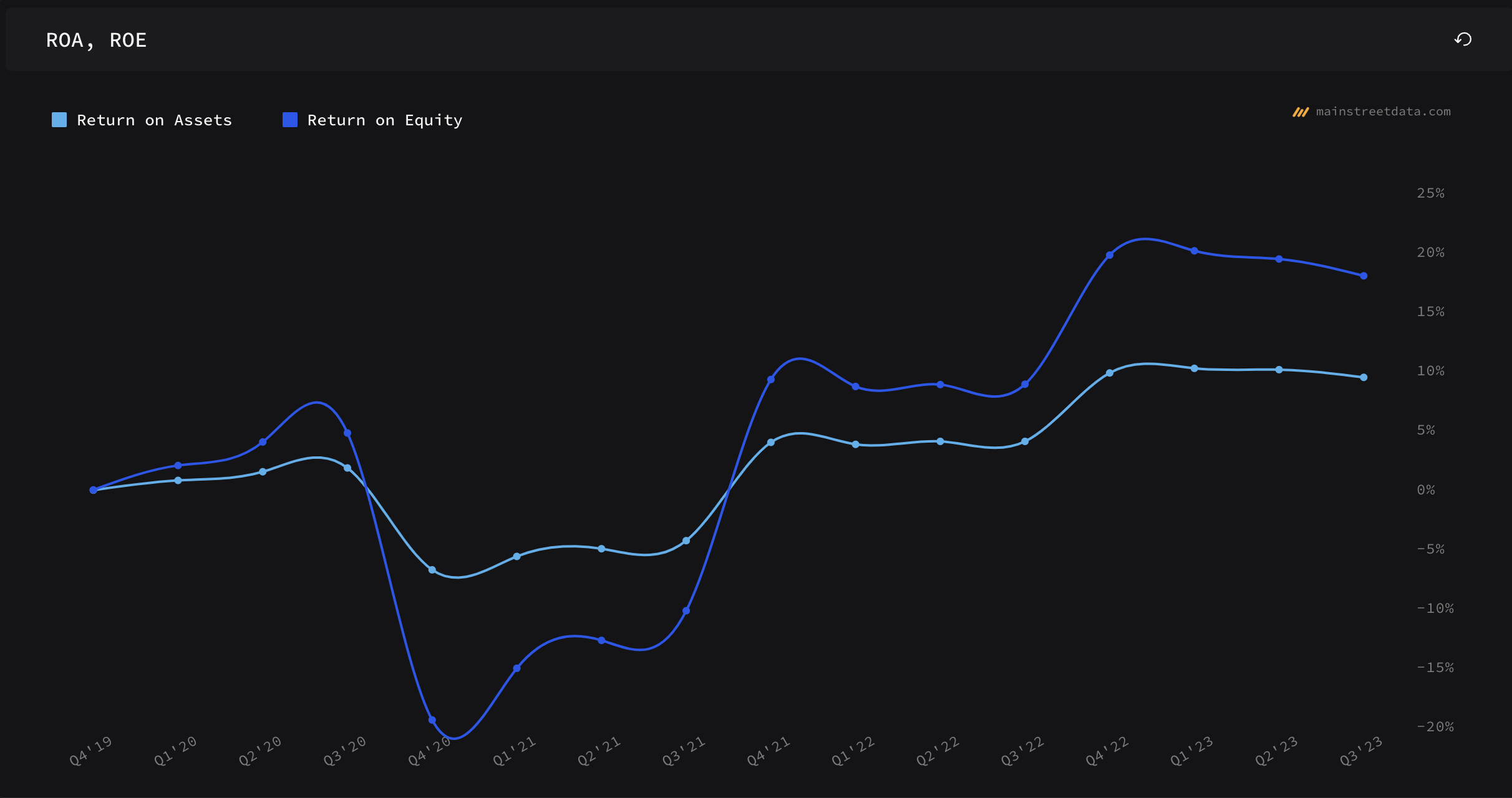

In terms of efficiency and profitability, ROA and ROE are also pretty good, except for the last 3 quarters as these have been trending down, and may continue for a little while longer.

ROA and ROE downtrending (Main Street Data)

{kind=link}

So, overall I think the situation could be worse and it may get worse but only in the short-run, unless the company isn´t able to win any meaningful contracts to expand its business. However, with a decent balance sheet, the company will continue to weather the negativity, even though, the share price may continue to get hit.

NOK stock valuation

I had to update my valuation analysis as there were a lot of things that changed since April in terms of efficiency and interest rates. Back when I covered the stock first, the treasury yield was 3.44%, and just a couple of weeks ago it was close to 5%, only coming down in recent days.

For revenues, I decided to take a conservative approach, seeing that the company went nowhere in terms of growth. Below are my assumptions for the base, optimistic, and conservative cases.

{kind=link}

The value is not going to be driven by top-line growth. Efficiency is what matters here. I went with margins that are worse than I assumed back in April as operating margins deteriorated significantly since then. Also, over time I am going to improve these back to FY22 figures because the drastic cost-cutting measures will drive some expenses down. Net margins were inflated by a tax break as historically these were at around 6%-7%. Below are the margin and EPS assumptions.

Margins and EPS Assumptions (Author)

{kind=link}

It may be a little too conservative, however, the negative sentiment and the loss of a big contract will most likely adjust the company´s long-term outlook to the downside. This way I get a larger margin of safety.

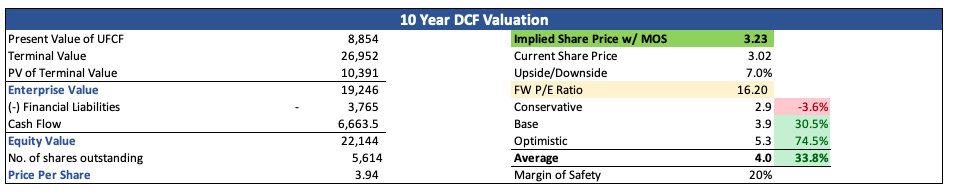

On top of these estimates, I went with a 10% discount instead of the company´s WACC of around 7%, this way I get even more margin of safety. Furthermore, I added another 20% MoS to be even more protected on the downside. With that said, NOK´s intrinsic value is $3.23 a share, which is very different from when I first covered it.

{kind=link}

Closing Comments

I´m wondering now, is all the bad stuff priced in right now, or is there going to be more coming up in the next half a year to a year that may keep the company´s share price low? My biggest gripe with the company right now is its inefficiency. Over the last 3 quarters, the company managed to become very incompetent and the management was not able to control the costs effectively. Therefore, I am forced to update my rating from a buy to a hold until we see actual improvements in margins, which may take a long time especially if the macroeconomic conditions don't improve.

The company needs to win some meaningful contracts, the ones that would be catalysts to their goal of improved growth and to "grow faster than the market". Furthermore, the company needs to stay on top of its game to not lose any more big clients in the future.

Right now, I will continue to monitor the situation over the next couple of months and see if there will be any considerable changes that will affect the company in a big way, as for now, I don't see anything.

For further details see:

Nokia Stock: Not Looking Great Anymore (Rating Downgrade)