NKRKF - Nokian Renkaat: Problems With A Potential Solution Far Off

2023-04-06 15:40:51 ET

Summary

- Nokian Renkaat Oyj is a small position that, yes, I still own. The company has absolutely fallen apart (in some ways) after the Ukraine/Russia conflict.

- The reason is simple - the company's sourcing was done almost strictly in Russia, which left the company in shambles when the West pulled out.

- I'll revisit things to see what we can expect from Nokian going forward.

Dear readers/followers,

A reader recently contacted me and asked why I hadn't picked up my coverage on Nokian Renkaat Oyj ( NKRKF ) since the company is now trading at less than $9/share for the ADR and less than €9/share for the native TYRES ticker on the Helsinki stock market.

This is a very interesting company to look at, despite the fact that I haven't done so for almost 3 years' time. My M.O. by the way, stands. I don't sell a stock or a company that I don't suspect of risk of fundamental default. Nokian, while in a precarious situation, is not a company I view as being in danger of defaulting.

Why is that not the case?

That is something we will look at today!

Nokian Renkaat - a play for an iron stomach

Nokian is a play that both on a high level and on a granular level, is rife with fundamental warnings and signs of distress. The company's net income is in the toilet. It has gone from being a cash-heavy company to being debt-heavy, with less cash than previously. Every single margin-related or return-related metric, including but not limited to Gross Margin, Operating Margin, RoE, RoA, ROIC, and ROCE is among the worst in the industry with Nokian at less than the 20th percentile in every single comparison (Source: GuruFocus).

Imagine for a moment that your company is based on manufacturing location X, but Location X is destroyed by a landslide that makes any rebuilding or salvage untenable. What you're left with is the potential of essentially rebuilding most, if not all of your manufacturing base elsewhere.

That is essentially the situation Nokian Renkaat found itself in around a year ago now. The closing "hammer" on that was only back a week ago, when Nokian Renkaat officially closed its Russian operational sales to the local operator PJSC Tatneft. This marks the end of all operations in Russia for the Finnish company.

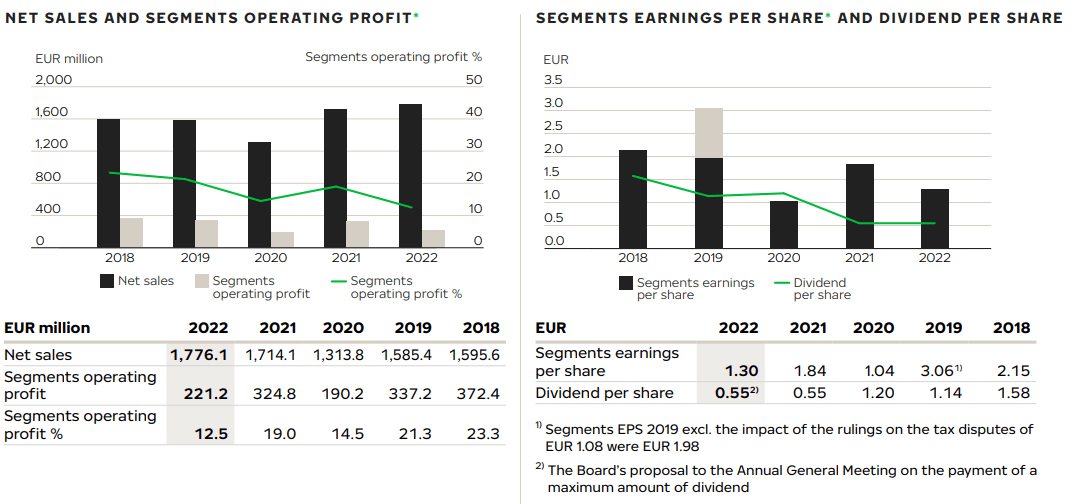

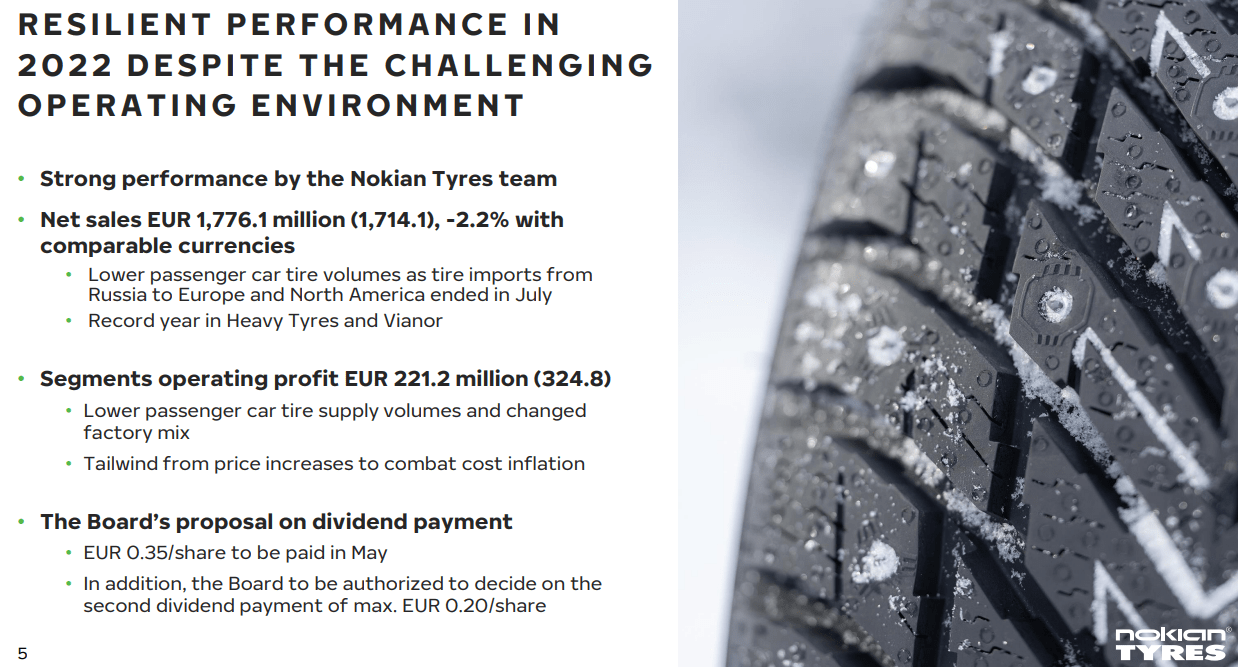

2022 results, which the company reported, were actually better than expected considering the degree of impact we saw. The company, for instance, managed a positive operating profit , and net sales of €1.77B and still managed to retain 55% of the relevant market winter tire share. Overall, 2022 doesn't really show as bad an impact as you might have expected.

{kind=link}

The company even has posted a dividend - in fact, unchanged from the 2021 year - which is impressive.

It's important to remember that Nokian is primarily a Nordic play. Not just European, but Nordics, with Nordic countries accounting for over 40% of net sales, and almost 70% of sales being made in the passenger car tire segment.

The real "deeper" impacts are those we can see in the ROCE and return metrics. Those are down - ROCE is down to less than 11%, down from 15.8%. However, despite the multitude of issues and challenges arising from the company's exit from Russia, I expect many a working night has been spent moving the company forward.

To that end, this is what Nokian has managed to do since.

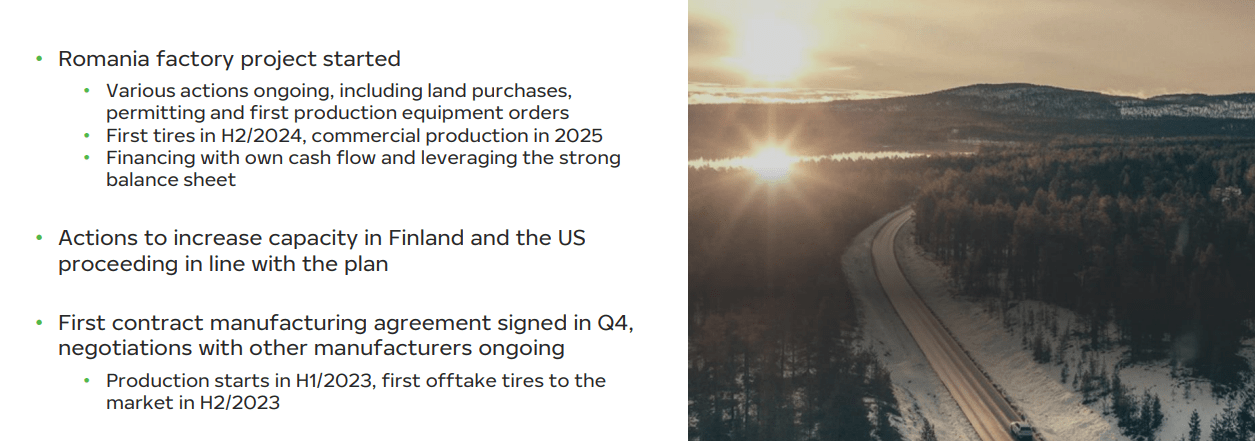

- €650M in investment in a new passenger car tire factory in Romania, which will form the modern backbone of Co2-zero emission car tire production. This is the very first of its kind and will form the foundation of the company's new and improved production capacity - without the need for anything out of Russia.

- The company has developed tires that are over 90%+ based on renewed materials, which moves the company closer to its goal of 50% of the materials used is either recycled or renewable.

- 2022 was a record for Nokian Heavy Tyres and Vianor. Despite macro, Heavy Tyres had its best sales year ever as well as profitability, and Vianor had ATH sales as well.

Of course, Romania's capacity isn't enough. In order to secure production, Nokian also had to outsource some of its capacities to contract manufacturing.

{kind=link}

The picture that Nokian wants to present investors with is that despite the ongoing issues (or at least until the sale) in Russia, Nokian is committed to building a new, non-Russian manufacturing base that's better than before. To build a "new" Nokian Heavy Tyres, that's already able to navigate the high demands in sustainability and recyclability for the industry.

The fact that the company has delivered record sales in certain segments really goes some way to confirm an upside here. At the same time, some headwinds remain. The company saw lower supply volumes, as well as 22.2% in company-wide net sales during 4Q due to lower volumes of passenger tires. 4Q results in terms of operating profit were positive, but barely, down to €13.2M from €88M. However, as mentioned, for the full year things are looking surprisingly excellent.

{kind=link}

Despite taking on some more debt, the company still has a relatively solid balance sheet in terms of safety. Nokian has typically been a net-cash company, and this is the first time in some time that we're looking at a positive gearing ratio, now at around 10%.

The important question for me will be, just how long will it take for "the new" Nokian to come around? When can we expect the new production basis, and the new organizations that are needed to drive Nokian back to where it once was to be around and started?

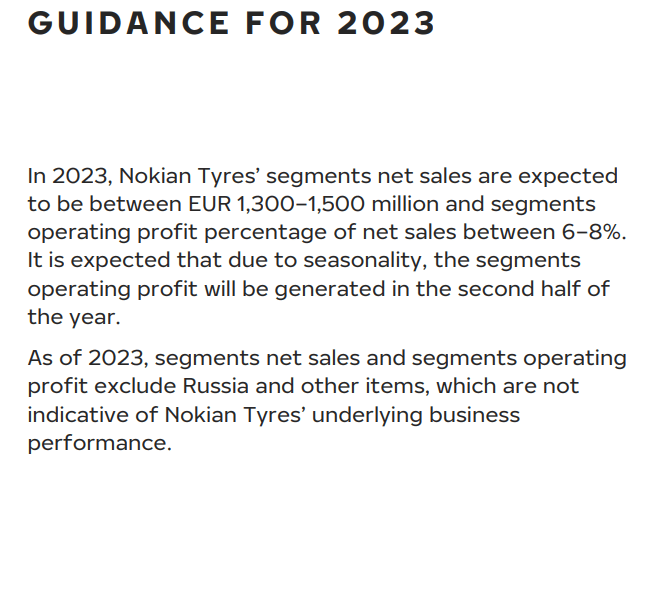

Well, the company does have some expectations. 2023E and the first half are actually expected to be quite weak due to constrained capacity, causing a lower supply of tires and negative seasonality, with 2H being able to offset some of that. However, Nokian doesn't expect as positive a trend for Heavy Tyres as the company saw this year but rather expects things to go somewhat negative in this segment.

Here is official company guidance - and as you can see, it's lower than 2022.

{kind=link}

The company's version is the "new start" angle. That it's really a fresh start for the company, and a chance for investors to really get in on the "ground floor" at this new investment. There are several key arguments the company uses to drive this message home.

{kind=link}

And you know what?

It's not unrealistic. Everywhere, tires are needed, regardless of EV or ICE cars. The company's market leadership in the Nordics has not been challenged or threatened by the last year, which means that I do not expect it to be significantly challenged going forward either. The company's manufacturing profile has changed somewhat and now includes contract manufacturing to a growing degree. We'll see if this is something that'll fade with time or something that'll stick with it.

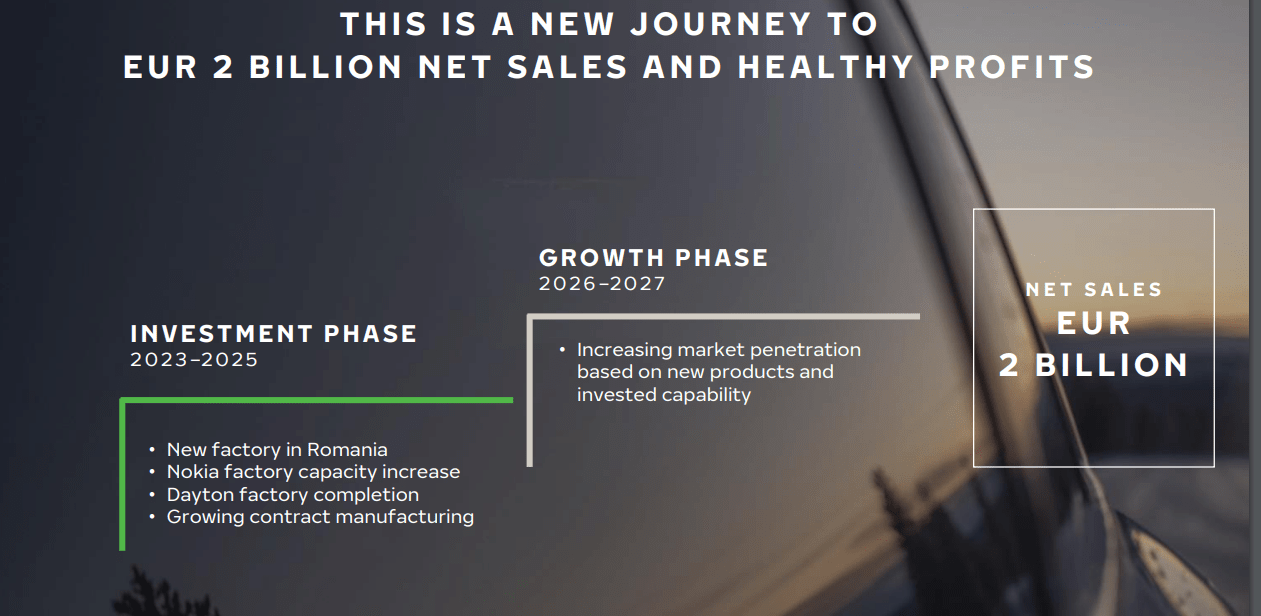

And, more importantly, we have a pathway to growth. Take a look at this relatively generalized set of ambitions.

{kind=link}

Don't get me wrong. I'm not a big fan of tire companies overall - they have some margin problems, production problems, and overall challenges in their business model. But I am a valuation investor - and Nokian, as a company, through its avenues of sales as well as Vianor, does have some appeal that makes the company a potential "BUY" at a good valuation.

With a reduced dividend of €0.55/share, the company yields no less than 6.3% at this time. That's a damn good yield, even if we need to be clear about the fact that this is a company in some distress.

But things aren't really as bad as you might expect - that is my message from looking at the company here.

Let's look at company valuation.

Nokian Valuation - Undeniably attractive, but problematic

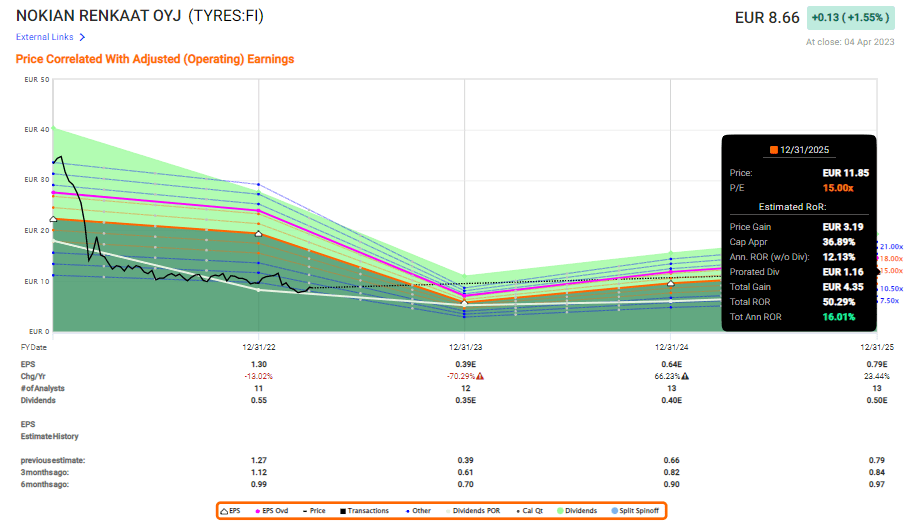

To say that the company's valuation is not attractive would be a lie. The simple fact is that even on today's relatively negative forecast, including a forecasted decline of 70% in adjusted EPS, we're still able to see a market-beating set of returns based on a 15x P/E on a 2025E basis.

{kind=link}

Does this mean that Nokian is a no-nonsense excellent "BUY"? No, of course not. We're still talking about a company in distress. What I want to highlight is that based on earnings, and where the company actually trades, it's not as bad as might be expected. This is most certainly true if you in the next 4-5 years expect any sort of normalization on part of Nokian Renkaat, which I just happen to do. Consider also for a moment that product and company quality has historically meant that Nokian has warranted a premium, and that upside, once things turn back to normal, might be even higher.

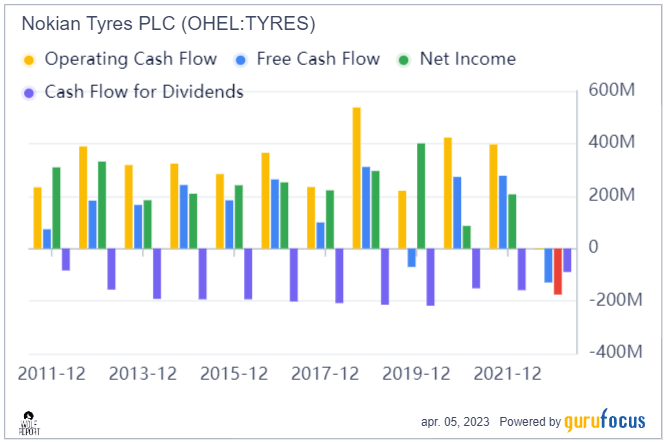

The current state of the company is unfortunately a horror show in terms of margin, in terms of growth, and in terms of its near-term. Net income is negative for 2022, the first time net has been negative in over 15 years. Free cash flow ("FCF") is showing similar trends, and ROIC/WACC, which has been remarkably positive for a company in this particular field, has taken a turn to "downtown."

{kind=link}

Those following Nokian in terms of analysts have a very interesting view on the company. S&P Global goes to between €7-€11/share, implying a low upside - but 5 out of 12 analysts are actually positive to the average PT of €9.09, and there's an upside of 5% here. Valuation methods that include combining various cash flow and earnings forecasts, can, if we include GDF valuation metrics, and project non-impacted free cash flows and price/sales multiples, come up to between €25-€30/share, which is essentially a non-impacted valuation for this company. And I don't see why, in the long-term, the company shouldn't reach this. Together with dividends and the like, this makes for a 200-400% potential RoR.

I'm somewhat biased due to my own proximity to the company and the relevant geography, but given that the company hasn't actually declined or failed in the worst thing that might have happened - and is already building a world class-leading new factory in Romania, I would go so far as to say that the worst is past.

And if the worst is past, all that remains is to estimate when we might see a turnaround, or if now is a good time to invest in the waiting for a turnaround.

While Nokian may indeed go lower from here as a result of negative quarterly trends, I fail to see how this would change the thesis for long-term Nokian investors. Like myself, they likely hold the stock due to seeing what might happen in the next 2-3 years. Most international comps in Tires such as Bridgestone, Michelin ( MGDDF ), Continental AG, and others are, of course, larger. Nokian is at the bottom of the comp in terms of market capitalization. It wasn't, in fact, even a leader in size when it wasn't impacted by Russia.

But Nokian has the combined appeal of owning a large market share together with the potential for realistic reversal. Yes, tire companies will continue to be heavily correlated to overall macro, and that isn't necessarily looking all that good in 2023-2024. However, this is a play to at least 2025, and by then I see the potential for Nokian to perform well.

Make no mistake - this is as "speculative" as a "spec buy" gets. We're talking about a distressed tire business.

But at this time, I do actually view it as a "spec buy," despite some of the impacts here.

Here is my thesis for Nokian Renkaat.

Thesis

- Nokian, to me, is the textbook definition of a turnaround play where the turnaround actually has pretty good visibility. The main problem with this is that there are so many alternatives on the market that are not only somewhat better but also come with higher overall safety.

- Due to this, Nokian is of marginal interest even to a native investor in the Nordics like me. I own a stake in Nokian, but I have no immediate plan to increase my stake.

- I view Nokian as a "BUY", but it's speculative, and I go as high as €12.5/share for the native in the near term here. But again, it's speculative and shouldn't be considered unless this is within your risk tolerance parameters.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

The company does fulfill 3 of my 5 criteria, but given the recent trends, I can't call it qualitative or fundamentally safe - yet. For that reason, the "BUY" is speculative.

For further details see:

Nokian Renkaat: Problems, With A Potential Solution Far Off