NKRKF - Nokian Renkaat: We Need Time To See An Upside Even With A Spec 'Buy'

2023-11-16 23:48:01 ET

Summary

- Nokian Renkaat, a tire company, has faced significant challenges after the Ukraine/Russia conflict due to its heavy reliance on sourcing from Russia.

- The company is slowly improving its fortunes and has made progress in rebuilding its manufacturing and sourcing capacities.

- Despite its current challenges, Nokian Renkaat has maintained its dividend and shows potential for improvement in the future.

Dear readers/followers,

In my last article, I gave Nokian Renkaat ( NKRKF ) a "BUY" rating - but I made it clear that my small position was at a very long timeframe. Why? The company has absolutely fallen apart (in some ways) after the Ukraine/Russia conflict. The reason for this falling apart is very simple as well, as you can see in the picture in the article above. The company's sourcing was done almost strictly in Russia, which left the company in shambles when the West pulled out.

I've been covering the company a few times since to see what it will take for the business to pull itself back out. Why am I so insistent on covering and even owning part of this company in what is otherwise a very tyre-free portfolio?

Fairly simple.

The company is actually a very good business, and it does make some of the best tires in the world.

This is an update to my Nokian article which you can find here - this update will serve to show you why I expect improvement in the company in the future.

Nokian - an iron stomach may be an understatement

This is very much a fundamental play - both on a high level and on a granular level. It's also rife with fundamental warnings and signs of distress, though these are slowly abating as the company once again slowly starts to improve its fortunes.

Of course, it's nowhere near where it once was. It has gone from being a cash-heavy company to being debt-heavy, with less cash than previously. Every single margin-related or return-related metric, including but not limited to Gross Margin, Operating Margin, RoE, ROA, ROIC, and ROCE is among the worst in the industry with Nokian at less than the 20th percentile in every single comparison - and this is the case as of the latest results as well. So while I will be somewhat positive about the 3Q23 results, which were reported not that long ago, I want to make clear that this company still has a long way to go.

So what's been going on in 3Q23?

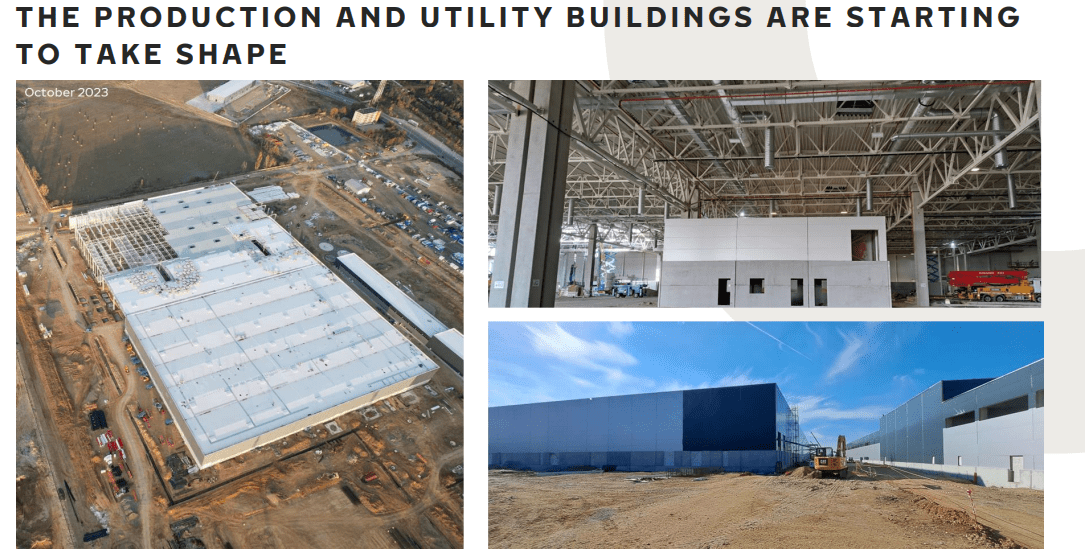

Well, quite a few things, as it turns out. The company has got the permit, and broken ground on its new Romanian factory. The company's first Tires are expected to be produced at this site in 2H24, with a commercial start-up in 2 years' time. Do you see why investors are hesitant to go in deeply here?

The company is also trying to save and get synergies and money from every part of the equation - among other things, they have applied for almost €100M worth of subsidies, already approved by the Romanian government and currently under EU review. I believe the company, based on trends since the Russo-Ukrainian war, has a good chance of seeing this being granted.

{kind=link}

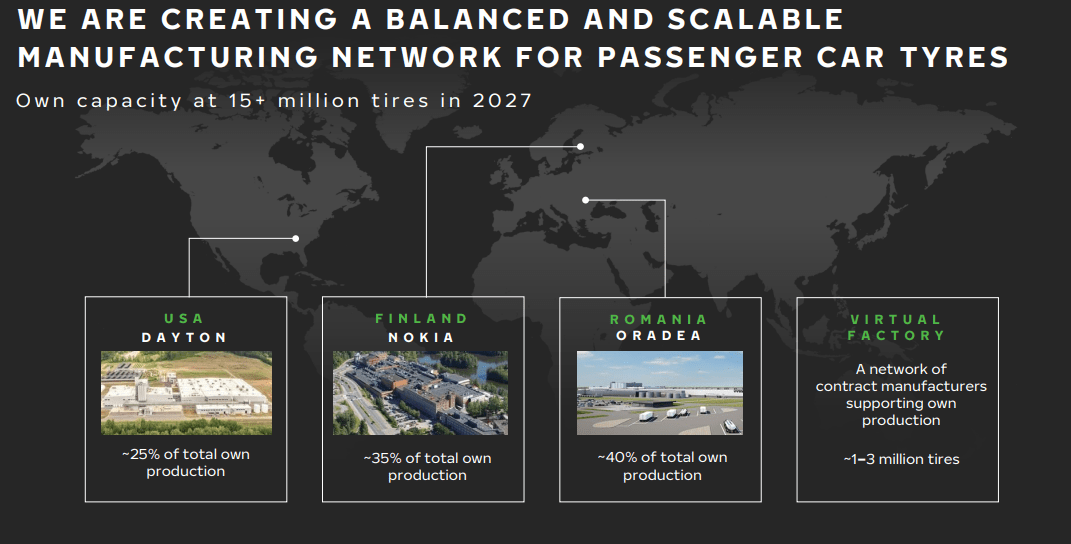

Of course, another way of saying this is saying that the company won't be seeing any tires from here for 2 years - not commercially, at least. The company is in the process of slowly rebuilding its manufacturing and sourcing capacities. In its home nation of Finland, the company is adding capacity as well, and the same is true for the US operations. 125 new people have been hired in the US, and the company is trying to expand its portfolio, with a current contract manufacturing volume of 1.5M secured for 2023.

Here is the company's current, and planned base - and it showcases just how devastating the loss of the Russian capacity was.

{kind=link}

The company boasts improved profitability as of this quarter, with improvements in 3Q. Net sales revenues are at €276M, down 12.7%, but segment EBITDA is firmly back into positive numbers, with a €46.1M EBITDA and a margin of 16.7%. That's the real highlight here because YoY this was at 2.2% (Source: 3Q23 Nokian Earnings ).

I also want to ensure here, that the company has not canceled its dividend , despite the significant impact. We're still talking about a two-dividend payment dividend policy, with the second installment being paid in December of this year. This also puts the company's current dividend yield at no less than 4.15% despite the impact.

Is it good? No, not really. Is it good enough? Also, again, not really. We can get 5%+ from A-rated monthly paying REITs, and even those are undervalued while being BBB+ or higher. Nokian has no credit rating worth speaking of, a market cap of less than €1.2B at the current time, and while it does have low leverage at less than 25% LT debt/Cap and it is a good company , I understand anyone who does not want to invest in Nokian at this particular time.

Still, recovery is ongoing - and the company's balance sheet is surprisingly stable given the current specifics we see today. Also, the operating profit has recovered nicely, far earlier than I expect it to. It was negative last year, it's now positive, and the EPS is back to €0.09/share for a segment EPS.

Segment-specific trends are also fairly encouraging. Passenger tire trends are coming in at lower numbers , but with good margins , which is far more important. The company's inventories are also at a high level, and we have some clear profitability trends here, with improving sourcing costs. The segment operating profit for passengers was over 11%, up from negative 8.4%. Again, almost a 20% improvement, which is fairly amazing.

Heavy tyres meanwhile, are down in net sales due to bad aftermarket sales, but these margins never really collapsed at all, and as of this quarter, are still at a 12.1% level, which continues to be solid. Vianor also continues to be its own segment for the business - and this is the last that has not recovered to any significant degree. The company still maintains its 150+ service centers, but these have seen declining sales at 4.2% drop, with a strong FX headwind both from SEK and NOK which is certainly a part of the reason for this, and the negative operating profit of €4.8M.

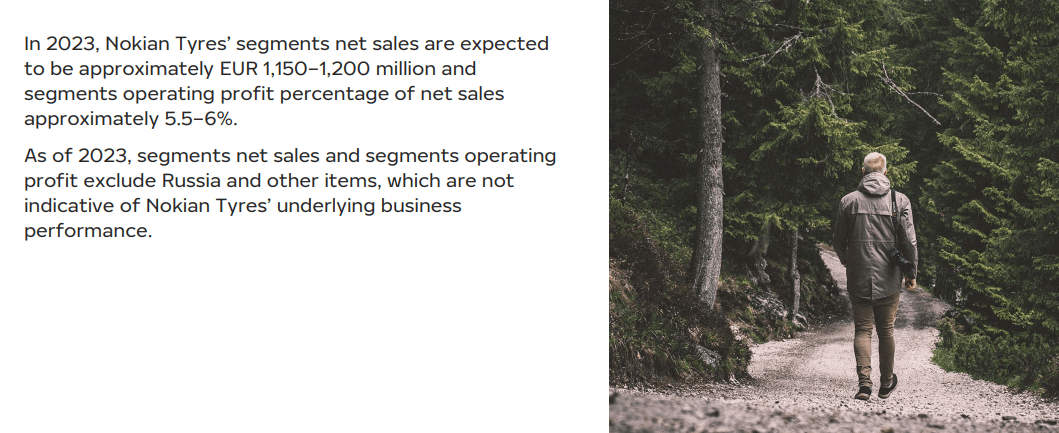

However, we have guidance from the company here for the full year.

{kind=link}

Solid positives indicating investability in this company? Not really. Remember what's on the market today, and remember what you in fact can easily get if you look at any other business here.

In fact, the recent improvement in the share price moving up to around €8.5/share has had me looking at the overall forward possibilities.

While Nokian is expected to significantly improve its earnings and profit in 2024 and 2025, if we use valuation as a guide, the company has a fairly low limit of return here, stopping at about 20% annualized.

This may sound much - and is acceptable for me, and why I consider the company a "BUY", but the risk profile if you invest here is far worse than many other companies with only slightly less or even equal upside here.

Let's look at that valuation.

Nokian Valuation - Eventually, we'll probably see prices of over €20-€30/share gain, but for now, the upside is to €15/share

This company definitely remains a "spec play" at these valuations, without a doubt. While some things have improved, and the valuation now implies a 20.8% annualized upside to a 2025E valuation of around 17-18x, which is where this company typically trades historically, these valuations do not take enough into consideration the current environment and other factors we're currently seeing in the market.

However, to say that the company's valuations and forecasts are not attractive would be a lie. The fact is that even on today's relatively negative forecast, including a forecasted decline of 70% in adjusted EPS, we're still able to see a market-beating set of returns based on a 15x P/E on a 2025E basis - that 20% is market-beating, for sure.

{kind=link}

While we're no longer in a "horror show" in terms of margins, as I said in my last article, the company I would argue fails to hold up in a comparative appeal to many other attractive investments today. There would be a far stronger argument to be made if we could see 200-400% RoR from a trough - but this is not the case. Unless you say the company should revert to over €30/share in less than 2 years, then we're talking around 250-300% ROR - but I view this as extremely unlikely in this environment.

Current targets for this company come to €8.5/share, which means that this company is now barely on the cusp of buyability in terms of S&P Global targets. Only 2 analysts give the company a "BUY", with most at "HOLD" or sell at the valuation, the analysts going from a low of €6.2 to a high of €11/share. My PT is higher.

While this company does have things going for it, and I'm sticking to my price target in this case, I also caution anyone from investing too much here, because as of now, there are many better alternatives. Because of that, I give you my updated thesis for the company here.

Thesis

- Nokian, to me, is the textbook definition of a turnaround play where the turnaround actually has pretty good visibility. The main problem with this is that there are so many alternatives on the market that are not only somewhat better but also come with higher overall safety.

- Due to this, Nokian is of marginal interest even to a native investor in the Nordics like me. I own a stake in Nokian, but I have no immediate plan to increase my stake - even less now as of November 2023, because of the many better alternatives out there today.

- I view Nokian as a "BUY", but it's speculative, and I go as high as €12.5/share for the native in the near term here. But again, it's speculative and shouldn't be considered unless this is within your risk tolerance parameters - and even then, look at what's available.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

The company does fulfill 3 of my 5 criteria, but given the recent trends, I can't call it qualitative or fundamentally safe - yet. For that reason, the "BUY" remains speculative, and I actually would say that it's now less attractive than other plays.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Nokian Renkaat: We Need Time To See An Upside, Even With A Spec 'Buy'