NOMD - Nomad Foods: A Packaged Foods Value Option

2023-03-05 11:46:18 ET

Summary

- Nomad Foods is a multinational packaged foods company that produces and distributes a range of frozen food products.

- The company has recorded mid-single digit revenue growth since 2016 while recently released Q4 2022 results inspire confidence.

- NOMD stock trades at a relatively inexpensive valuation.

Thesis

In the current, unstable market environment, where previously beloved technology, growth stocks are recording tremendous losses, many investors have returned to the search of value opportunities in more traditional sectors. The Consumer Staples sector is known for its defensive attributes and is generally regarded as a safe harbor for turbulent times.

Nomad Foods (NOMD) is an up-and-coming packaged foods company operating on a global scale. In this analysis, I explore the company's financial attributes and attempt to determine whether it can be regarded as an attractive value opportunity.

Note that for the purpose of this analysis, given that the company reports earnings in EUR (€), most financial numbers are reported in EUR as noted throughout this analysis. Where it is deemed useful, the respective amounts in USD ($) are also provided.

A Brief Introduction to the Business

Nomad Foods is a multinational packaged foods company that produces and distributes a range of frozen food products. The company was founded in 2014 and is headquartered in the United Kingdom. NOMD maintains operations around the world, including in Europe, North America and Australia.

In recent years, Nomad Foods has made several strategic acquisitions to expand its product portfolio and increase its presence in key markets. For instance, in 2018, the company acquired Aunt Bessie's, a leading frozen food brand in the UK, and in 2020, it acquired Fortenova Group's Frozen Food Business in Croatia, Serbia, Bosnia, and Herzegovina, and Montenegro. These acquisitions lead Nomad Foods to further product portfolio diversification in an attempt for customer base expansion.

Stock Performance

Despite steady and respectable financial performance, as discussed in the segments below, NOMD's share price has seen large fluctuations over the last 3 years. The stock reached a price of $31.7 at its peak in 2021 and has been on a continuous decline since, as the broader market struggles as well. Currently, it trades at $17.8 ($3.10B market cap) and pays no dividend.

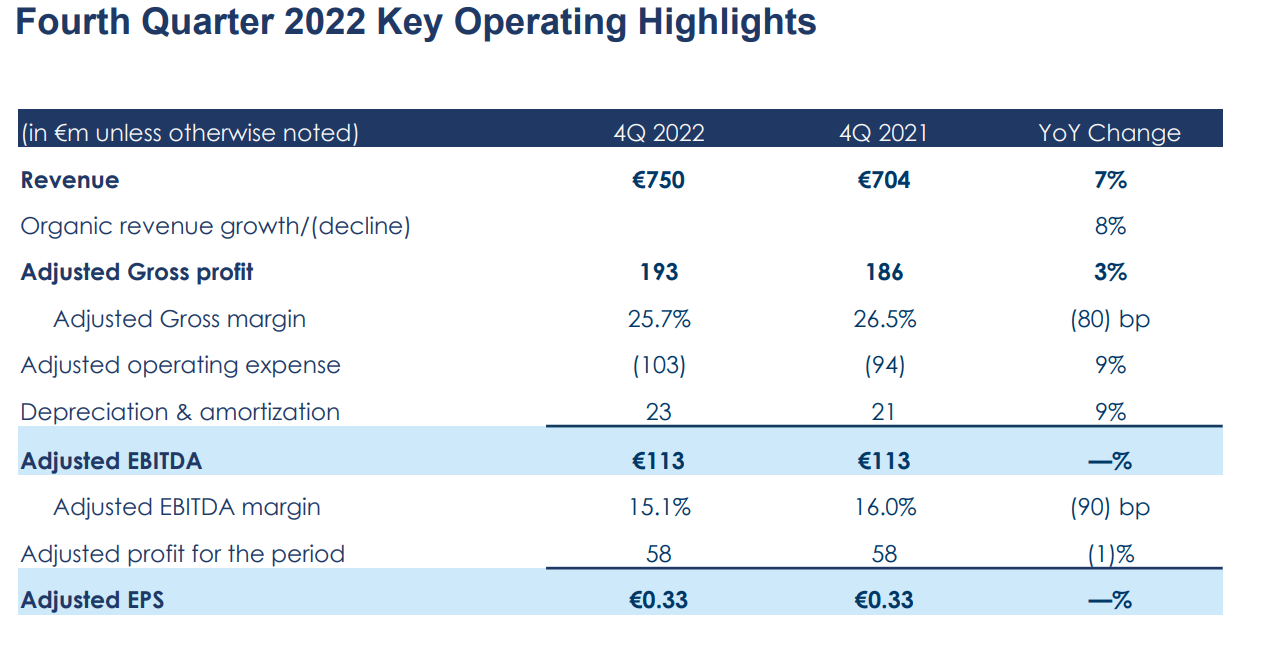

Q4 2022 Results

On February 23, 2023 Nomad Foods reported financial results for the fourth quarter of 2022 and the full fiscal year. The company slightly missed on earnings by -€ 0.01 (EPS of € 0.33 for the quarter), while beating revenue expectations by € 15.6M (revenue of € 750M for the quarter). YoY sales increased by 7%, while EPS remained flat. The Q4 earnings report also resulted in an upgrade to a Buy from Goldman Sachs, expecting upward revisions in 2023.

{kind=link}

Financial Performance

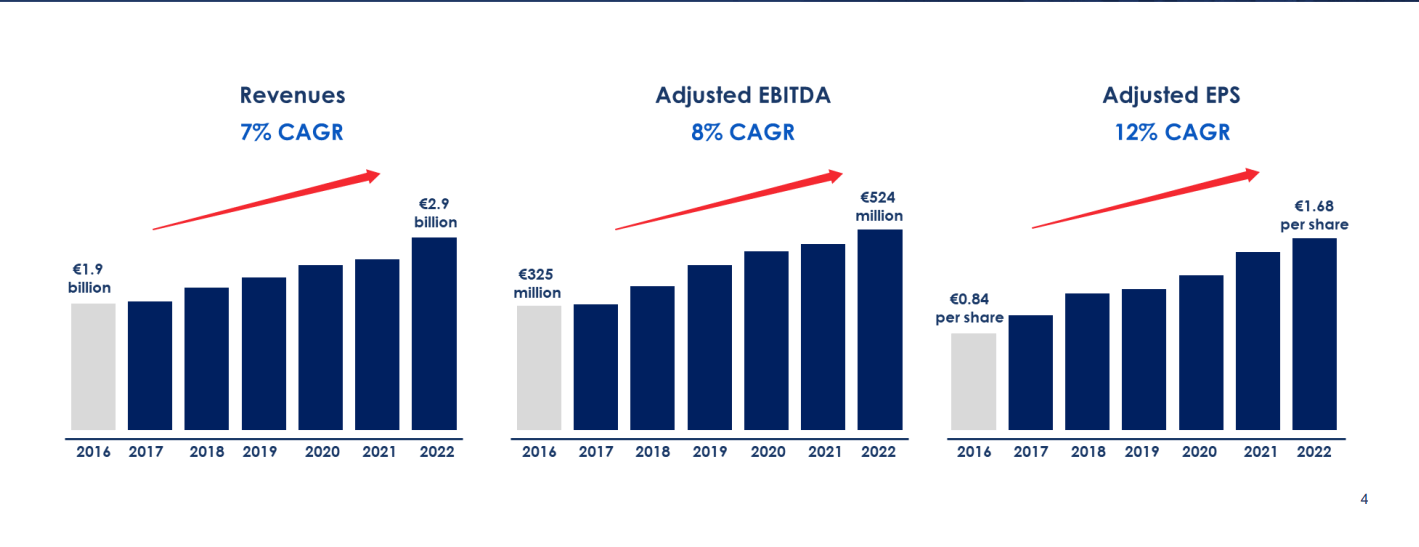

Nomad Foods has followed a steady top and bottom-line growth strategy over the last few years. For 2022, the company generated € 2.9B ($ 3.15?) in sales, marking the 7th consecutive year of consecutive annual revenue growth. Since 2016, revenues have grown at a +7% CAGR, EBITDA at a +8% CAGR and Adj. EPS at a +12% CAGR. Overall, performance clearly outpaces the average sector growth in all financial metrics mentioned and should be considered rather impressive for a food company in the Consumer Staples sector.

{kind=link}

When it comes to profitability NOMD's gross margin has somewhat decreased over the past couple of years from 30.5% to 28% and currently stands a bit lower than the sector average of 32%. A few lines down in the income statement, however, profitability performance picks up, as Nomad Foods' records an EBITDA margin of 16.5% (11.5% sector average) and a Net margin of 8.5% (3.5% sector average). Bottom-line profitability appears strong throughout the past 5-year period.

One thing that stands out for the company is the absence of a dividend payments that investors are used to seeing in the consumer staples sector by most of its peers. That said it is important to note that Nomad Foods was founded in 2014, so it is still early for the dividend payment that we should expect in the future.

Free cash flow generation for the company has been rather inconsistent, mainly due to changing CAPEX spending used towards acquisitions. Still, the company generated € 173M of Unlevered FCF in 2021 and € 188M in 2022.

The company displays a current ratio just over 1.05x indicating sufficient short-term liquidity while maintaining a € 370M cash balance. Inventory have also increased more or less proportionally to revenue growth over the last few years. One thing for potential investors to take notice of should be the company's large, growing debt balance. Long-term debt currently amounts to almost two thirds of Nomad's market cap, which is a very significant amount and a risk multiplier for the business in the mid and long-term.

Forward Estimates

For the fiscal year 2023 management forecasts mid-single digit growth in revenue, while expecting EPS of €1.50 - €1.55 ($1.60 - $1.66 based on current FX rates). Cash flow conversion rates are expected to range between 90-95%. Analysts also expect revenue to continue to grow at mid-single digits through 2025, with slower rates however than the company's average growth from 2016 to 2022.

Risk Factors for The Business

In this segment a brief analysis on some major risk factors that affect the prospects of the company is presented.

Fluctuations in raw material prices: Nomad Foods relies on a range of raw materials, including meat, fish, vegetables, and fruits, to produce its frozen food products. Changes in the supply and demand of these raw materials, due to factors such as weather conditions or government regulations, can lead to fluctuations in prices. In addition, Inflationary pressures Nomad Foods may struggle to pass on these price increases to consumers, resulting in lower profit margins. Additionally, if the company is unable to secure a stable supply of raw materials at predictable prices, it may struggle to maintain its product quality and consistency.

Dependence on key suppliers: Nomad Foods relies on a limited number of suppliers for its raw materials, packaging materials, and other inputs. Any significant disruption in the supply chain can adversely affect the company's ability to produce and deliver products.

Intense competition: The packaged food industry is highly competitive, with established and emerging companies competing for market share across the world. Nomad Foods must continuously innovate and invest in research and development to stay ahead of its competitors while staying ahead of ever changing consumer trends and preferences If the company fails to keep up with changing consumer trends and preferences, it may struggle to retain its market share. Additionally, intense competition could result in pressure on prices, reducing the company's profit margins.

Currency exchange rate risks: Nomad Foods operates in multiple countries, and fluctuations in currency exchange rates can impact the company's financial performance. This can result in a decrease in revenue and profitability. Additionally, currency exchange rate risks can impact the company's ability to manage its debt, as changes in exchange rates can result in increased borrowing costs.

Valuation

Nomad Foods exhibits low valuation metrics across the board. The company trades at a 10.3x P/E multiple compared to a sector average of 20.0x, an EV/EBITDA ratio of 9.9x versus a sector average of 13.6x and a P/S ratio of 0.98x (sector average of 1.21x).

While a cheaper valuation likely accounts, to some extent at least, for the company's smaller size and less established market position compared to the competition (therefore it carries higher risk), still, at current levels, Nomad Foods' valuation appears attractive.

In the graphs provided below by YCharts, NOMD's 5-year P/E and P/S multiples are plotted against those of one of the largest firms in the packaged food industry, General Mills (GIS). Nomad Foods trades near historic lows in both metrics compared to its own 5-year history and relative to GIS as well.

Final Thoughts

After all things are considered, Nomad Foods presents an attractive investment case for most investors. Although the company carries more risk than the average large cap company in the food industry, its moderate growth attributes and very low valuation multiples leave a lot of room to the upside. For these reason, I would rate NOMD as a buy, at current price levels.

For further details see:

Nomad Foods: A Packaged Foods Value Option