NMR - Nomura Loses On Low BoJ Rates In Retail But Not In Investment Banking

Summary

- Nomura has a very Japan-focused business, and while the stance of the BoJ to keep rates low hurt them in some of their businesses, in others it helped.

- Overall, their performance ends up being resilient on account of their idiosyncratic mix.

- However, with the return to some modicum of certainty coming to reduce volatility, it doesn't seem that Nomura is particularly well positioned to benefit.

- Moreover, cost control was a problem in their major wholesale division despite growth.

- There isn't a huge reason to pick Nomura over other banks.

Published on the Value Lab 1/18/22

Nomura ( NMR ) used to be a larger bank than it is today, where it is now much more focused on Asian markets, with a dominant position in Japan. With quite large differentials between the Japanese economy and the rest of the world in the current environment, Nomura's performance has also been relatively different from other banking peers. Segments that should have been somewhat of a disaster performed alright, but in general Nomura's volatility levered businesses did well as there was still speculation over what was going to happen in the Japanese economy, and if policymakers, mainly the BoJ, were going to pivot on policy and mirror the rest of the West. While Nomura turned out to be pretty resilient, they are conversely not going to be as levered to the recovery as peers. Overall, Nomura doesn't appear too interesting.

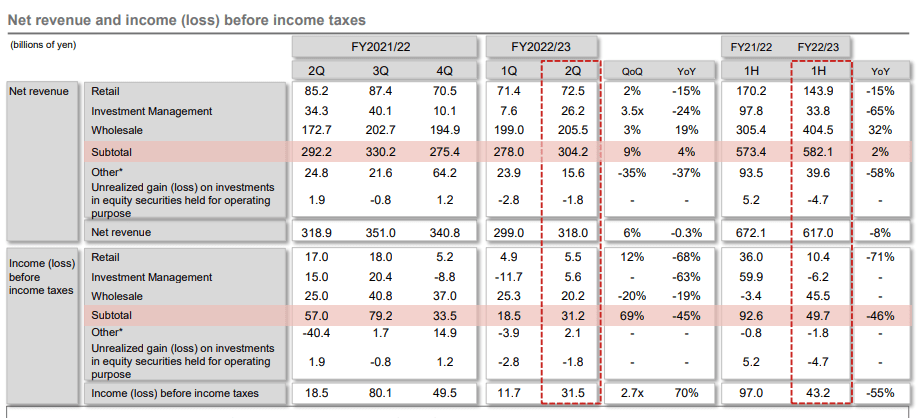

The Q2

The high level revenue disaggregation is the following, but it's not very descriptive, so we must go deeper.

{kind=link}

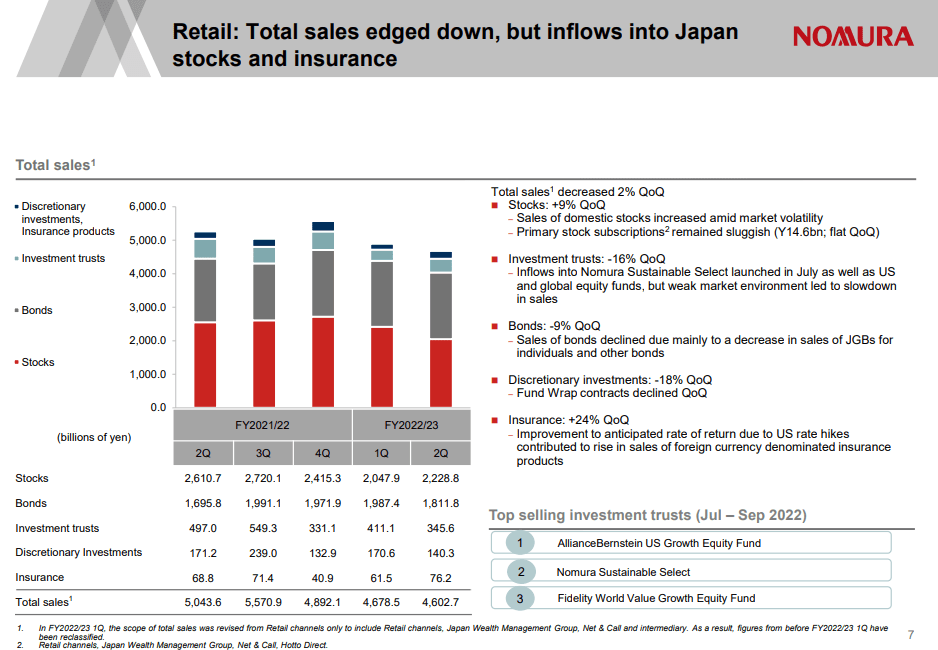

The retail businesses can be divided into recurring and flow revenue, where flow revenue is volatility related and includes the selling of stocks, bonds and other retail products. Recurring revenue, driven by the loan/deposit business and annuity sales etc. stayed strong and consistent thanks to stable BoJ policy while flow revenue shrunk YoY by 25%.

QoQ the commissions on the sales of stocks grew, but not on bonds as markets recently expected BoJ rates to rise and JGov bonds to perform poorly. YoY stocks contributed to declines while bonds contributed to growth, so the reverse effect and also demonstrating the strong retail support for bond investment in Japan, as opposed to countries like the US where it's more an institutional product. Investment trusts also declined quite precipitously QoQ and YoY as well as other discretionary investments which are driven by a consulting and financial advisory approach . So overall, stocks and insurance products did well QoQ, but stocks weakened YoY and insurance, which did grow YoY, is very marginal.

{kind=link}

Client assets continue to grow in the retail segment, and thanks to that, overall retail declines were not too bad at 15%.

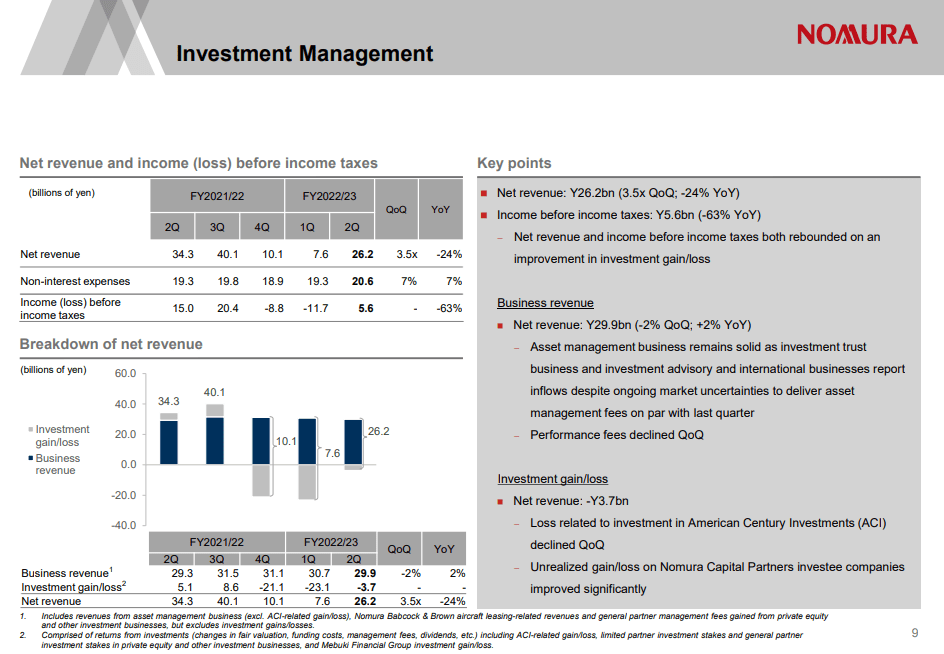

Investment management is another business, although it's 1/3rd of the size of retail. Here, revenue is recurring, but losses in the Nomura Capital Partners portfolio did a number on the final results. Business revenue was basically flat YoY and QoQ, but investment losses calculated mark-to-market hit the business with a 24% decline.

{kind=link}

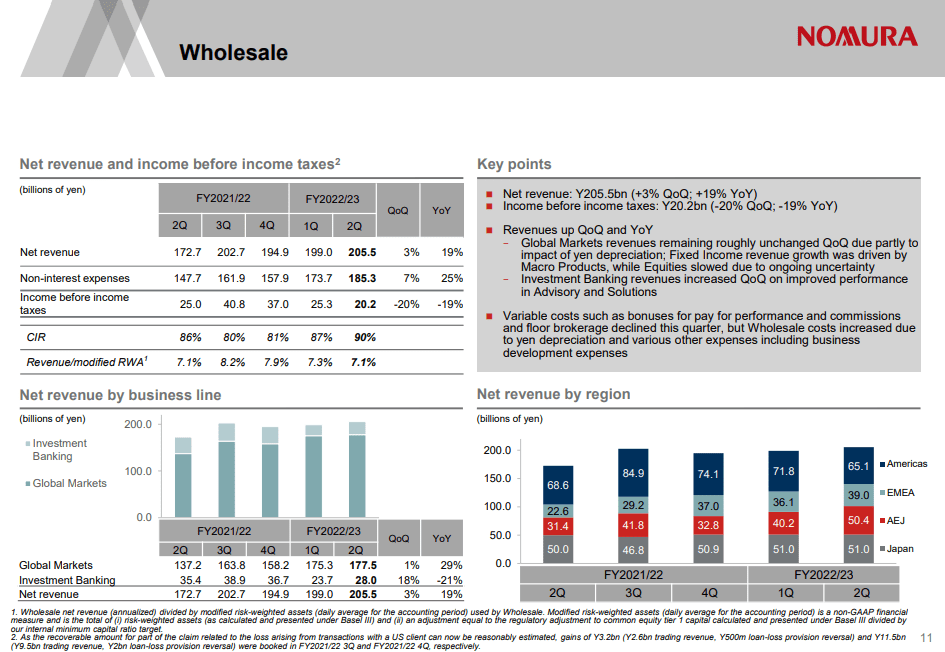

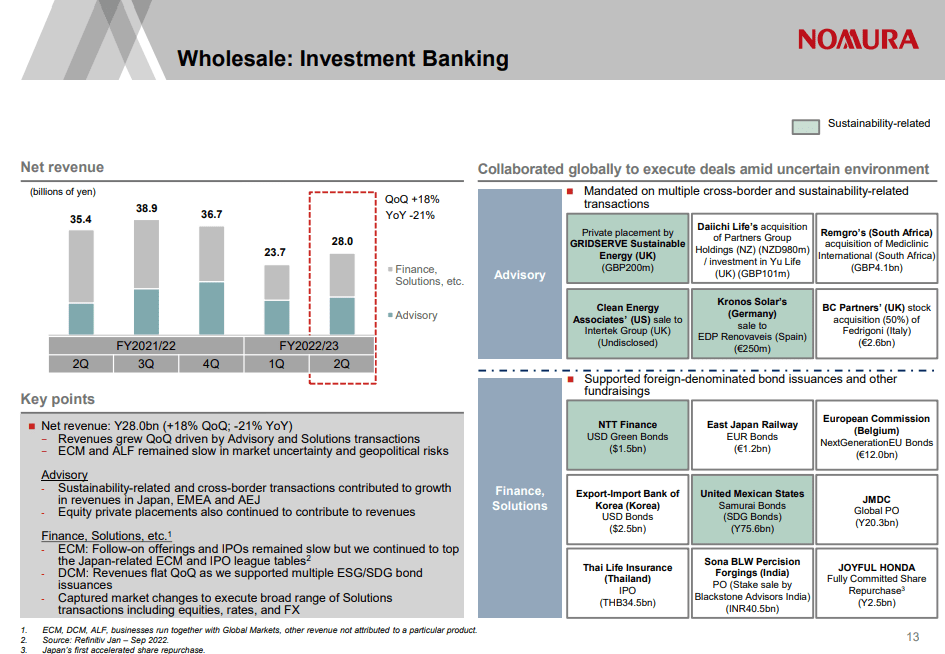

Wholesale is the most important business, and accounts for about 2/3rds of the revenue. Within it are the sales of wholesale products to corporates, including hedging instruments etc., but also investment banking services. Global Markets is the volatility levered business and it grew well by almost 30% YoY as corporates moved to hedge risks in the current complicated environment. Equity Products declined slightly even though volatility still supported good results in the business despite poor economic conditions globally and in Japan on account of the Yen's depreciation. But Macro Products, part of Fixed Income, rocketed more than 60% YoY.

{kind=link}

Investment Banking was the other piece of the wholesale business, and a very small one, accounting for more than the whole investment management business does in a typical business year. Its declines were 21% YoY comprehensively.

Surprisingly, Financing Solutions didn't suffer as much here as it could have, and this is because DCM activity didn't completely collapse as companies take advantage of the low Japanese rates. Asian revenue was the main growth driver in wholesale, where Japan-based revenue remained totally stable. The Americas were a weak point, and this is consistent with our coverage, where American focused peers suffered more in the corporate finance solutions area than Nomura has, but also Nomura reports that their agency mortgage business is pretty big there, and this slowed substantially on housing market concerns. Advisory is up YoY, which massively bucks the trend. Advisory is 50% of the IB revenue, so a 21% decline overall in IB is a testament to their resilience, despite large exposure to DCM and ECM which was a weak point globally. Advisory is benchmarked at around 30% declines for megadeal brokers, and still at around 15-20% for mid-market players in the US, so growth is a good marker. Greentech maybe has something to do with all of this.

The issue is that the growth in wholesale revenue did come with even more growth in costs. While some of this is extraordinary according to management, including some markdown effects from a challenge in the market environment, some of it is from difficulty in controlling cost outside of Japan, which is the majority of wholesale revenue. Still, relative to peers, performance could have been worse on the bottom line.

{kind=link}

Bottom Line

However, there is still operating leverage to worry about. While compensation declined as most businesses performed badly, EPS still declined 64%. Also looking forward, while IB may resume its performance, and likely other wholesale products like equities should keep performance strong there, IB is a small part of wholesale. And retail could have been harder hit, and probably has less room to recover. And the AM business is not performing badly in terms of client flows, even though its actual results end up being volatile due to mark-to-market accounting. In all, there's probably less room to recover than with other peers that do full-service corporate banking, and in terms of P/E at around 12x on forward income, Nomura trades in line. While the loans and deposits business might be slightly advantaged relative to global peers due to Japanese interest rates staying low, we still don't see a reason to pull the trigger here.

For further details see:

Nomura Loses On Low BoJ Rates In Retail, But Not In Investment Banking