NDLS - Noodles & Company: Disappointment Likely To Continue

2023-07-24 06:21:09 ET

Summary

- Noodles & Company, a fast-casual restaurant known for its pasta dishes, has seen its stock decline significantly, dropping nearly 40% year to date.

- Despite having unique offerings and a strong digital sales strategy, the company faces stiff competition, economic concerns, and leadership changes, making a rebound difficult.

- NDLS's financials are also concerning, with a small cash balance and significant debt, poor margins, and a failure to achieve profitability in two of the last three years.

For every high-flyer such as Nvidia ( NVDA ) there are stocks on the opposite end of the spectrum. When this company became public over ten years ago it was declared by some "the hottest IPO of the year."

A decade later this company is on the ropes as the stock has massively declined since their IPO and is down nearly 40% YTD.

With increased competition, economic concerns and a recent change in senior leadership, it seems this company will have a tough time rebounding. That organization is Noodles & Company.

The Company

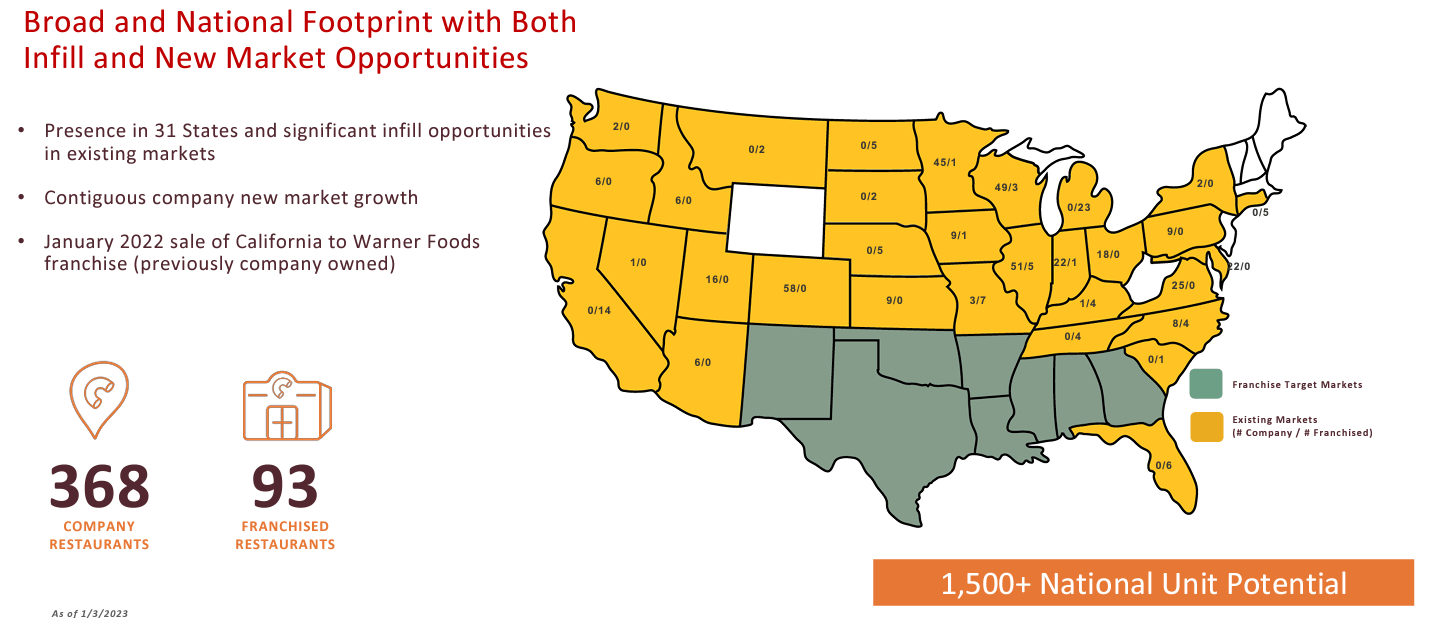

Noodles & Company ( NDLS ) is a fast causal restaurant that is known for their pasta and noodle dishes. As reported on the company's last 10K filing, Noodles & Company operates in 31 states and had a total of 461 restaurants. Of these 461 restaurants, 368 were company locations and 93 were franchise locations. The company has various unique pasta dishes they are known for including their "world famous macs."

{kind=link}

Noodles & Company went public in 2013. Over the last ten years the stock has continued to decline as it's now trading under four dollars a share.

{kind=link}

Moat and Opportunity

I think it's clear Noodles & Company has no moat. Although, it has unique offerings which differ from competitors, they are in very competitive industry with other fast causal restaurants such as Panera Bread and Chipotle (CMG).

As stated on a recent inventor presentation the company believes they have opportunities to expand their national footprint with possibly up to 1,500 new units.

{kind=link}

Noodles & Company plans to focus on digital sales which accounted for 54% of their sales mix in 2022. As part of their digital campaign the company has launched a reward program which had 4.5 million members in 2022. Noodles & Company is hoping that by rewarding customers and creating new innovative products consumers will be dying to try this will result in increased traffic and increased margin expansion.

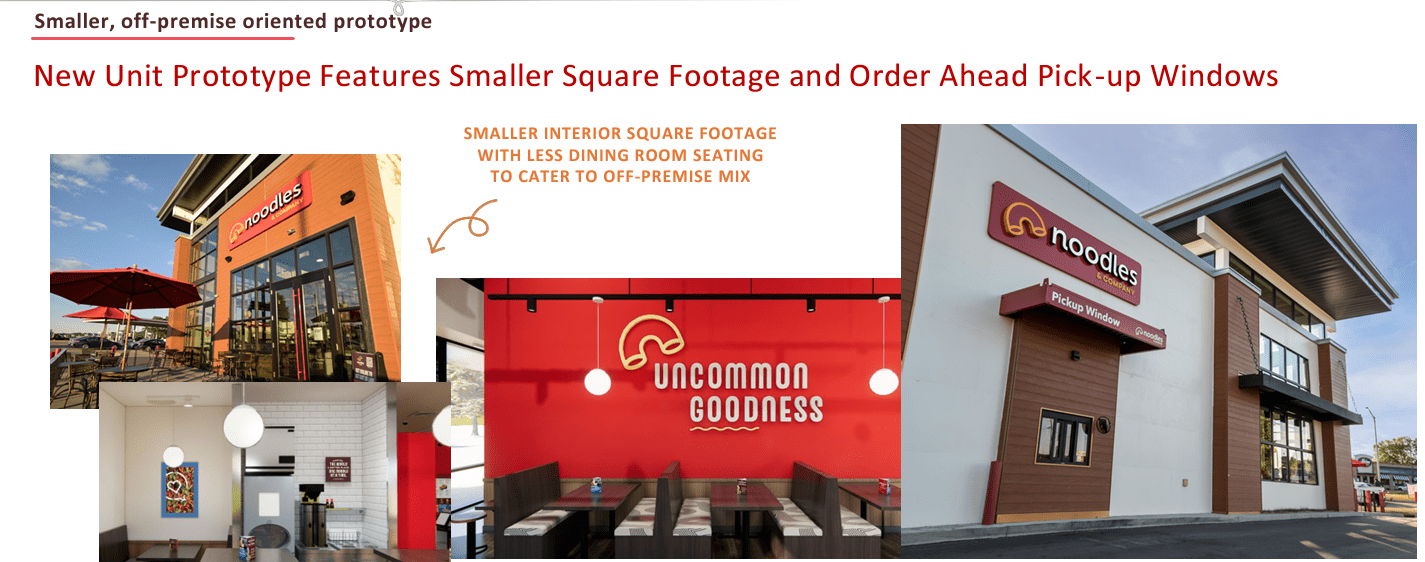

As stores roll out the company is focusing on having locations with smaller square footnote to prioritize takeout. Again, this aligns with their focus on being a digital leader in the fast causal space.

{kind=link}

Management

The CEO of Noodles & Company is Dave Boennighausen. Boennighausen has been with the organization since it went public. He served as the CFO until 2017 and then transitioned to the CEO role.

There has been a recent shake up in the CFO role as the former CFO Carl Lukach resigned in May to seek another opportunity. He held the role for just a couple of years.

Last month, Noodles & Company announced their new CFO would be Michael Hynes . Hynes comes over from Ruth's Hospitality Group where he was the Vice President of Finance and Accounting.

Only time will tell if Hynes can make his mark on the organization, but I find it troublesome Lukach left after such a short duration. Of course, the press release noted his desire to be closer to his family, but I'm inclined to believe there is more to the story.

Despite the CFO transition, I think it is beneficial Boennighausen has a long tenure with the organization. As you can see from the Glassdoor ratings, most employees approve of the job Boennighausen is doing. Also, compared to other CEOs in the restaurant industry 72% is on par if not higher than others (like the CEOs of Sweetgreen and Chipotle).

Glassdoor

Noodles & Company has received various additional accolades as well, indicating it appears to one of the better restaurant chains to work for:

Investor Presentation

Economic Conditions

The consumer has been resilient as the Fed has continued rate increases throughout 2023. However, I do believe consumer discretionary spending has slowed. As noted in this Seeking Alpha analysis (which I completely agree with) as student loan repayment begins again I find it highly likely consumer spending will decline even further and likely spending on entertainment and restaurants will be one of the first areas consumers will slash in their budgets.

Additionally, should a recession occur, a soft landing or hard one, I believe discretionary spending will certainly drop which does not bode well for Noodles & Company.

Competition

As noted on the Seeking Alpha's quant ratings, Noodles & Company is ranked dead last in the industry:

Seeking Alpha

In the company's latest investor presentation, it was stated that Noodles & Company appealed to teens and especially Millennials. However, in a recent Piper Sandler survey and several other surveys I researched Noodles & Company wasn't mentioned at all as a Millennial favorite. Restaurants such Chipotle, McDonald's ( MCD ), Chick-fil-A and Starbucks ( SBUX ) were the most consistently mentioned.

Financials

The balance sheet for Noodles & Company is not pretty. As you can see from the company's latest 10Q filing the cash balance is only two million dollars whereas the debt amount is significant.

SEC.gov

The company has used debt to fuel expansion, and I don't see a situation where that 1,500 new store goal is accomplished without this debt figure becoming even more inflated.

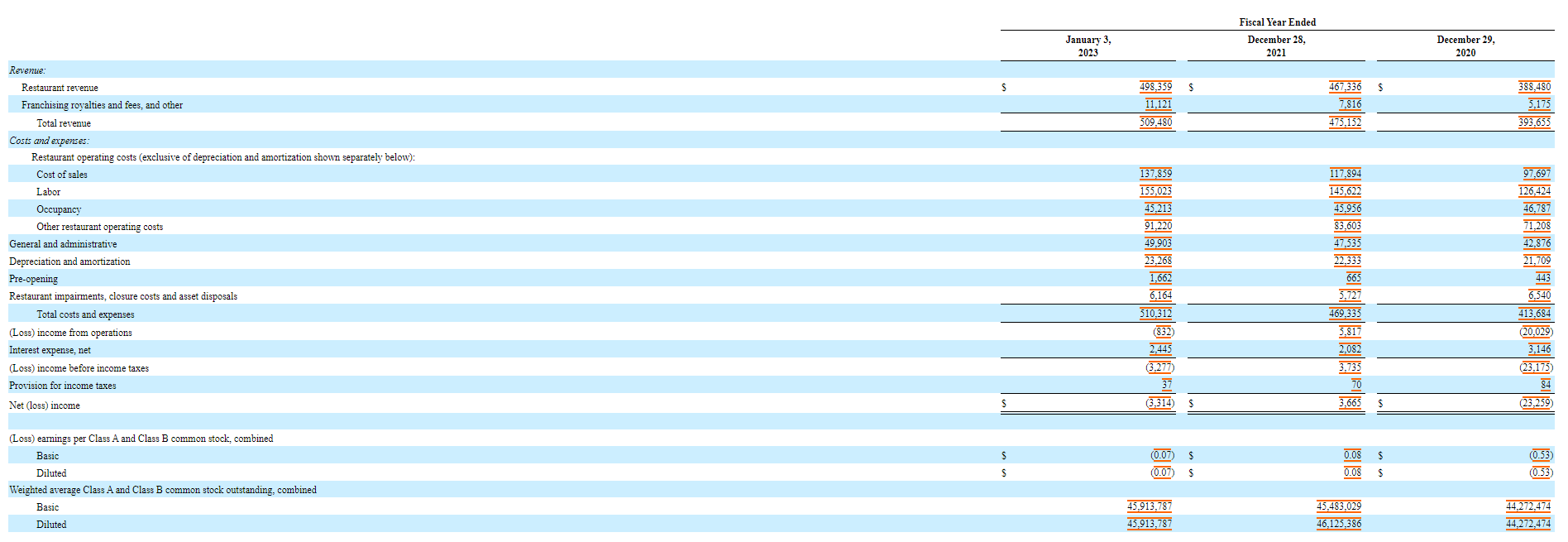

From a revenue perspective, Noodles & Company has managed to increase revenue over the last three years. However, costs have risen as well, and the company failed to achieve profitability in two of the last three years:

{kind=link}

Also, as another analyst noted, the margins for Noodles & Company are terrible. On the company's first quarter earnings call, Noodles & Company had a restaurant level contribution margin of 13.7%. For the year, the company is predicting full year restaurant contribution margins between 16% to 17% (which would be better than 14% the prior year). Compared to Texas Roadhouse ( TXRH ), their margin goal (as stated on their conference call ) is at a similar target of 17% to 18%. That estimate seems more attainable as Texas Roadhouse grew revenue, average unit volume, and comparable sales as traffic growth increased for the company.

In Q1 2023, Noodles & Company did not fare as well as Texas Roadhouse. Revenue increased however management mentioned a meaningful decline in delivery sales and mentioned price increases were impacting overall traffic trends. Additionally, the company noted seeing a reduction in the frequency of low to middle income guests. Management noted some success with their 7 for $7 menu and the introduction of the $10 mac and cheese meal.

Valuation

Despite Noodles & Company being a cheap stock it's not from a valuation perspective. As you can see from the below valuation metrics from Seeking Alpha, the overall value grade is a "C."

Seeking Alpha

I think this score is kind as I believe Noodles & Company is an overvalued company. Given the competition and economic conditions I find it difficult to believe this company can make significant improvements and alter their current trajectory.

Conclusion

Noodles & Company has unique offerings within the fast causal restaurant market. The company has a decent digital footprint, and it is promising to see many members sign up for rewards program.

However, I think there are more headwinds for the organization. The industry is very competitive, and Noodles & Company doesn't appear to a brand as beloved as other restaurants. The survey results, consumer sensitivity to price changes, and a reduction in traffic all illustrate this point.

From a financial perspective, the company's margins are poor and there is a significant amount of debt on their balance sheet.

Additionally, if consumer discretionary spending declines (or declines further) I think Noodles & Company would be negatively impacted.

Lastly, the CFO transition I believe also will impact the organization. I think it's a bad sign the prior CFO jumped ship after a short tenure, and it will take some time for Hynes to get up to speed.

As much as I like their mac and cheese, I'm not of fan of their business and I think Noodles & Company will continue to struggle.

For further details see:

Noodles & Company: Disappointment Likely To Continue