NDLS - Noodles & Company Is Gearing Up For Growth

2024-01-04 18:48:09 ET

Summary

- Noodles & Company has struggled with growth and profitability in the past few years.

- The company is making efforts to improve earnings growth with significant investments into restaurant count growth and initiatives for improving the profitabilty.

- The targeted goals for growth and profitability are still far off, and the current valuation of the stock does not provide upside for the risk.

Noodles & Company ( NDLS ) operates restaurants and works as a franchiser with a total of 377 company-owned and 91 franchise restaurants as of Q3/2023 . The restaurant chain offers dishes that mostly include noodles and pasta as the company’s name suggests.

{kind=link}

Noodles & Company's Progress in Recent Years (NDLS March Investor Presentation)

The company’s growth ambitions and profitability have lagged after the company became publicly traded in 2013. As a result, the stock has been a very poor investment – so far, the stock has lost 93% of its initial value. The following years could be Noodles & Company’s comeback to earnings growth, making the stock quite intriguing for a watchlist.

{kind=link}

Seeking Alpha

Years in a Growth & Profitability Hiccup

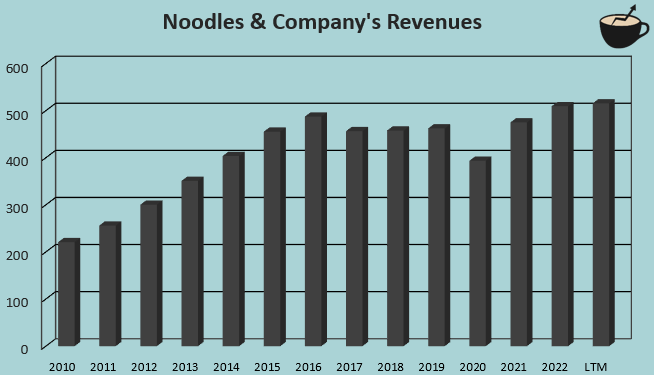

Noodles & Company has strived for store count growth. From 2010 to LTM trailing revenues, the company has achieved a CAGR of 6.9%, with the growth being mostly achieved in the earlier years of the available historical financials – from 2010 to 2016, the CAGR is significantly higher at 14.1%. Afterwards, growth has slowed down both prior to the Covid pandemic, and worsened in 2020 due to its effects.

{kind=link}

Author's Calculation Using TIKR Data

The hiccup in growth isn’t the only concerning financial after the initially good years in growth, as Noodles & Company has struggled with profitability as well after 2014. From 2010 to 2014, the company achieved a decent level in profitability with an average EBIT margin of 4.7%, but since, margins have dropped very near to zero with even negative margins in some years. Currently, Noodles & Company’s trailing EBIT margin stands at 1.5% , slightly up from 1.0% in 2022, but still at a poor level.

Gearing Up for New Earnings Growth

It seems that Noodles & Company is again gearing up for a recovery in growth. The company is expanding its franchising stores by at least 24 in 2024 within the southern part of the United States, as it sees a good opportunity in the region. On top of franchising growth, Noodles & Company has a growing amount in internal investments. After the company’s capital expenditures peaked in 2014, the company has had several years with quite minimal investments. The pandemic has started a new wave in the investments, though – the company has scaled its capital expenditures into a current trailing figure of $48.1 million, over double of the annual spend in 2017 to 2020.

{kind=link}

Author's Calculation Using TIKR Data

New units are estimated to have around $900 thousand in net development costs in Noodles & Company’s March investor presentation – although the current level in CapEx includes a good amount of maintenance-related costs, the amount also seems to include a high amount of new development. As new restaurant locations’ volumes take time to pick up, I believe that the company’s growth will start to slowly accelerate with the higher investment level. In the third quarter, the company opened up four new restaurants, but one franchise location was closed in the period.

NDLS March Investor Presentation

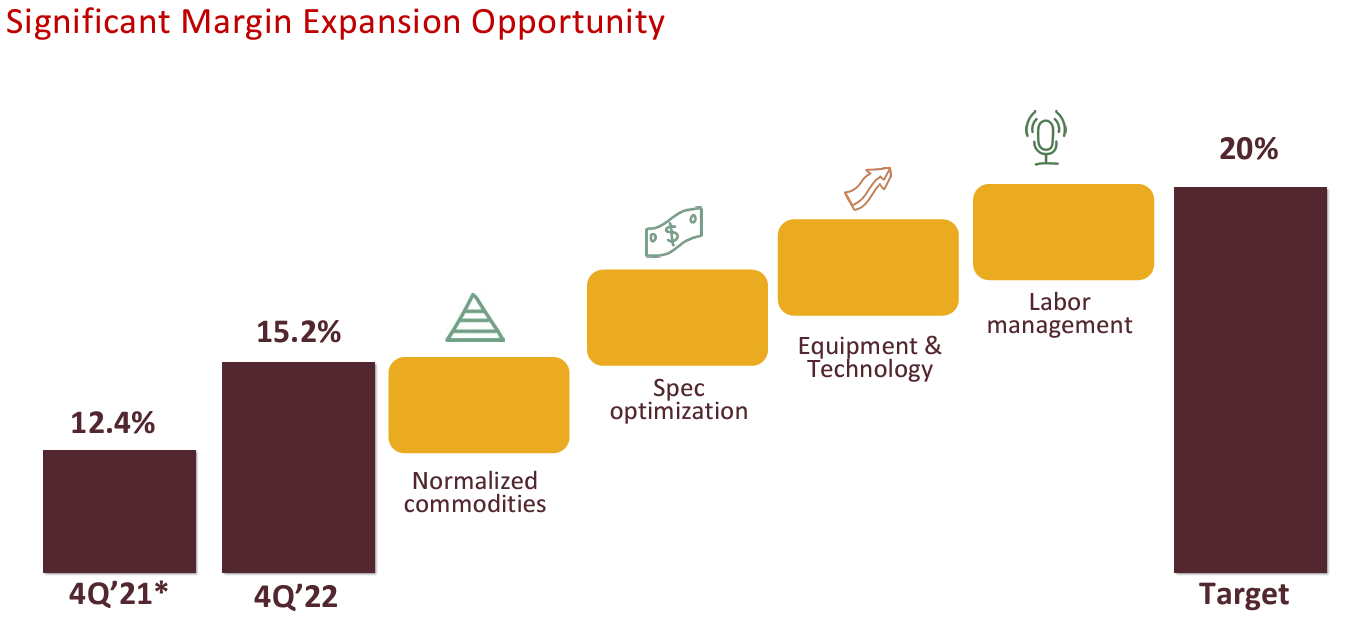

For the growth to be worthy of striving for, Noodles & Company needs to improve its profitability. The company has a number of initiatives to tackle the poor earnings. Firstly, Noodles & Company targets a store contribution margin of 20% through normalized food prices, better contracts for food, and a better in-restaurant technology that mainly mitigates some of the need for labor. In Q3, Noodles & Company’s contribution margin was 16.4%, still below the targeted figure, but slightly above the previous year’s figure of 16.2%.

{kind=link}

NDLS March Investor Presentation

Secondly, the company is trying to improve its annual volume per location to $1.5 million. Although the company doesn’t necessarily attribute the target to margin initiatives, I believe that higher same-store sales are a significant factor in driving profitability as a single location has a set amount of fixed costs including lease payments and overhead. The company targets the $1.5 million figure with better brand awareness, culinary innovation, digital and data transformation, restaurant modernization, and pricing capacity according to the March investor presentation. I believe that a better brand awareness plays a key role in the possible improvement, which a larger overall scale of locations could improve. In Q3, Noodles & Company had an average unit volume of $1.34 million as told in the Q3 earnings call – the company still has distance to the goal.

Although the goals are progressing, the targeted goals are still far off. The small efforts have still had a good impact so far, as in 2023 so far profitability has been better and the company’s EBIT margin in Q3 was 3.3%, 0.8 percentage points above the previous year’s level. I anticipate that a more solid macroeconomic background, and the restaurant base growth should start to affect the profitability as well at some point, but at the moment, I believe that investors should be quite cautious.

Valuation Doesn't Provide Upside for the Risk Yet

Due to Noodles & Company’s volatile margins, the company can’t be easily valued with a single key multiple – the company’s valuation depends largely on the future earnings growth rate. To estimate a rough fair value for the stock, I constructed a discounted cash flow model. In the model, I estimate the revenue growth to resume with a 2024 revenue growth of 7.5% and 2025 growth of 9%, that slow down into a perpetual growth of 2.5%. Altogether, the revenue growth represents a CAGR of 6.0% from 2022 to 2032.

For the margins, I estimate the margin expansion initiatives as well as store growth to have a good effect. I estimate the EBIT margin to expand from a 2023 estimate of 1.2% by three percentage points into an EBIT margin of 4.2%, achieved in 2026 and forward. The estimate represents a mostly good success in the initiatives, but does leave room for a positive surprise as well. With the large amount of capital expenditures, I estimate the cash flow conversion to be poor in the next few years, but to improve incrementally into a moderately good cash flow conversion.

With the mentioned estimates along with a cost of capital of 11.75%, the DCF model estimates Noodles & Company’s fair value at $2.76, around 9% below the stock’s price at the time of writing. The potential reroute to growth doesn’t seem to create upside at the moment, unless better margins than I estimate are achieved.

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Noodles & Company had around $1.2 million in interest expenses. With the company’s current amount of interest-bearing debt, Noodles & Company’s annualized interest rate comes up to 7.43%. The company has a decently high amount of debt at the moment compared to the equity valuation – I estimate a long-term debt-to-equity ratio of 40%, implying a similar financing in the future. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.97% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Noodles & Company’s beta at a figure of 1.65 . Finally, I add a small liquidity premium of 0.5%, crafting a cost of equity of 14.22% and a WACC of 11.75%.

Takeaway

It seems that after a hiccup of multiple years in growth, Noodles & Company is gearing up to accelerate the growth back. The company has had a significant amount of capital expenditures for restaurant unit growth and has multiple initiatives to improve the performance in all of the current restaurants. The targeted improvements haven’t yet had a very large effect, but have started to have some significance with an improved profitability in Q3. At the moment, the valuation doesn’t bring enough upside considering the risk level with currently showcased financials; for the time being, I have a hold rating.

For further details see:

Noodles & Company Is Gearing Up For Growth