NDLS - Noodles & Company: Poor Margins And Slowing Growth Are Concerning

2023-06-08 17:05:38 ET

Summary

- Noodles & Company has experienced a decline in share price due to worsening financial performance and a change in future outlook.

- The company faces risks from the rise of "Ghost Kitchens" and increased competition in the fast-food industry, but is well-positioned to cater to the demand for non-tradition QSR foods.

- Noodles & Company is leveraging menu innovation, limited offerings, and seasonal offerings to maintain interest in the brand and attract returning customers.

- The company's financial profile is poor. Margins are low, debt is climbing and growth is slowing.

Investment thesis

Our current investment thesis is:

- NDLS has some fundamentally attractive qualities, allowing the business to grow successfully thus far. In recent years, however, increased competition and changing industry dynamics have contributed to slowing demand.

- The financial profile of the business is concerning. Margins are poor and growth is slowing. We believe this is driven by increased competition.

- NDLS performs poorly compared to other restaurant businesses, primarily due to its GPM weakness and inability to maintain its growth trajectory.

- With difficult economic conditions, we believe NDLS will struggle in the coming year.

Company description

Noodles & Company ( NDLS ) operates fast-casual restaurants. It offers cooked-to-order dishes, including noodles and pasta, soups, salads, and appetizers. It operates company-owned locations and franchise locations.

Share price

NDLS's share price has experienced a monumental decline in recent years, as investors digest worsening financial performance and a change in future outlook.

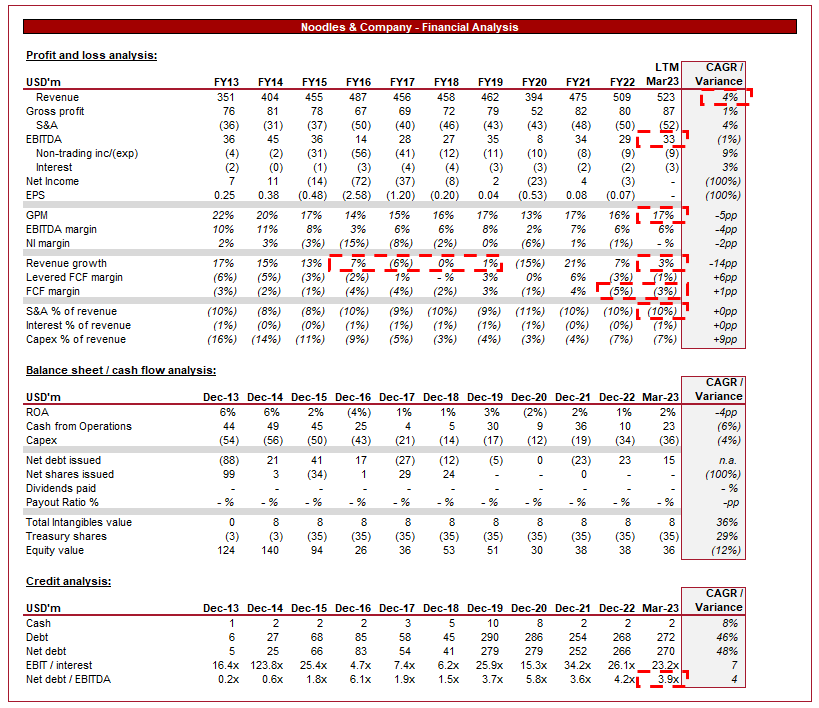

Financial analysis

Noodles & Co Financials (Tikr Terminal)

{kind=link}

Presented above is NDLS's financial performance for the last decade.

Revenue & Commercial Factors

NDLS has grown revenue at a CAGR of 4% across the last decade. The historical period began well, with strong growth and high prospects. However, growth slowed, and the business has found itself in a difficult financial position.

NDLS operates under a niche business model, combining quick-service convenience with a focus on high-quality ingredients and customizable options. The company is looking to convince the fast-food crowd that a healthier, potentially tastier alternative is available compared to traditional cuisines. Further, speaking of cuisine, NDLS operates in a segment (Noodles / pasta), which is underserved in the QSR space relative to burgers, pizza, etc. NDLS is estimated to be the second largest in the Asian cuisine segment, behind Panda Express.

The QSR industry has seen innovation in the last few years, with the rise of convenient food delivery and takeout options through apps such as DoorDash ( DASH ). This has contributed to a massive disruption in the industry, as consumers suddenly had significantly more choices and decisions are increasingly being made through scrolling apps (and less through traditional marketing). This represents an opportunity and threat for NDLS. The ability to discover the company is better than ever, but equally the pressure to diversify is high. If consumers just see the business as a generic noodle brand, they are going to bucket it alongside all the other generic noodle brands and choose based on reviews or price. This is what we feel has happened to NDLS, contributing to pressures to keep pricing aggressive.

For this reason, we are seeing increased leveraging of social media platforms for marketing, as well as design language to appeal to a younger audience (the users of these apps). We believe NDLS has done well here, its design language and site usability is very good, and the key message (affordable but quality) is conveyed well. Our prior concern remains, however, as the name gives the business the impression of being generic.

This concern around identity means NDLS is facing a risk from the rise of "Ghost Kitchens". Out of the rise of delivery companies has come ghost kitchens, which are brands created purely for the purpose of selling online, producing food in an industrial kitchen rather than an actual restaurant. These companies have incredibly low costs and can essentially platform themselves for free on the apps due to the desire to maintain the network effect. These brands are undercutting the traditional QSR players. We believe NDLS is not positioned well to face this threat.

Further, we are seeing increasing consumer demand for plant-based and vegetarian menu items. This has been driven by health issues and the development of food products to improve taste. NDLS is positioned well here due to the low reliance on meat.

Another factor NDLS is leveraging to maintain interest in the brand is menu innovation and the use of limited offerings / seasonal offerings. This strategy works well to attract returning customers, as well as encourage trying out options. The underlying strategy here is to win customers who are willing to repeat purchases.

Overall, we like the business model. The ability to customize and the difference in cuisine relative to other QSRs is attractive, however, we are concerned that the business lacks a noticeable moat. This makes growth difficult as we are seeing increased competition, which NDLS does not look positioned well to combat.

Economic & External Consideration

Current economic conditions represent a key risk to the business. We are seeing slowing discretionary spending as inflationary pressures negatively impact consumers' finances. With heightened inflation for an extended period, the concern is that the impact is compounding, increasing the chance of a material reduction in demand. Restaurant dining is generally discretionary in nature, which is the reason for this. This is likely the reason for the LTM revenue growth slowdown (3%).

Our expectation would be for NDLS to remain resilient given its affordable pricing, however, growth is likely to be minimal until economic conditions improve.

Margins

NDLS's margins are not good. The company currently has a GPM of 17% and an EBITDA-M of 6%. According to Seeking Alpha's factor grades, the average GPM for the industry is 35%.

This is likely a reflection of a highly competitive restaurant landscape, pressuring the company to keep prices low in order to maintain growth. This is why sufficient differentiation is key, as it allows for improved pricing.

Further, NDLS is committed to high-quality ingredients, stating "We use only the finest, most wholesome ingredients". This is understandable as NDLS looks to attract the segment of the market who are looking for fresh, quality foods. Also, a portion of this is likely driven by the need to stock a wide variety of ingredients due to the ability to customize.

Finally, the company has faced industry headwinds, as inflationary pressures have contributed to an increase in the national minimum wage. Due to the factors above, NDLS has been unable to increase prices in response.

We are struggling to see how margin improvement will materialize. Assuming pricing remains relatively flat / inflationary increases, but cost pressures maintain, margins will only rise with operating cost leverage, which is not sufficient. There are also questions to be asked regarding whether the high-quality, affordable pricing strategy is correct.

Peer analysis

NDLS is currently ranked 45 out of 45 (Restaurant industry) according to Seeking Alpha's quant rating.

The average 5Y revenue growth of this cohort is 16%, with NDLS underperforming this, achieving 3%. This is a reflection of the company losing steam at a point when delivery apps began to gain rapid momentum.

Further, the industry average EBITDA-M is 11.1%, almost double NDLS. Given the GPM deficit, this implies NDLS is performing well on an Opex basis. The issue is that increased marketing spend might be required in order to kick-start growth.

When compared to peers, NDLS' weaknesses are glaring. Growth has not only slowed to a halt but is far below the industry average despite being in its growth phase.

Balance sheet

NDLS has utilized debt in recent years to maintain its growth trajectory. This has left the business in a precarious position. It currently has c.$2m in cash and over $270m in debt. This represents a ND/EBITDA ratio of 3.9x, far too leveraged in our view.

The good news is that interest coverage is good, owing to the debt being mainly lease-related. However, this does restrict the company's ability to take on further debt in the coming years.

Valuation

Valuation (Tikr Terminal)

NDLS is trading at 13x EBITDA and 0.8x Revenue. This is a depressed valuation relative to its historical trading.

Our view is that the company remains overvalued relative to its current trajectory and commercial profile. The coming quarters look difficult, primarily due to weaker economic conditions. Looking more long-term, we struggle to see how margin improvement will materialize, as well as NDLS improving its competitive positioning.

Management

NDLS's share price declined c.15% in mid-May, driven by the announcement that their CFO would be departing, as well as an analyst downgrade. This is a concerning development as it is a reflection of views of the company's current trajectory.

Key risks with our thesis

The risks to our current thesis are:

- The NDLS brand has done well to grow thus far, and so if growth can increase, momentum may return.

- Operational and technological investment has the scope to generate margin improvement beyond what has been achieved thus far.

Final thoughts

NDLS has many attractive qualities. Growth achieved thus far has been strong, and the market does have space for a business offering what it is. The issues we are seeing are financial. Poor margins and slowing growth are highly concerning, with all momentum gone. Compounding this is the near-term uncertainty in the economy, and so we rate this stock a sell until we see evidence of a change in trajectory.

For further details see:

Noodles & Company: Poor Margins And Slowing Growth Are Concerning