NDLS - Noodles & Company: There Could Be More Pain Ahead

2023-10-25 04:35:41 ET

Summary

- Noodles & Company has been struggling with growth and low margins and a 5% price increase in February led to a 5.5% system-wide decline in comparable restaurant sales in Q2 2023.

- Noodles is now focusing on cost cutting but I doubt that it’s likely to be back in the black anytime soon.

- In my view, NDLS stock looks overvalued at 3.7x price to tangible book value and short selling seems viable as the short borrow fee rate is below 1%.

Introduction

I’ve been looking at investment opportunities in the US restaurant sector following my SA article on Flanigan's Enterprises (BDL) in July and this is how I stumbled upon Noodles & Company (NDLS). In my view there is a good short selling opportunity here as the company is in the red and its lack of a moat has been hampering its pricing strategy. Noodles is trading at over 3.7x price to tangible book value and I think it could go down below 1x in the coming months. The short borrow fee rate is just 0.41% as of the time of writing. Let’s review.

Overview of the business and financials

Noodles was founded in 1995 and is a fast-casual restaurant chain known for its noodles and pasta dishes. As of July 4, the company had a network of 465 restaurants across 31 states, including 373 company-owned restaurants and 92 franchise locations (see page 6 here ). Noodles focuses on millennial families and young adults, and it has a strong focus on digital sales, with about 54% of revenues coming from this channel in 2022 (see slide 10 here ). In my view, the company offers some interesting flavors of noodles and pasta products that set it apart from its competition – e.g., Wisconsin Mac & Cheese, Tortellonis, and Pan Noodles.

{kind=link}

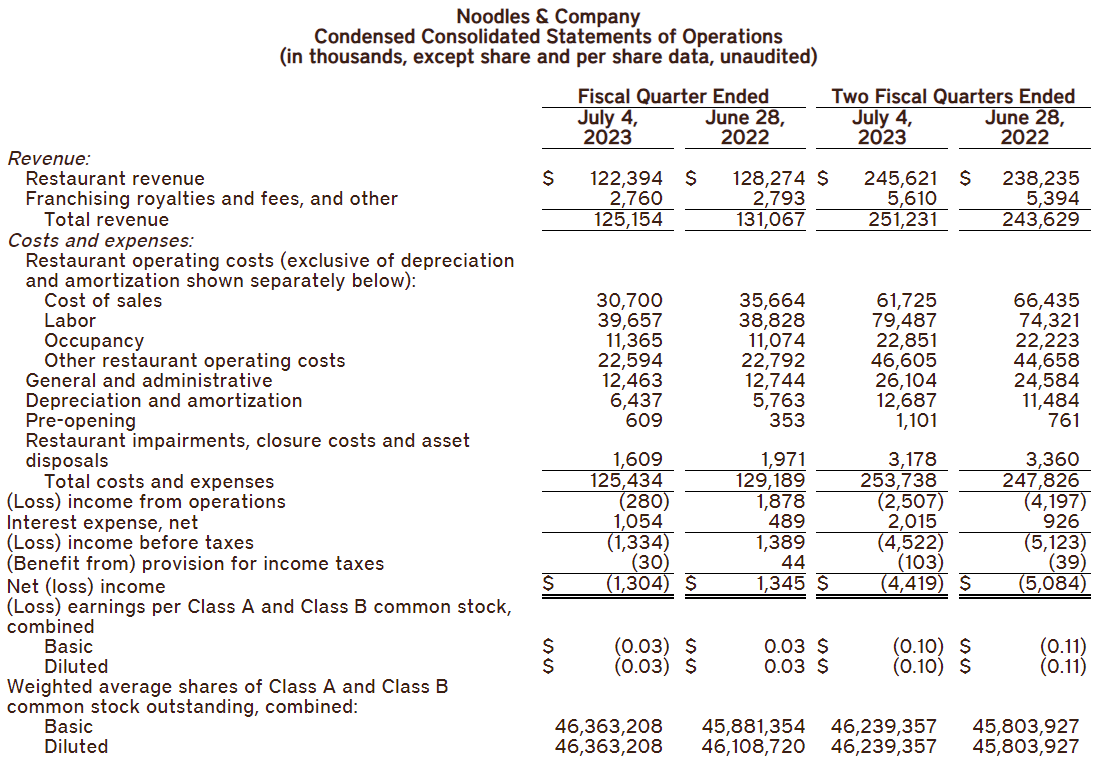

However, the fast-casual restaurant market is characterized by strong competition and low barriers to entry, which typically leads to low margins, and I think that having a few unique products doesn’t provide a good moat for the business. It’s also challenging to pass on cost inflation customers, and this is the main reason Noodles posted underwhelming Q2 2023 financial results. You see, the company implemented an incremental 5% price increase in February which it singled out as the key contributor to a 5.5% system-wide decline in comparable restaurant sales in the quarter due to a lower guest count. Total revenue was down by 4.5% to $125.2 million despite Noodles opening six new restaurants during the quarter while income from operations slipped into the red as fixed costs remained almost unchanged. The operating margin for Q2 2023 was minus 0.2% compared to 1.4% a year earlier. Another worrying development was that quarterly interest expenses surpassed $1 million.

{kind=link}

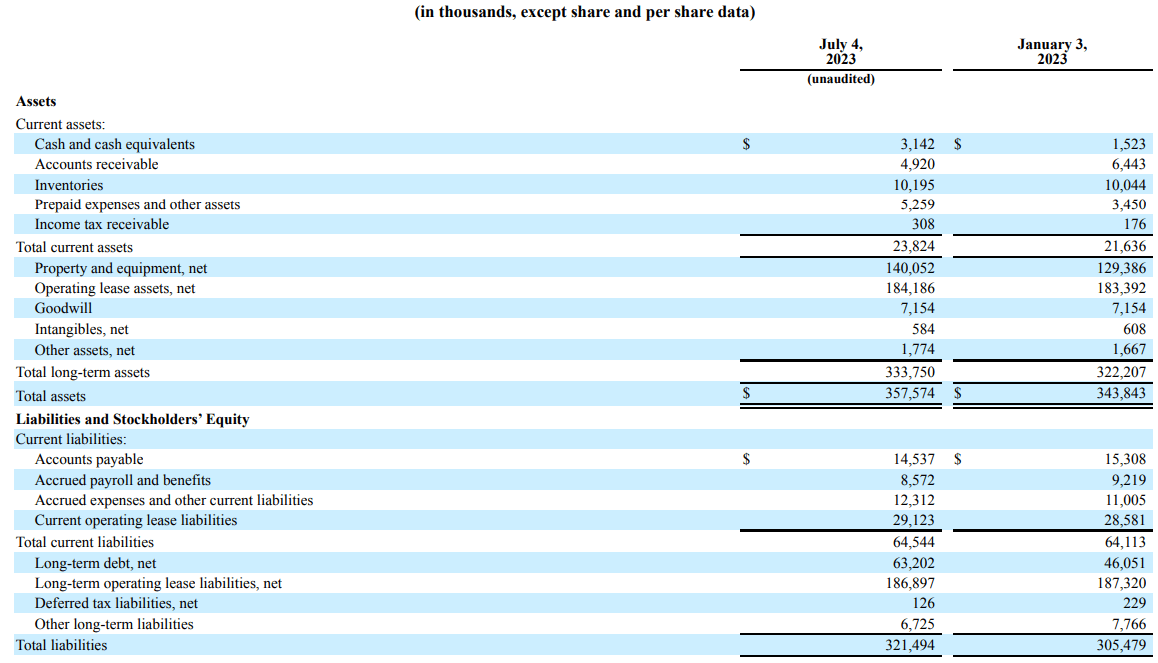

Looking at the balance sheet, net debt stood at $60.1 million at the end of Q2 2023 compared to $44.5 million at the start of the year as operating cash flow for the first half was $10.4 million while CAPEX came in at $23.9 million. In addition, lease liabilities were $216 million as of July 4 while the tangible book value was just $28.3 million or about $0.61 per share. Overall, I think the balance sheet of the company is in a rough shape.

{kind=link}

Looking at what to expect for the future, Noodles has now switched from price increases to cost cutting and growing its catering business to turn its financials around. While I think this is the right move considering customers are highly sensitive to price increases, I doubt that there is much room for improvement in the cost structure. In addition, even a significant growth of the catering business is likely to have an inconsequential impact on the company’s results considering it accounted for just 1.4% of sales in Q2 2023. In view of this, I think that Noodles’ expectations for revenue of $500 million to $510 million and operating income of adjusted EPS of minus $0.11 to $0.00 for 2023 could be overoptimistic. And considering CAPEX for the full year is forecast at $45 million to $50 million, I expect a further increase in the net debt level, possibly above $75 million by December. Noodles is set to release its Q3 2023 financial results on November 7 and I think that operating income for the quarter is likely to be in the red once again.

Turning our attention to the valuation, I think that it’s better to look at EPS and price to tangible book value here than EV/EBITDA considering this is a business with high depreciation due to the large size of lease liabilities - depreciation and amortization for 2023 are expected to come in at $26.5 million to $27.5 million. EPS is negative at the moment, and I don’t expect this to change anytime soon. Tangible book value is also decreasing and Noodles is trading at 3.7x price to tangible book value as of the time of writing. In my view, this seems high for a restaurant business that is struggling with growth and low margins and I think it could gradually decrease to below 1x over the next several months.

Overall, I think the business of Noodles isn’t worth much in its current state and I think that this could be a good time to open a small short position as data from Fintel shows that the short borrow fee rate stands at 0.41% as of the time of writing. Looking at opportunities to hedge the risk here, $2.50 call options don’t look expensive at the moment.

{kind=link}

Turning our attention to the upside risks, I think that the major one is that the prices of microcap stocks can increase significantly without clear catalysts. It’s also possible that I’m underestimating the prospects for the business and Noodles gets back in the black over the coming quarters. In addition, the business could return to growth soon thanks to franchise deals. In August, the company announced deals for 24 new franchise restaurants.

Investor takeaway

Noodles operates in a tough sector, and it has been struggling with growth and low margins lately. Raising prices proved to be a bad move as comparable sales dropped but I doubt that cutting costs will put the company in the black either. In addition, free cash flow is negative and net debt has been rising rapidly which resulted in interest expenses more than doubling in Q2 2023. Overall, Noodles is in a tough spot with no clear way out and I think the company looks significantly overvalued at 3.7x price to tangible book value. Short selling seems viable as the short borrow fee rate is below 1% and call options are relatively cheap. Yet, it could be best for risk-averse investors to avoid Noodles. This is a microcap stock and it takes over six days to cover at the moment, which means that there could be significant share price volatility ahead.

For further details see:

Noodles & Company: There Could Be More Pain Ahead