NRDBY - Nordea: An Interesting Scandinavian Bank But Overvalued At Current Price

Summary

- I've written about Nordea directly and indirectly over my career as a Seeking Alpha contributor.

- Nordea, like most of the incumbent major banks including Swedbank, Handelsbanken and SEB, is a great business - but it's also stagnated in terms of growth.

- Valuation is key to investing in any of the banks - and all of them are currently at a very high valuation. For that reason, I consider Nordea either fully/overvalued.

Dear readers/followers,

Boy, it's been some time since I covered the Scandinavian/Nordic banks and Nordea (NRDBY) in particular. In fact, when I last wrote specifically about Nordea, it had a different ticker, Biden wasn't president, and we weren't even in COVID-19.

Out of the major Scandinavian and Swedish banks I follow, Nordea is the "least Swedish" of the bunch, owing to its domicile for a few years actually having moved to Finland for a myriad of reasons - most of them related to taxes.

In this article, I'll provide a comprehensive bank overview, and give you my target for Nordea - but I'll be a bit of a spoilsport here and say - this one is highly valued at this time, and I wouldn't buy the common share.

Let's get going.

Nordea - Reviewing the bank

Nordea is a Nordic (not Swedish, Nordic) bank and financial company. Its roots go back "only" about 22 years, when it was formed by merging Merita-Nordbanken, a Swedish/Finnish bank that itself was the result of a merger. It then merged with Danish Unibank, which resulted in the name Nordic Baltic Holding.

After the purchase of the Norwegian Kreditkassen, another bank but in Norway this time, the company took the name "Nordea", a play on its clear Nordic roots in all of the Scandinavian countries, with roots in all of them.

The company's headquarters were moved to Finland in 2018, which also on a formal level means that Nordea is part of the European bank union - which Swedish banks because we don't have the Euro, are not (in the same way). There was also a myriad of other reasons for the move, many of them tax-related.

Nordea is one of the largest banks in all of Scandinavia. It has over 11 million customers, over 1,400 global offices, and 700,000 commercial customers, and its internet banking platform is one of the most used, with 260M transactions per year. It employs over 25,000 people and has a strong shareholder history.

The company once had very strong shareholders in the form of Sampo (SAXPF), the finished investment/insurance company. However, Sampo divested all of its Nordea, once owning 21.3% and today owning essentially 0% of the company. Instead, Nordea is owned by SEB Funds (11.2% of capital and votes), followed by BlackRock (BLK), Cevian Capital, Nordea Funds, The Central Bank of Norway, Vanguard Funds, and a whole other host of funds owning between 1-5% of the bank's shares and voting rights.

Not an entirely negative shareholder picture.

Nordea is a high yielder - even as valued as it currently is, the yield is still over 6%, and that's because Nordea's dividend policy goes up to 70%, with excess capital returned as well through the use of buybacks while maintaining a buffer of around 150-200 bps above CET1.

Nordea has, overall, withstood the trouble of the times quite excellently. During times of low-interest rates, the bank has focused on fee-oriented income generation as opposed to NII. Loans and AUM are solid, even during pandemic trends.

Nordea IR (Nordea IR)

The bank, moreover, has an established trend of growing income faster than growing cost/OpEx. Structural cost reductions have been a thing for Nordea, which has managed to reduce the cost-to-income ratio by 9pp over the past 3 years - it's not just a fluke when it's 3 years of reductions running.

Dividends, of course, took a hit during the pandemic as well as due to political pressure, but the company came back with a "roar" in 2021, delivering beyond-solid dividends and buybacks in -21.

Nordea IR (Nordea IR)

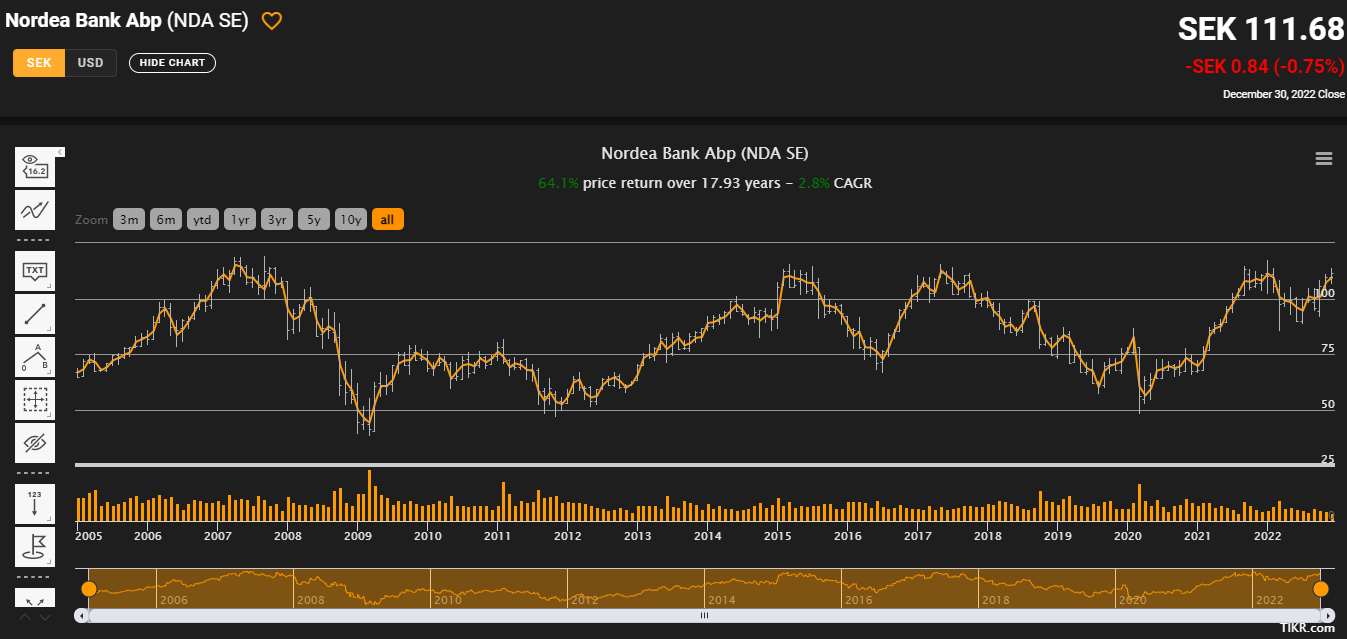

Unfortunately, the bank known as Nordea is a market underperformer. Long-term investing in this bank does not looking at the history, make for a good case in investing.

{kind=link}

The company performed significantly below market due to the inherent volatility to the stock. As you can see above, several troughs as well as several highs. While volatility may be unpleasant for some investors, remember that for value investors, we actually find this to be positive. It means that not only can we buy "cheap", but we can also make a reasonably-based approximation of when a stock or a company is trading above, or at the level, it's going to before coming down.

Put it simply, I wouldn't be mad if I sold Nordea at 110 and it grew to 120 before crashing - because it doesn't, historically, go much higher, and I don't see many catalysts in the near term for it to do so. Similarly, I would buy Nordea to "the gills" at below 40-60 SEK and would be happy to hold indefinitely or until the company climbed back up again.

Scandinavia is a very specialized banking region. You can see that in Nordea's history. It's no fluke that Nordea was created by merging many banks, and that the same story has been going on for years prior to and around that time. Scandinavia is a banking geography run by incumbents - I would argue that the major ones are DNB ( DNBHF ), Swedbank ( SWDBF ), Nordea, SEB, Handelsbanken ( SVNLF ), and Danske Bank ( DNKEY ). There are a few smaller ones around, but these are really the major ones that most people have. Even if you like me, have savings accounts in 3 other banks, and 2 other banks for brokers, you usually have accounts across one or more of them.

These banks cannot be dislodged without outside interference - and outside interference is very unlikely because as most major banks have found out here, it's not easy making a profit against these established banks.

What I am saying is that all of these banks are technically decently attractive, and I've owned stock in all of them at some point - as well as most of them now, at a good cost basis. But it's become time to consider rotating here, which is why out of 4 of them, I currently have opened call options on 3 - Nordea being one of them.

However, Nordea at its heart is attractive. The current interest rate environment means a massive increase in NII, upwards of €1B at the very least as Nordea expects.

Nordea IR (Nordea IR)

At the same time, NII-related headwinds are back - meaning wholesale funding costs are up, and costs to hedge deposits are up as well. Actual pass-through NII increases will depend on the specifics of these, and the specifics of the rate hike cycle in the bank's various geographies.

Impaired loans that the company has is low - but not market-leading. Handelsbanken is far better, and Nordea is at around 0.88% that are in stage-3 impairment.

The current macro outlook in Scandinavia is heavily impacted by the high inflation and rising interest rates. The next few years are unlikely to be all that great, but Nordea has other income drivers in the meantime, and as you can see, unemployment hasn't really reached or climbed to alarming levels here.

Nordea IR (Nordea IR)

The GDP estimates are still somewhat positive as well - at least if you disregard Sweden, which is expecting to see a dip of 0.5%, compared to the other Nordic states which are positive with Norway leading at 1% 2023 growth, but back to full growth for all in 2024.

Still, Nordea owns the best-rated and best-performing online bank in Scandinavia - it has very satisfied customers, and it's leading the charge in ESG metrics - if you're interested in that sort of thing.

Expectations are for the bank to continue to perform well. P&Ls are stable, with recent operating income up 7% YoY, and pre-loan-loss profit up 9% YoY. EPS is up 2 cents on a diluted basis YoY, and numbers like NII, deposit margins, and other things are all up.

{kind=link}

However, headwinds persist and the competition from the other 5 major banks means that there is a cap to the performance that Nordea can achieve. With funding costs what they are, and banks battling for mortgage customers, there is a limit to how little a bank can charge and still make a profit. This means that it can become clearer when the market is overreacting in any one specific direction, and that's what I take advantage of when it comes to any of these banks.

So, here's the case for Nordea.

Nordea Valuation

Nordea is currently above a triple-digit share price in terms of SEK. That's not a situation I like, because typically, that's an indication that it's overvalued. It's not like Handelsbanken, where the bank may crawl around that 100-110 level for some time - which is why my covered calls for Handelsbanken are close to at 130 strike.

For Nordea, once the bank hit that triple-digit, I was busy on the options chain looking at the best opportunity to take advantage of the situation - and I found one (more on that later).

Nordea natively trades in Euro on the Finnish stock market - but it has Danish and Swedish listings as well - you can take your pick, or go for the ADR.

Banks have been enjoying higher valuations as NII has come back to play - and Nordea is absolutely no exception to this trend. Current analyst PTs from S&P global range from 110-120 SEK, or translated to €11-€12 on average, with an average of €12.11. 10 out of 15 analysts are currently viewing the company as a "BUY" or an "Outperform", in part certainly for its role as an income generator, in part because of comparative exuberance.

I am not at a "BUY", because I look beyond current trends, and the fact is, some of these analysts can't really be trusted with their PTs because they shift like the wind.

{kind=link}

While the analysts can be excused for the dip in -09 - it was the financial crisis after all, there is to my mind no excuse for the dip during COVID-19. Were they expecting banks to suddenly be worth half due to a pandemic? And then in less than 6 months or 10 at most, suddenly worth half again as much - double?

What you see here is the reason that I take most of these analyst targets with more than a pinch of salt - they're too event-driven. I take advantage of such events - on both sides. When a bank drops as it did during COVID-19, I buy, I don't shift my price targets.

The same is true now when it's high as this.

My average long-term PT for Nordea has ranged from 65 to 85 SEK for the past few years. While I can understand that you might "Hold", until about 110, as I am doing now, I don't see a long-term case to be made for buying above 90 SEK at any time.

This is not rocket science. Nordea typically commands a 10-year average LTM price to BV/share of 1.18x-1.2x - no more than that. The latest is 1.35x - with a record high of 1.7x and a record low of 0.56x. This shows you about where you want to get in with Nordea, and that certainly is not today.

I want a good upside, and I see a good upside below 85 SEK/share. Above that, I'm just not "that into it".

Here is my current thesis for Nordea.

Thesis for the common share

- Nordea is a sector-leading sort of banking play in the Nordic region, with a presence across one of the most attractive banking regions in the world due to its incumbent status. The bank is well-capitalized and has an almost-un dislodgeable position in the market. It has an attractive yield and good growth prospects.

- However, it's all about valuation - and I don't see a good valuation here. in terms of Book value, earnings, and other relevant multiples, Nordea shows all the signs of being slightly above its standard valuation trend, calling for me to give it a "HOLD".

- That is what I am doing. PT is 85 SEK/share, and I'm at a "HOLD" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The covered call play

I've written options on the Swedish version of the Nordea share, with the following specifics.

Nordea Call (Author's Data)

To be clear, I want this to expire ITM. That's why the long period, and that's why the good premium. Nordea has never reached a share price of 120, nor the 125 sales basis I'm going in with. Aside from a great yield, I'll also be selling at nearly a 68% profit including dividends, which is great. If it falls back down, that's fine too - but that's my reasoning for putting it so close here.

Questions?

Let me know!

For further details see:

Nordea: An Interesting, Scandinavian Bank, But Overvalued At Current Price