NBNKF - Nordea Bank: 8.2% Yielding Bank That Has Fallen Under Radar

2023-07-01 04:34:45 ET

Summary

- Nordea is the largest Nordic bank, which is well-capitalized and significantly de-risked from unfavourable exposures to risky markets and volatile corporates.

- Nordea's exposure to Nordic economies provides favourable conditions to deliver long-term earnings growth in a prudent manner. Nordic households and corporates are extremely resilient, and public sector carries extremely low debt loads.

- The higher interest rate environment benefits Nordea as it allows to generate stronger NII results, reduce cost-to-income ratio, and ultimately embark on massive share buybacks.

- Yet, the market has been discounting Nordea's stock below its 3- and 5-year historical average and well-below its peers, which have not performed that well.

- I expect to enjoy at least 30% of returns via price appreciation (via multiple convergence to more justified levels) and additional 10% from the shareholder yield in 2023.

Brief overview of Nordea

Nordea Bank Abp (NRDBY) is a universal bank, with 200+ year history, operating primarily in Sweden, Denmark, Finland, and Norway. It generates ca. 60% of its income via vanilla lending products such as mortgages, household loans and corporate loans. Nordea is also the leading bank in the Scandinavia for underwriting equity and debt issuances, which constitute about 10% of its total income. The bank also provides life and pension, savings and asset management, as well as private banking services to high net worth individuals.

The lending portfolio is well-distributed among the Nordic countries: Finland (21%), Denmark (24%), Norway (22%), and Sweden (33%).

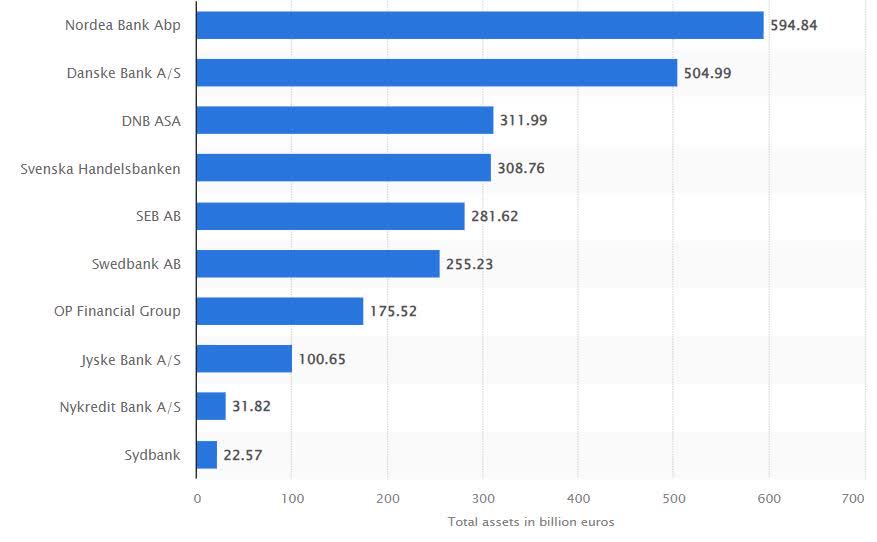

As of now, Nordea has roughly $37 billion in market cap and is classified as the largest bank in the Scandinavia (by total asset size).

{kind=link}

Investment thesis

Currently, Nordea accounts for ~30% of my total portfolio value. I have held Nordea in my portfolio since late 2018, when I wrote my second Seeking Alpha article that happened to be about the Company ( Nordea Bank : Secure 9.75% Yielder).

{kind=link}

During the holding period, Nordea has clearly outperformed both U.S. banks and its European peers.

Below I will articulate 6 reasons, why Nordea is still a strong buy and why I am still reluctant to consider reducing the significant concentration risk in my portfolio.

#1 A critical ingredient for long-term success is the presence of secular tailwinds, which Nordea has plenty of

The combination of Nordea's geographical presence and its size allows it to capitalize on the structural forces stemming from the great Nordic economies.

For so universal and dominant bank as Nordea it is vital to have healthy economy that is underpinned by financially resilient households, Governments (i.e., with strong fiscal power/buffer) and vibrant corporates.

And here are several facts, which elegantly capture the story of Nordic economic environment in the context of banking activity.

Nordic societies rank global top ten in:

- Social safety nets (#1 Denmark, #2 Finland, #3 Norway and #9 Sweden)

- Digital transformation readiness (2# Denmark, #6 Sweden, #8 Norway and #9 Finland)

- Sustainable development goals index (#1 Finland, 2#Denmark, 3# Sweden and 4# Norway)

{kind=link}

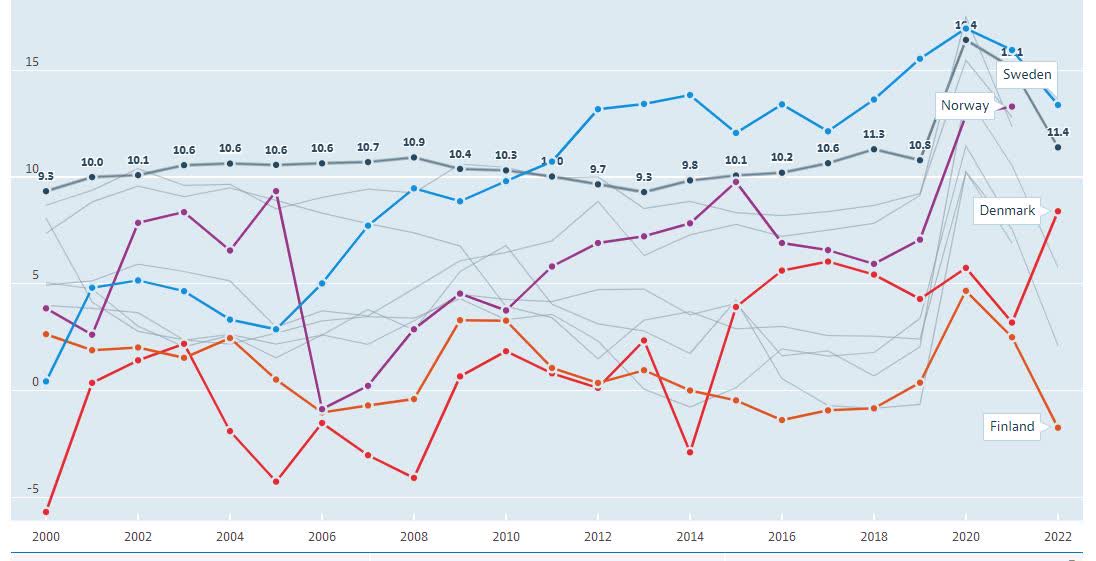

Among the G7 countries, the Nordics (except Finland) have one of the best households saving rates as a percentage of the total disposable income.

{kind=link}

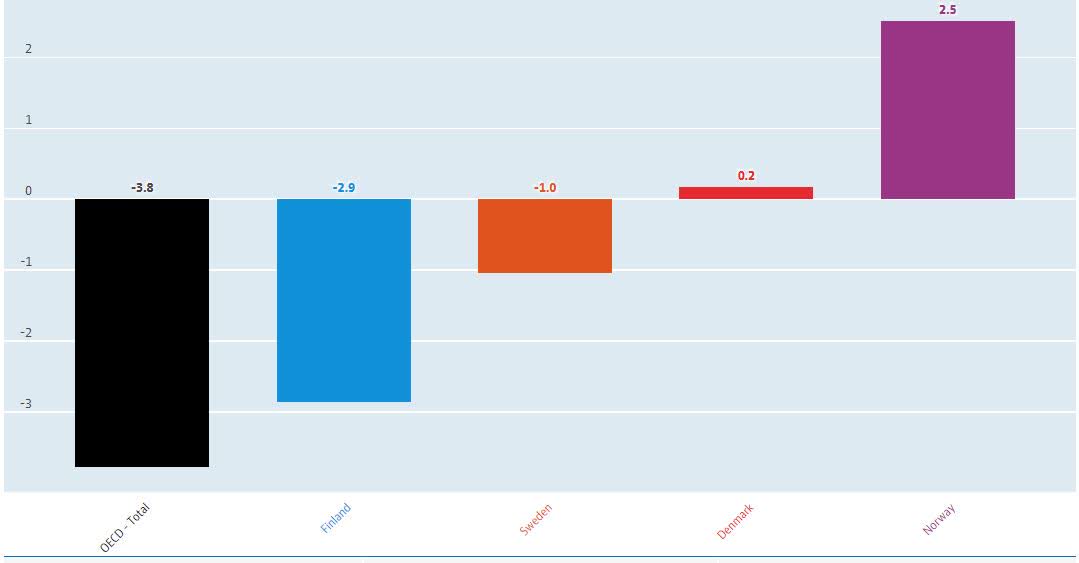

Compared to the OECD total, in 2022 the Nordic households were more resilient to the recent economic turbulences, where the disposable income as a percentage of the GDP per capita fell less and in Norway's case even experienced a slight uptick despite the surging inflation and global economic headwinds.

IMF

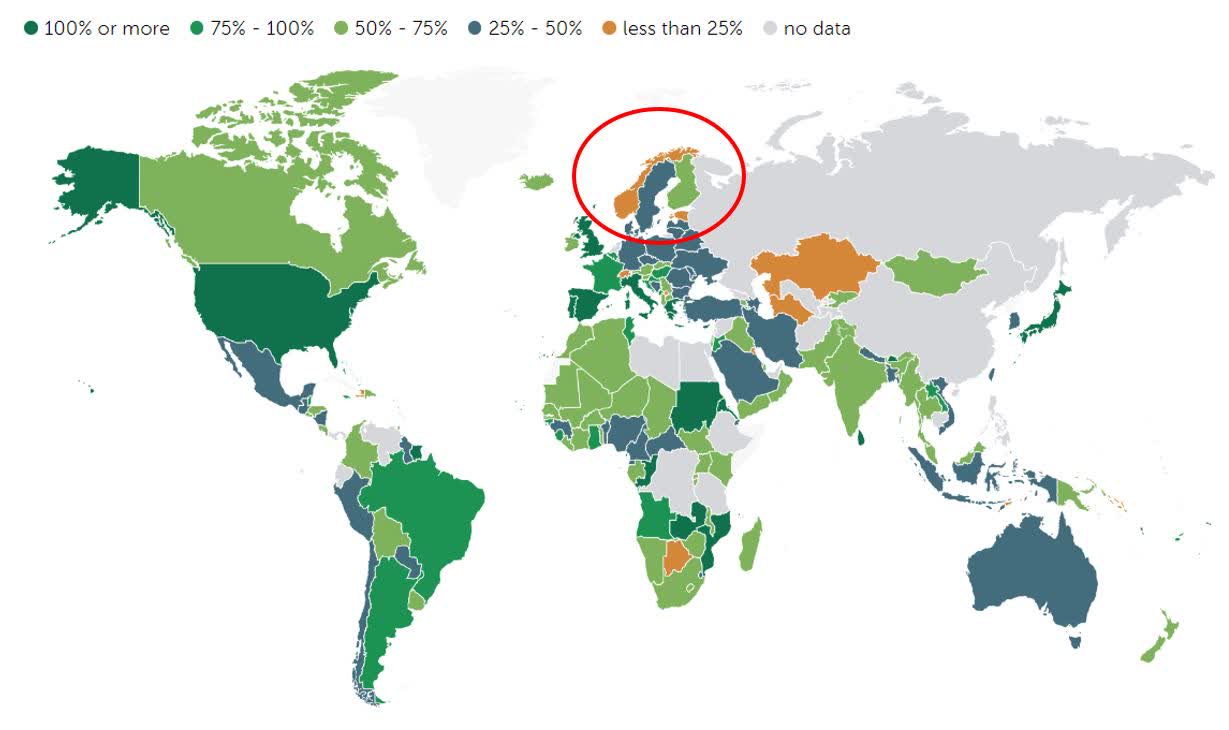

The corporate side in the Nordic market is also robust, which de-risks the lending activities. According to the most recent Financial System Stability Assessment (2023) by IMF, the corporate debt amounts have gone up, but are offset with stronger accumulation of equity.

{kind=link}

The Nordic Government debt metrics are rather healthy as well with the highest debt load attributable to the Finnish Government (i.e., 55% of the GDP).

Nordea investor relations

Going further Nordea estimates healthy growth rates in mortgage and corporate lending as well as in savings activity for all four markets in which the bank operates in.

Given that Nordea is a bank of a systematic importance, it is heavily exposed to the systematic risk. In other words, if the Nordic economies drop, Nordea's share price should respond accordingly considering how important role it plays in the economies. So, the fact that all four Nordic markets embody healthy fundamental characteristics, the market (systematic) risk seems to be of a relatively low concern.

#2 The resiliency of Nordea's markets provides a structural shield to loan book from unfavourable provisions and write-offs

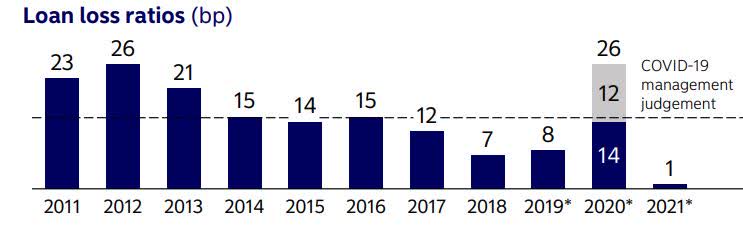

There are two angles from which we could test the level of risk that is embedded in the Nordea's loan portfolio. First is through the loan loss ratio back in the COVID-19 era and second is through both impaired loans and internal estimates (which are governed by robust procedures) on the probability of defaults in the current macroeconomic environment.

{kind=link}

During the pandemic, Nordea managed to deliver superb results by registering loan losses at a lower level than its historical average. The discretionary loan provisions made in 2020 were successfully unwound later in 2021, which still resulted in a more favourable loan loss ratio than 2011-2021 average.

Nordea investor relations

As we can see in the chart above, even under these challenging economic dynamics, where credit has become more expensive and where inflationary forces have eroded purchasing power, Nordea has delivered once again.

The percentage of impaired loans and the loans subject to elevated risk of default remain extremely low and are characterized with positive rate of change since Q1, 2022.

Now, it is not a secret that one of the risk hotspots in the Nordic economies is the commercial real estate market, which has experienced massive boom since the GFC forcing many corporates and households to assume loads of leverage. When the ECB, Riksbanken (Swedish central bank), Danmarks Nationalbank and Norges Bank have all switched to a restrictive monetary approach, the already highly leveraged real estate market has automatically become even a more serious concern than prior to the rate hikes.

However, even this aspect has been well-managed by Nordea.

Nordea investor relations

As of Q1, 2023, Nordea had 92% of its commercial real estate exposure with low probability of default with only 2% towards high risk. The quarterly impairments have remained stable since the early 2021 at an average impairment rate of 40 bp and the corresponding coverage ratios above 50%. This is mainly explained by the following facts (CRE portfolio characteristics):

- Total average LTV ~53%.

- Average interest rate coverage ratio (ICR) at 5.3x (which is extremely solid)

- Low vacancy rates with an average letting ratio of 93.5%.

- Portfolio mainly comprised of central and class A office and residential buildings.

Moreover, the fact that Nordea has remained consistent in the commercial real estate lending activity (unchanged quarterly lending amount of ~ $32 billion since Q1, 2022) is a clear testament to its defensive customer base and the overall Nordic economic resiliency.

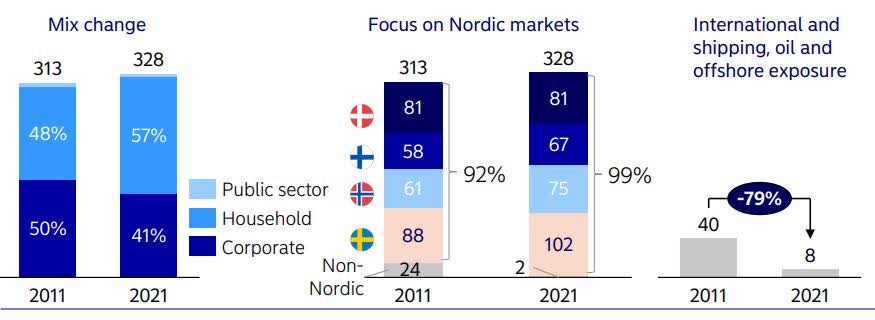

#3 The de-risking policy assumed back in 2011 paves the way for continued stability in the future

Since 2011, Nordea has devised a bold strategy to significantly de-risk its business operations and decrease the level of risky exposures in its loan book.

{kind=link}

In the most recent capital markets day event, Nordea outlined the progress. As we saw above, the actions are already bearing fruit.

In the last decade, Nordea has managed to reduce its exposure to Nordic corporates and instead increased focus on the resilient Nordic households and ultra-safe Government bodies.

It also exited Baltic markets, which tend to be very volatile during times of distress.

Similarly, Nordea has shrunk its risky international shipping and oil exploration loan book by roughly $34 billion.

As a result of all this and great Nordic economies, Nordea was the first bank in the European Union that received a green light from the ECB to embark on a share buyback program post COVID-19.

Finally, the underlying resiliency of Nordea is also confirmed by the fact that in the past decade it has exhibited significantly lower profit volatility than other 30 comparable EU peers.

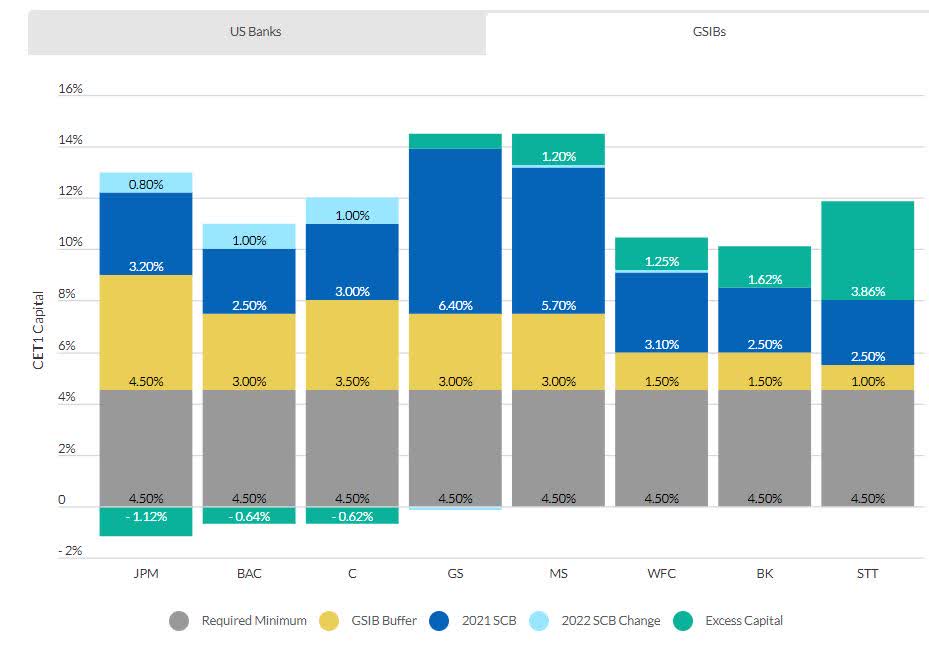

#4 Nordea's CET 1 capital ratio adds a cherry on the top

Although Nordea operates in four markets at a similar scale, where each country has its own central bank, it is supervised by the ECB because its headquarters are placed in the Finland, Helsinki (euro economy).

The minimum CET 1 (common equity tier 1 capital) capital ratio is set at 4.5%. And as of Q1, 2023 Nordea had it at 13.5%.

{kind=link}

If we compare Nordea's CET 1 level to some similar U.S. banks that provide a diversified offering and are deemed of a systematic importance, we can see how safe the Company really is.

Relative to the 20 largest EU banks, Nordea's CET 1 ratio is precisely in line with the average .

Nevertheless, we have to keep in mind that most of the EU system-critical banks are overcapitalized and exhibit superb fundamentals.

Recent wobbles in US and European banking markets have been triggered by idiosyncratic issues at some institutions and broader uncertainty about the impact of central banks' monetary tightening. However, capital and liquidity levels of the banking industry in Europe continue to be very robust. In addition, asset quality and profitability are the strongest since the financial crisis 15 years ago.

Granted, not all what is in excess of the required minimum (CET 1 4.5%) can be deemed discretionary. It is not that the EU banks themselves have freely decided to carry so strong CET 1 ratios. For example, in Nordea's case there are extra mandatory layers that have to be complied with to strengthen the CET 1 (e.g., Pillar 2, counter-cyclical buffers).

With that being said, Nordea has still ~2% of excess capital, which currently stems from internal capital policy procedures. Looking at the chart above, we can see how unique this is.

#5 Improving cost-to-income ratio as one of the key sources for value-creation

In the recent capital markets day event, Nordea communicated its plans to reduce cost-to-income ratio mainly through digitalization activities. Since then, the macroeconomic backdrop has imposed serious headwinds for improving this metric. As we can see in the chart below, in 2022 Nordea experienced a slight uptick in the cost-to-income ratio despite its outlined strategy.

Nordea investor relations

However, the Q1, 2023 figures revealed positive surprise, indicating that the future trajectory of brining the costs down remains intact (and is fully doable).

In the recent quarterly report a ~5% improvement was registered compared to Q1, 2022 data. Relative to Q4, 2022, the progress continued (from 44% to 42%).

In a nutshell, Nordea has already over delivered on its 2025 objective to bring down the cost-to-income ratio in the 45-47% territory.

The exceptional results are mainly attributable to the increased profitability associated with higher interest rate environment (i.e., revenues growing faster than costs) and solid performance on the cost control side.

Compared to the U.S. banks, which on average carry a cost-to-income ratio of 60%, Nordea seems to be considerably more efficient.

Also, in the context of EU and Nordic peers ( cost-to-income ratios of 62% and 55%, respectively), Nordea is a clear leader.

#6 Higher-for-longer scenario benefiting Nordea's profitability

All four Nordic (including EU) central banks have embarked on a restrictive monetary policy approach just as the FED. The rate of change and the magnitude of the rate hikes have been consistent among the central banks.

Nordea investor relations

The higher interest rate environment has allowed Nordea to boost the net interest income in a significant fashion. Nordea has estimated that each 50 basis point hike translates to an incremental gain of ~$350 million in net interest income. Couple of past quarterly figures confirm that this is the case in practice as well.

Currently, the consensus estimates signal one or two additional rate hikes depending on the country. At the same time, the base case seems to be a higher-for-longer scenario for the entire 2024.

All this bodes well for further growth in the net interest income component, which, in turn, should introduce tailwinds for achieving targets on the cost-to-income ratio.

Catalyst for further outperformance

All of the 6 aforementioned aspects provide a solid base of information pertaining to the Nordea's financial strength, competitive advantage and secular tailwinds that are relevant for a long-term growth.

However, this information is most probably not sufficient to answer whether by investing in Nordea there will be an alpha or not.

Why probably? Well, since Nordea is an EU-based bank with relatively low market cap compared to the U.S. largest banking actors, and not part of the major U.S. equity and / or bank indices, there is a probability that Company has just fallen under the radar of most (and largest) financial market participants.

In this case I do not see any event that could suddenly direct incremental flows of capital towards Nordea's stock and thus levelling the currently undervalued business (see more details below).

Yet, assuming all else remaining constant (ceteris paribus), investors should feel comfortable about receiving a 10% return per year. This comes from extremely stable dividend yield of 8.2% that is underpinned by healthy ~65% payout ratio and all of the fundamental outlined above. The extra ~2% return should come from the buyback programs, which Nordea has historically utilized to avoid overcapitalization. For instance, the current buyback program for 2023 implies a 1.89% yield based on the current market capitalization level.

Against the backdrop of structurally safe markets, rewarding efficiency measures and favourable interest rate dynamics, we should expect a continued earnings growth. Also, the consensus estimates indicate a 29.3% improvement in the 2023 EPS figure, followed by more moderate uptick of 2.9% in 2024.

From this we can safely conclude the following:

- Nordea is set to deliver strong earnings growth in the foreseeable future.

- In the long-term the odds are stacked in favour of Nordea's ability to deliver growing EPS.

- This, in turn, implies that ~8% dividend yield is extremely safe and predictable.

- Lastly, it also means that the share buybacks will present and most probability at a significantly higher magnitude, thereby providing extra yield on top of the secure 8% dividend.

Now, in my humble opinion, there is a notable catalyst, which should warrant higher returns that just ~10% stemming from the predictable shareholder yield (i.e., dividend plus buyback yield).

It is a question of Nordea's valuation and its convergence to a more reasonable level.

Currently, Nordea trades at the following multiples :

- TTM price to book at 1.25x (1.02x at FWD basis)

- TTM price to earnings at 8.16x (7.01x at FWD basis)

On a TTM P/E basis, this is implies at 33% and 41% discount from 3-year and 5-year average, respectively.

Compared with the Nordic peers, the TTM P/E discount lands at ~10% (selected peer mix / Nordic comparables: Swedbank AB (SWDBY), SEB SA (SEBYF), Danske Bank A/S (DNSKF), Sampo (SAXPF) and SpareBank 1 Nord-Norge (SPXXF))

Norde is underpriced even compared to the sector median valuations of U.S. banks, which certainly do not enjoy the same level of momentum and structural tailwinds (e.g., low public debt, financially resilient corporates, structurally secure households etc.).

Here the discounts in terms of the TTM P/E and TTM P/B are ~12% and ~2%, respectively.

I think that given how strong the Nordea's markets and how resilient the Company is with a huge EPS growth momentum, it is only a matter of time until the current valuations converge to at least EU sector average. Plus, I see no reason why Nordea should trade below its 3-year or 5-year average, which includes periods of lower interest rate environment, where it was very difficult for banks to increase profits. At those historical times, Nordea was a bit more risky business due to its exposure to Baltic markets and international shipping and oil exploration companies.

In my opinion, the market should reprice Nordea once it delivers the next quarterly figures, which have every reason to land in line with the market's expectations (especially, considering the recently communicated rate hikes by the ECB).

From this, investors should expect additional capital gains of ~10% and gradually up to ~30% to revert back to the historical average (all this is in addition to the juicy yield).

Three key risks and their mitigants

There are some theoretical risk that could potentially put a drag on the bull thesis.

- Inverted yield curve. All of the Nordic (and the EU) central banks suffer from the inverted yield curve problem, where the front-end of the curve is steeper than that of the long-end. In theory, this should harm banks' profits due to a classical business model of "borrow short (cheap), lend long (expensive)". This is largely irrelevant for Nordea since the lion's share of its loan book is comprised of floating loans - a Nordic and EU-specific approach by the banks. Plus, Nordea does not utilize any long-term hedges and it does not rely on significant future rollover strategies as most of the fixed rate loans are bound by the 5-year financing horizon.

- More restrictive policy stance by the central banks on the CET 1 ratios. An uptick in the CET 1 buffer decreases the profitability as banks are forced to hold more capital in the balance sheet. In the COVID-19 era and most recently once the surging inflation emerged, the policy makers have requested higher CET 1 buffers (i.e., countercyclical buffers). I find it extremely unlikely that there will be more restrictive actions given how well capitalized the Nordic and EU banks are. If anything, we could expect a gradual normalization in the required CET 1 levels, which, in turn, should provide an extra stimulus for continued outperformance. In the worst case, Nordea could sacrifice its internal capital allocation policy to avoid even deeper overcapitalization.

- Weakening economy. As mentioned above, Nordea is heavily exposed to the systematic risk in the Nordic region. If the Nordic economies start to fall and experience a notable slowdown in business activity and where households suffer from major erosion in their disposable income, Nordea might suffer badly. Yet, there are several counter arguments for this. First, none of the Nordic countries exhibit a major slowdown in the business (and lending) activity with an exception of CRE market, which is well-managed by Nordea. Second, government debt levels are still extremely low, which could be put at work to ride the economy out of the recessionary environment and help households avoid financial distress. Third, Nordea itself is a very safe bank due to the aforementioned reasons.

The bottom line

Nordea is a financially sound bank that is placed in markets, which provide the necessary secular tailwinds for continued long-term growth in a low volatile manner (due to inherently resilient households, public sector and corporates).

The higher-for-longer scenario introduces an additional support factor for Nordea's earnings growth - on top of the successful measures in the cost-to-income ratio front.

However, it seems that the market has not appreciated these dynamics, and has done the opposite - i.e., assigned greater discount factors than in the past, before the higher interest rate environment, which made it more challenging for Nordea to generate incremental profits. Nordea trades at a discount to its closest Nordic peers, the U.S. comparables and its 3-year, 5-year historical averages.

In my humble opinion, Nordea has all the reasons to experience a gradual convergence to more reasonable valuations that are more in line with either its peers or its historical average.

As a result, my base case is ~30% return stemming from stock price appreciation and additional 10% return coming from stable shareholder yield (8% dividend and 2% buybacks). As you know, when dealing with markets it is extremely difficult to make any assumptions on the timing of the potential gains. But I am expecting to capture these returns in the 2023.

For further details see:

Nordea Bank: 8.2% Yielding Bank That Has Fallen Under Radar